Last version published: 15/09/2020 07:23

Publication number: ELQ-98296-2

View all versions & Certificate

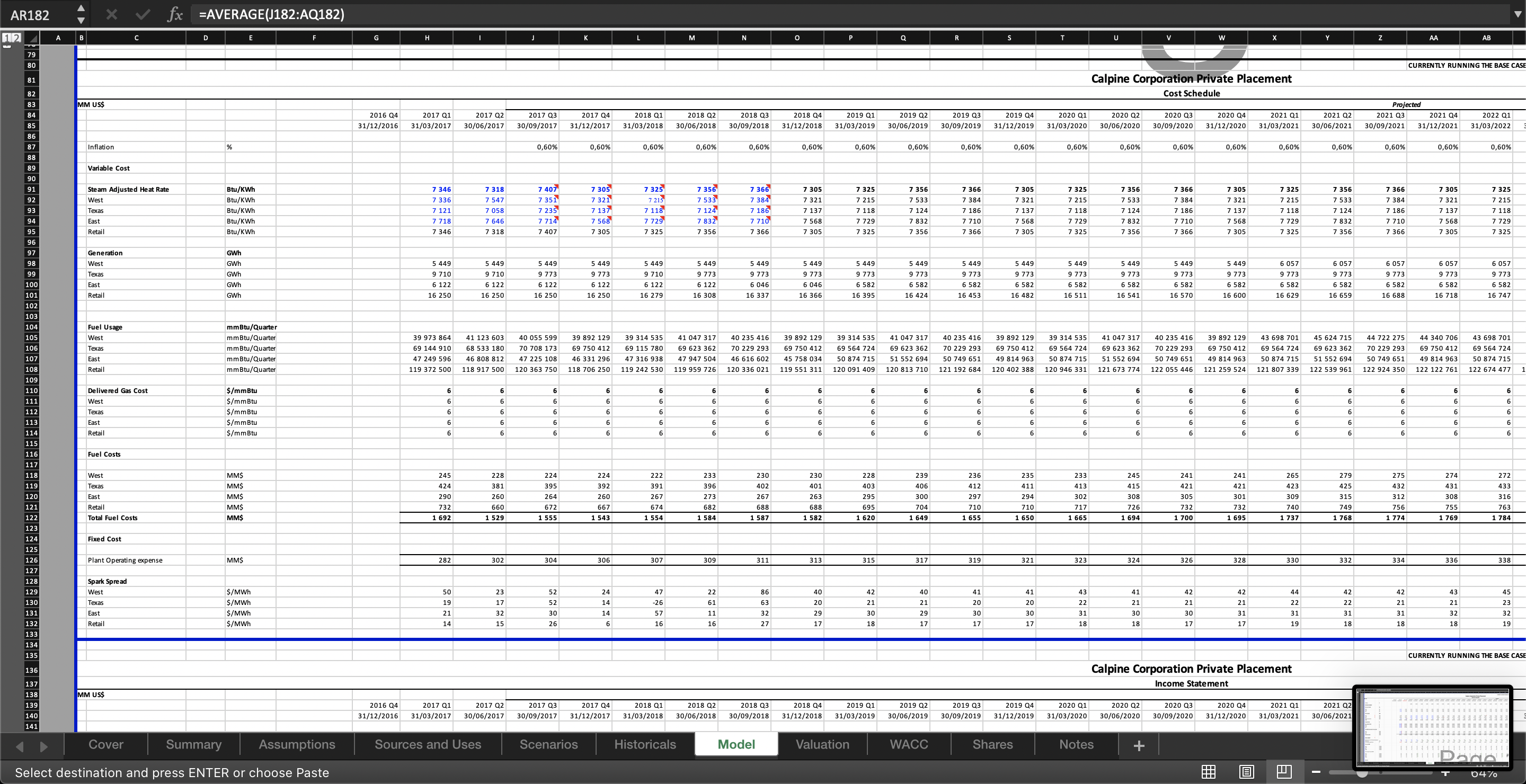

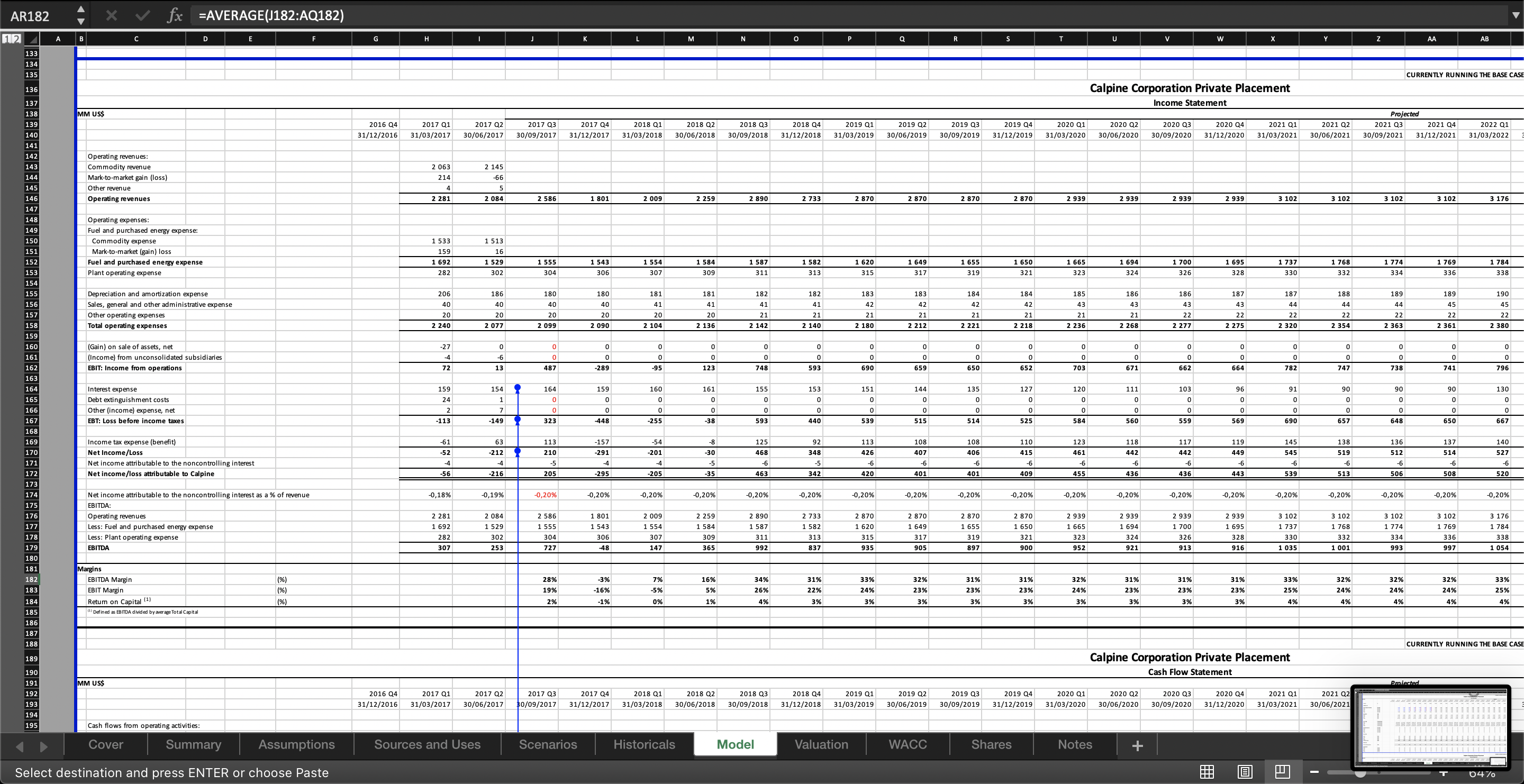

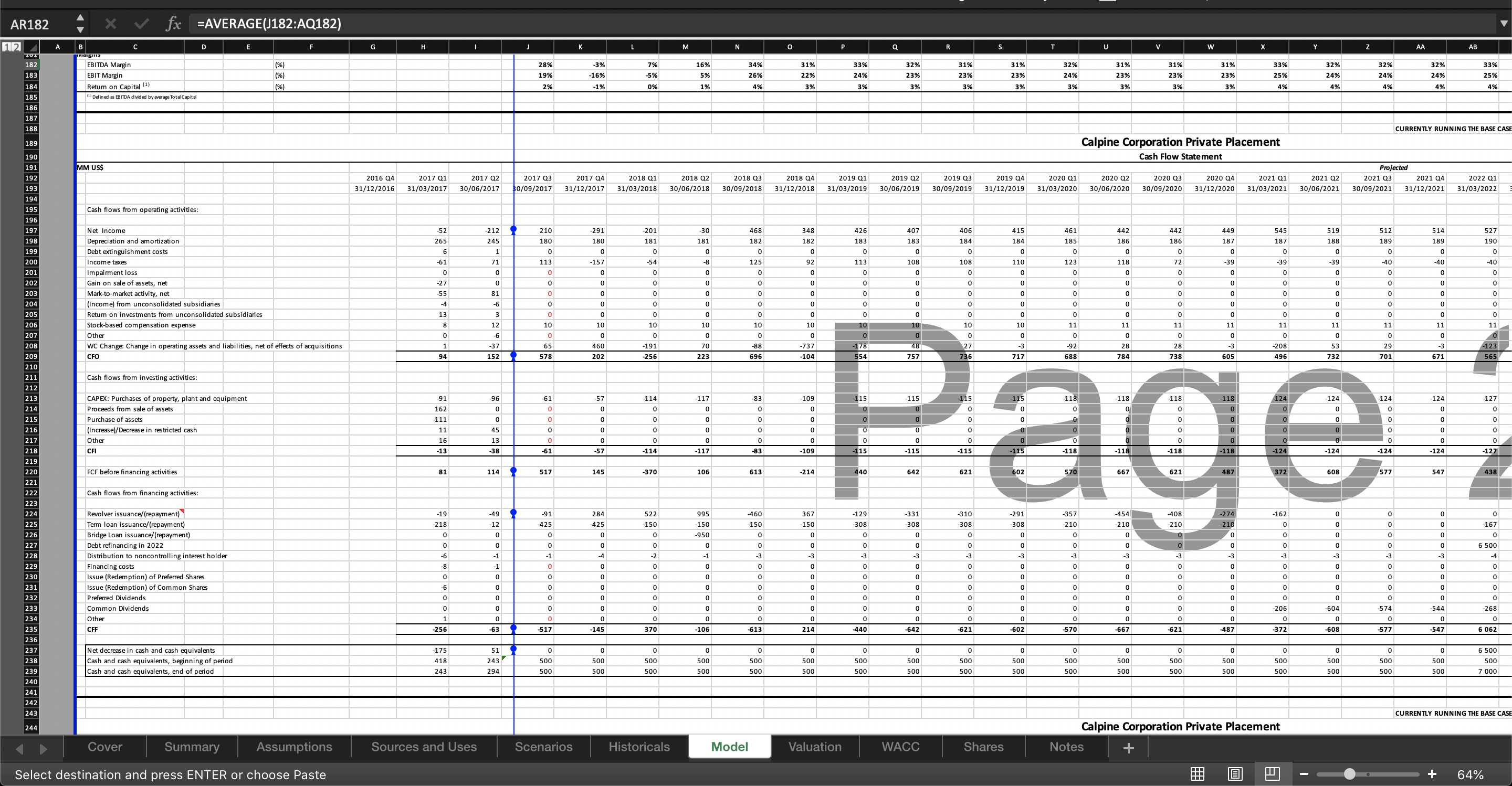

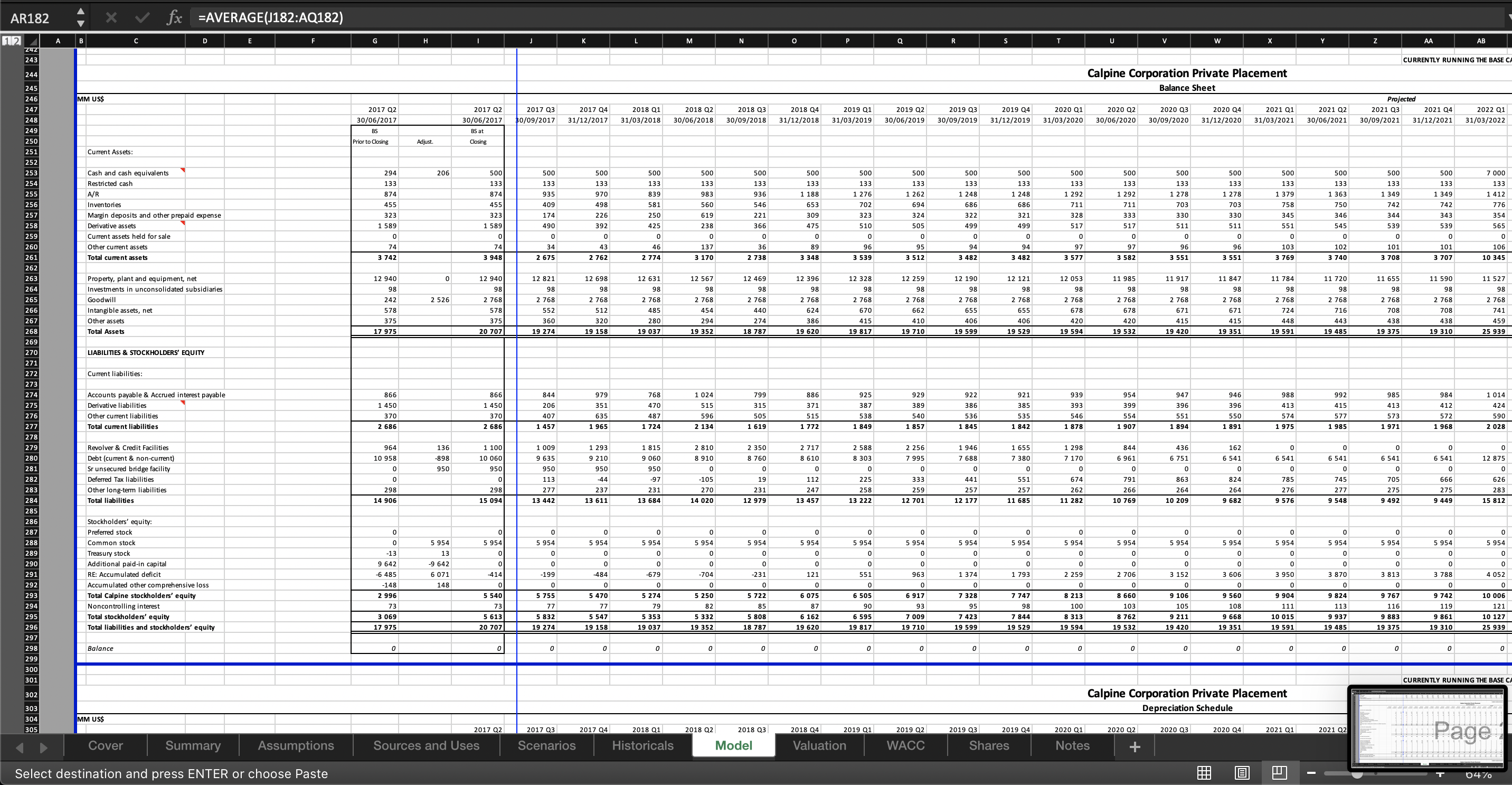

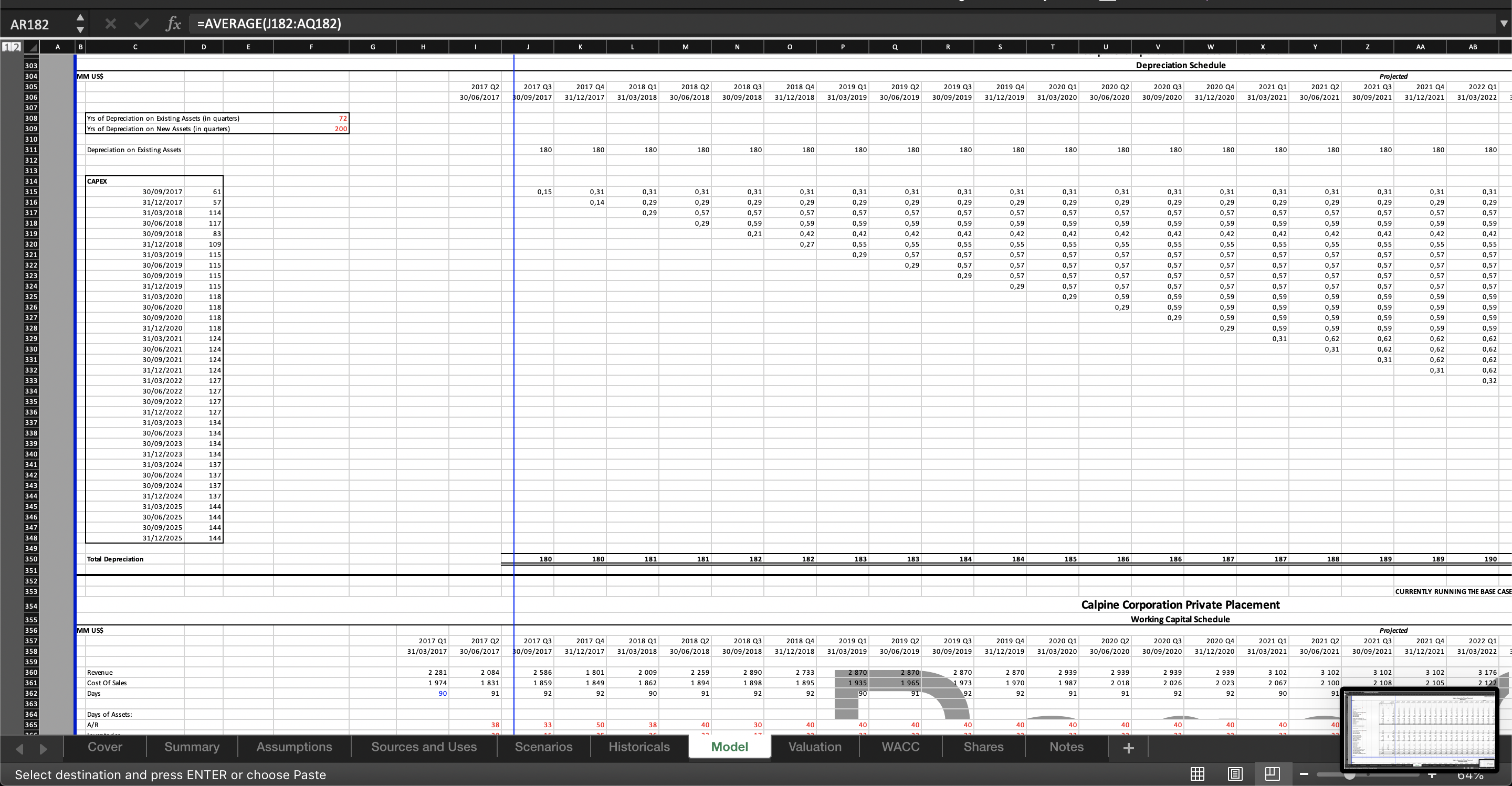

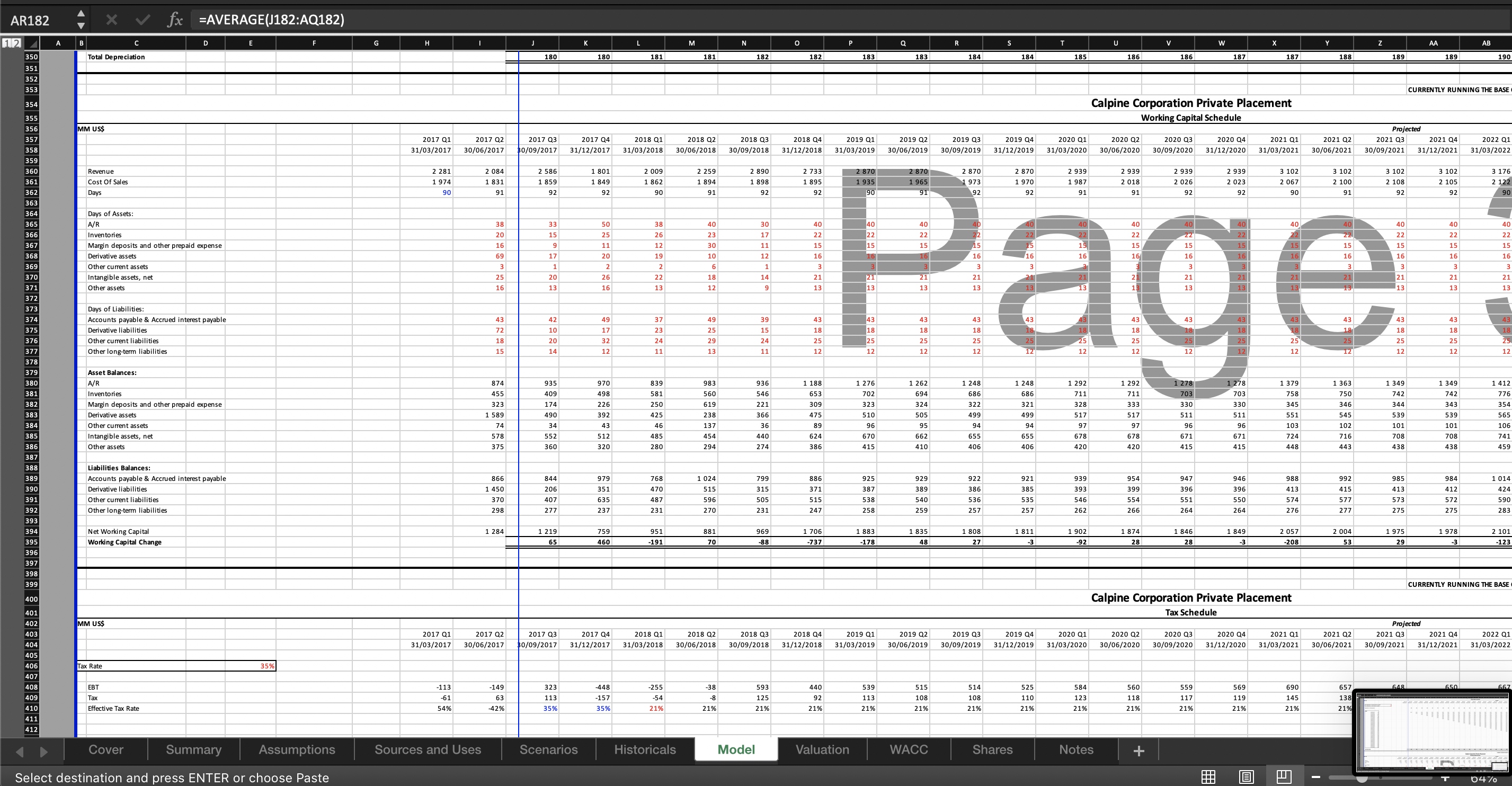

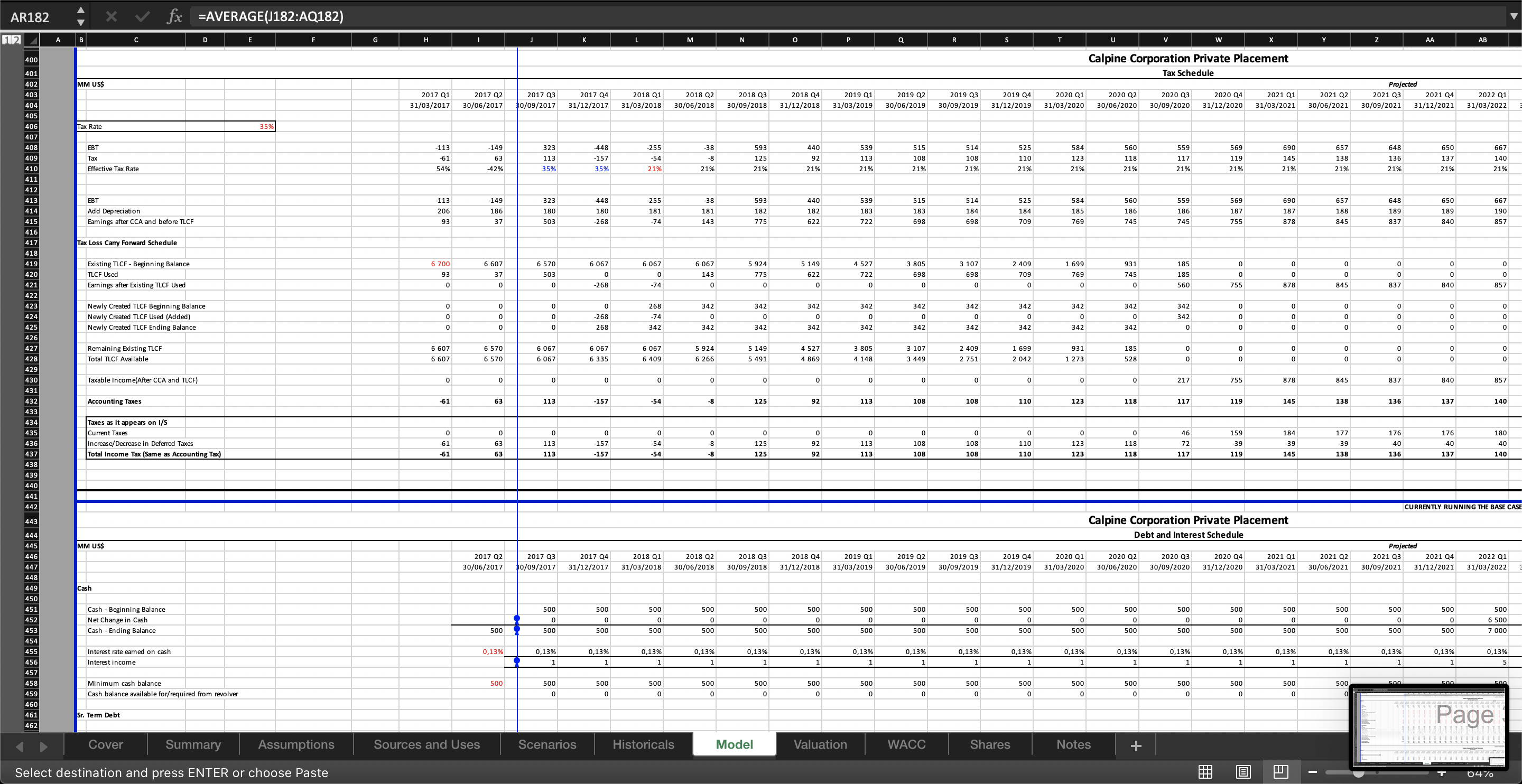

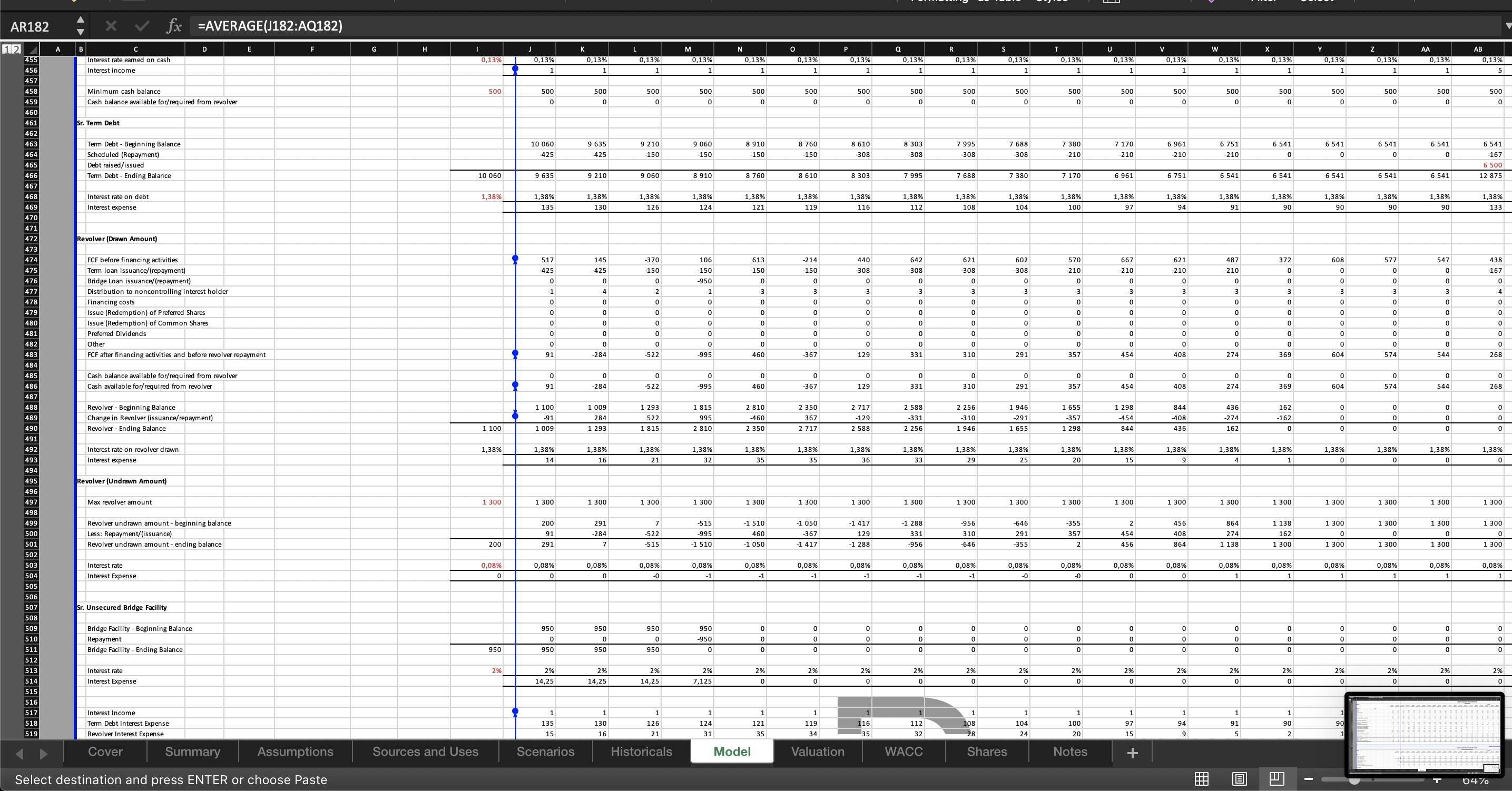

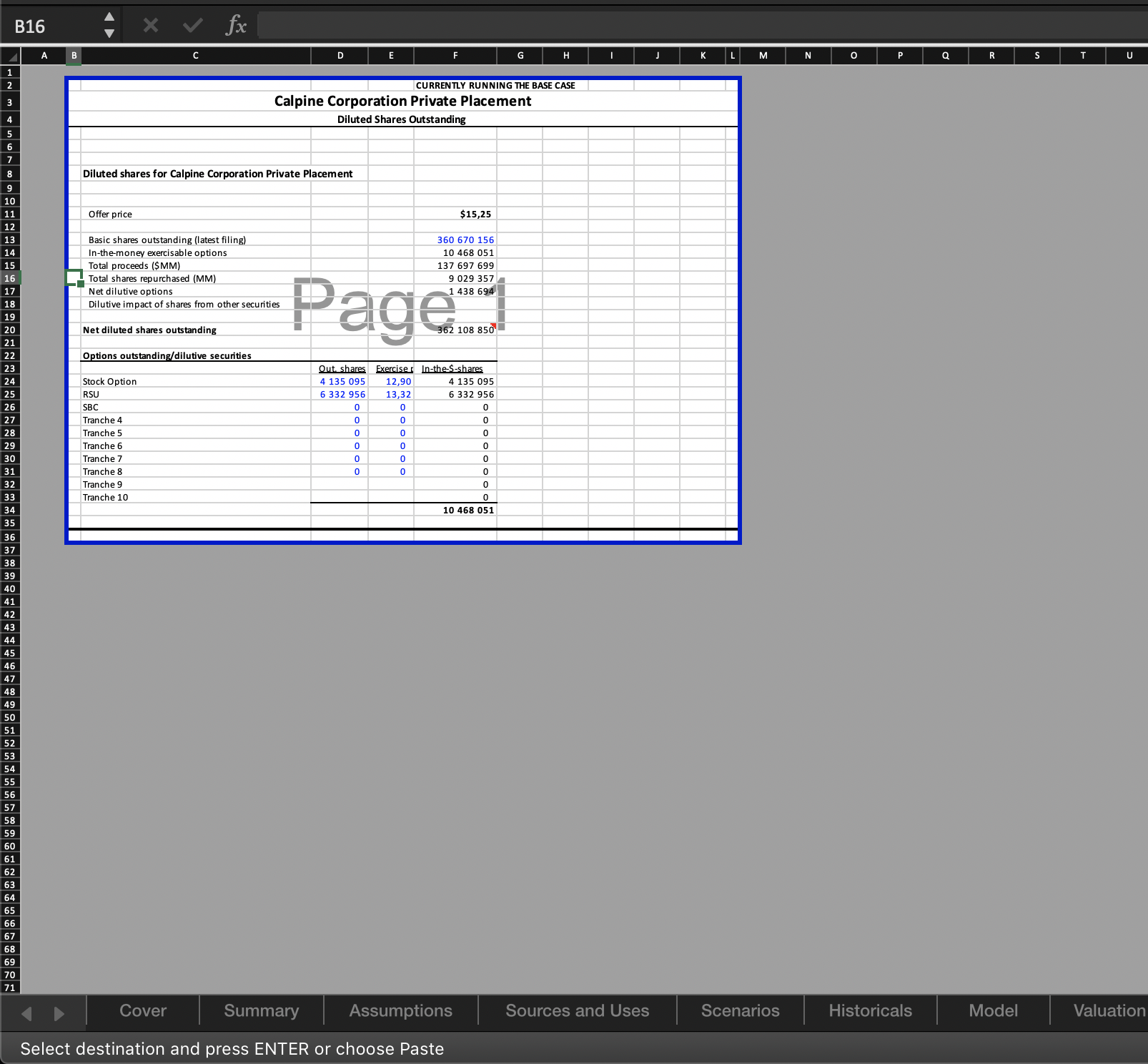

Independent Power Producer (IPP) Private Placement Financial Model

A financial model of a North American independent power producer private placement by a consortium of investors

Further information

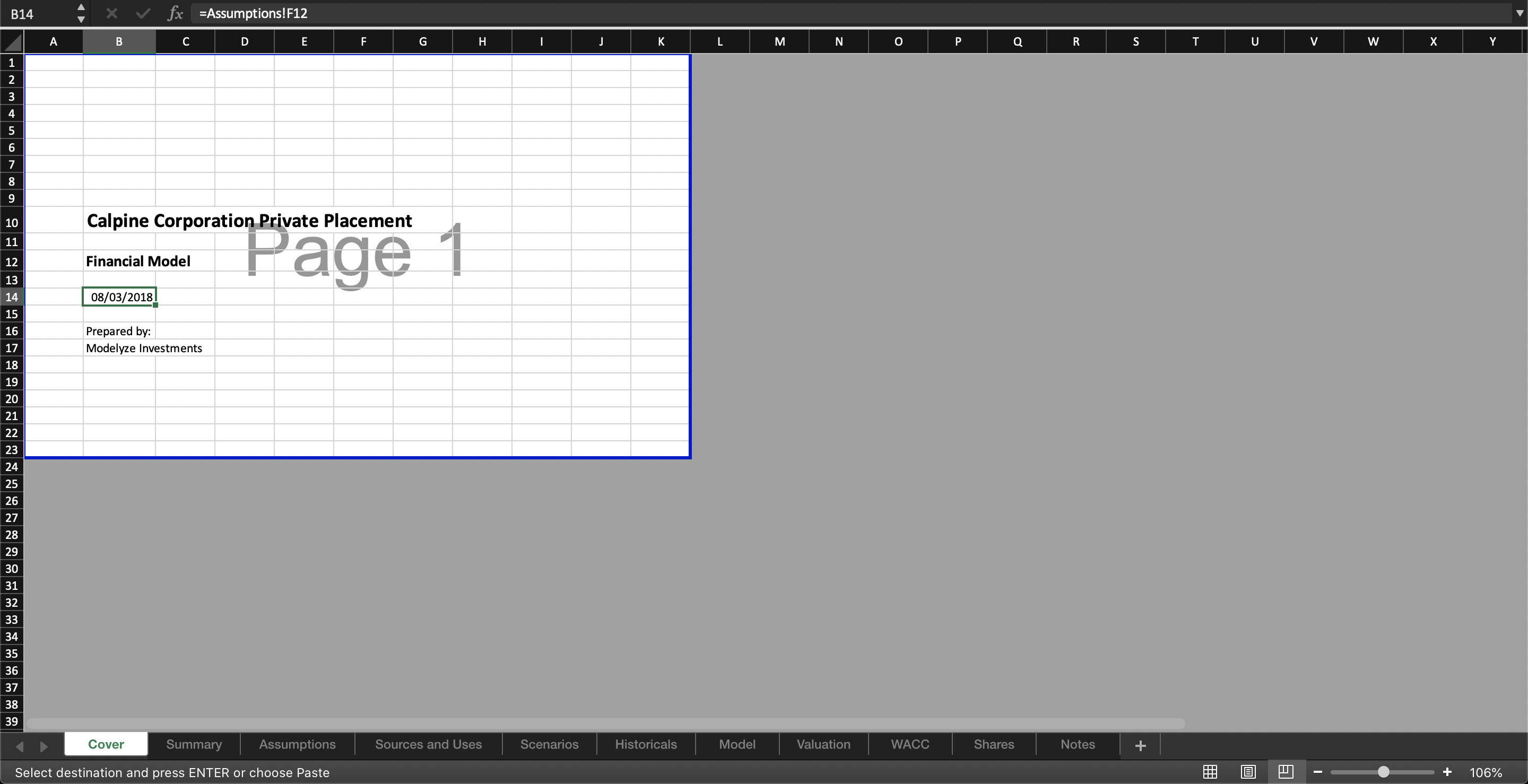

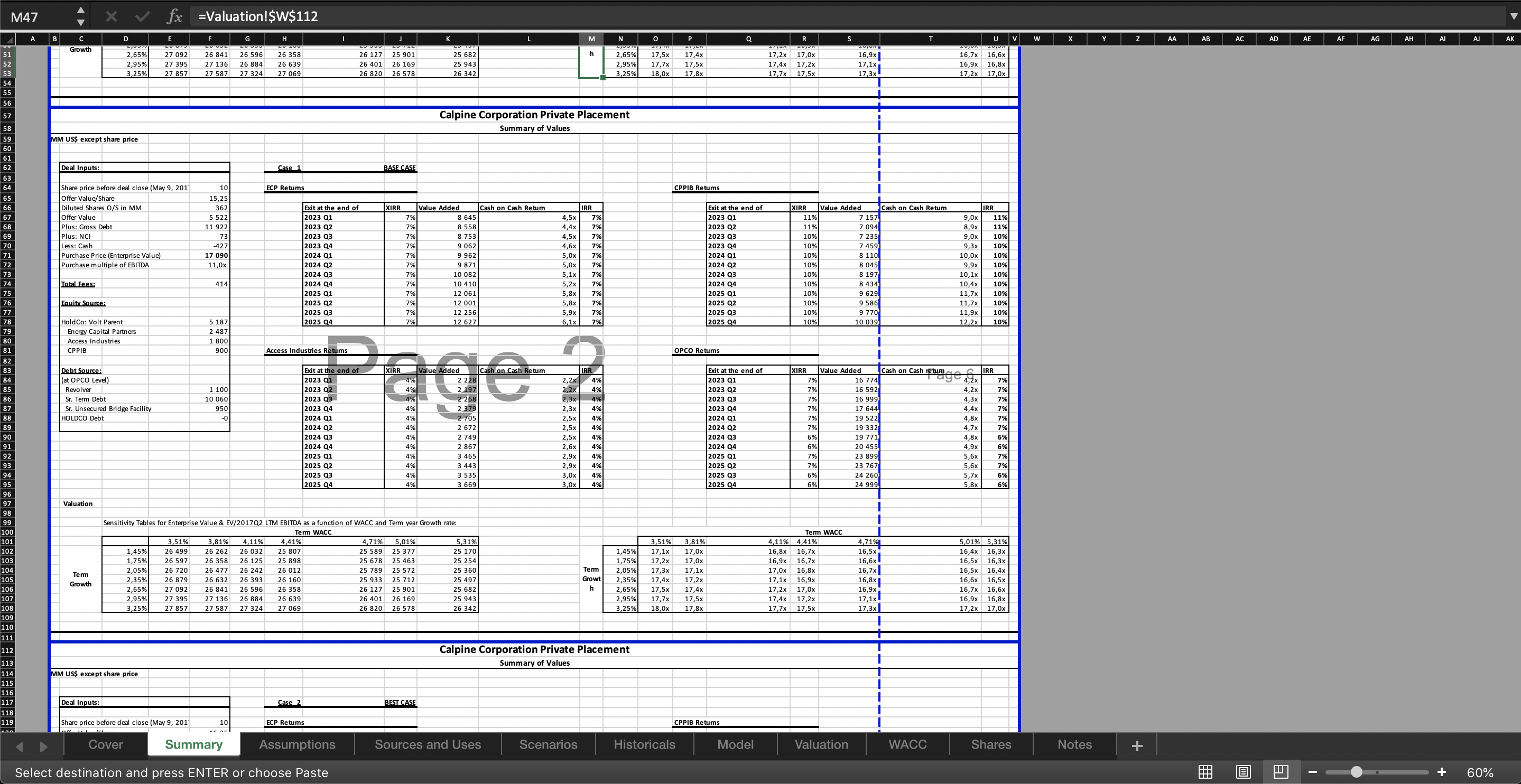

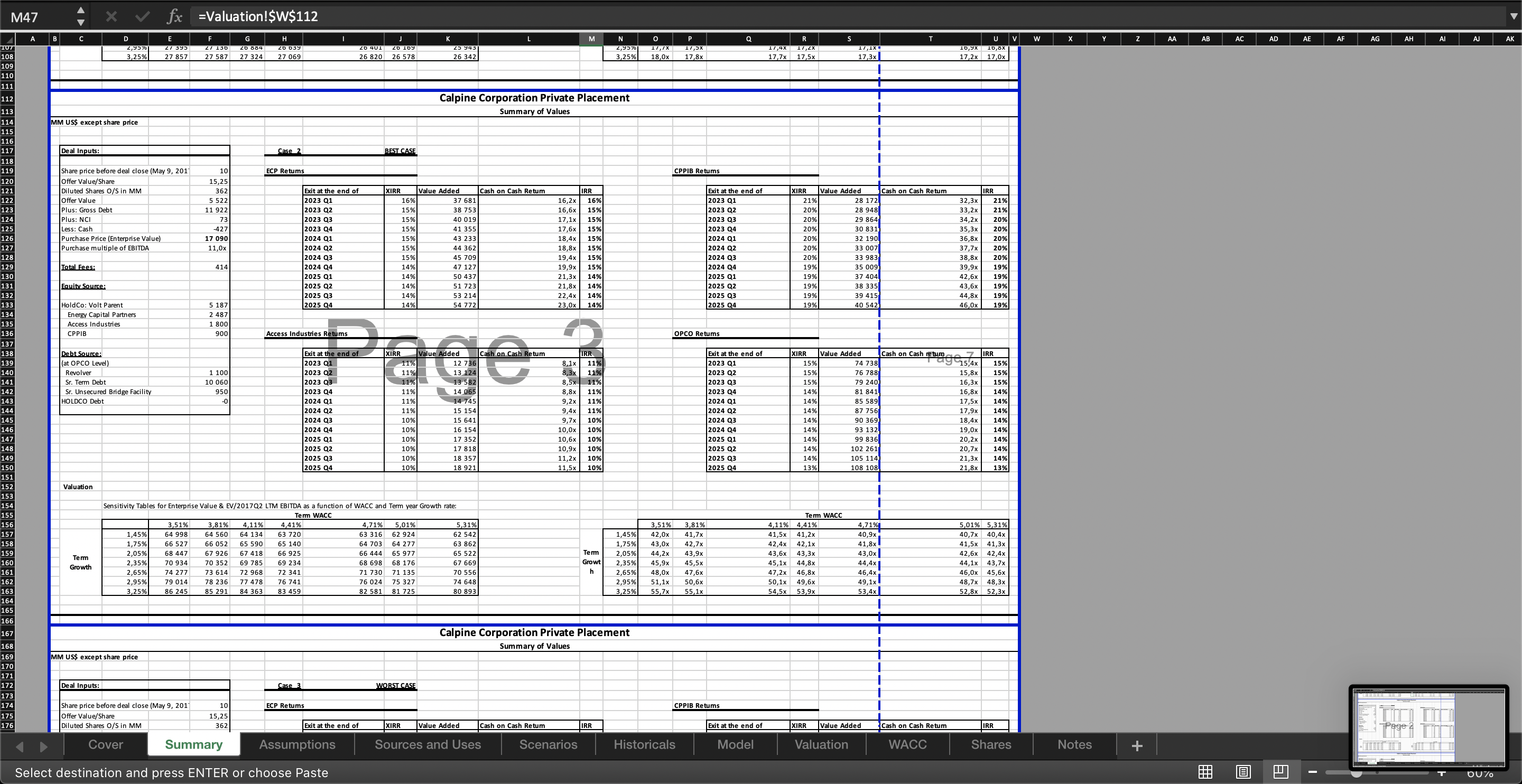

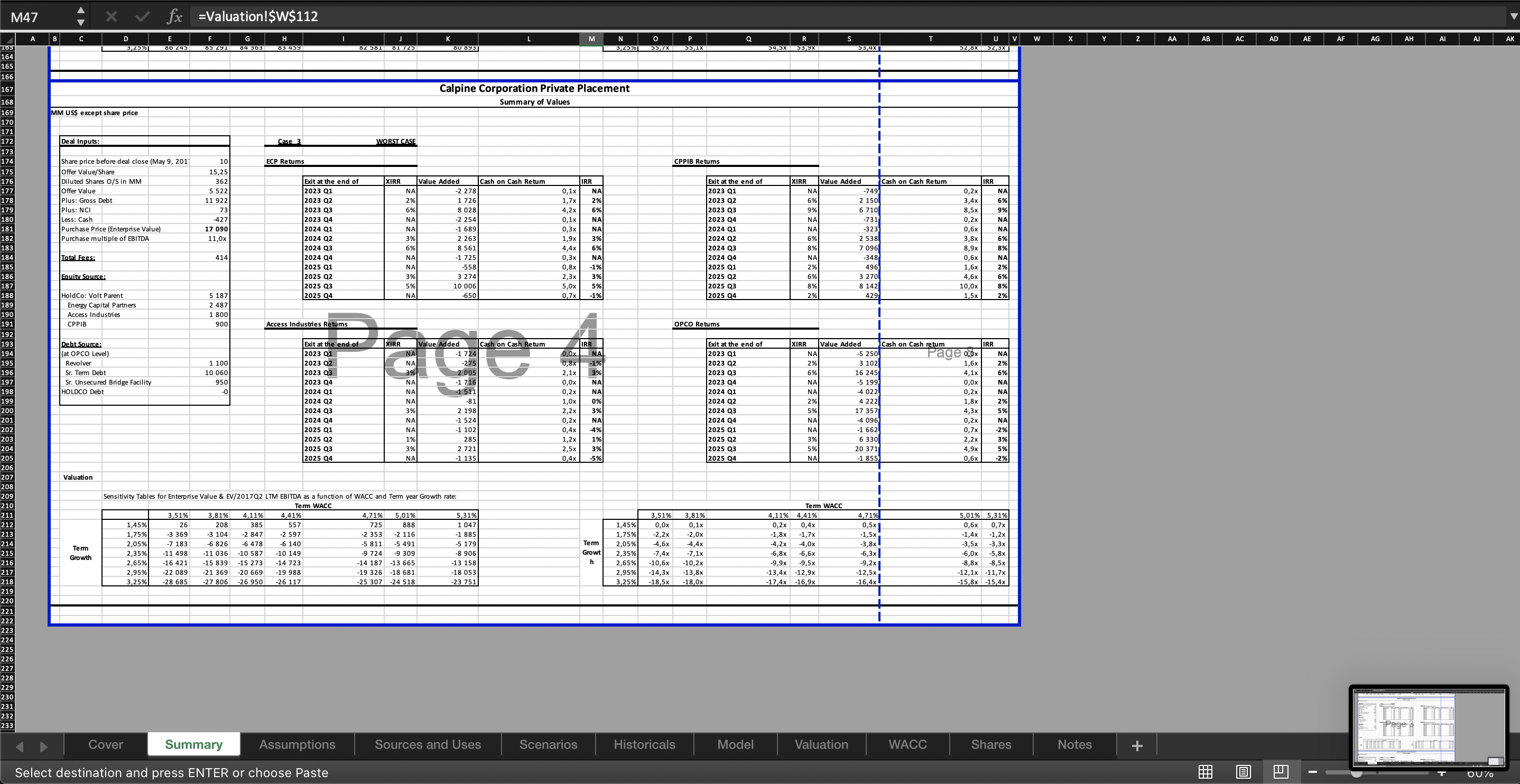

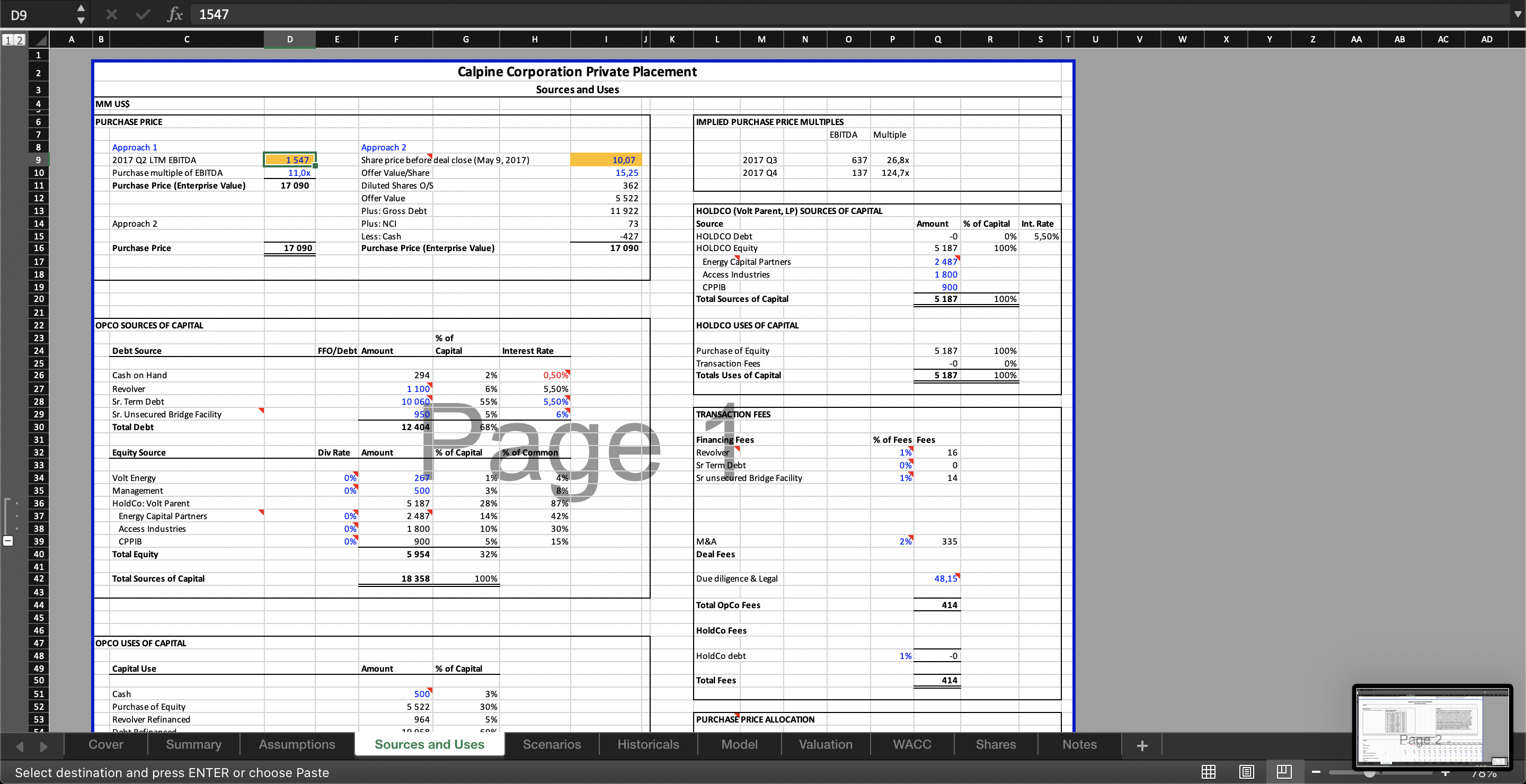

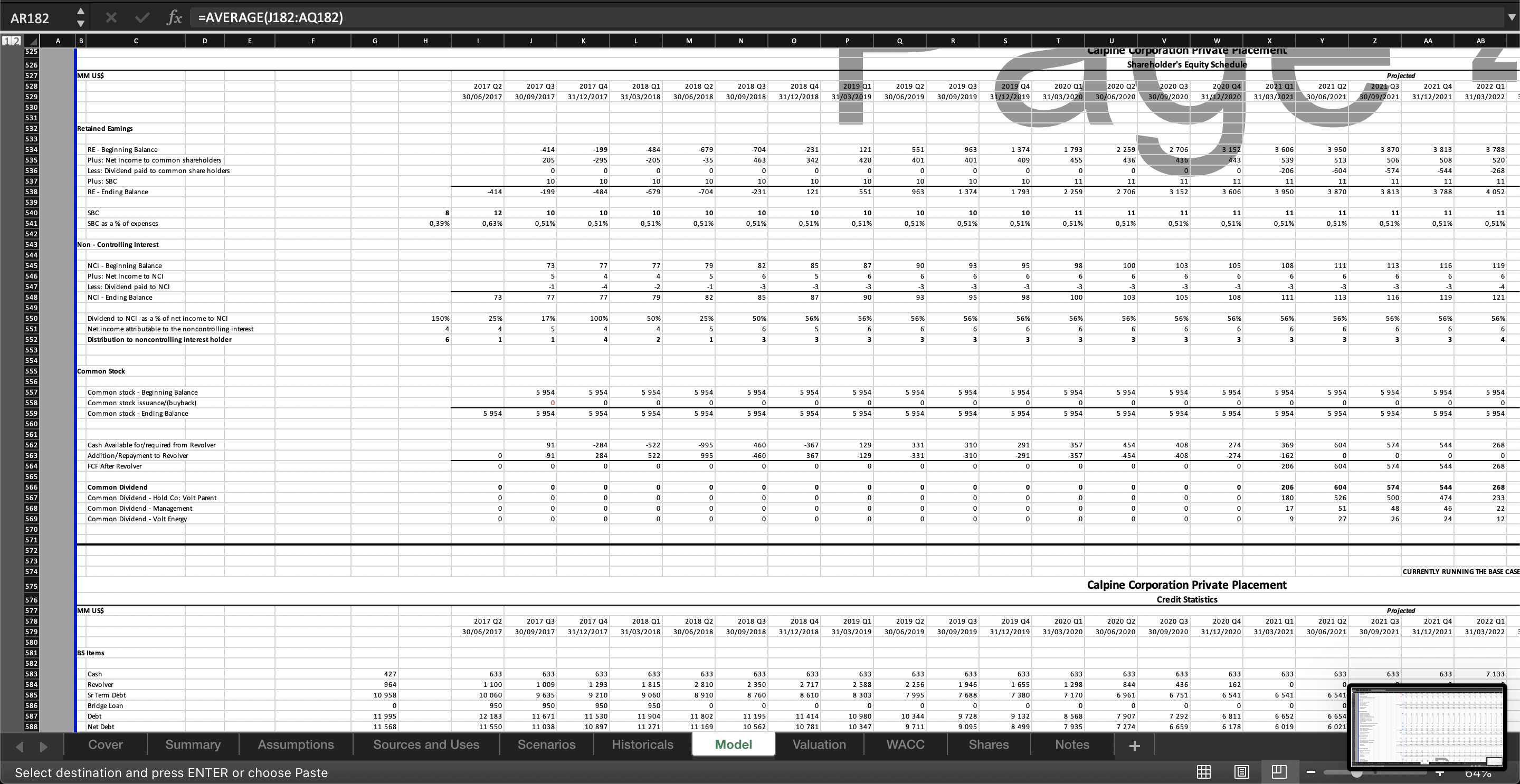

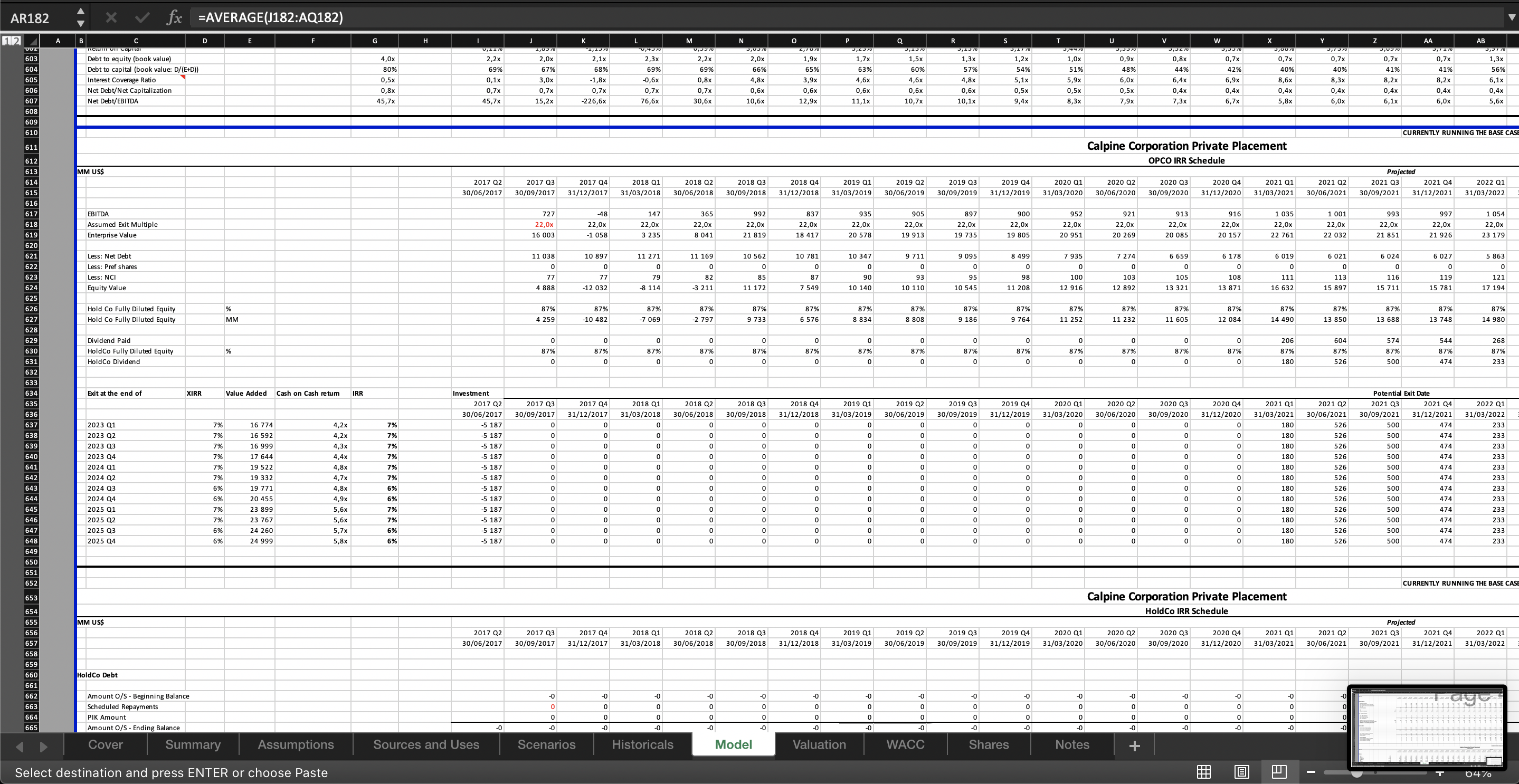

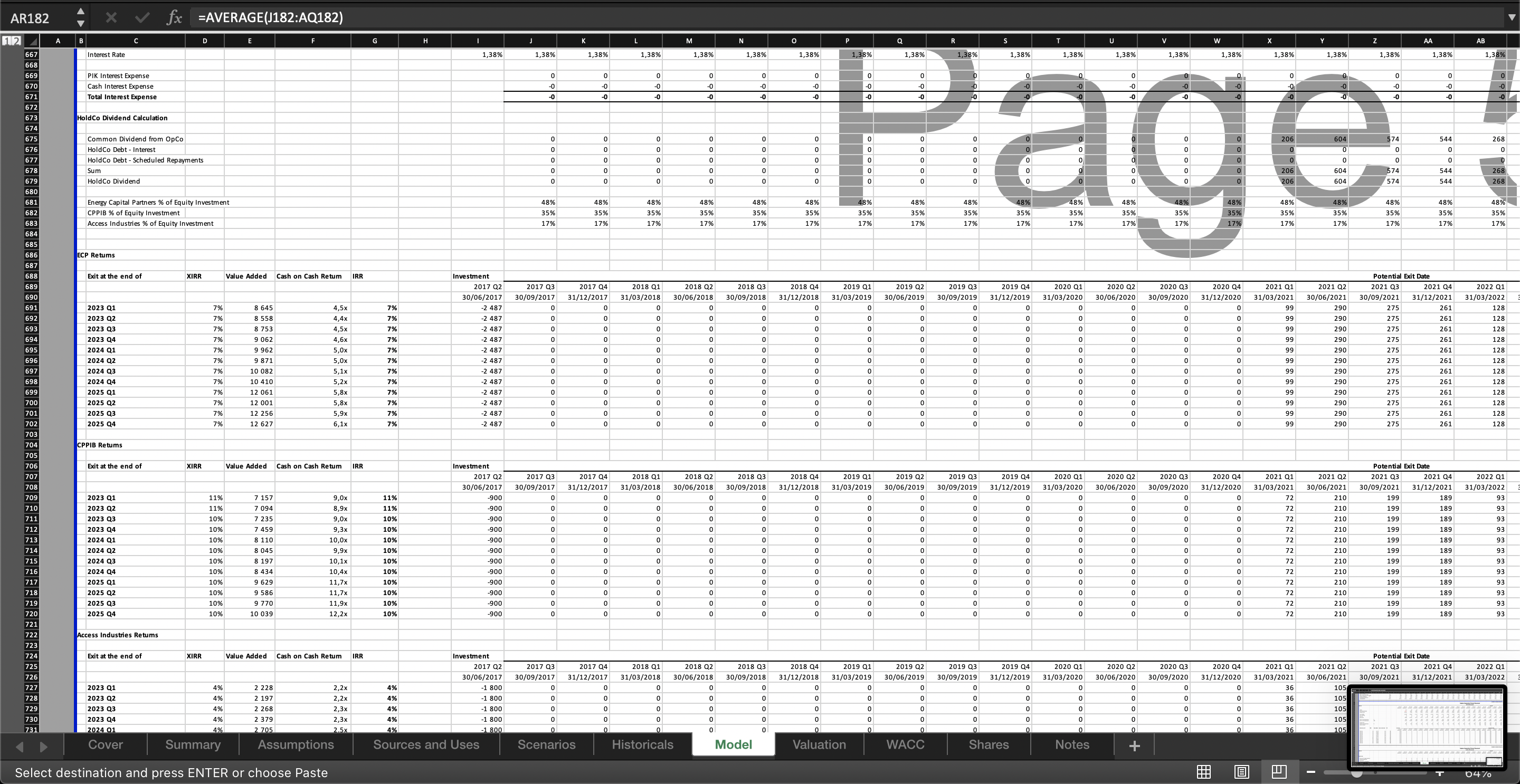

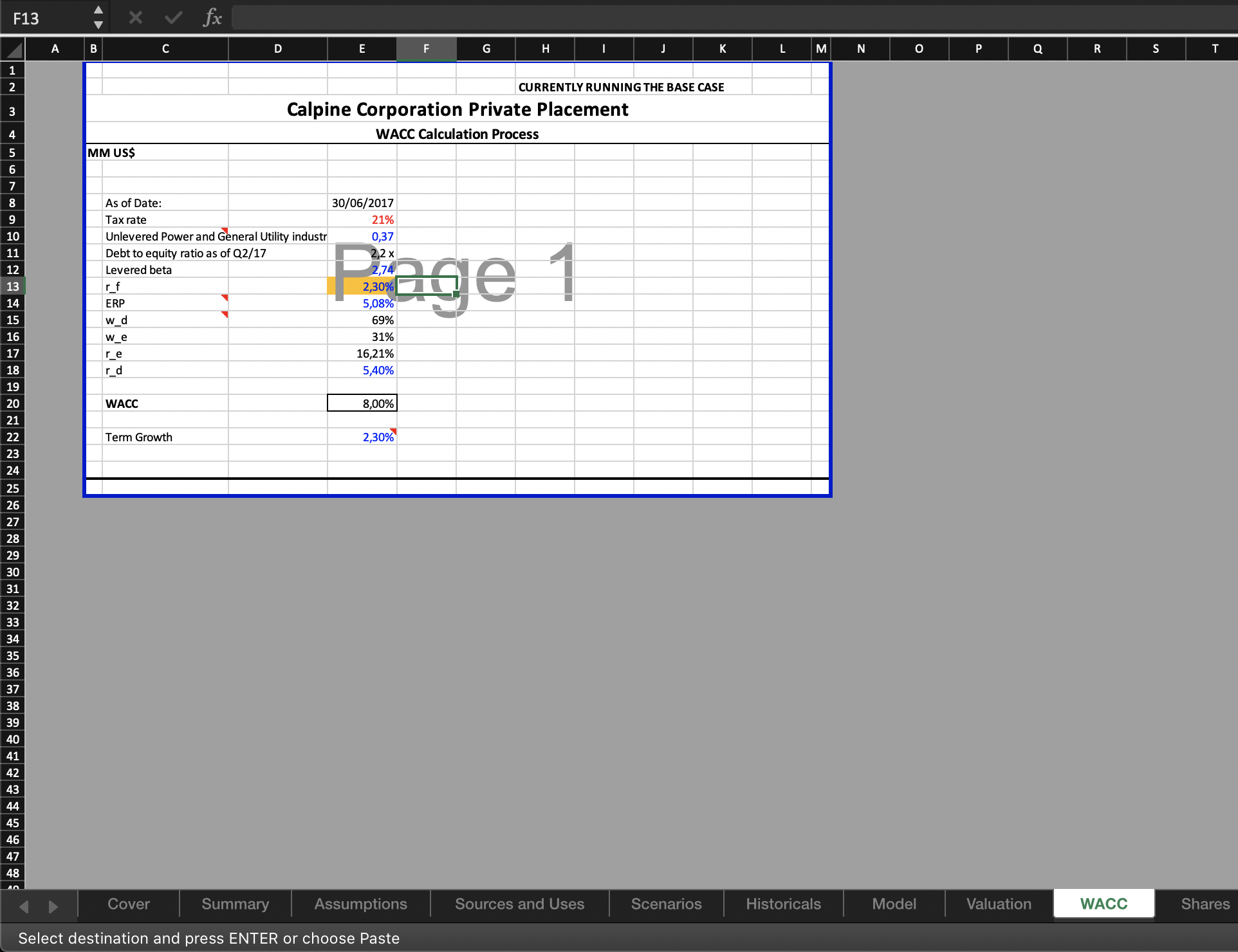

A financial model of a North American independent power producer private placement by a consortium of investors including Energy Capital Partners, Access Industries and CPPIB. The company has been struggling for two years prior to the take private given the shifting dynamic of renewable energy industry with share prices declining by 60%. The deal is a cash deal financed by mostly sponsor’s equity as well as debt, and structured as a stock sale. The model is ideal for investment banking, equity research, power and utility and private equity finance professionals, valuation and transaction experts.

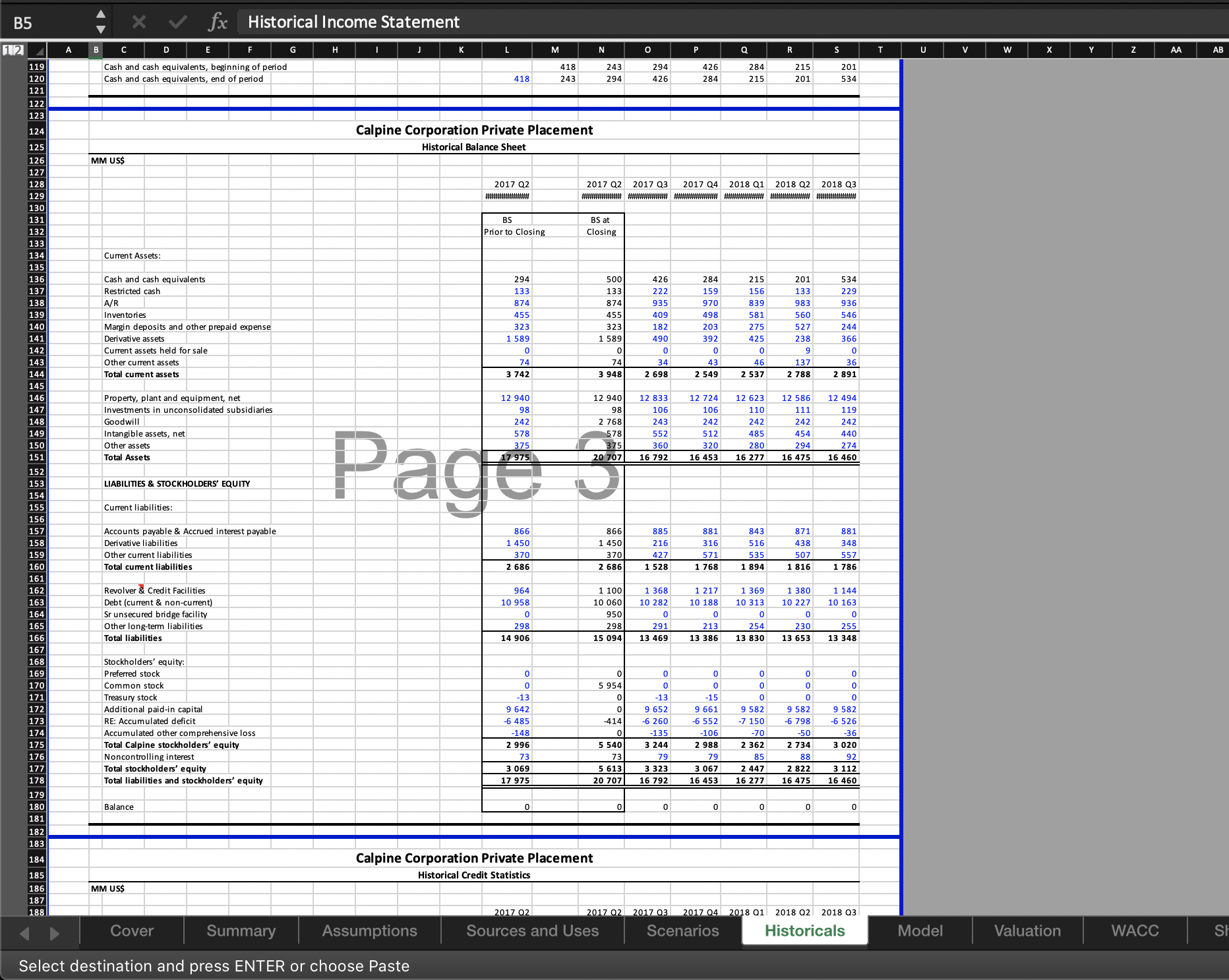

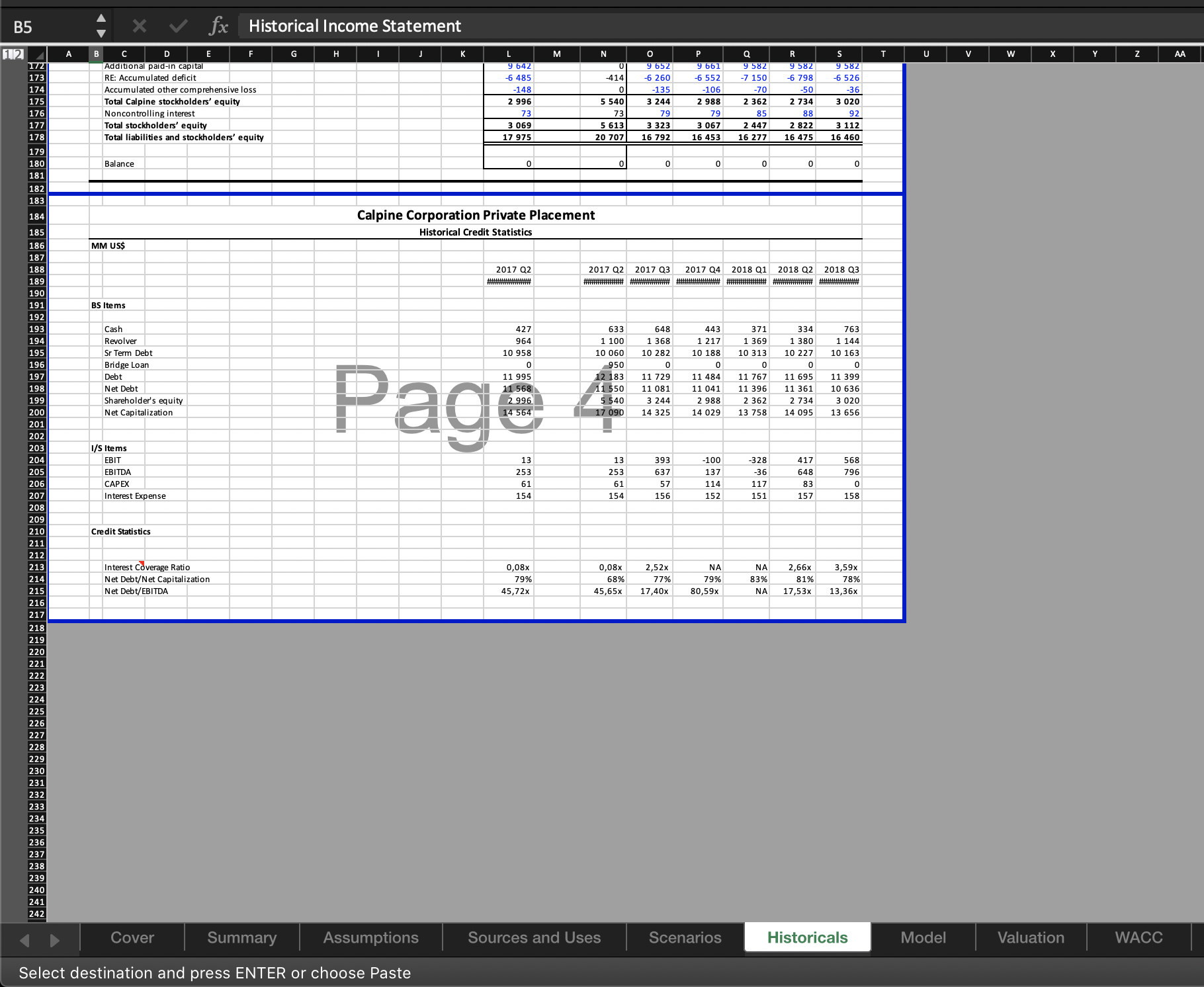

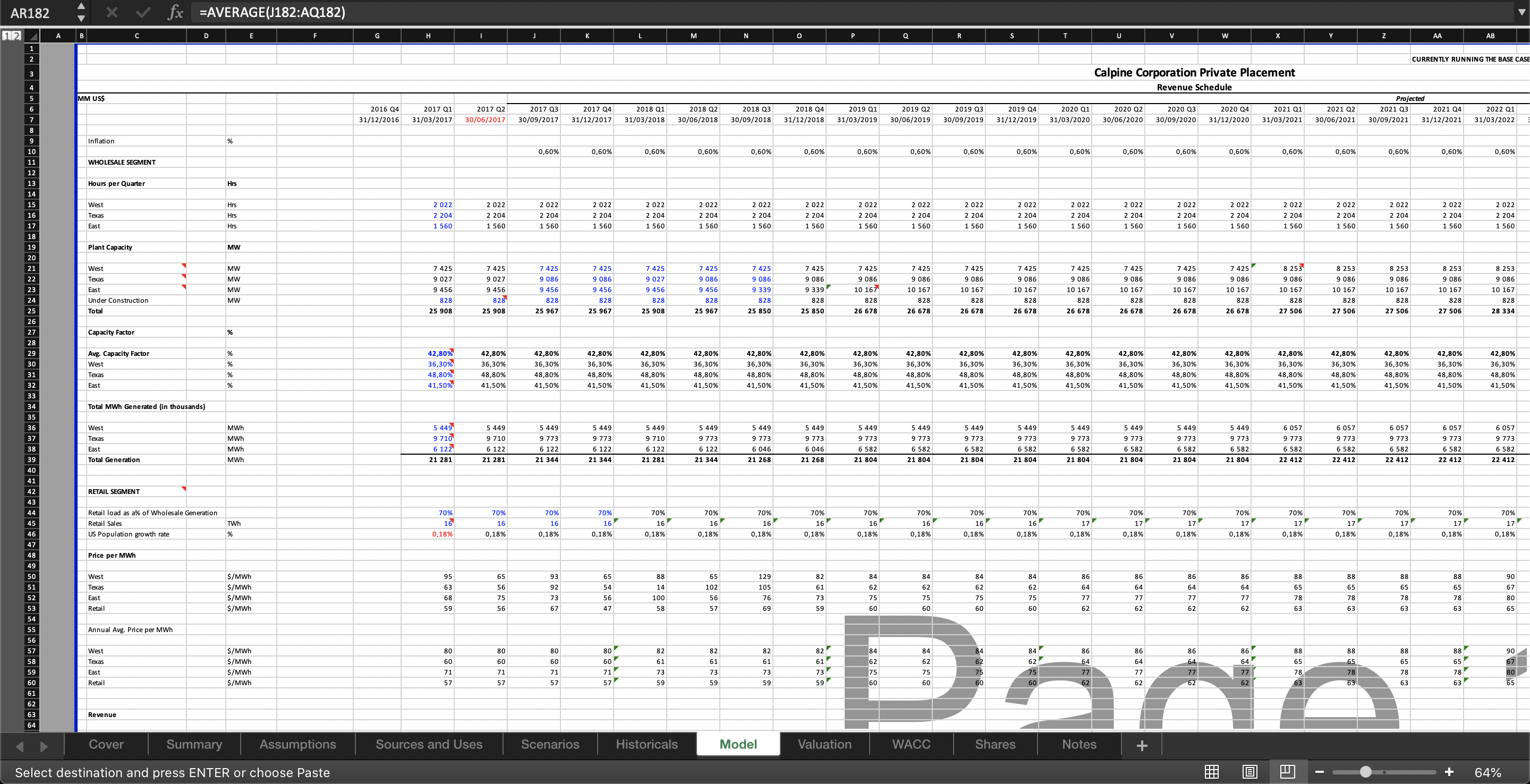

- This financial model is a circular, 3-statement model along with a comprehensive leverage buyout model with many other features explained in the product description. Please ensure prior to opening the excel sheet, iterative calculations within the excel workbook environment has been enabled under: File/Options/Formulas/Enable iterative calculations.

- Set the Calculation options under File/Options/Formulas to ‘Automatic except data tables’. In case of the existence of data tables in the models, press F9 to refresh and update the table calculations.

- The workbook contains a Macro in the form of the product Disclaimer which should be accepted by the user; hence, please enable macros in the workbook. The financial model itself contains no macros.

- Please ensure the above steps are implemented prior to opening the excel sheet.

- Please agree to the terms of use to be able to view the model.

- If at any point #Value! appears in the Model and the results, toggle the circularity switch on the Assumptions tab to ON and then OFF to address the problem. This switch sets all interest expenses to zero when turned ON.

- If any changes are applied to the assumption inputs in the model, toggle through the Scenario Switch on the Assumptions tab to Base, Best and Worst Case so that the Summary tab results are updated.

- All blue font in the model are hardcoded inputs, black font is calculation, red font is the references to the blue inputs on the Assumptions tabs, and any orange cells are values sourced from Refinitiv.