Publication number: ELQ-61264-1

View all versions & Certificate

Startup Loan Brokerage Financial Model (Mortgage, SBA & CRE + Capital Advisory)

This model was built to perform a 5-year financial feasibility study of a new loan brokerage business. It also has the capability to model capital advisory.

Overview

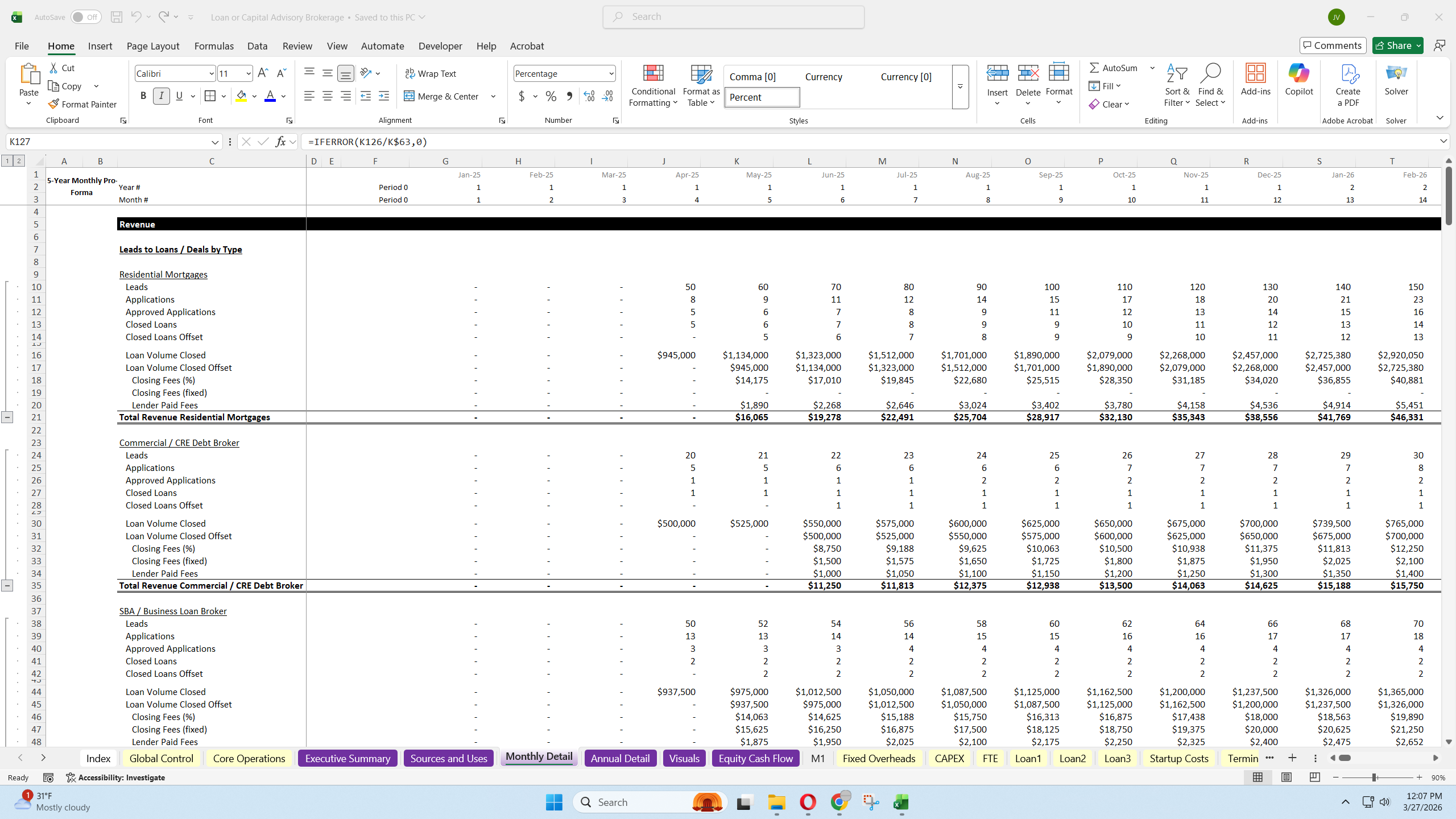

- This financial model template is built for businesses that earn fees on closed transaction volume.

- It is designed to support four core channels:

- Residential mortgages

- Commercial loans

- SBA loans

- Capital advisory / investment banking / deal brokerage transactions

- The model is built around the core economics of these businesses: generating leads or relationships, moving them through a funnel, and converting that activity into closed transactions and revenue.

- It allows users to define lead volume by channel, apply funnel conversion rates, account for timing to close, and project how that translates into monthly and annual financial performance.

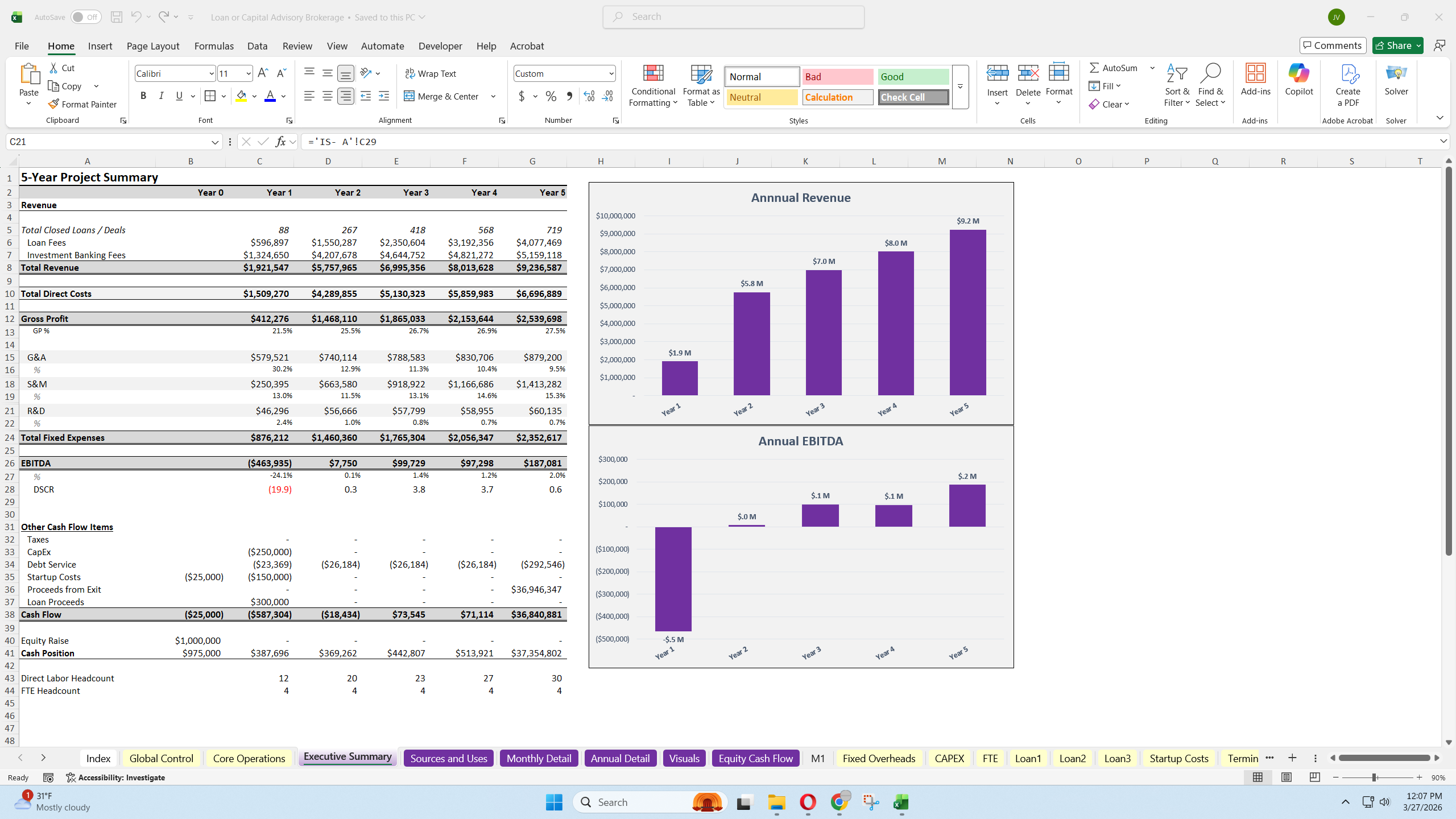

- Up to 5 years of projections.

- Monthly and annual granularity.

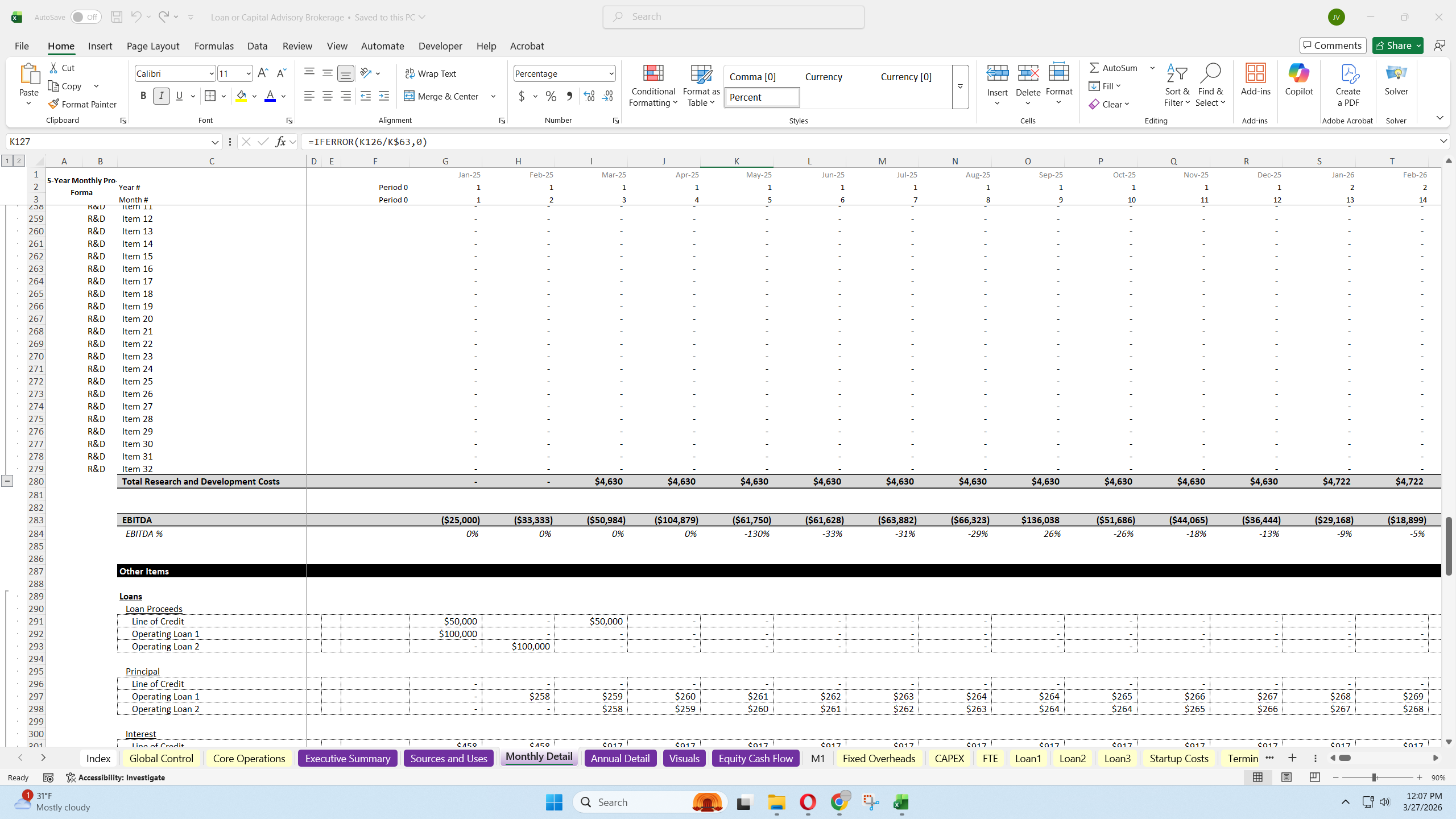

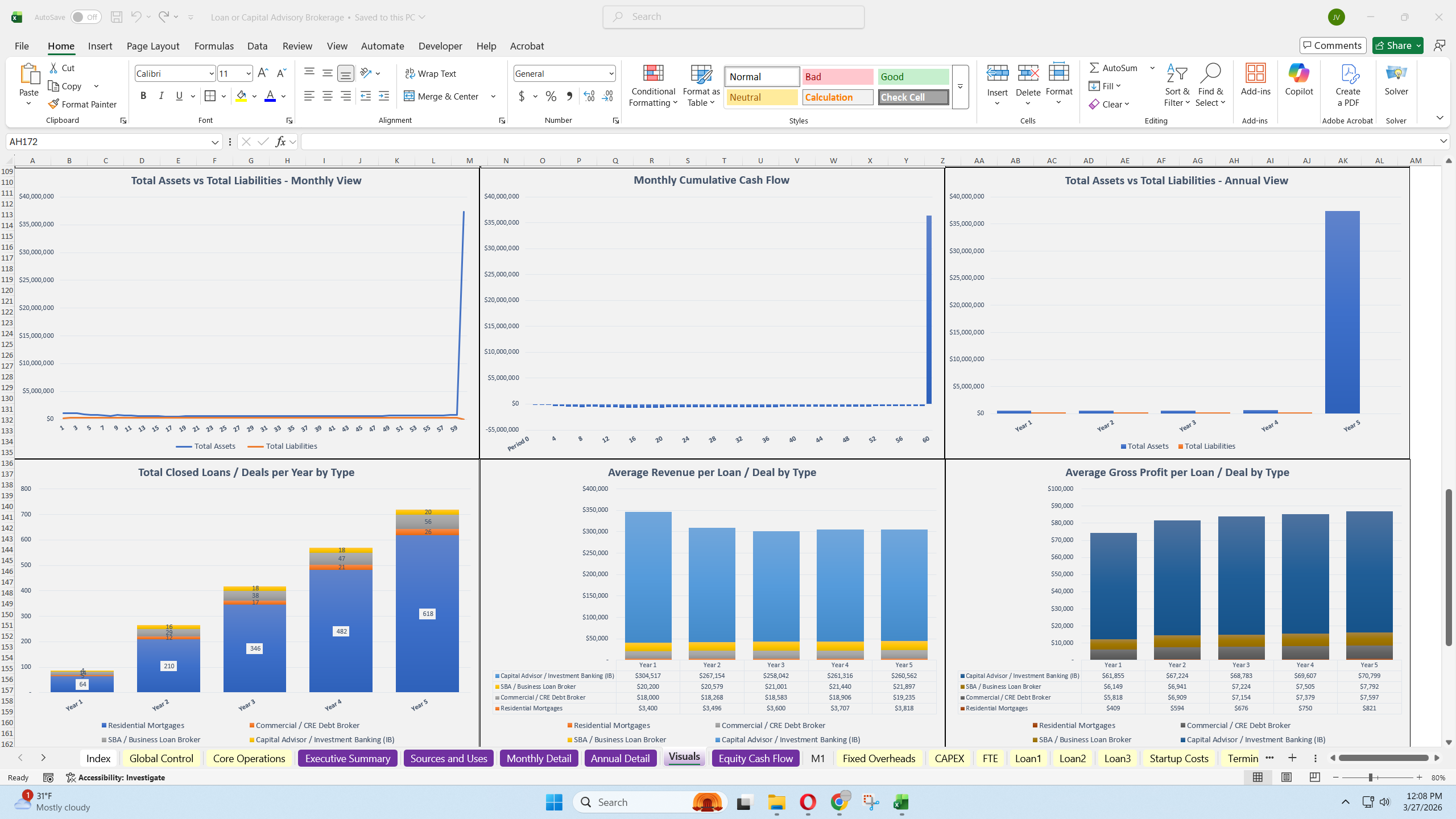

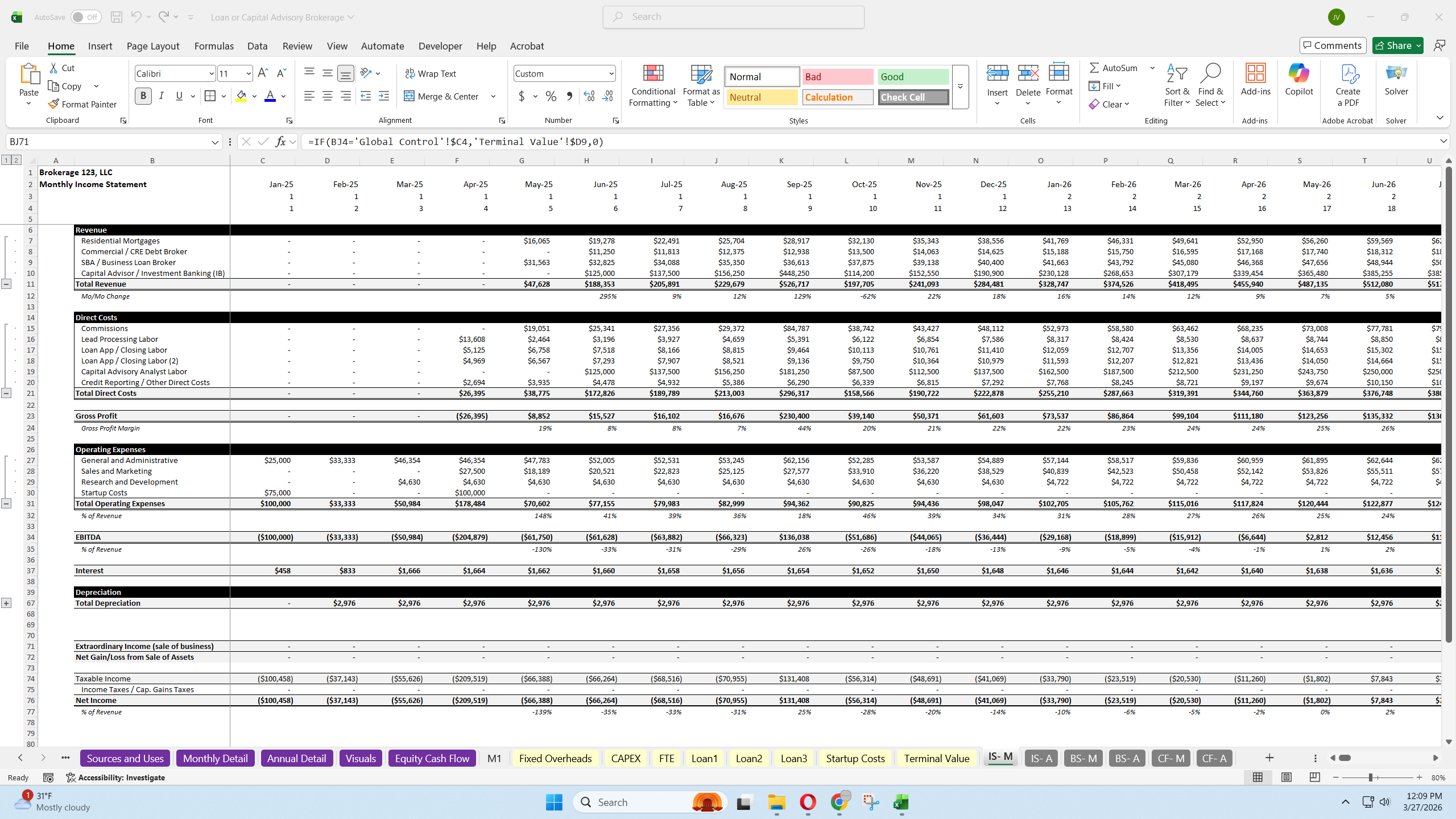

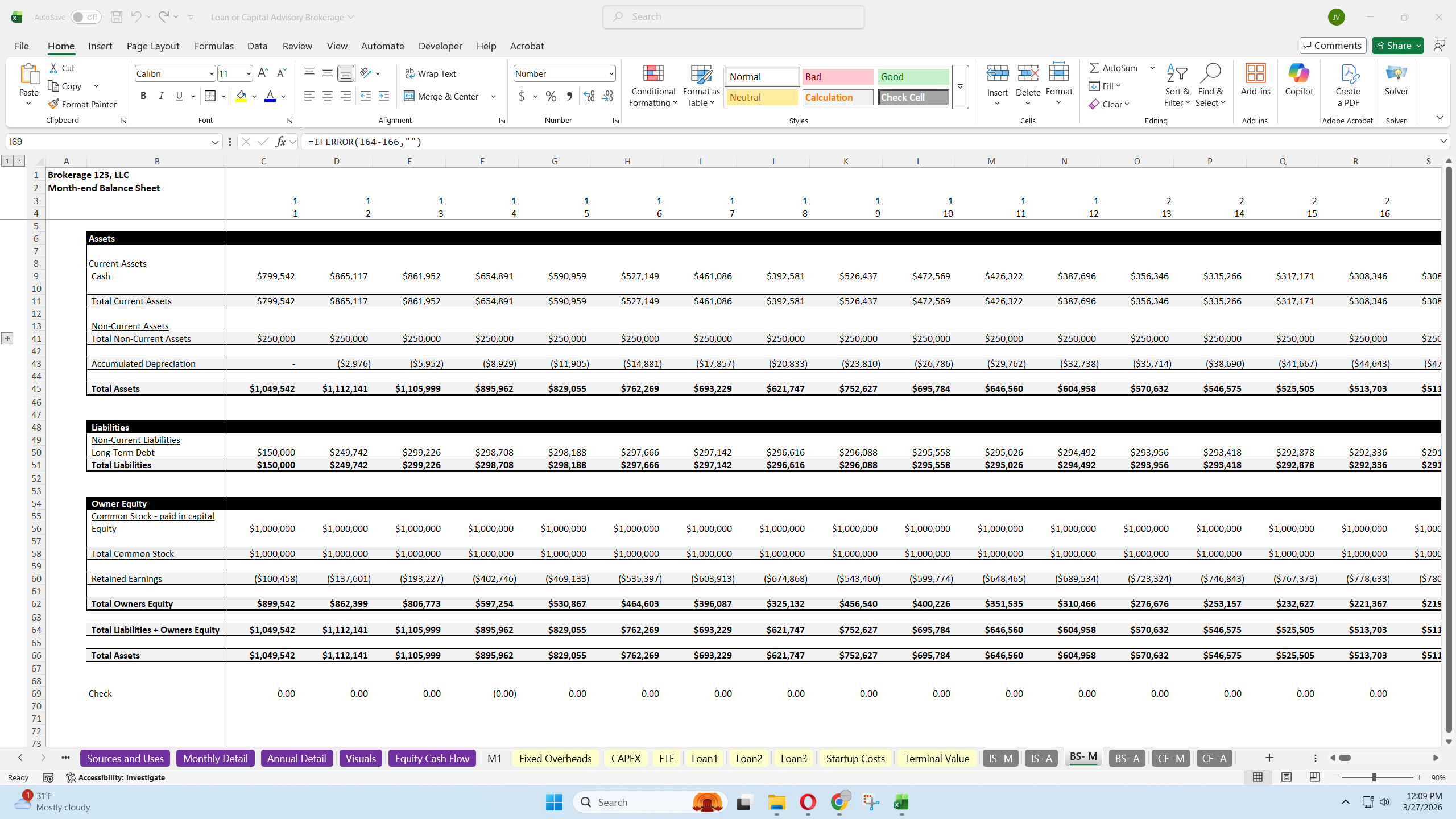

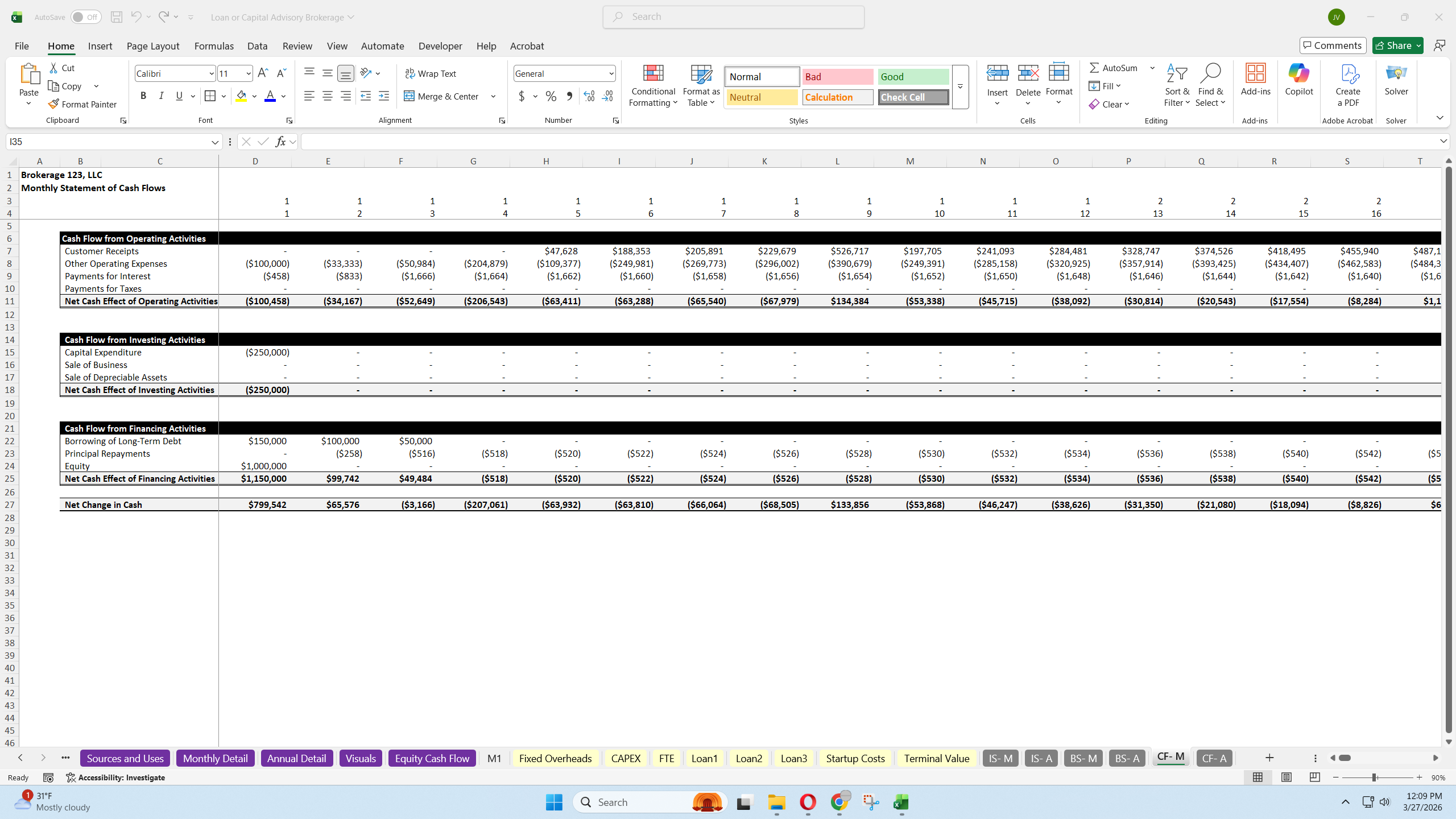

- Fully integrated financial statements:

- Income Statement

- Balance Sheet

- Statement of Cash Flows

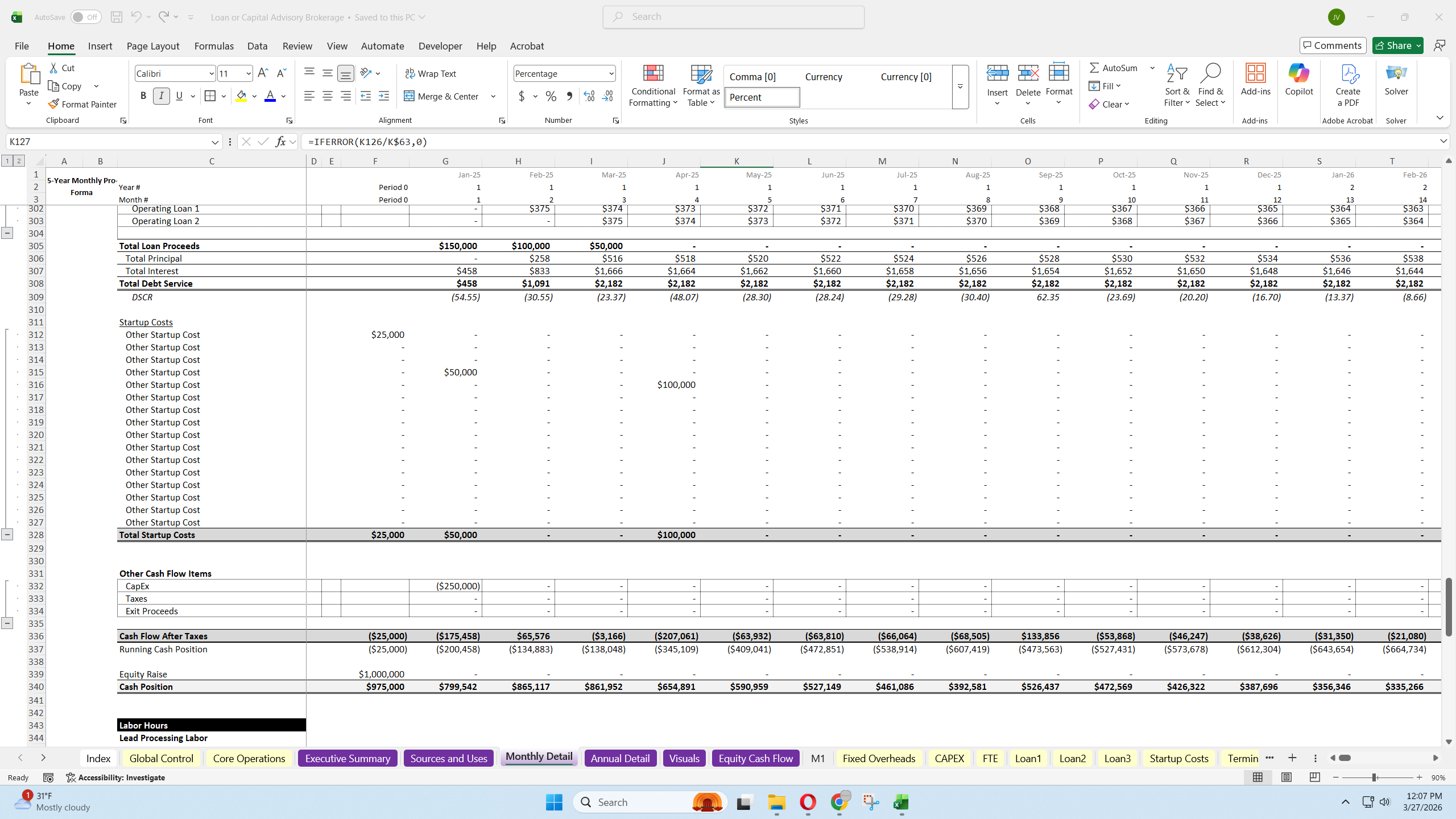

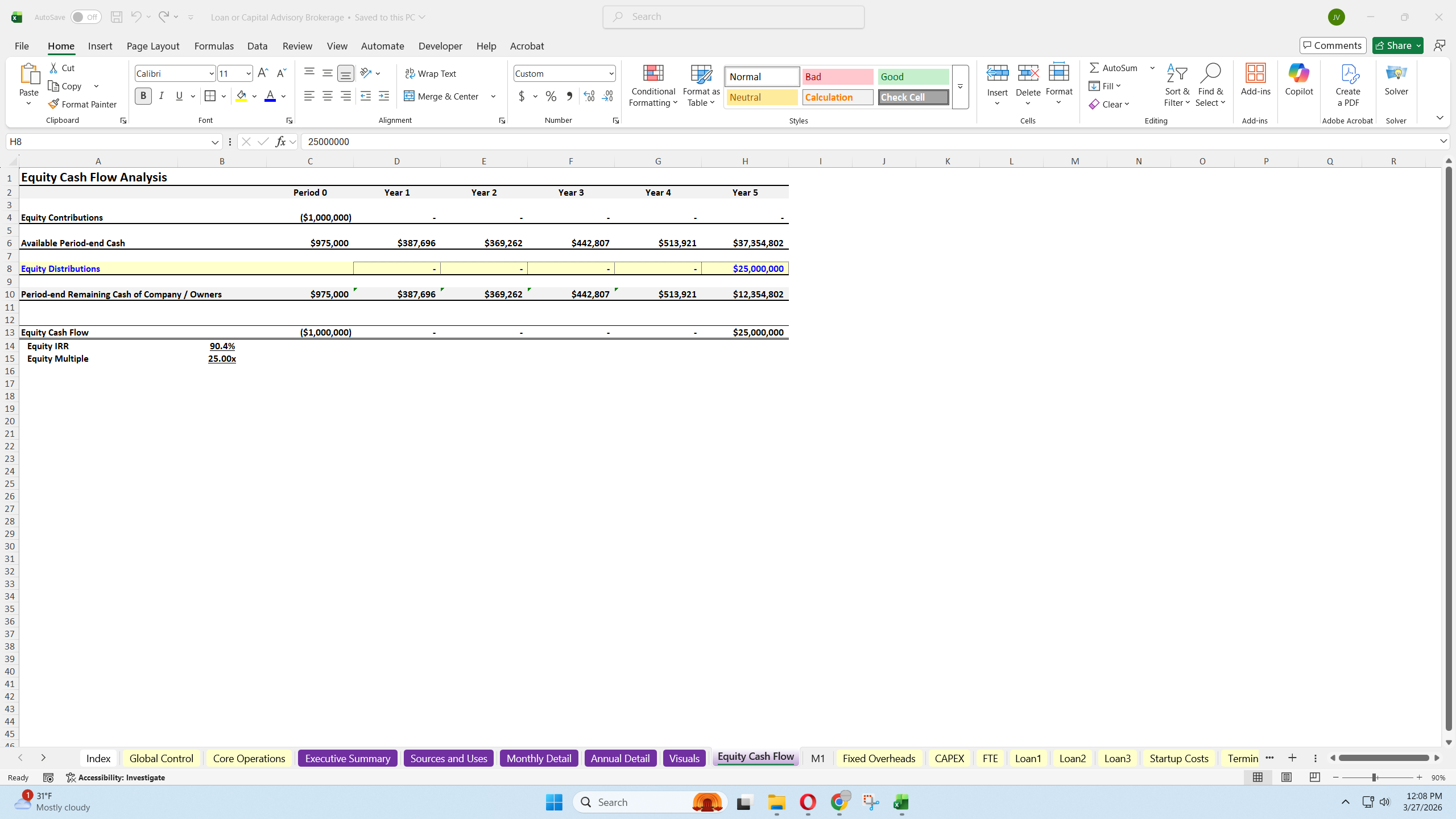

- Cash flow planning and equity investment tracking.

- IRR and Equity Multiple analysis.

- Terminal value analysis.

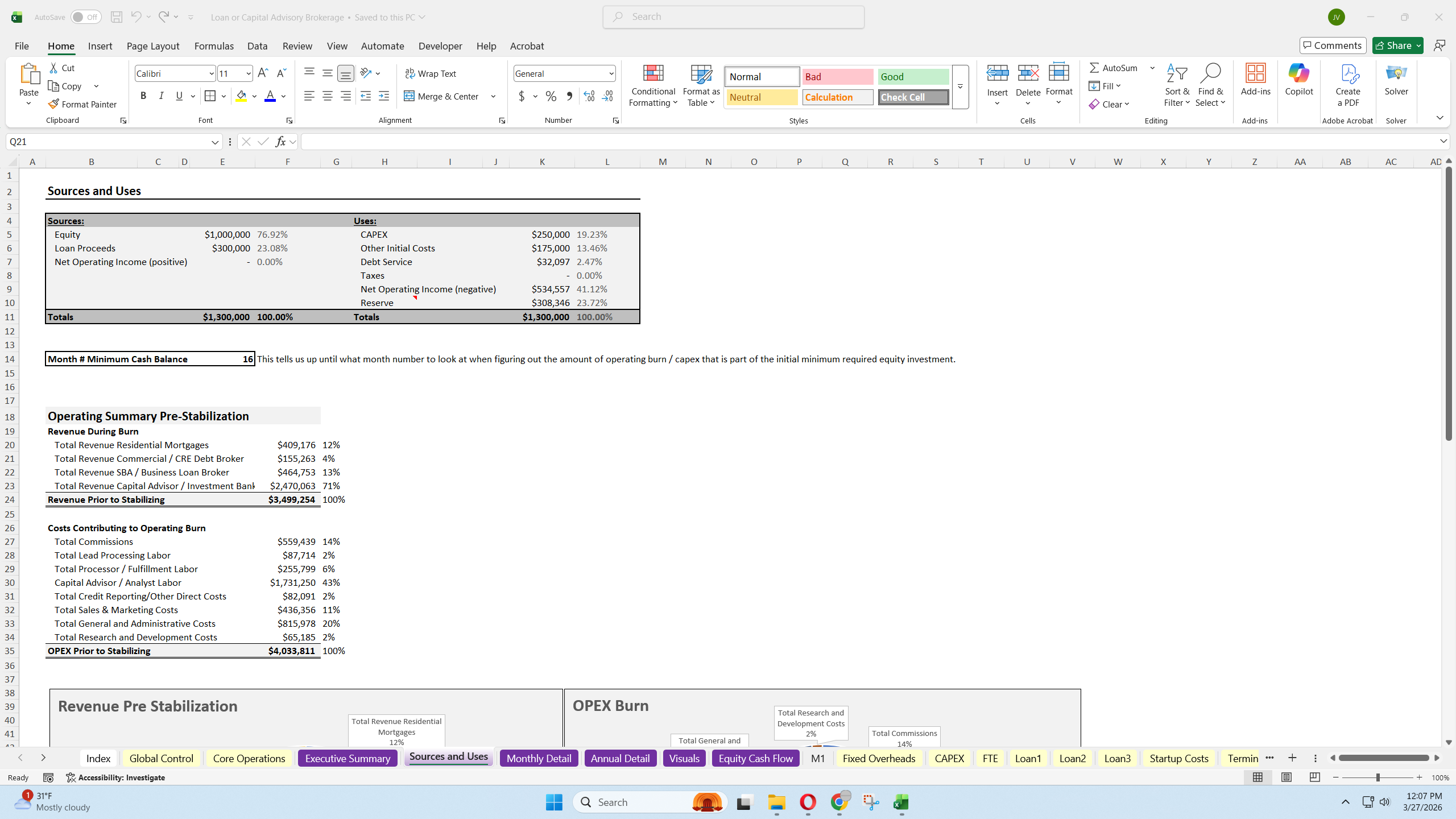

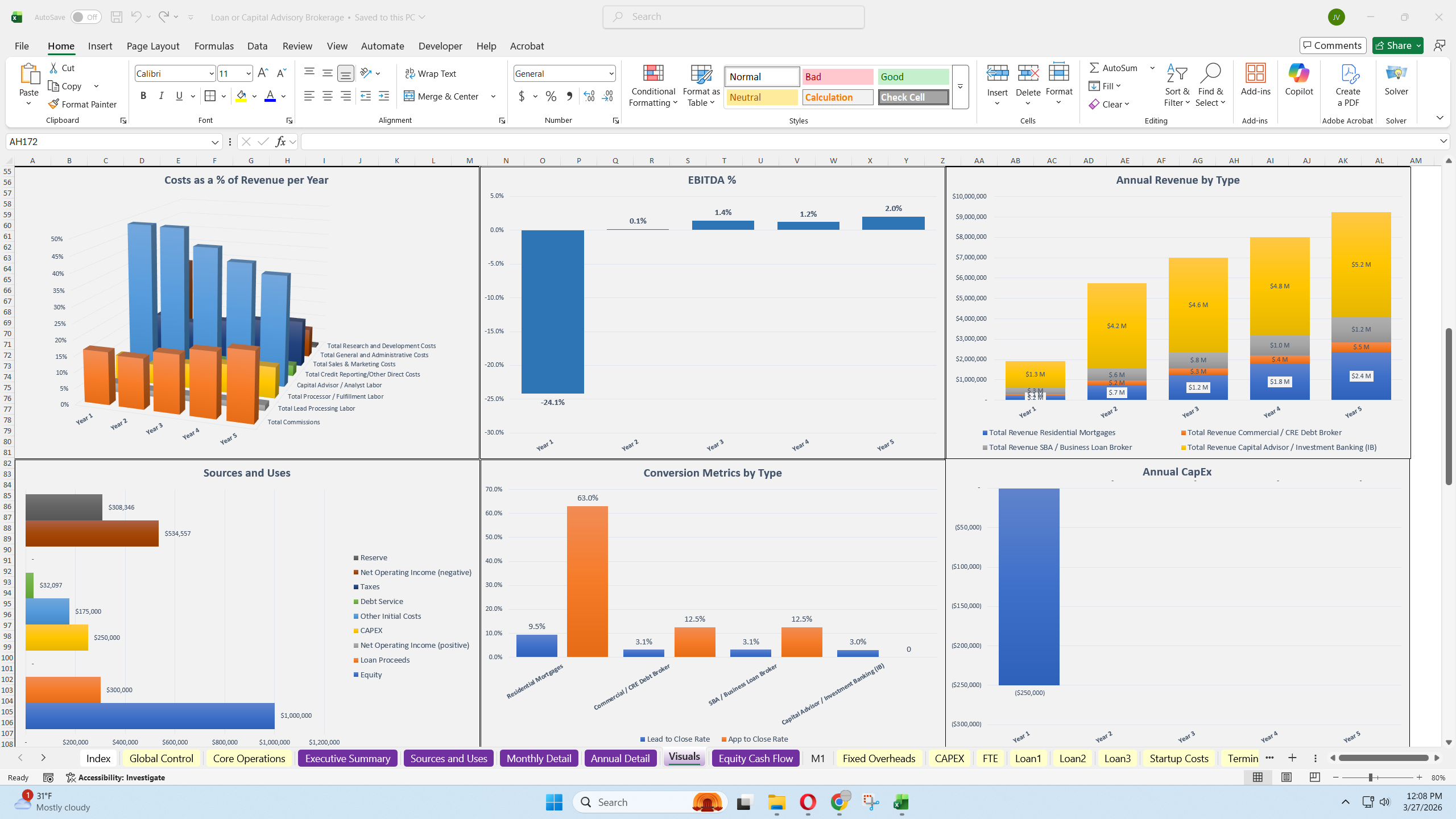

- Sources and Uses schedules, both high-level and detailed.

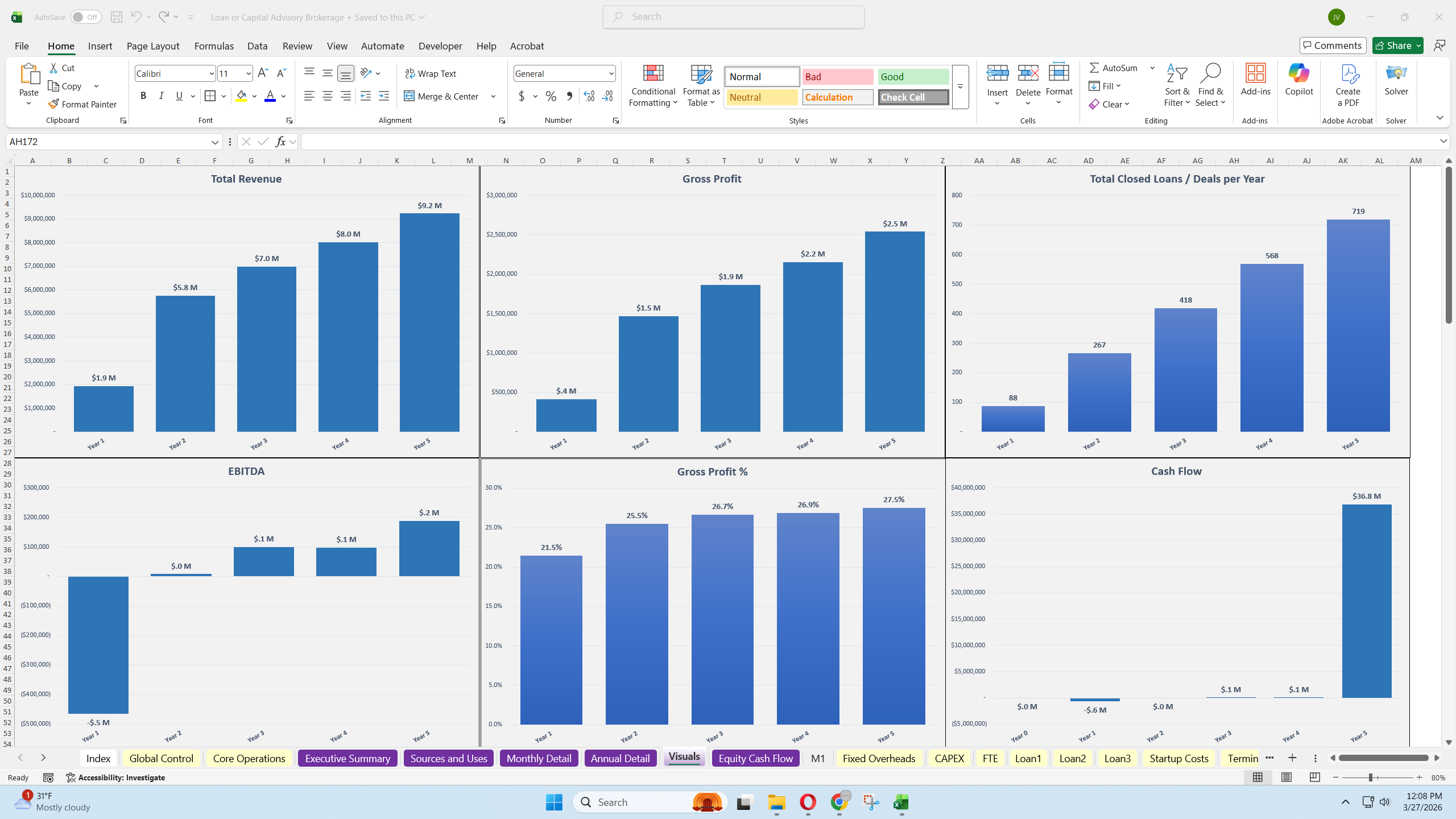

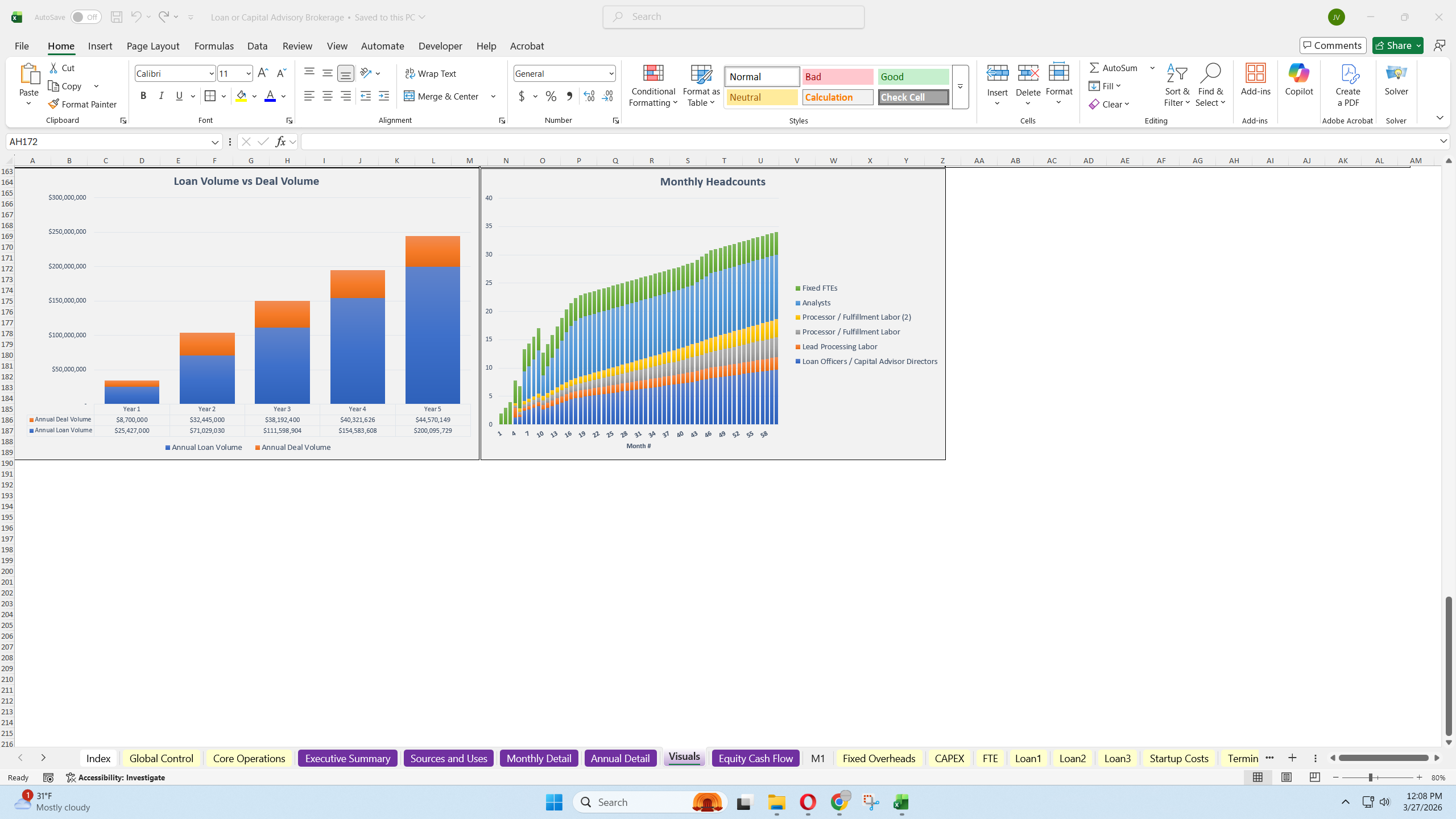

- 20 built-in charts for visual reporting.

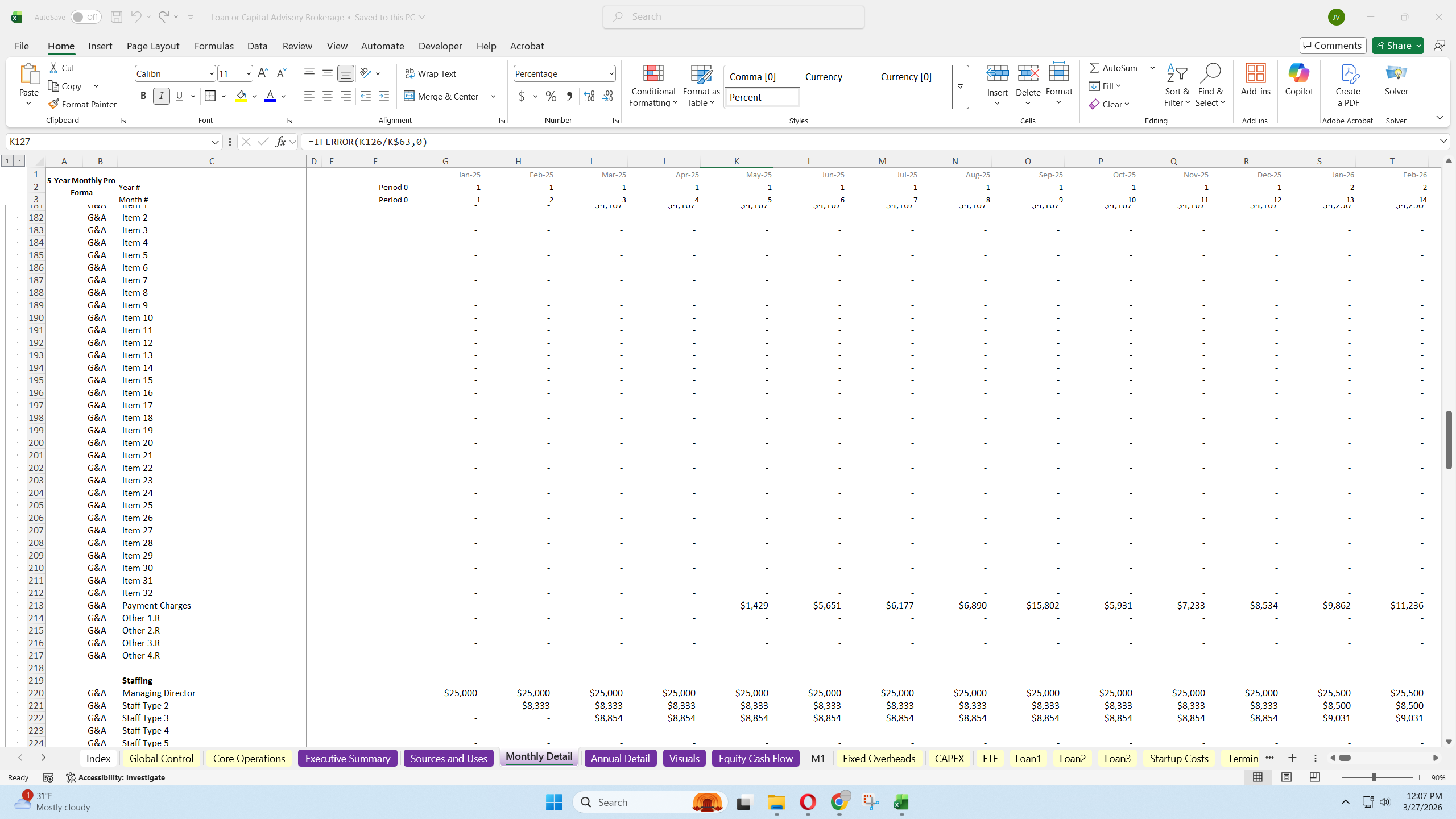

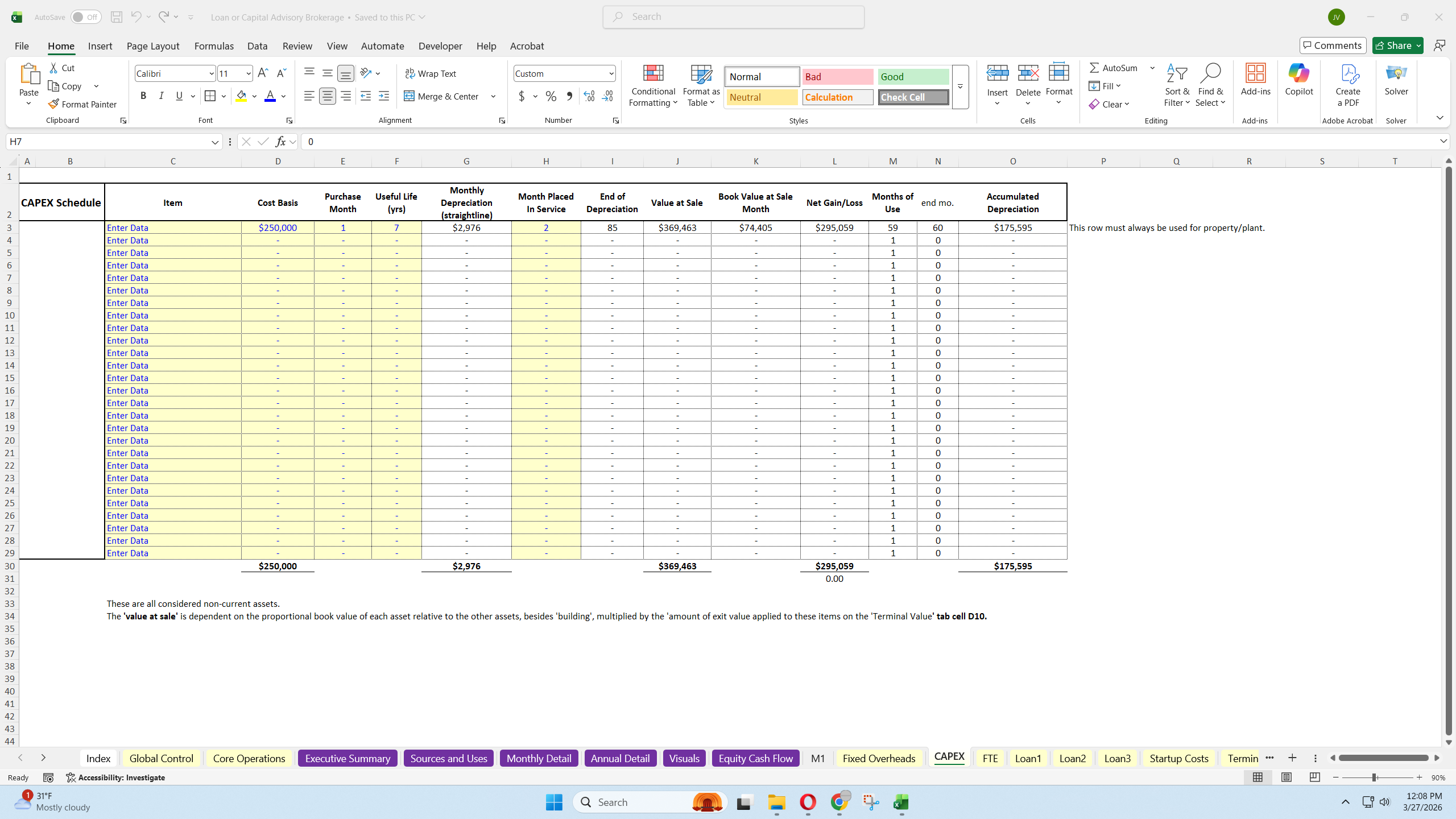

- Direct labor and direct cost schedules that scale dynamically with transaction volume.

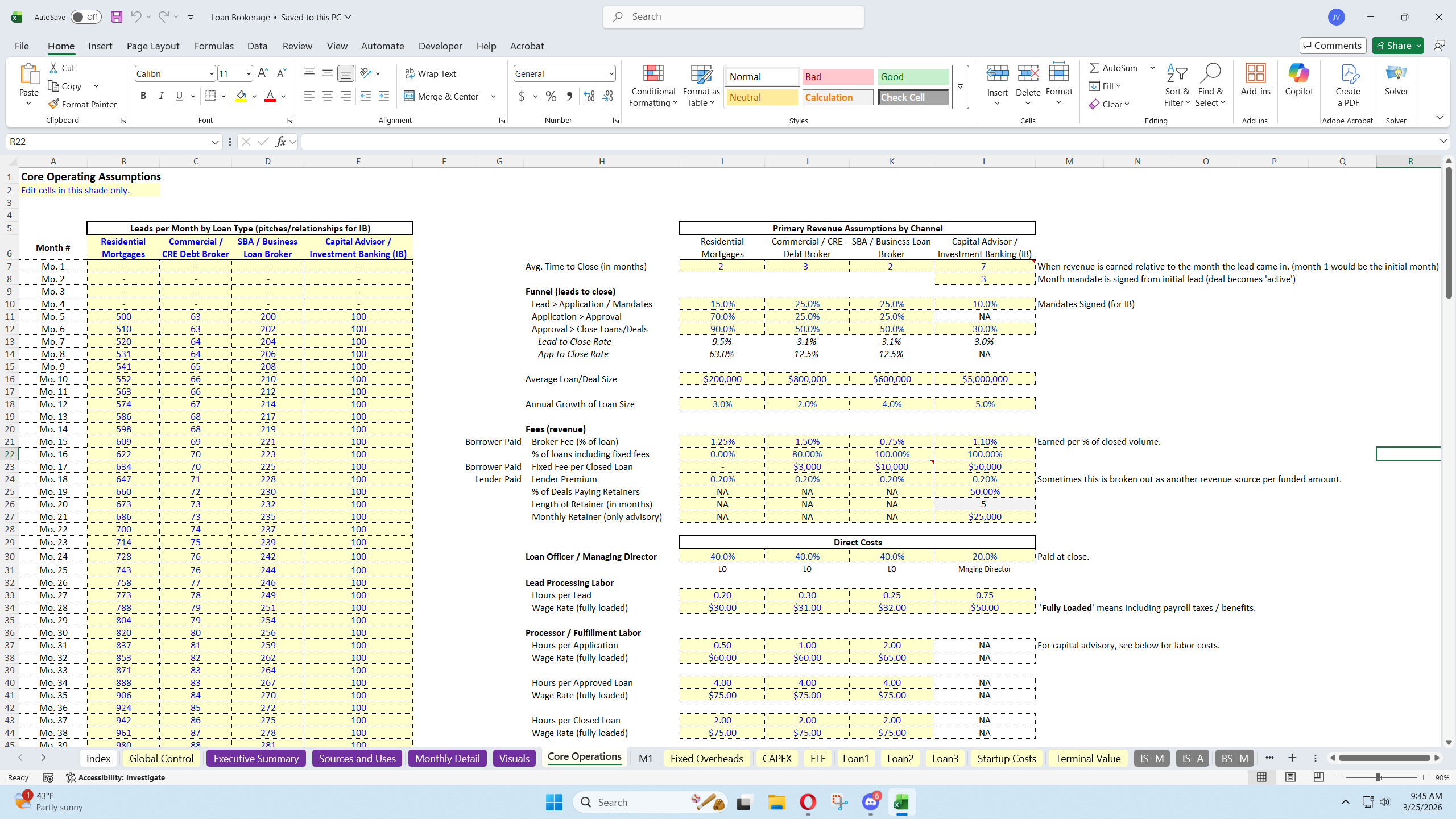

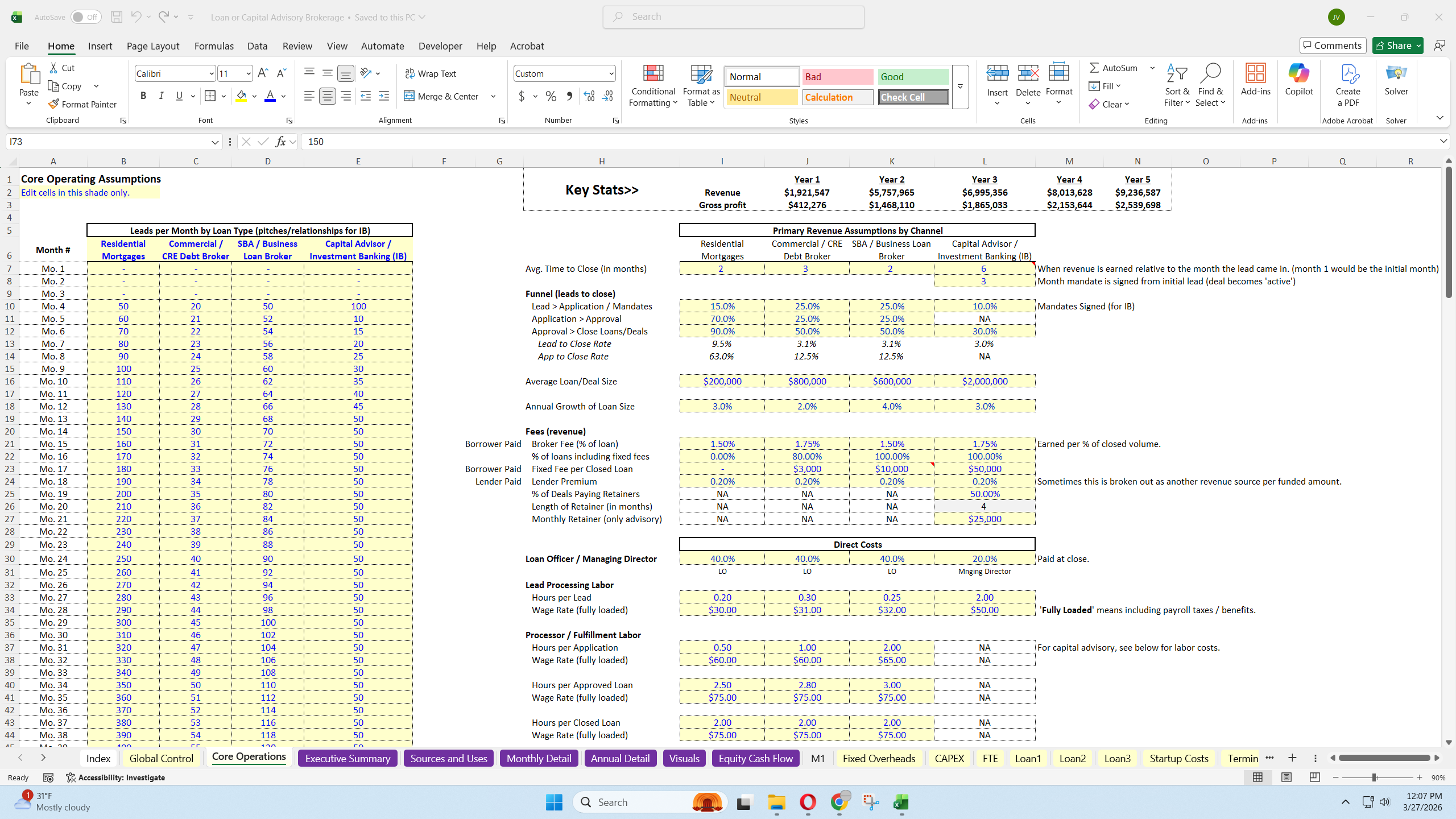

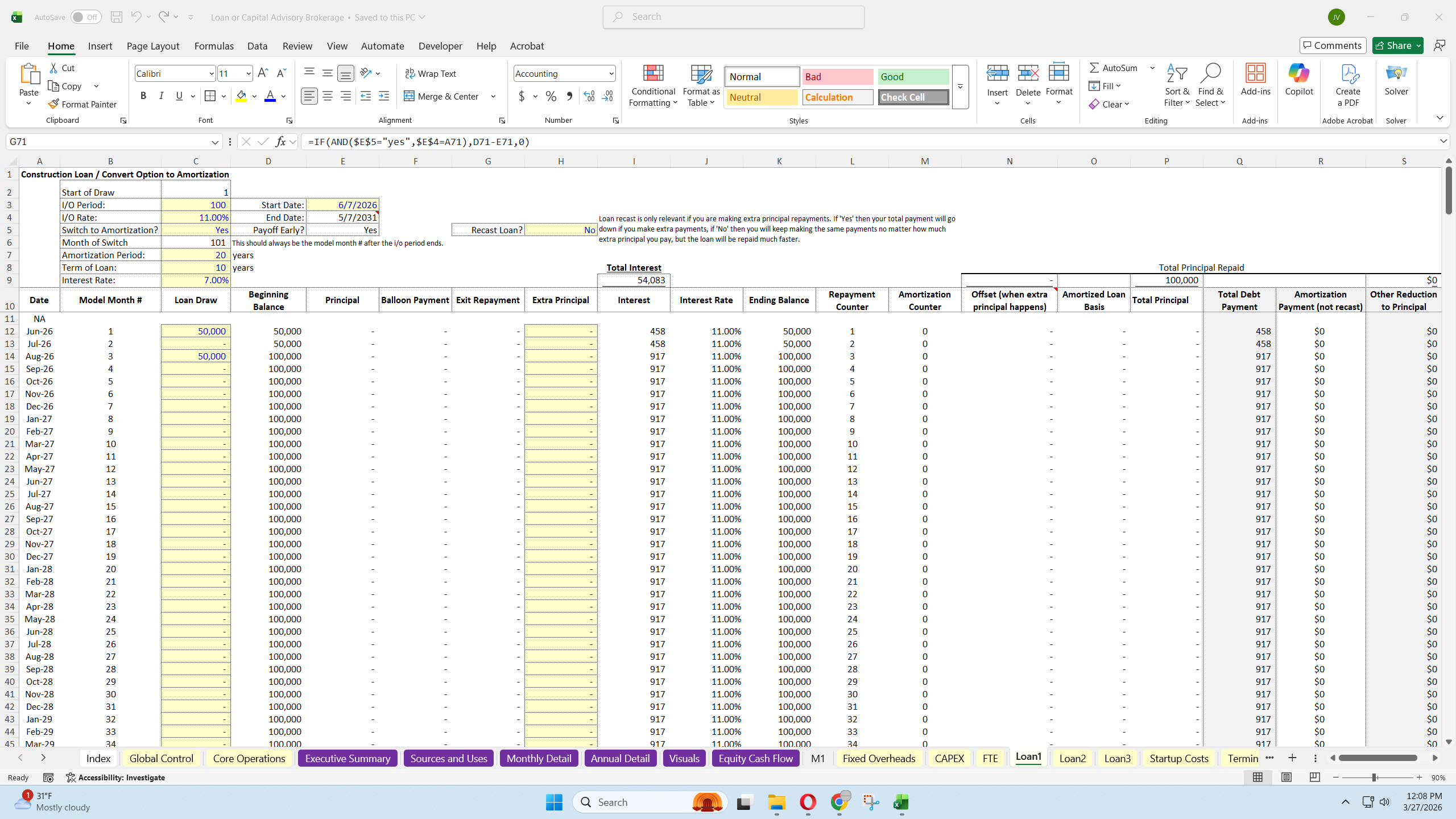

For the residential, commercial, and SBA loan channels, the model includes assumptions for:

- Leads per month.

- Average time to close, which offsets revenue timing.

- Funnel conversion rates:

- Lead to Application

- Application to Approval

- Approval to Closed Loan

- Average loan size.

- Annual growth in average loan size.

- Broker fee as a percentage of loan volume.

- Percentage of loans that include fixed fees.

- Fixed fee per closed loan.

- Lender premium.

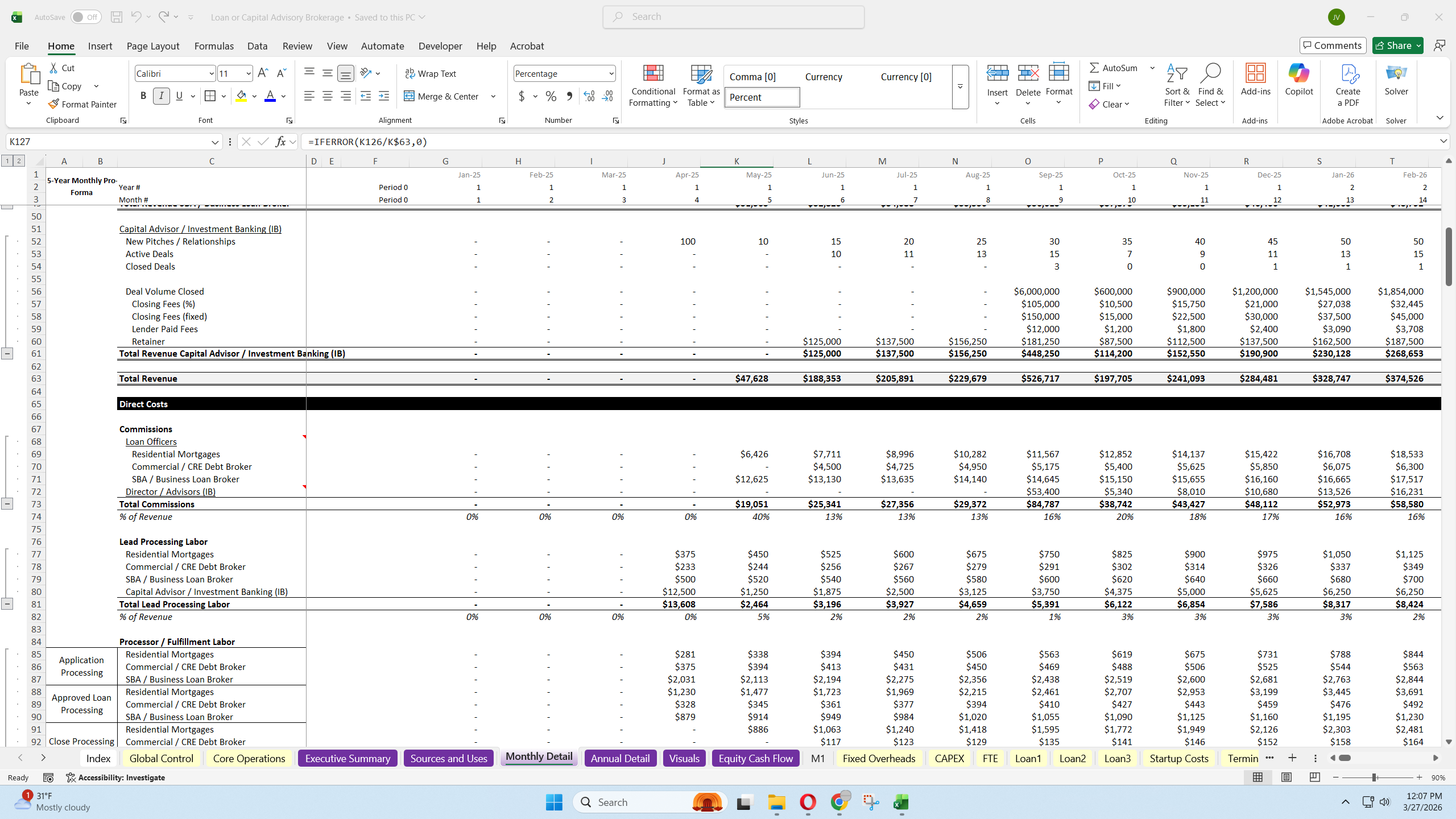

- Loan officer commissions as a percentage of revenue.

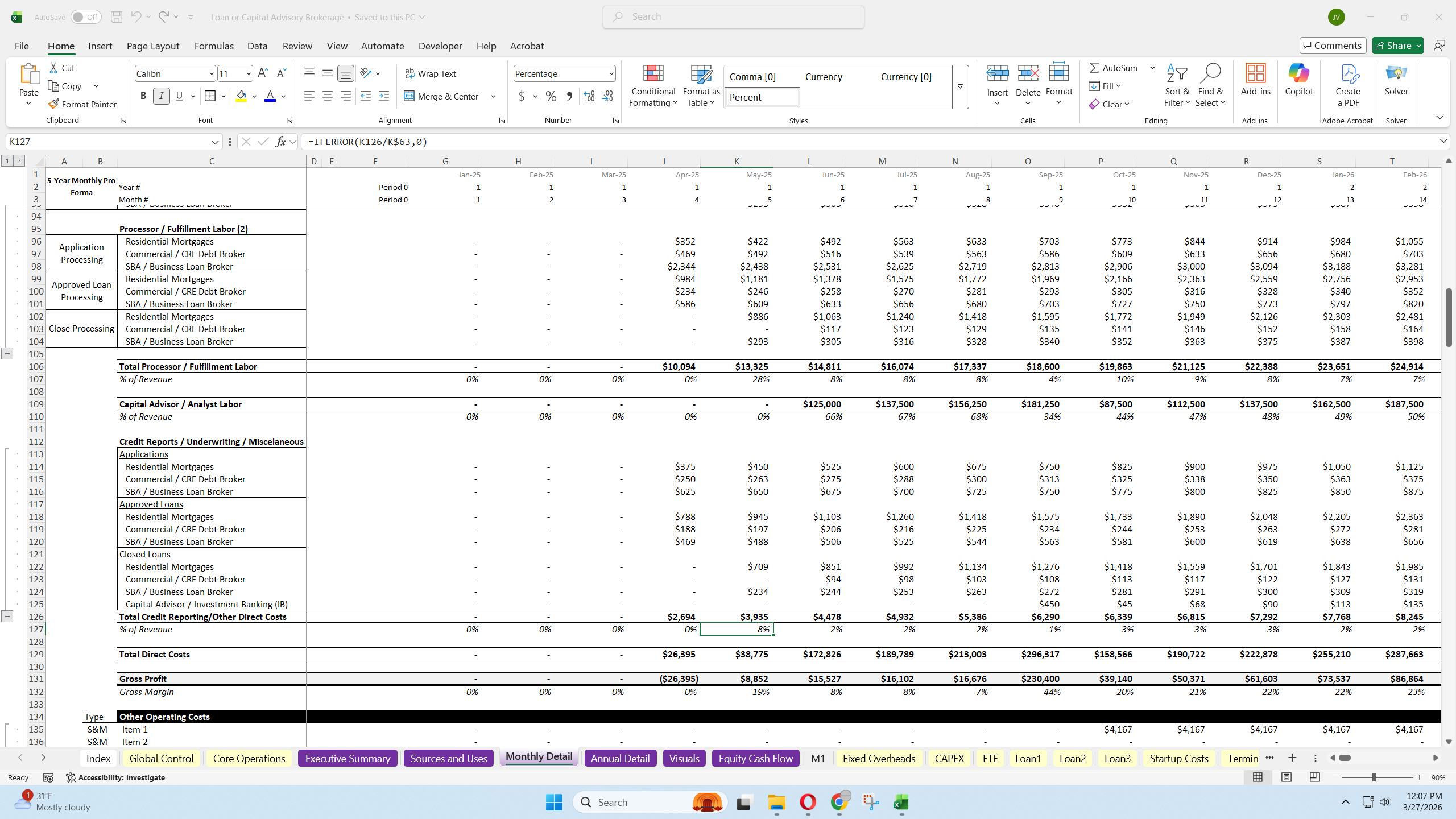

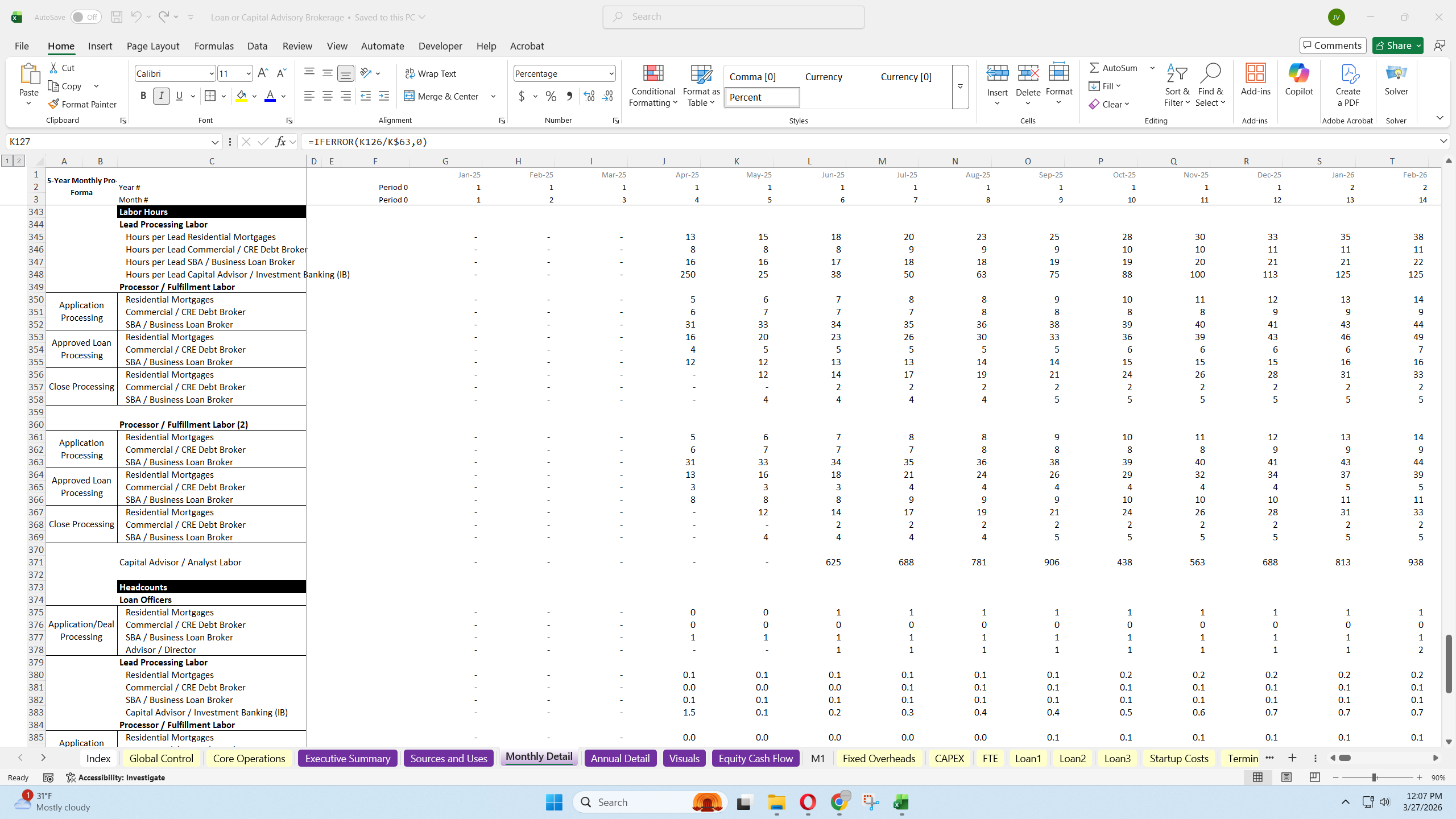

- Lead processing labor.

- Processor / fulfillment labor.

- Additional processor / fulfillment labor layer.

- Labor efficiency factor.

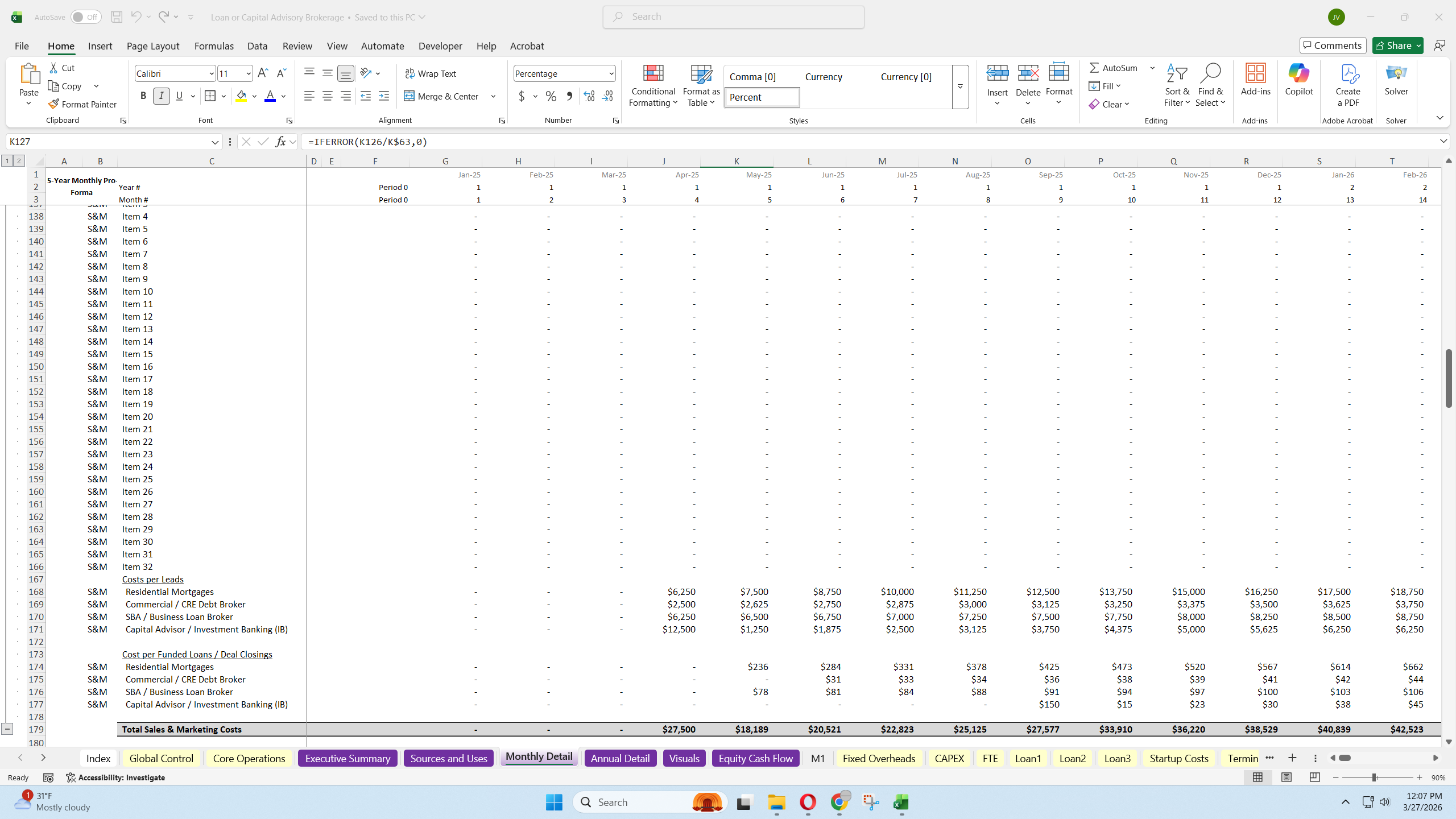

- Cost per lead.

- Cost per funded loan.

- Cost per application.

- Cost per approved loan.

- Cost per closed loan.

- Credit reports, underwriting, and miscellaneous transaction costs.

- Includes capacity assumptions to display implied headcount needs as volume grows.

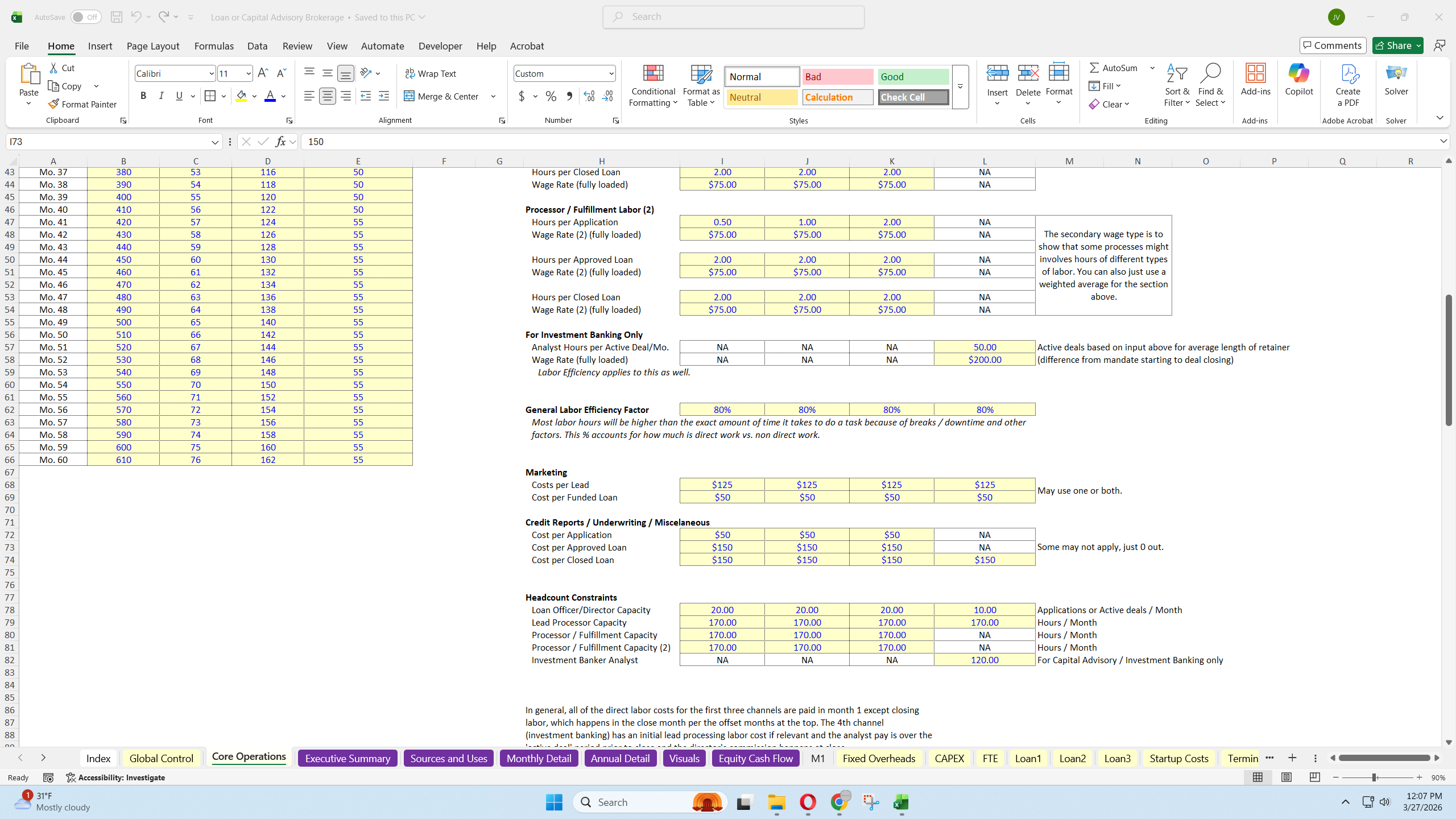

The fourth channel is built for capital advisory, investment banking, and other deal brokerage strategies, with logic tailored to those transactions.

Core assumptions

- Relationships started per month.

- Time to close.

- Mandate start timing after relationship start.

- Conversion of relationships to mandates.

- Conversion of mandates to closed deals.

- Average deal size.

- Annual growth in average deal size.

- Broker fee as a percentage of deal size.

- Percentage of deals including fixed fees.

- Fixed fee per closed deal.

- Lender premium where applicable.

- Percentage of deals paying retainers.

- Monthly retainer amount earned between mandate start and close.

- Director / advisor commissions based on close revenue.

- Lead processing labor.

- Analyst labor based on hours per active deal per month.

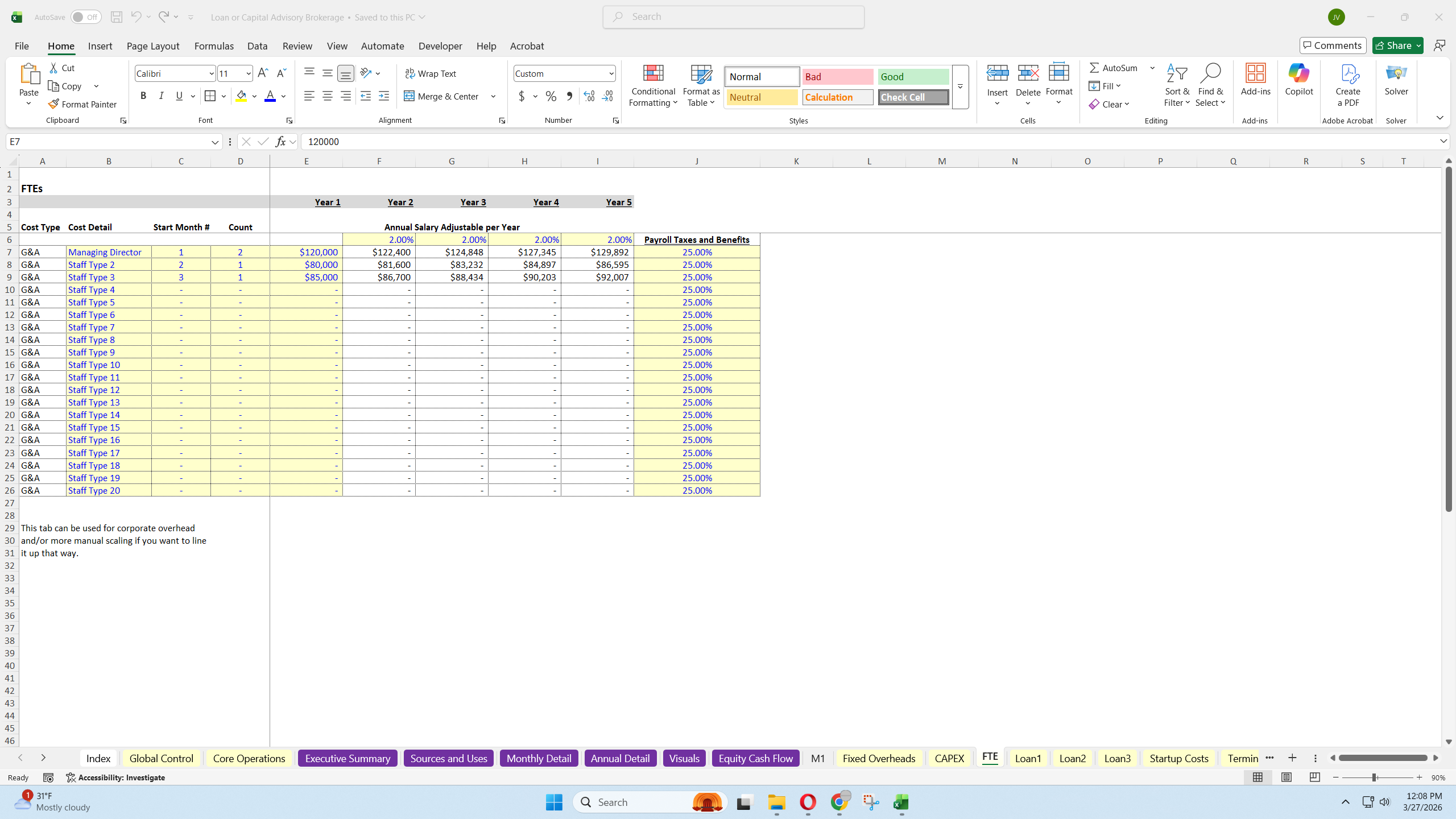

- Separate FTE expense schedule.

- Other direct costs such as cost per lead and fixed costs per closed deal.

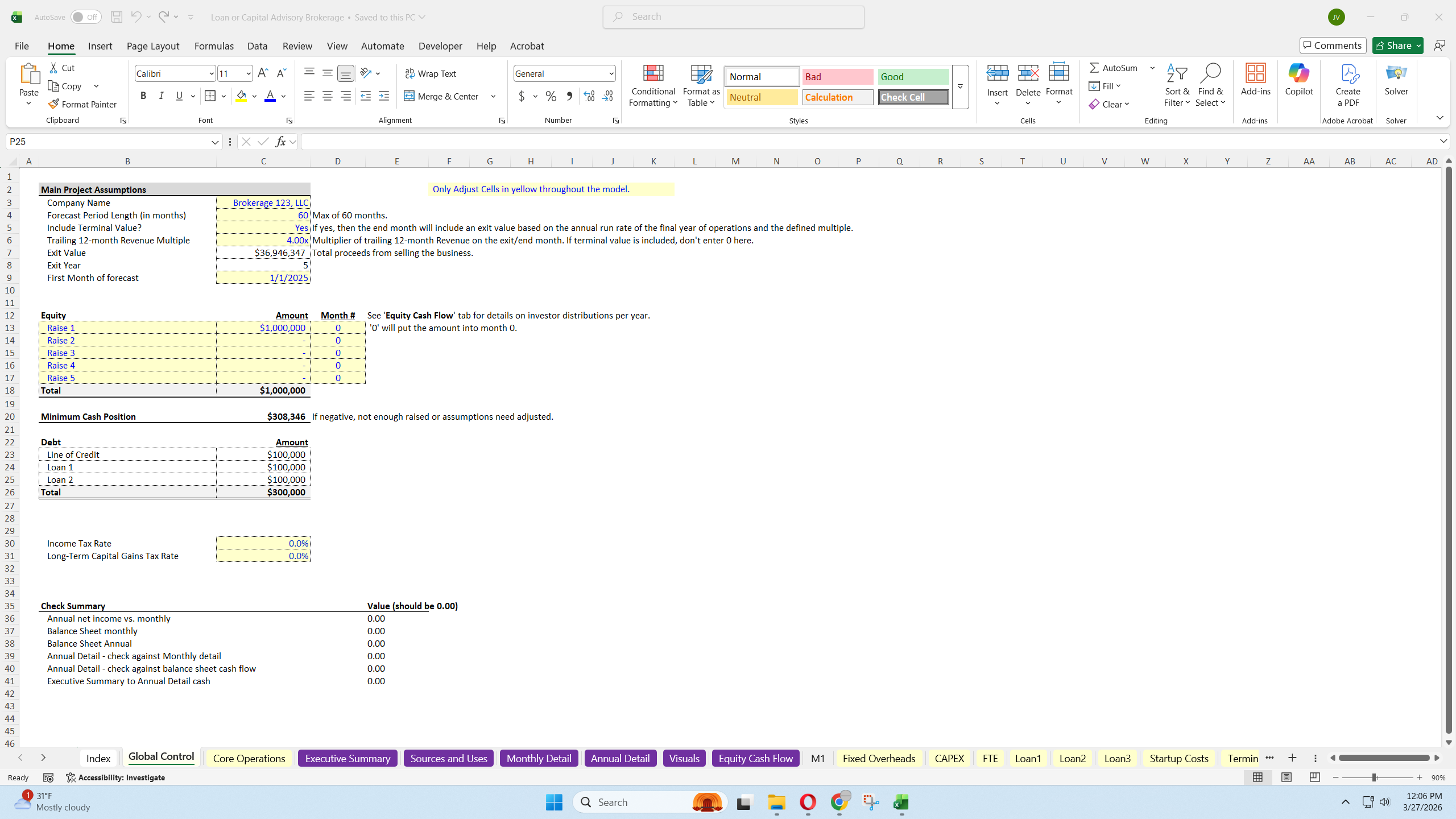

This version includes more flexible planning features than a standard all-upfront model.

- Up to 5 separate equity investment rounds can be modeled.

- Equity can be raised at different points in time instead of only at the start.

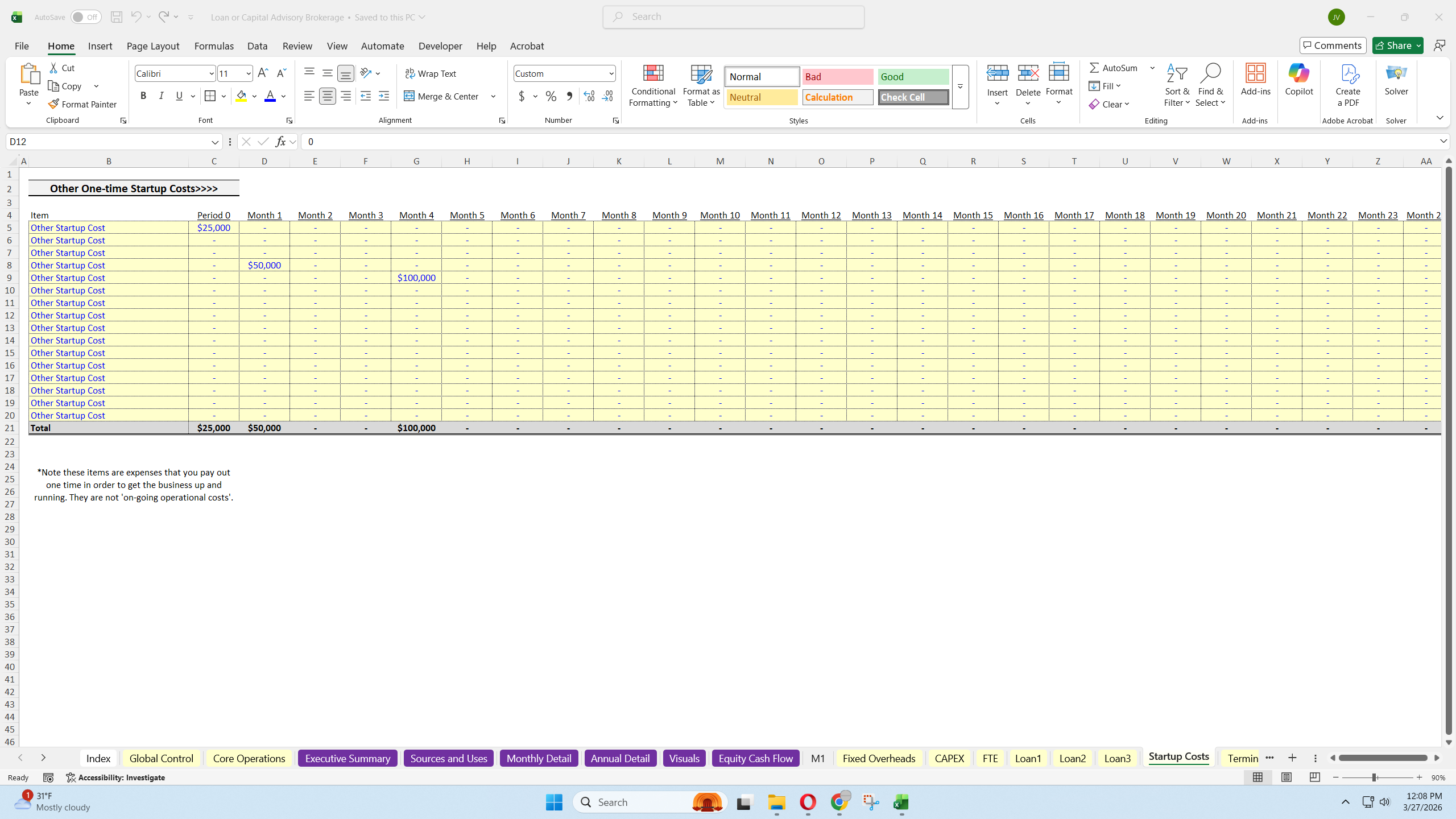

- Startup costs can be scheduled over the first 24 months.

- This better reflects how many real businesses launch, invest, and raise capital in stages.

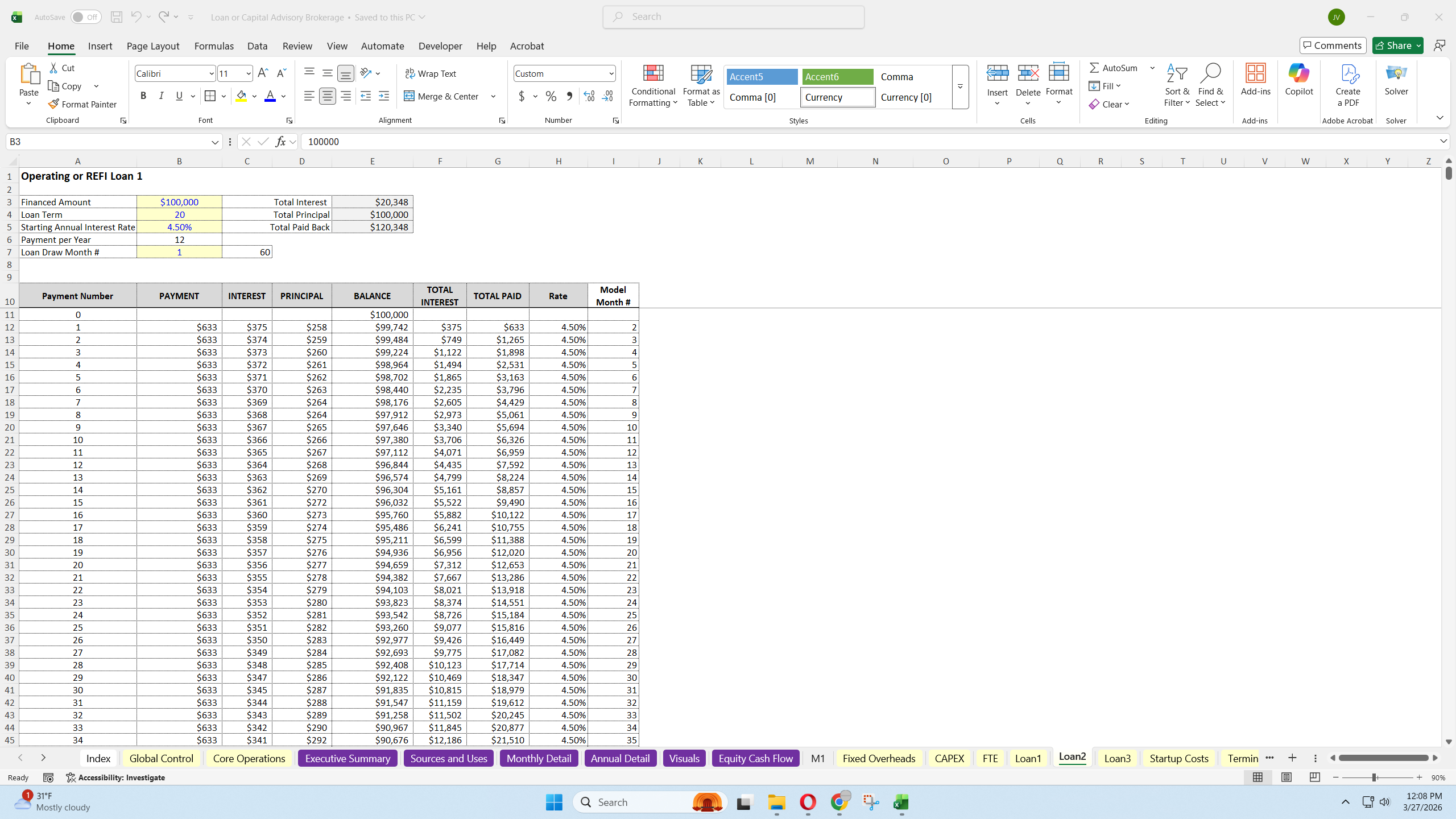

- Debt financing options for operations are also included.

- Most of the business inputs are completed in the Core Assumptions tab.

- After those assumptions are entered, the rest of the model updates automatically.

- Users can then review:

- Revenue build

- Direct labor and direct cost schedules

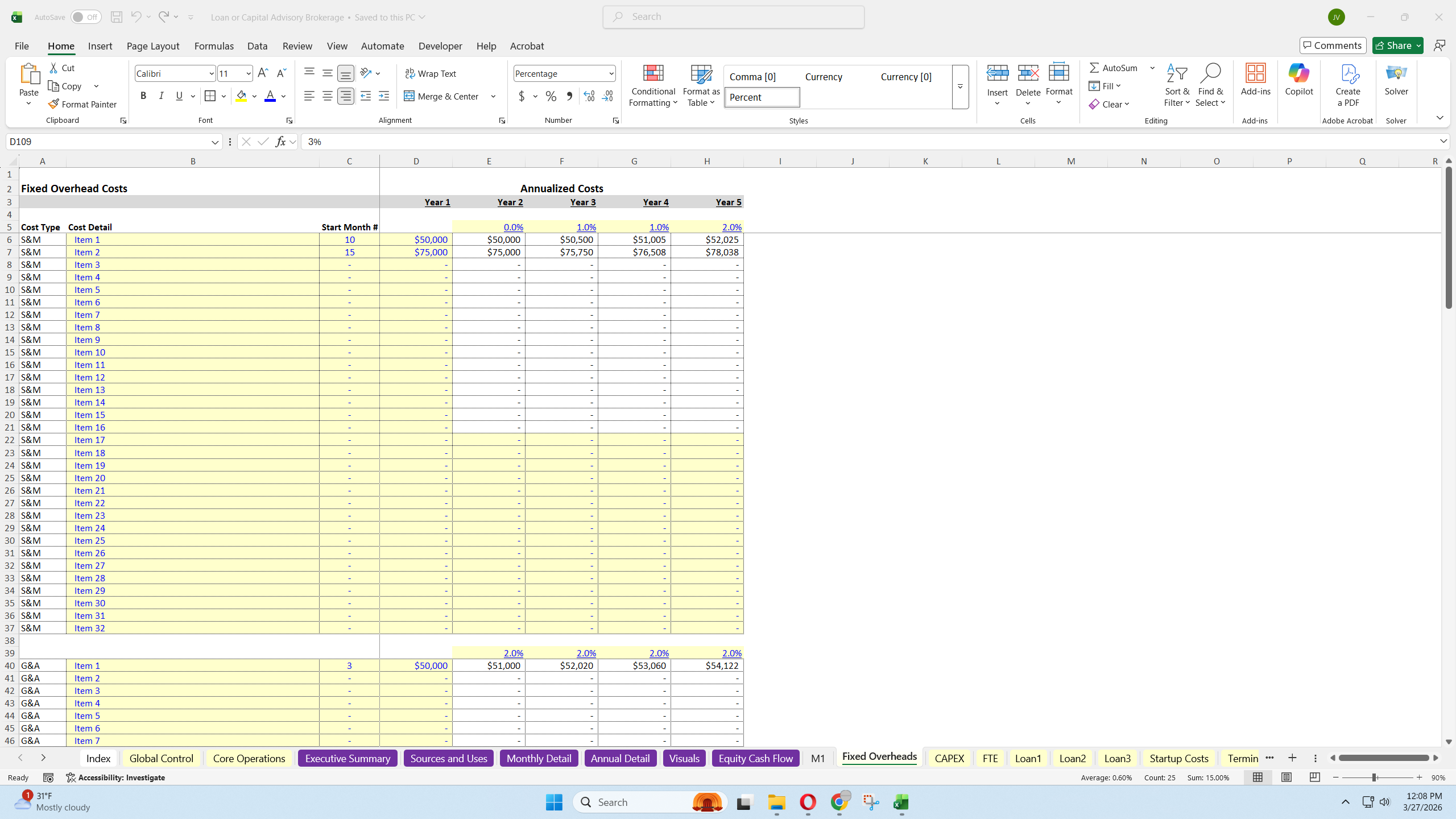

- Fixed overhead

- Startup costs

- Financing assumptions

- Investor return outputs

- Final reporting dashboards and charts

This model is useful because it goes beyond a simple revenue forecast and helps users understand how the business actually functions financially.

- It shows how leads, funnel conversion, timing, and average transaction size translate into closed volume and revenue.

- It helps users understand the relationship between production volume and staffing needs.

- It dynamically connects revenue growth to commissions, processing costs, analyst support, marketing, and other direct expenses.

- It provides a clearer view of margins, operating leverage, and scalability.

- It supports cash flow planning by showing when revenue is earned versus when costs and startup investments occur.

- It helps founders and operators plan hiring, capital needs, and growth targets more realistically.

- It is also useful for investors and lenders because it provides integrated financial statements, return analysis, and a more detailed operational view of the business model.

- It can be used for budgeting, fundraising, strategic planning, scenario analysis, and internal forecasting.

- Loan brokerage firms.

- Residential mortgage brokers.

- Commercial loan brokers.

- SBA finance businesses.

- Capital advisory and deal brokerage firms.

- Boutique investment banking teams.

- Founders building new transaction-based businesses.

- CFOs, FP&A teams, consultants, and investors evaluating this type of model.

- This template is built for transaction-based businesses that earn fees on closed loan or deal volume.

- It combines funnel-based forecasting, direct labor planning, dynamic cost scaling, cash flow planning, and investor return analysis in one integrated model.

- It is designed to be practical for operators and credible for investors, making it a strong tool for both internal planning and external presentation.

This Best Practice includes

1 Excel model, 1 overview video

Further information

Build a startup financial plan for any new loan brokerage business or capital advisory firm.

3 loan types and 1 capital advisory deal type.