Originally published: 19/04/2020 08:22

Last version published: 30/04/2020 06:56

Publication number: ELQ-97307-2

View all versions & Certificate

Last version published: 30/04/2020 06:56

Publication number: ELQ-97307-2

View all versions & Certificate

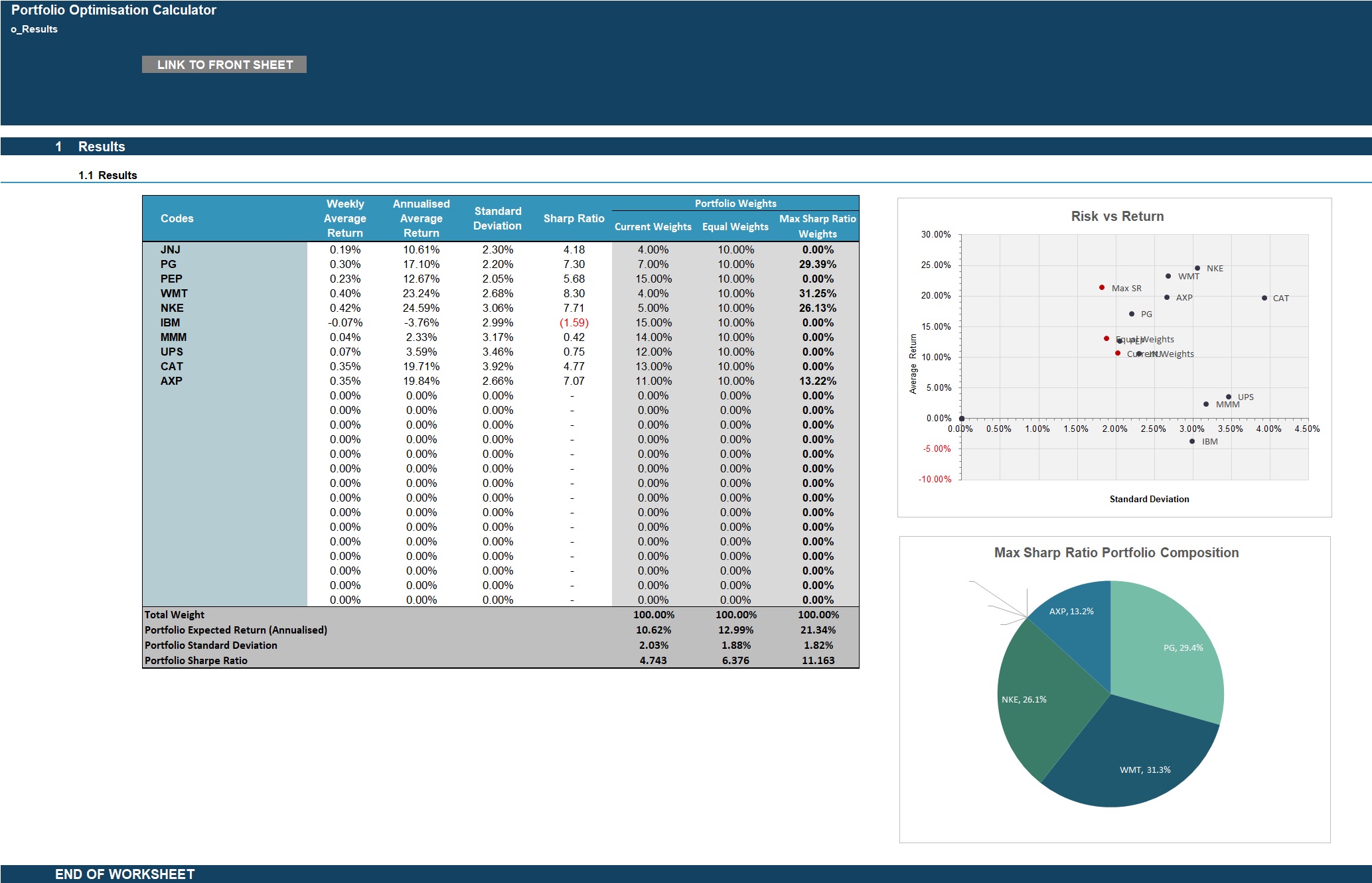

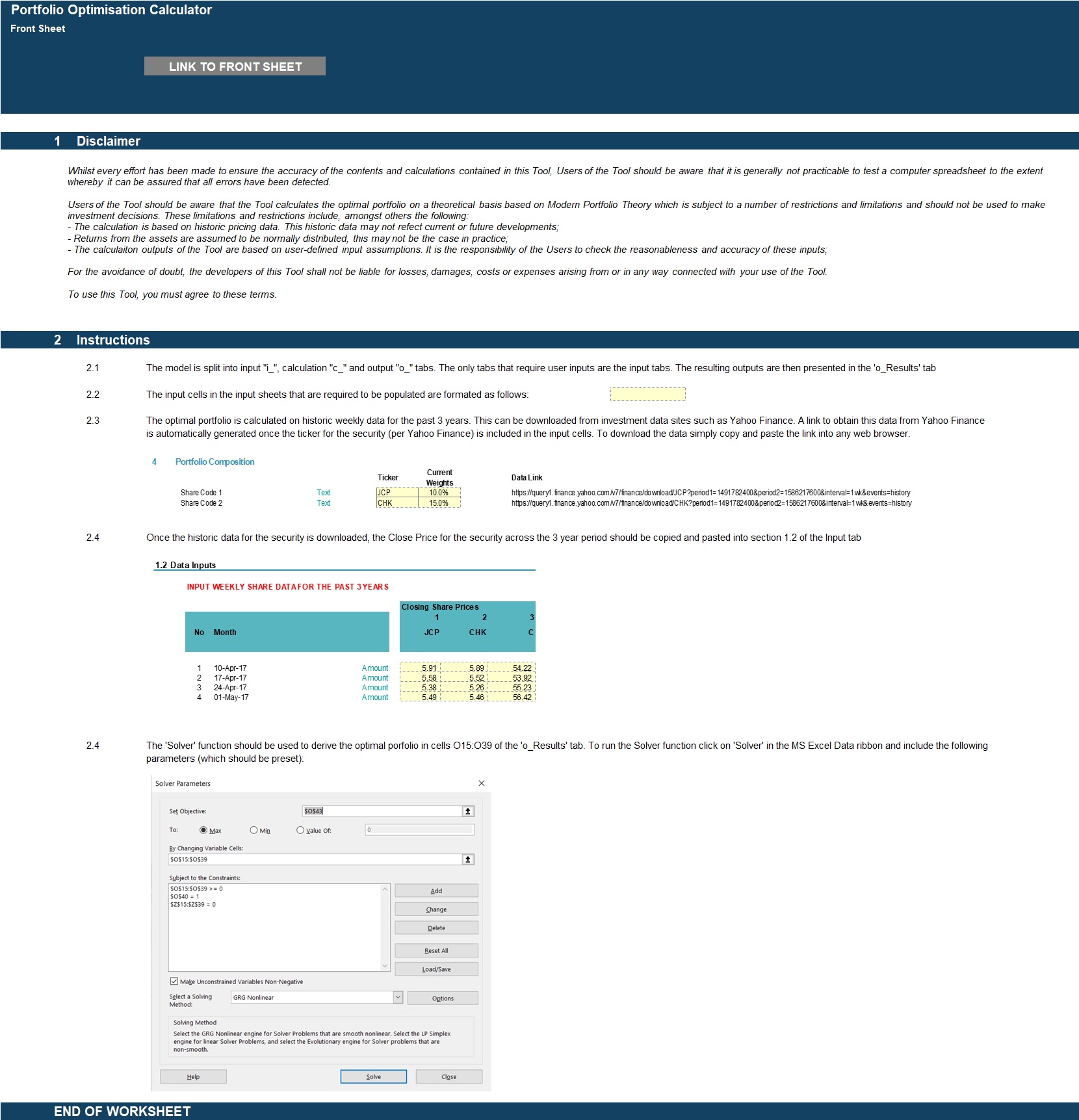

Theoretical Portfolio Optimisation Calculator

Excel tool for the calculation of the theoretical optimal portfolio weights for up to 25 securities

Further information

Calcualte the theoretical optimal porfolio weights for up to 25 securities using past histroic pricing data