Publication number: ELQ-69406-1

View all versions & Certificate

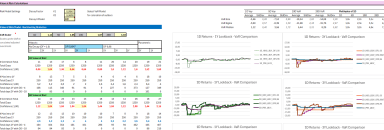

Portfolio Value at Risk Modelling Tool

Calculate Portfolio P&L | Study Distribution | Fine Tune Value at RIsk Model | Run Backtesting/Validation Analysis .

Further information

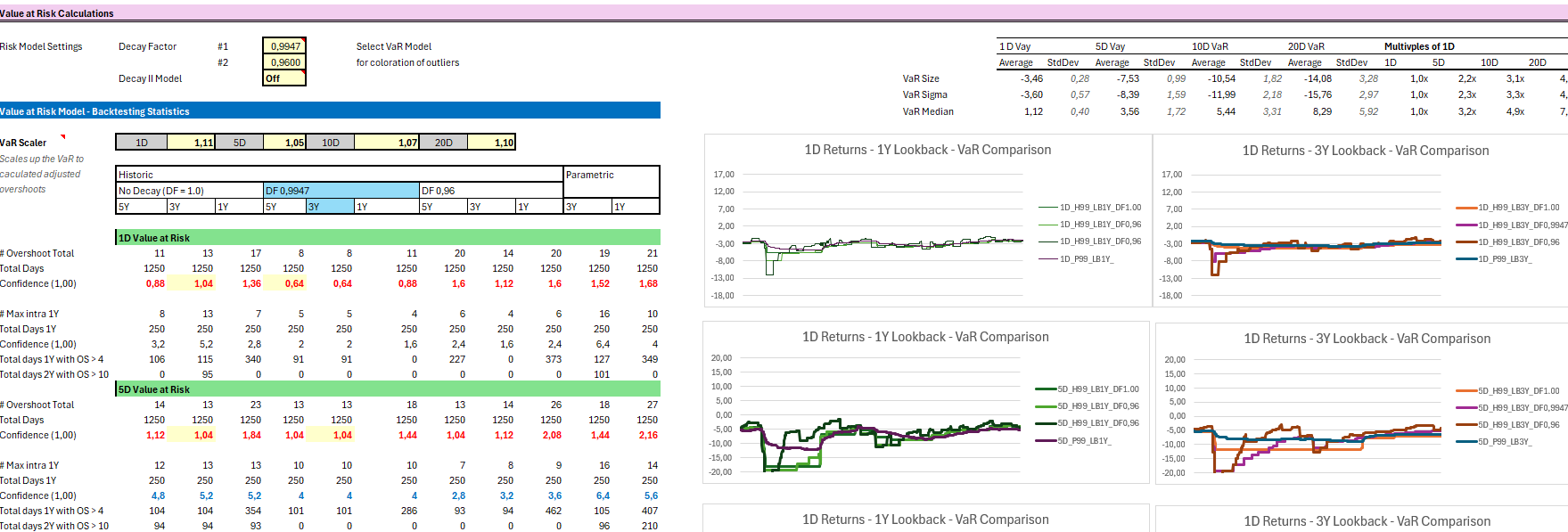

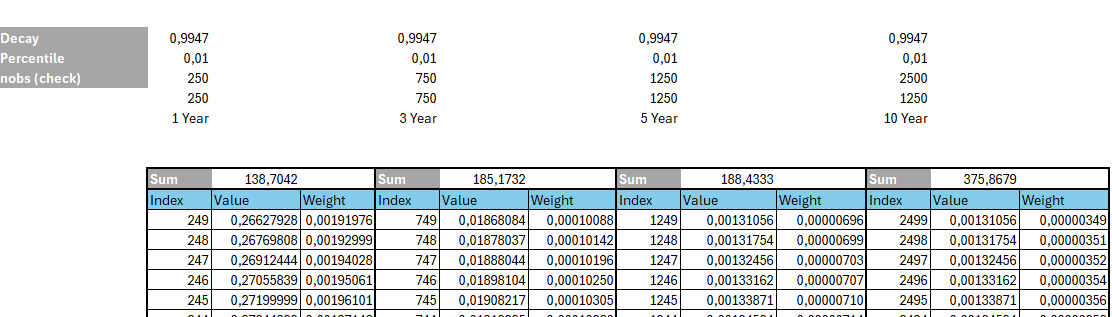

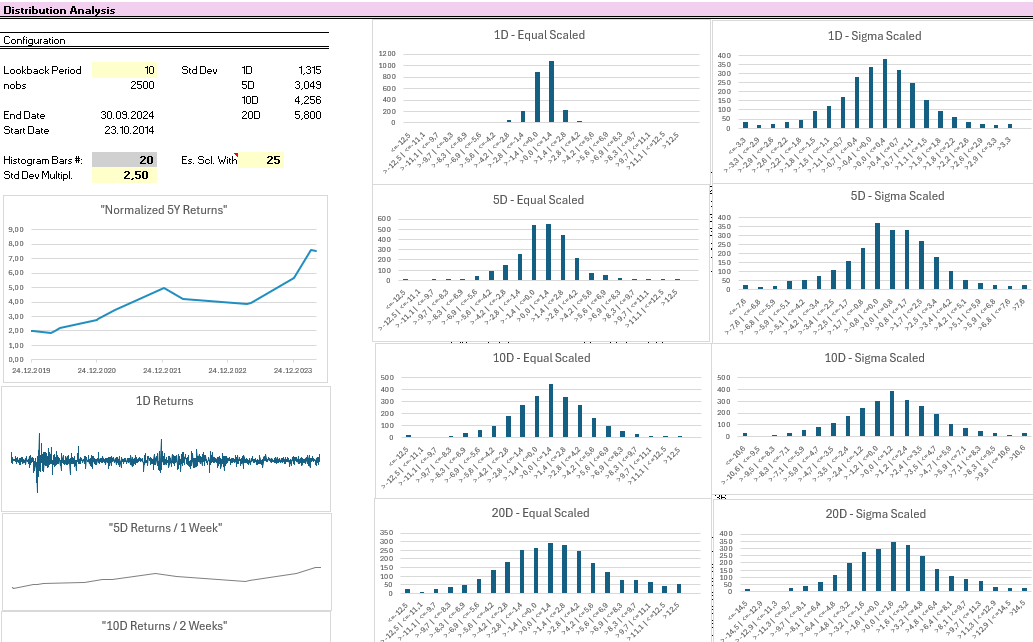

The tool shows you all you need to build your own Value at Risk Model on top of your portfolio. It can be used to define loss limits and manage the Value at Risk to stay an inch away of those limits. Or to rebalance the portfolio or add hedges to trim the Value at Risk. The art of using VaR for portfolio risk management is really about tracking the distributional risk inside of a correlated set of assets. This tool does not run complex Monte Carlo, but it provides you 10+ settings that you can validate for historical and parametric VaRs and helps you find the right model for your set of companies.

You should know where to get time series for your stocks. Currently the model is set up for 2006 - 2024 and the analysis is covering 5

I t hink the model uses Lambda functions which older versions of Excel do not support. Apart from that, it is plain vanilla without VBA and macros.