Originally published: 27/04/2023 15:09

Publication number: ELQ-69306-1

View all versions & Certificate

Publication number: ELQ-69306-1

View all versions & Certificate

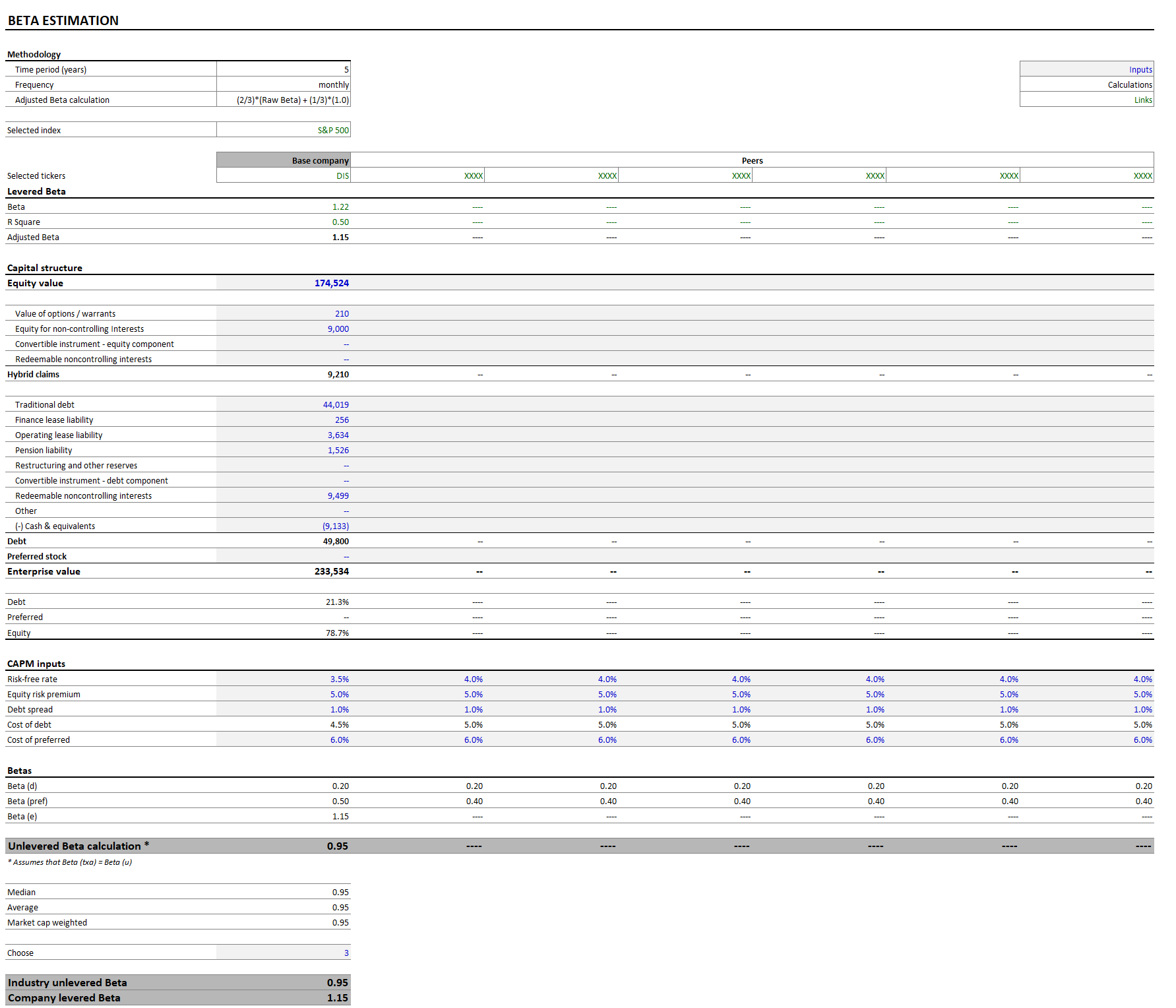

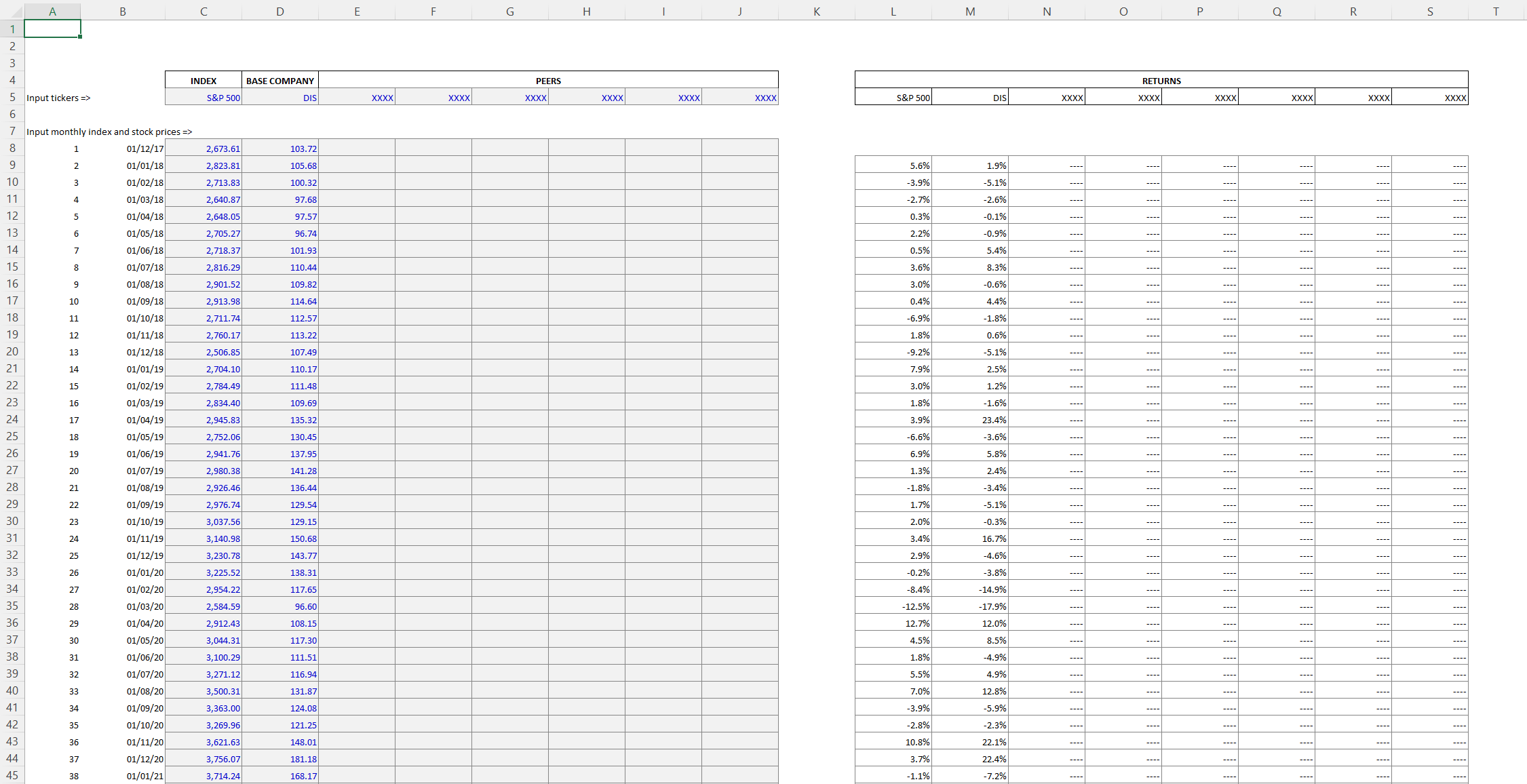

Calculate the Beta of a Stock

Beta is an important input for the CAPM and is calculated by comparing the returns of a particular stock to the returns of the overall market over time

Diverse background in finance, policy-making, and international affairs, with a focus on investment banking, corporate finance, public finance, and multilateral development finance.Follow