Originally published: 30/04/2019 15:22

Publication number: ELQ-19918-1

View all versions & Certificate

Publication number: ELQ-19918-1

View all versions & Certificate

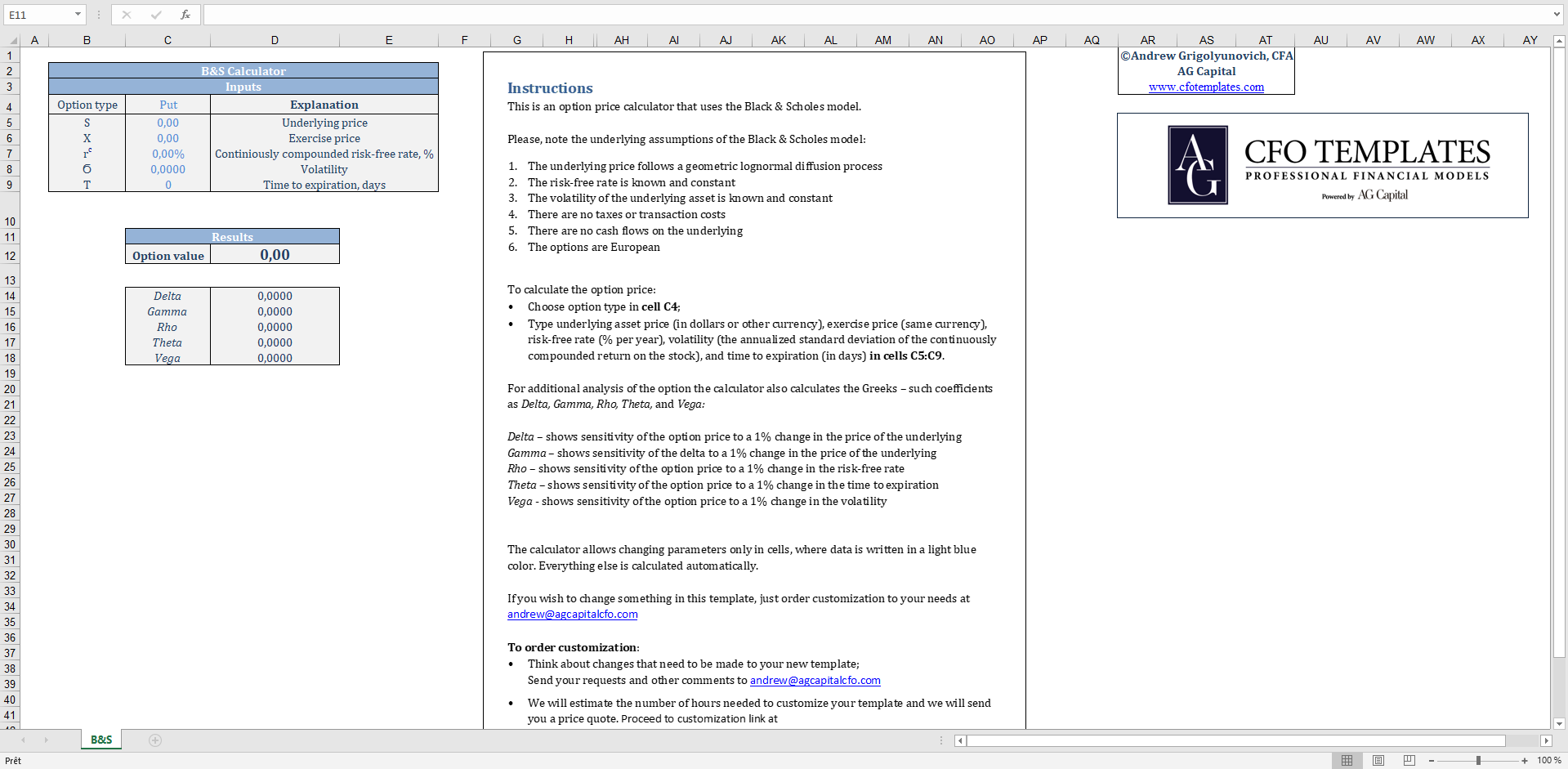

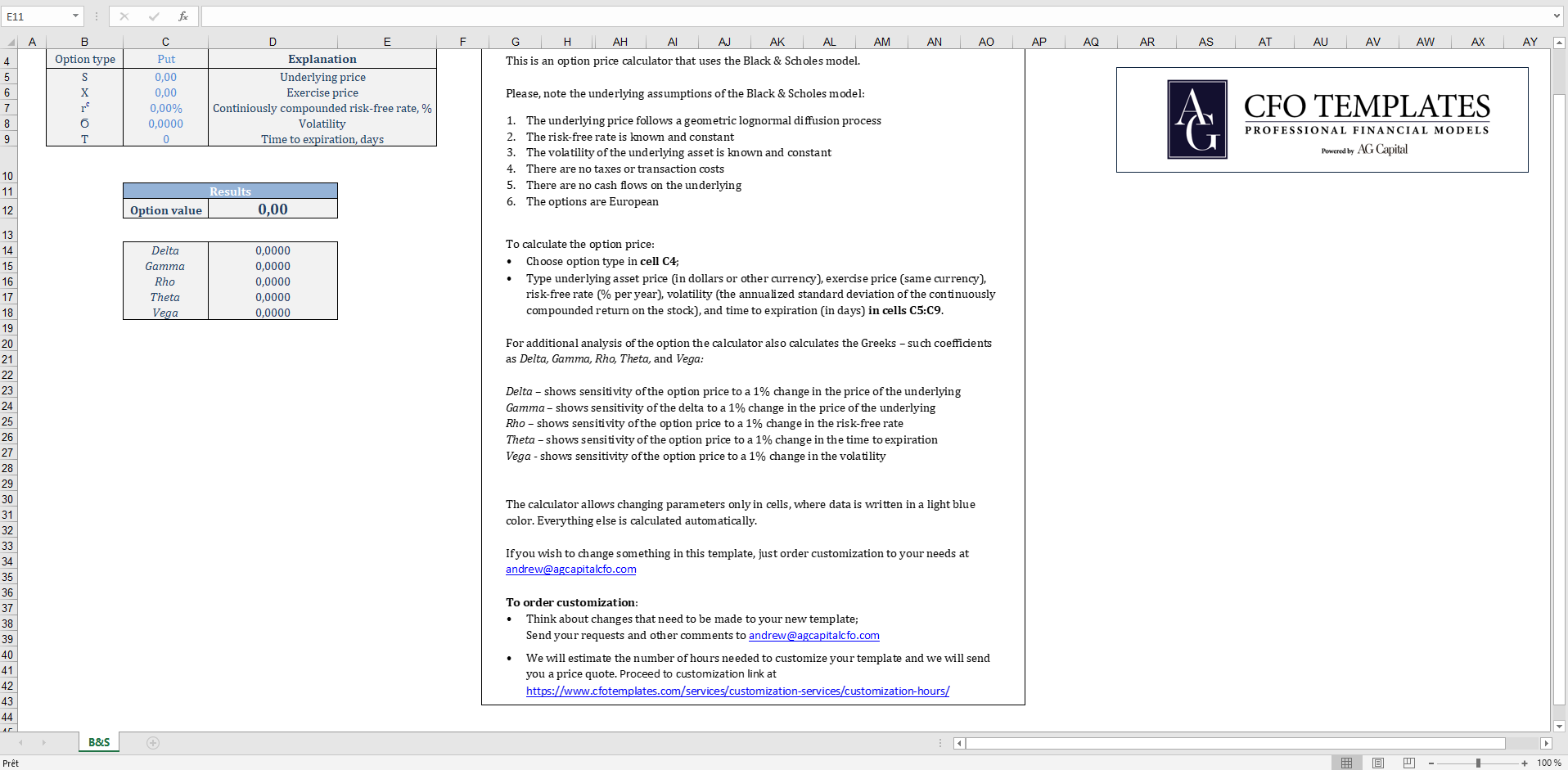

Black-Scholes Option Price Excel Calculator

Call and put options price calculator that uses the Black-Scholes model for option pricing

Andrew Grigolyunovich, CFA, CFM, FMVA offers you this Best Practice for free!

download for free

Add to bookmarks