Originally published: 21/09/2018 13:30

Publication number: ELQ-48334-1

View all versions & Certificate

Publication number: ELQ-48334-1

View all versions & Certificate

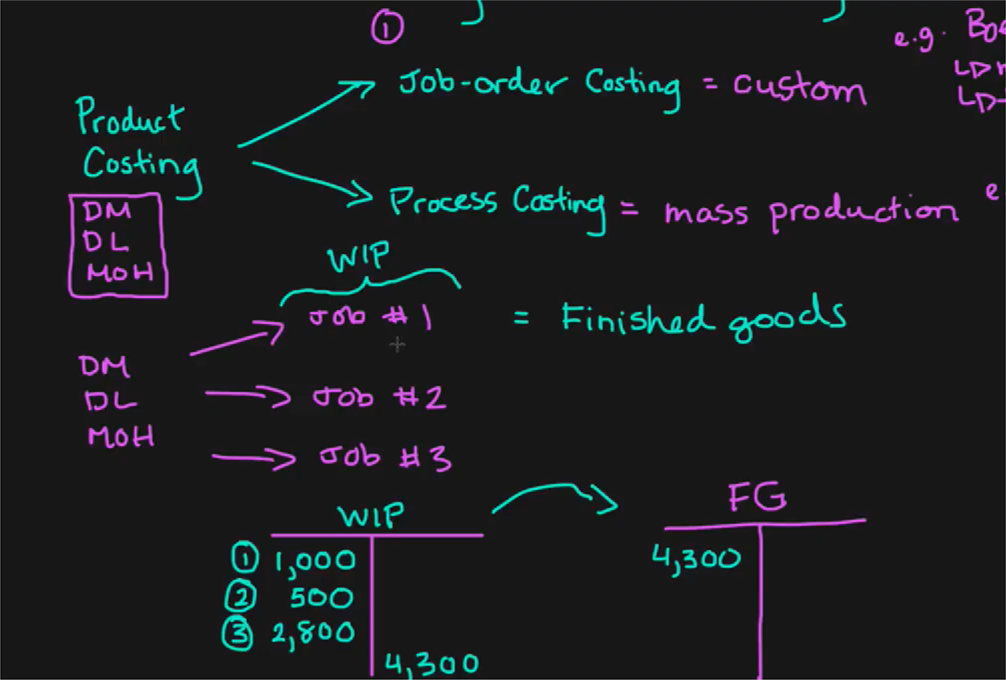

Job Order Costing vs Process Costing

A tutorial on the difference between Job Order Costing and Process Costing.

Add to bookmarks

Did David Burrell's Best Practice help you? You can make a small financial contribution to support the author.

helpSupport