Originally published: 29/01/2025 14:25

Publication number: ELQ-60861-1

View all versions & Certificate

Publication number: ELQ-60861-1

View all versions & Certificate

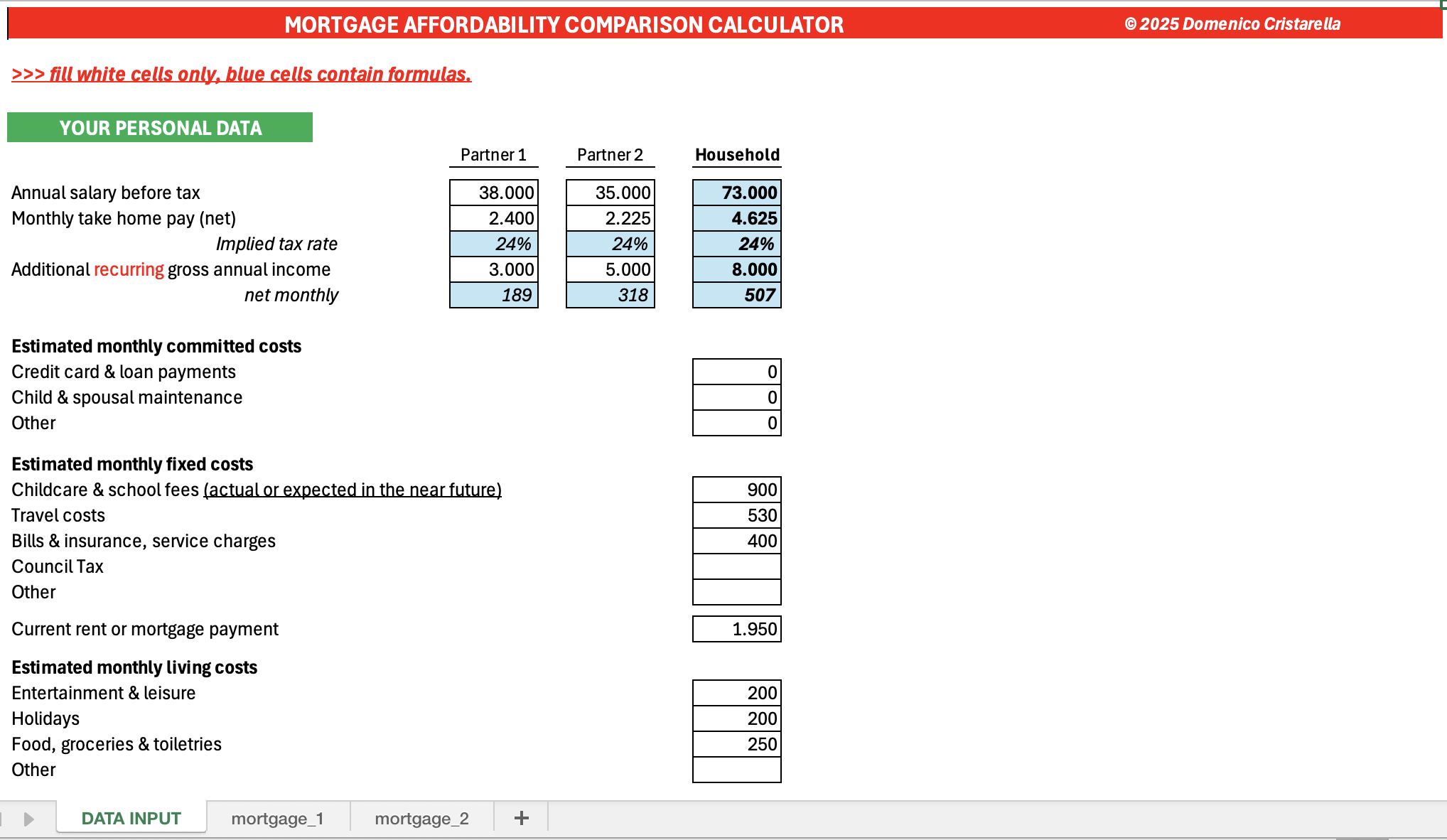

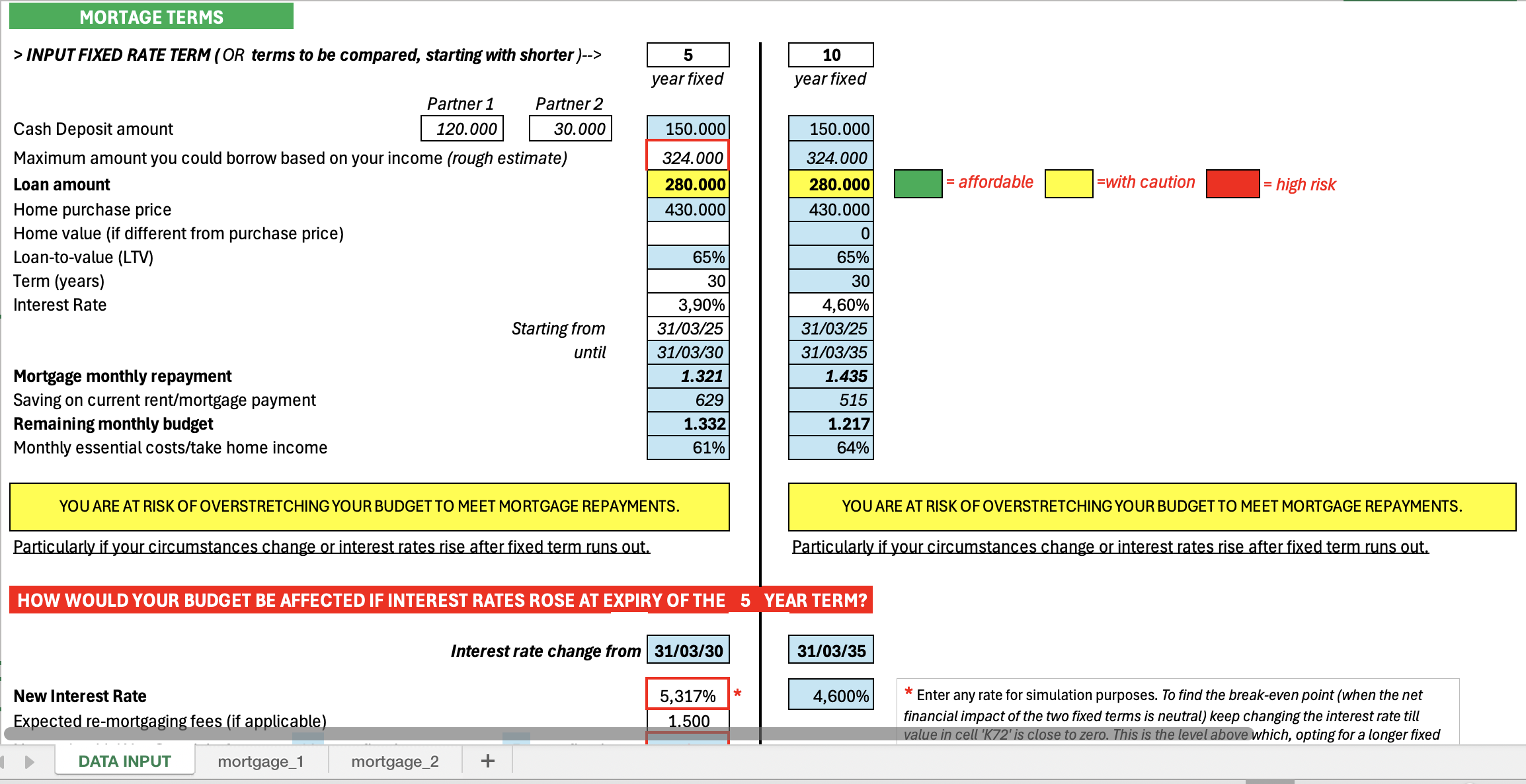

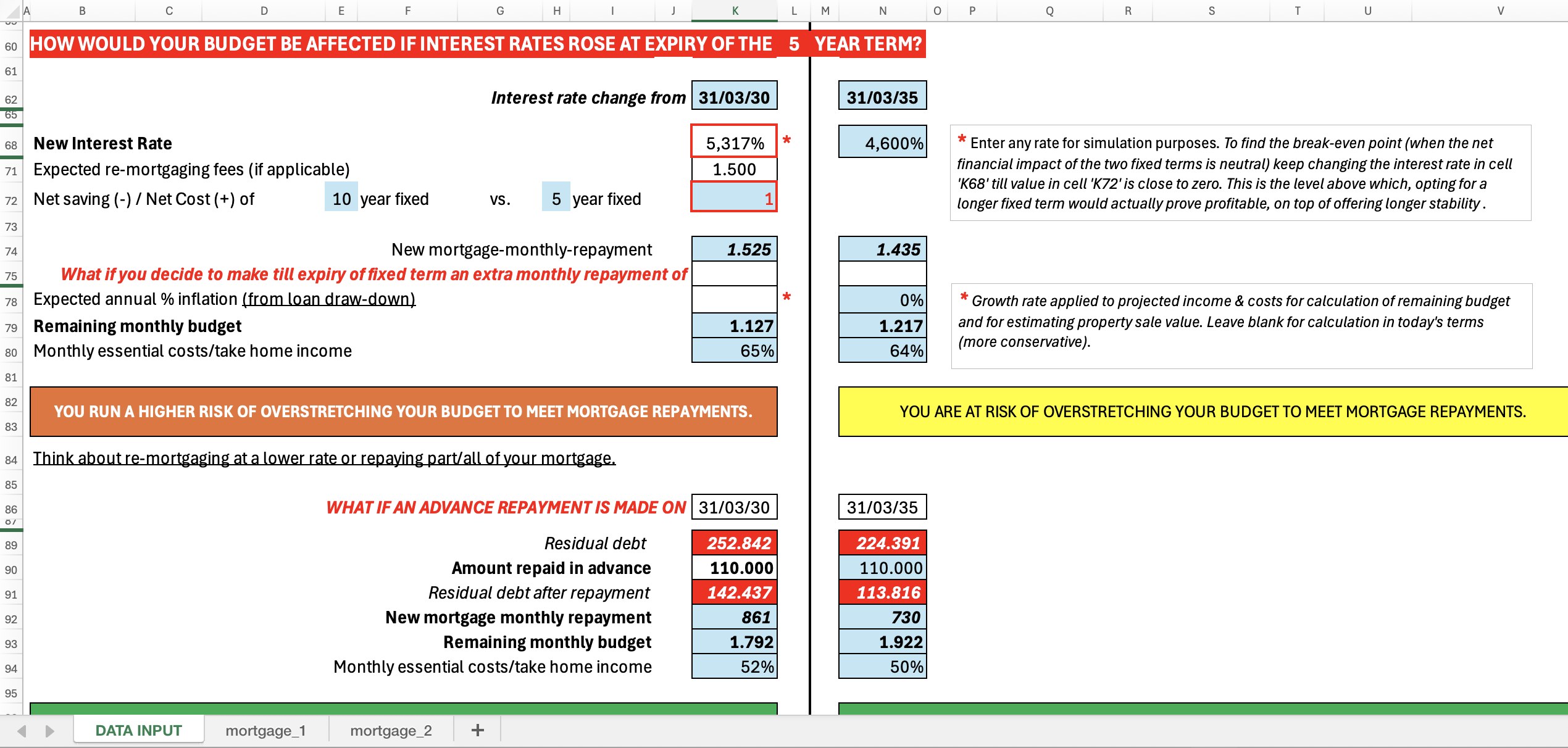

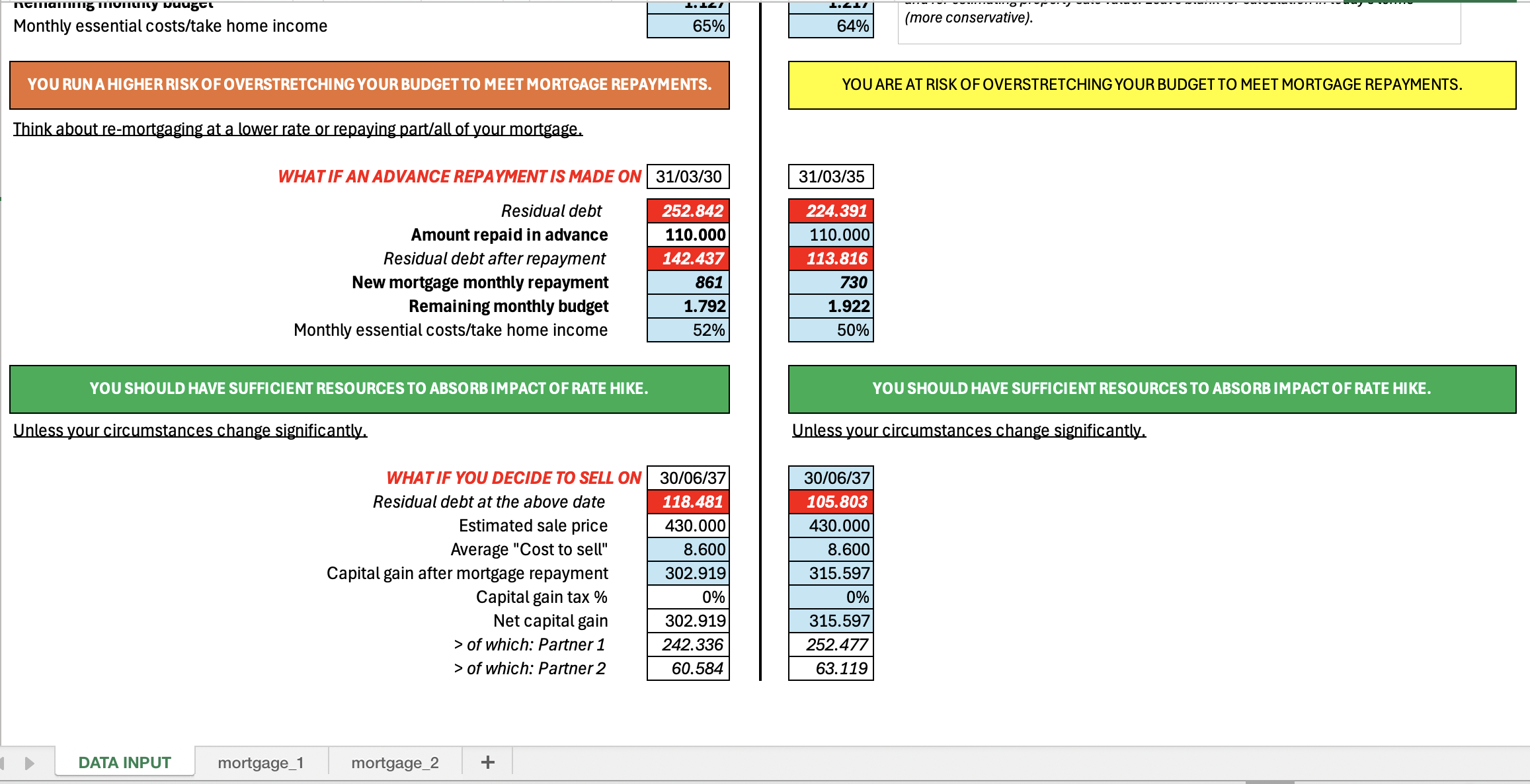

Mortgage affordability comparison calculator

Estimate how much you can afford to borrow to buy a home, based on your current income and expenses, for a maximum of 2 partners and compare offers.

Domenico Cristarella offers you this Best Practice for free!

download for free

Add to bookmarks

Further information

Support informed home buying decisions and best mortgage deal selection.