Publication number: ELQ-29185-1

View all versions & Certificate

Solar PV C&I Model

Solar PV C&I Model — Evaluate a Commercial or Industrial Solar PV Project in Any of 8 Markets, Including Tax Shield and Optional BESS

Further information

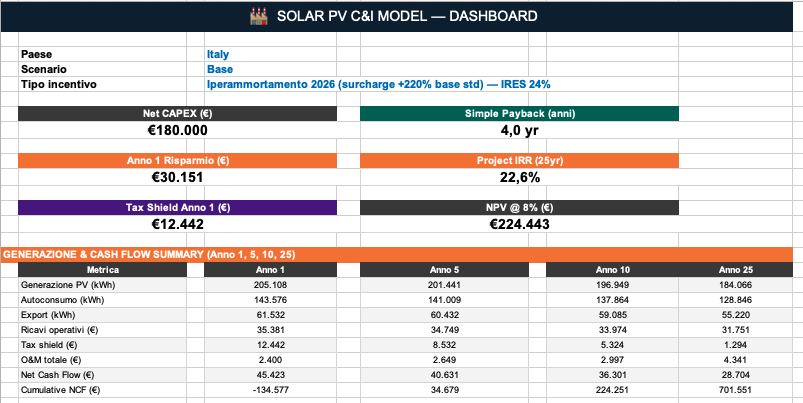

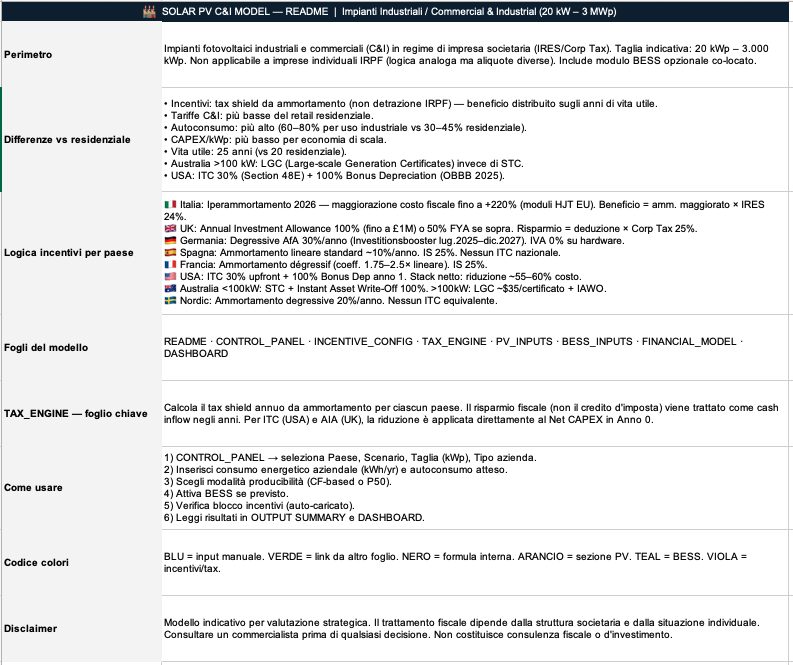

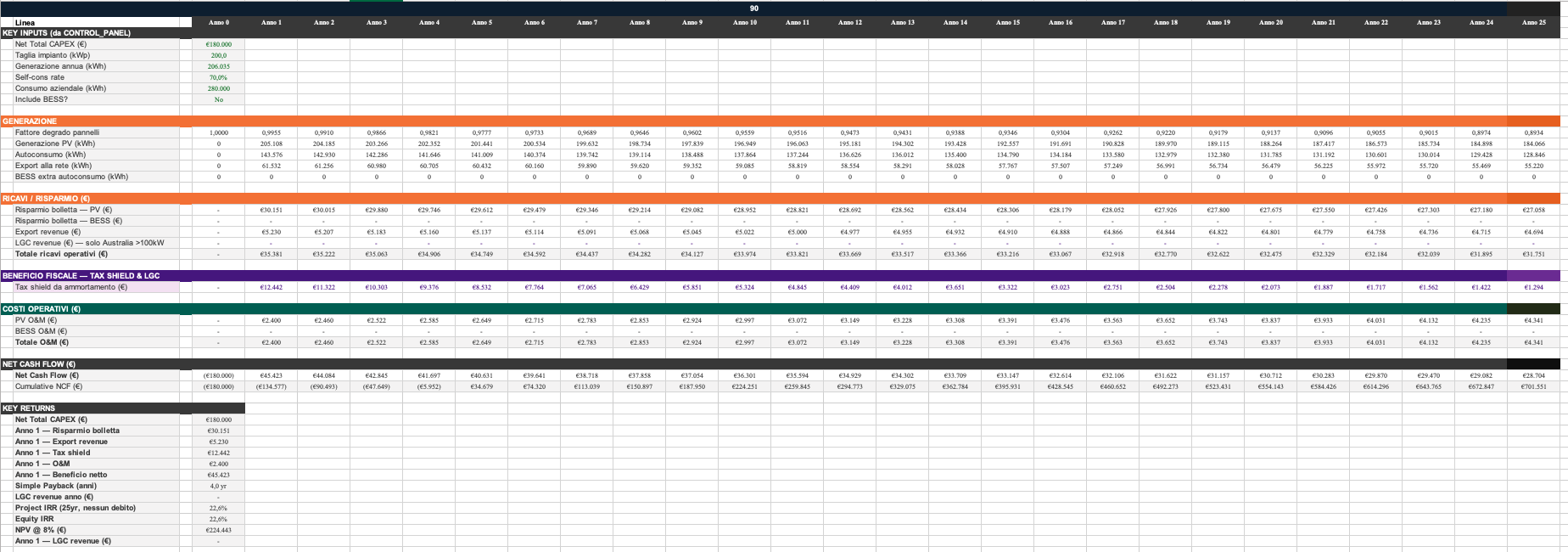

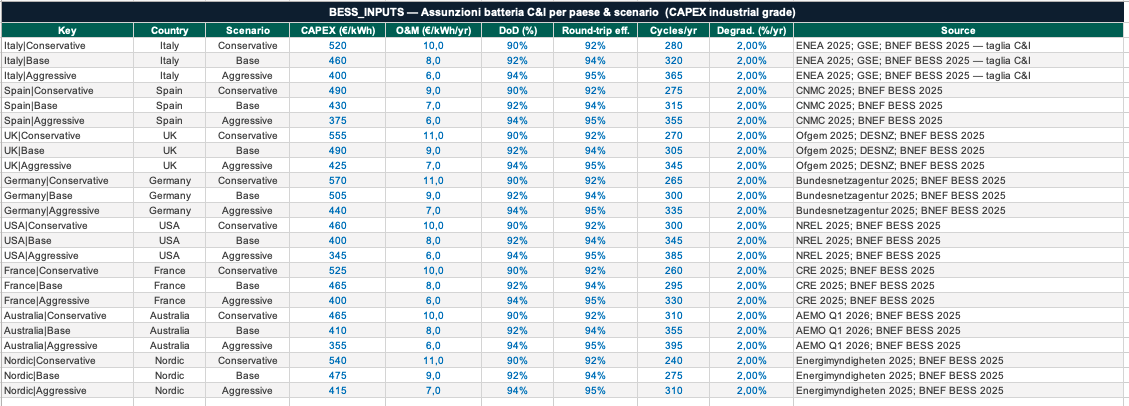

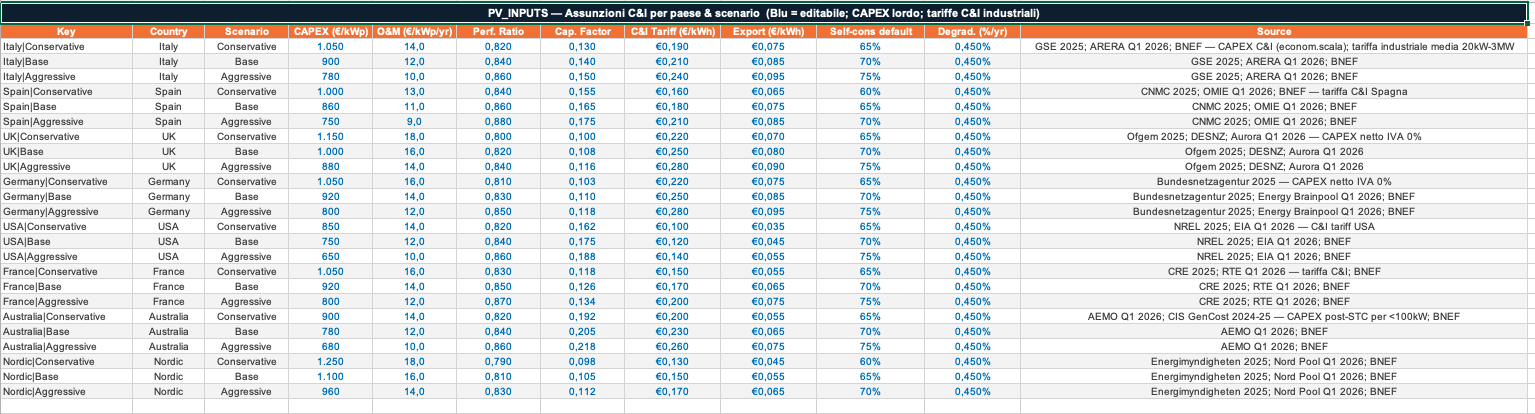

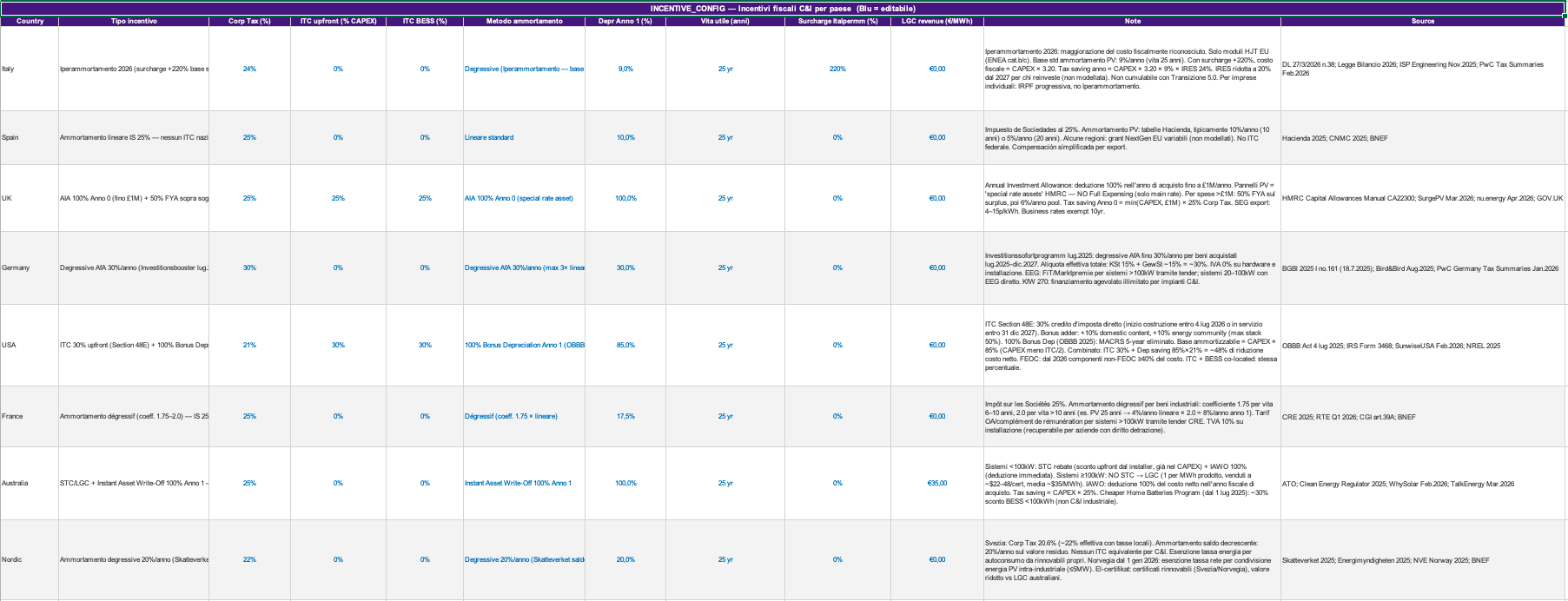

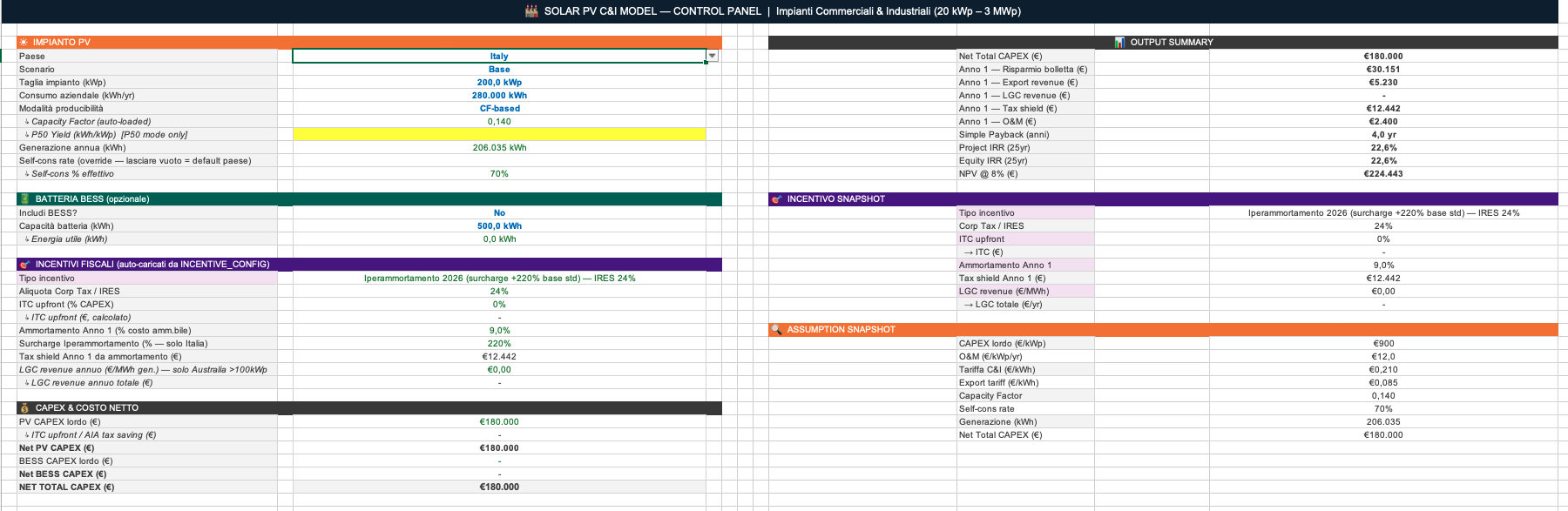

This model enables developers, advisors and corporate energy managers to evaluate the financial viability of a commercial or industrial solar PV project across 8 international markets, capturing the full corporate tax incentive mechanics specific to each country. It calculates bill savings on self-consumed energy using country-specific C&I tariffs, export revenue on grid-injected surplus, and annual tax shield from depreciation using the correct amortisation method and rate for each market — straight-line, degressive or ITC-based. It produces Project IRR, NPV and simple payback from a full 25-year equity cash flow with panel degradation and O&M escalation, and evaluates the incremental value of co-located BESS storage with country-calibrated assumptions across Conservative, Base and Aggressive scenarios.

This model is best suited to commercial and industrial solar PV projects in the 20 kWp–3 MWp range at early-stage feasibility or commercial evaluation, where the company operates under corporate tax — IRES, Corporation Tax, Körperschaftsteuer, Impôt sur les Sociétés or equivalent — and the tax shield from depreciation is a material component of the financial case. It works particularly well for Germany in the Investitionsbooster window (July 2025–December 2027), Italy with Iperammortamento 2026 eligible modules, and USA where the ITC plus Bonus Depreciation stack significantly compresses payback. It is also suited to sites where self-consumption is high — industrial processes running during daylight hours — and to projects considering co-located BESS to increase self-consumption further.

This model is designed for corporate entities under standard corporate tax regimes and is not suited to sole traders or individuals taxed under personal income tax schedules, where the incentive logic and applicable rates differ materially. It does not model debt financing — the cash flow is equity-based — and is therefore not appropriate as the primary tool for a leveraged project finance analysis. It should not be used as the sole basis for a tax planning decision: the specific incentive treatment depends on the corporate structure, the asset classification and individual circumstances, and must be validated with a qualified tax advisor before any investment decision. It is also not designed for utility-scale projects above 3 MWp, which have different tariff structures, grid connection costs and regulatory frameworks.