Originally published: 21/05/2024 07:46

Last version published: 19/12/2024 10:37

Publication number: ELQ-78177-2

View all versions & Certificate

Last version published: 19/12/2024 10:37

Publication number: ELQ-78177-2

View all versions & Certificate

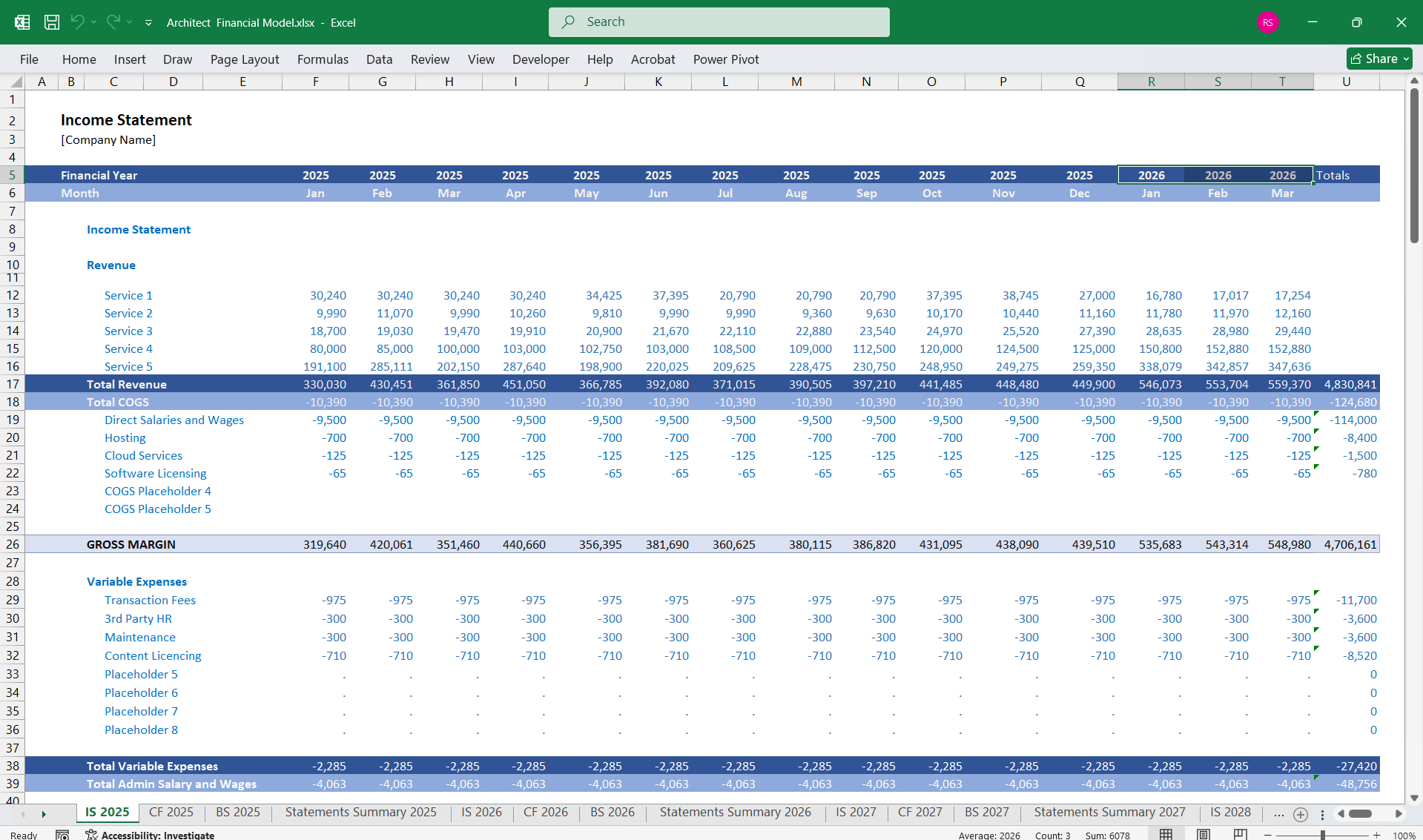

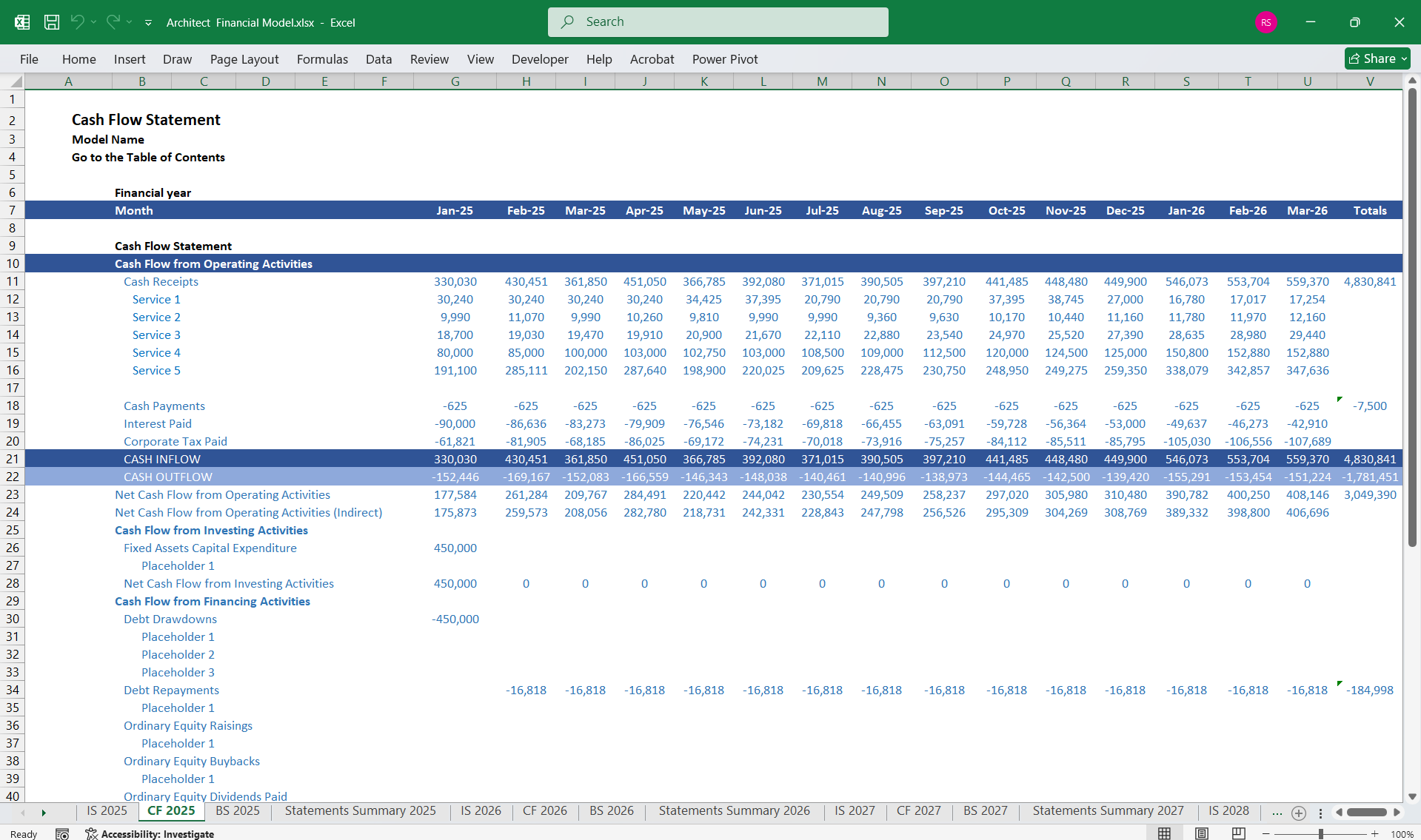

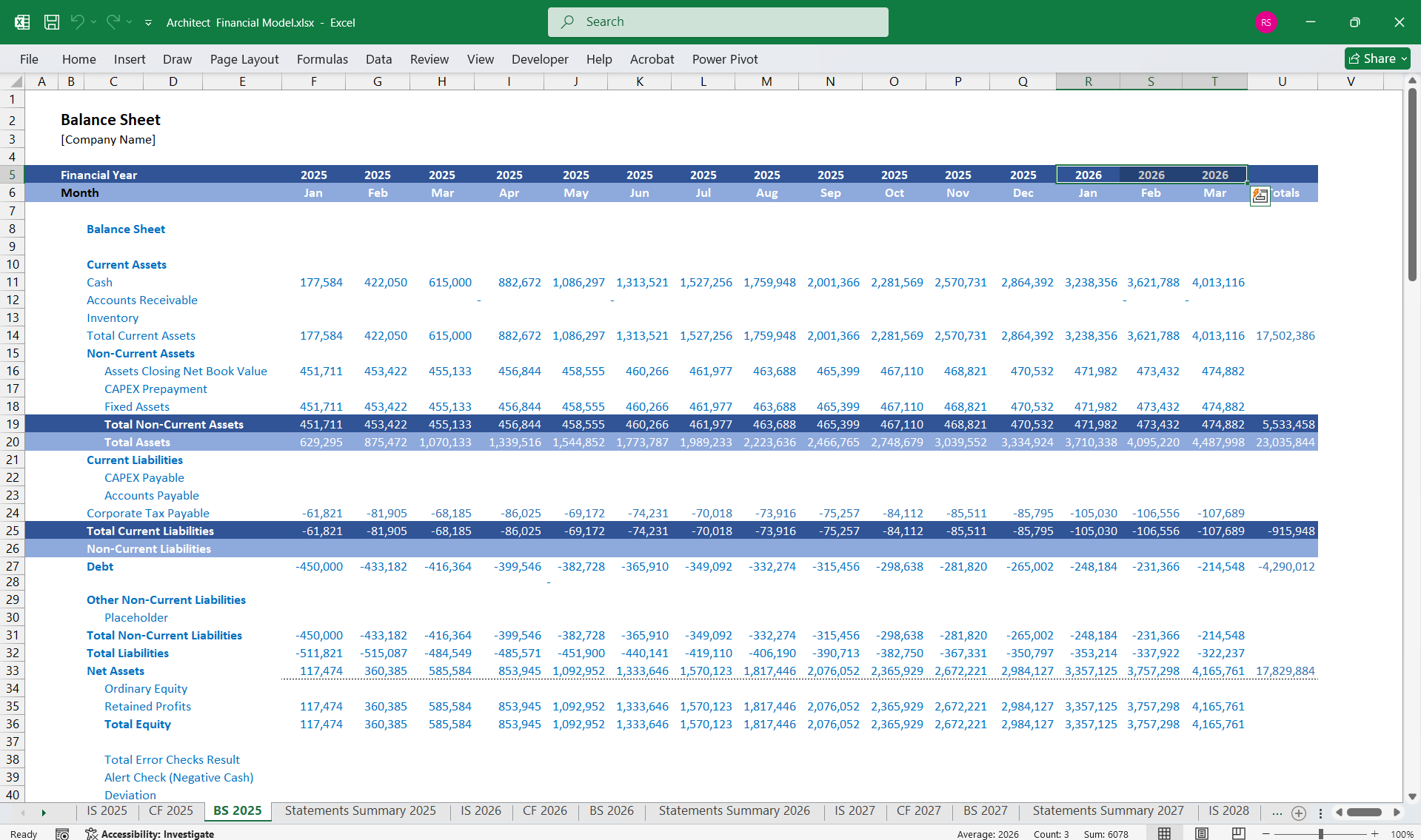

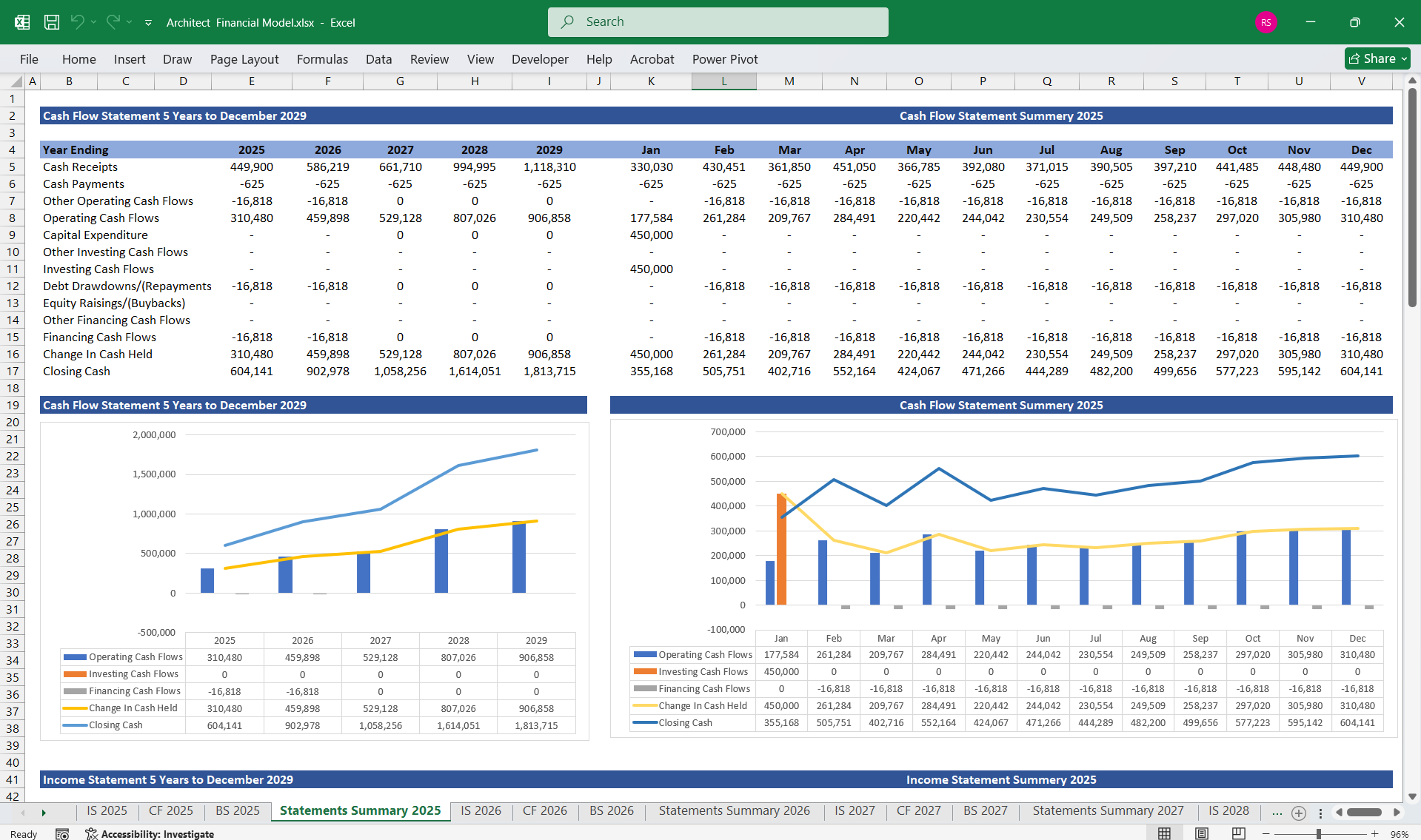

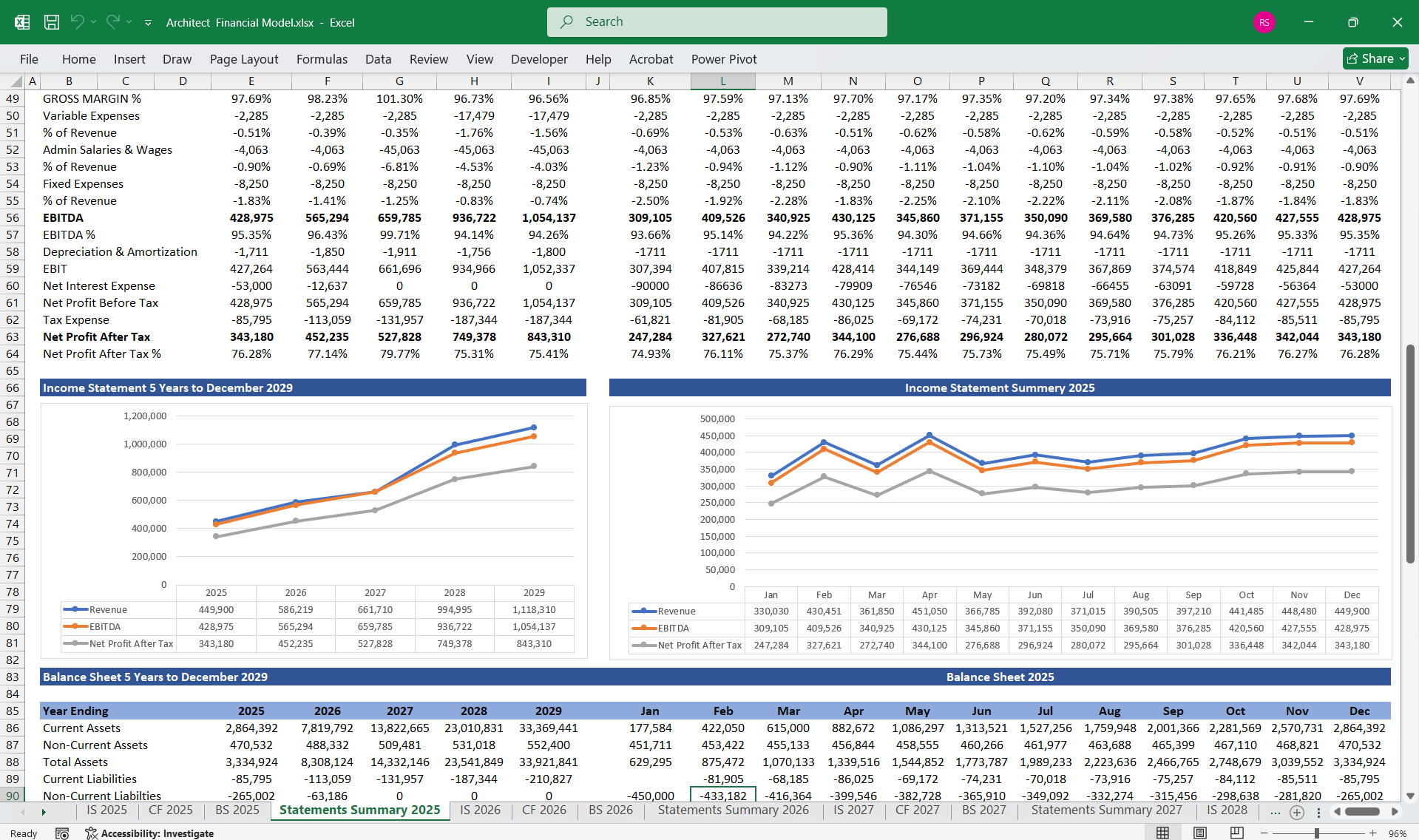

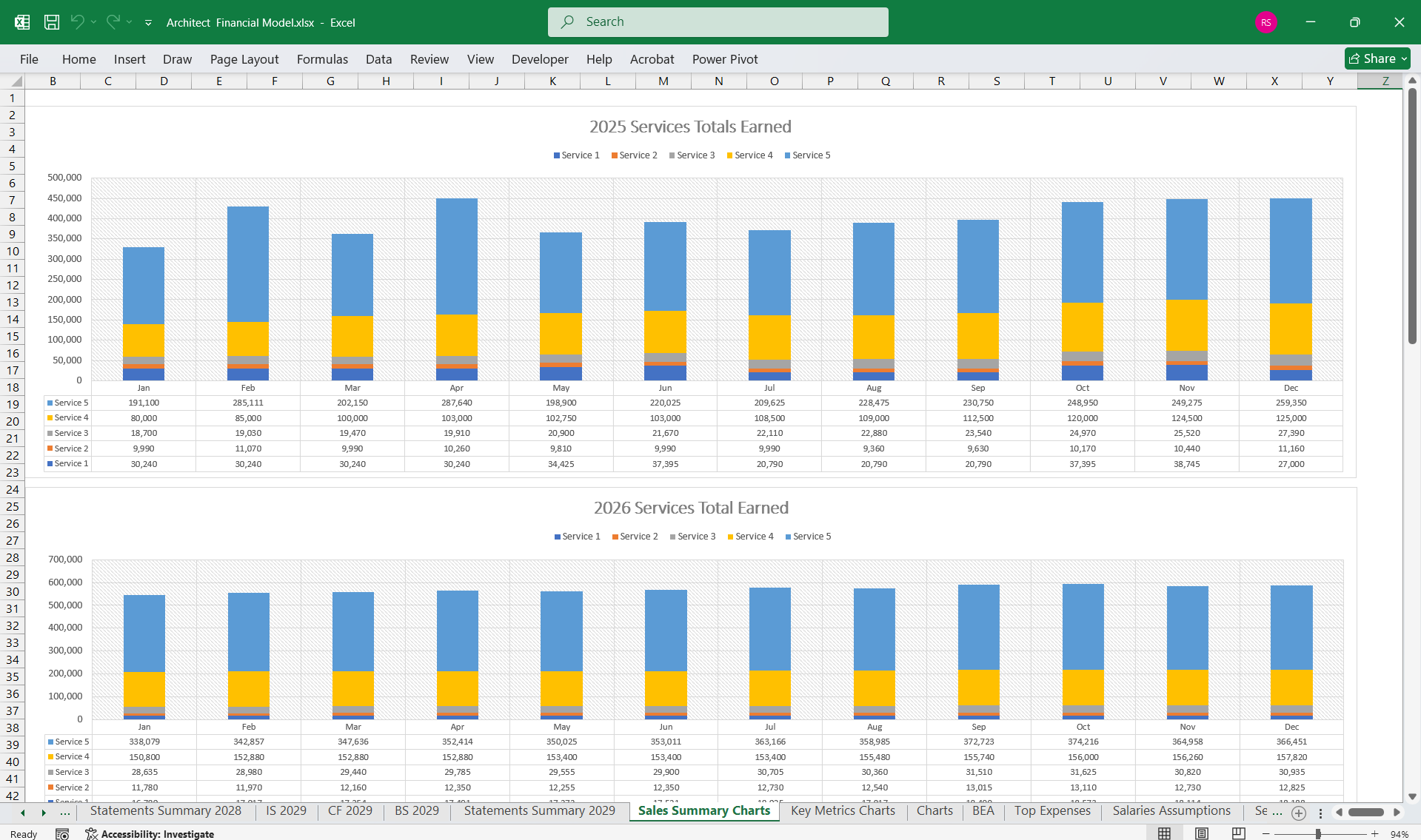

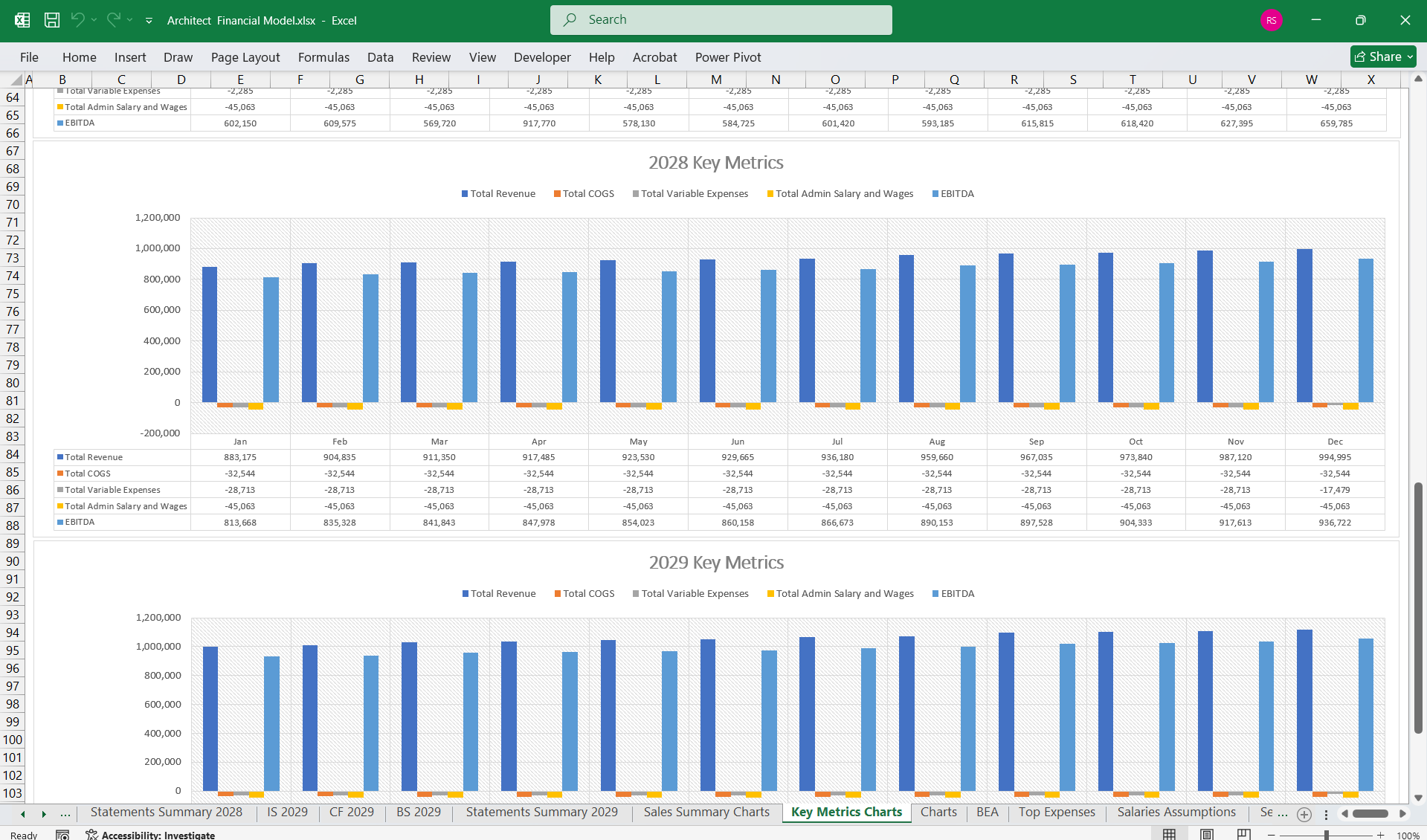

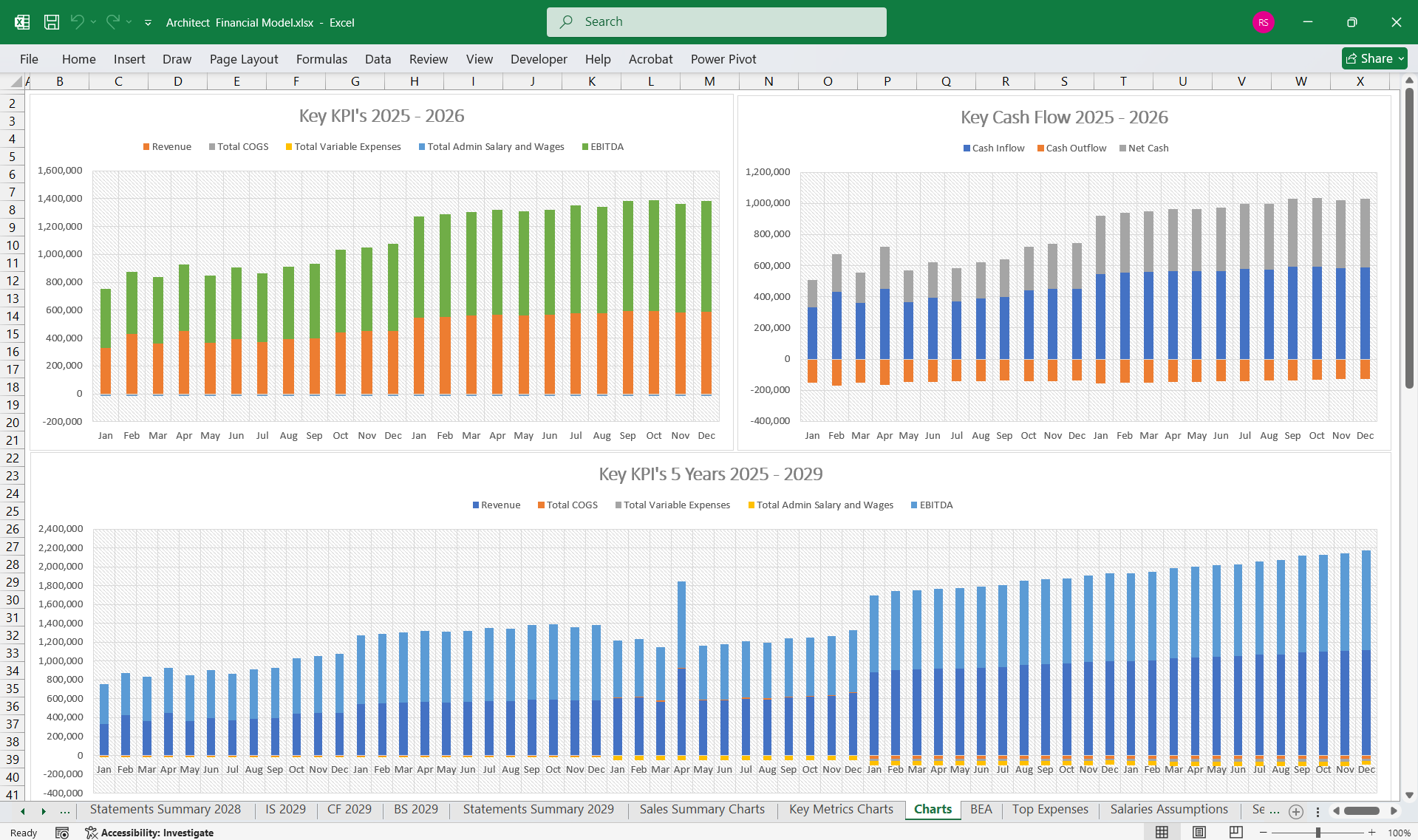

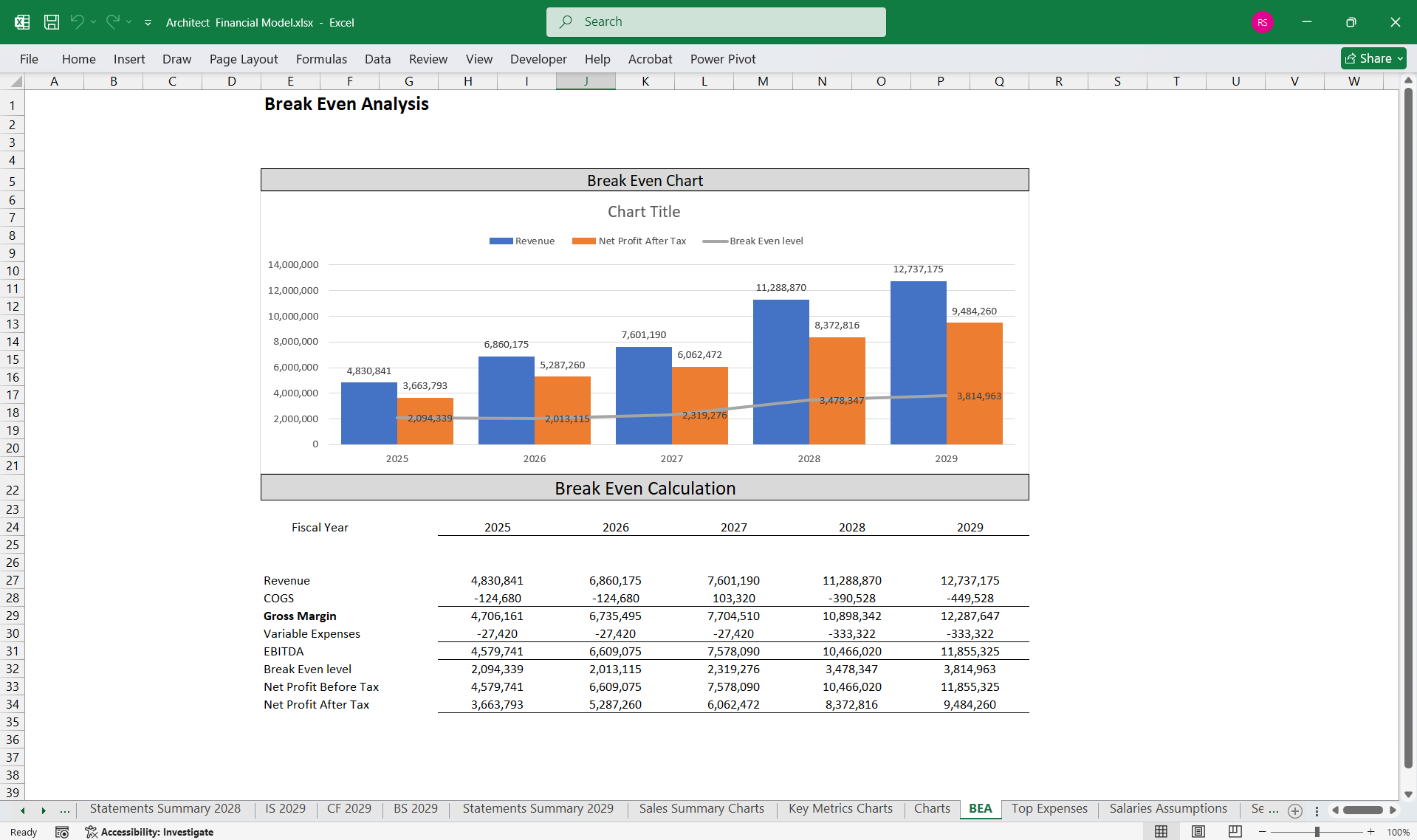

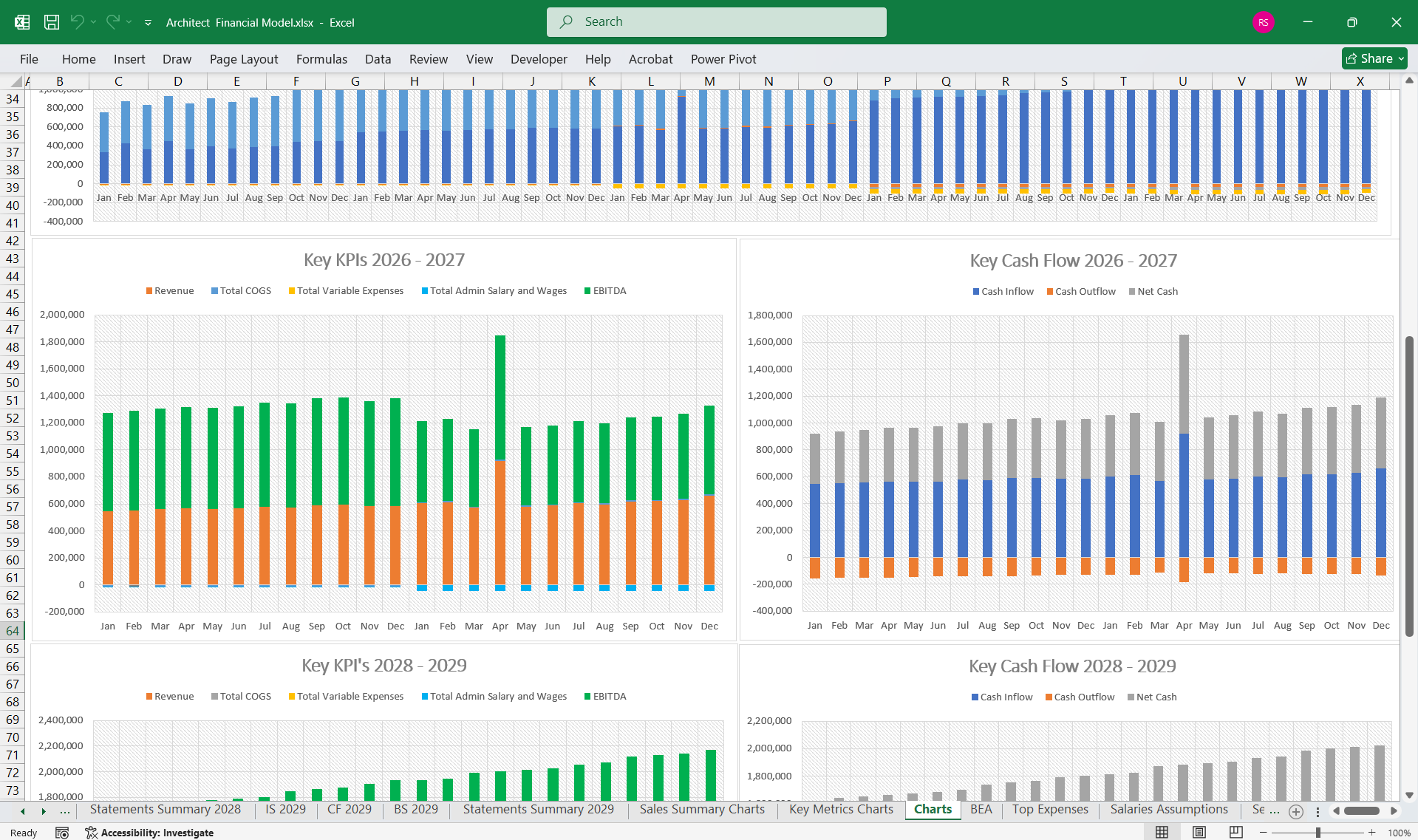

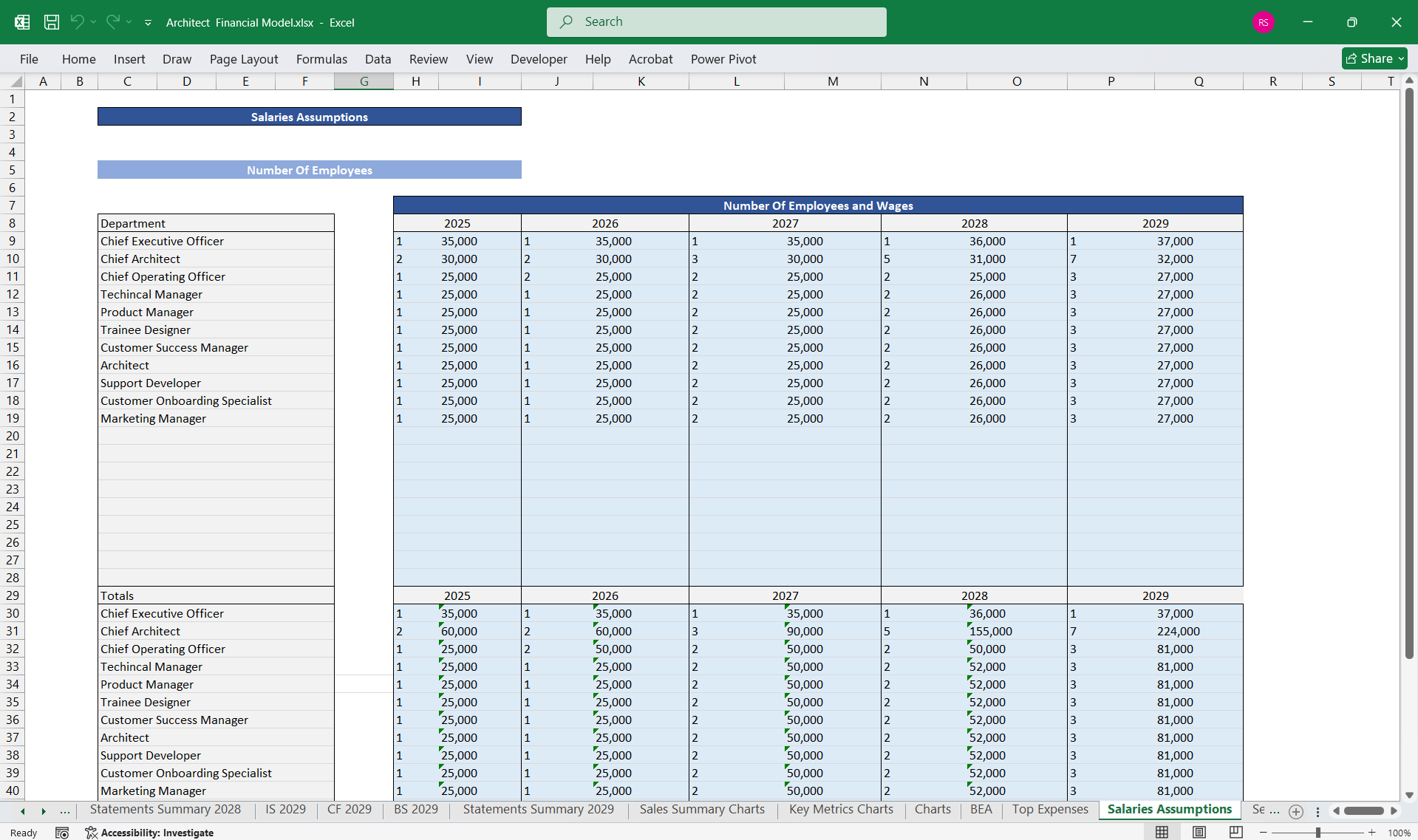

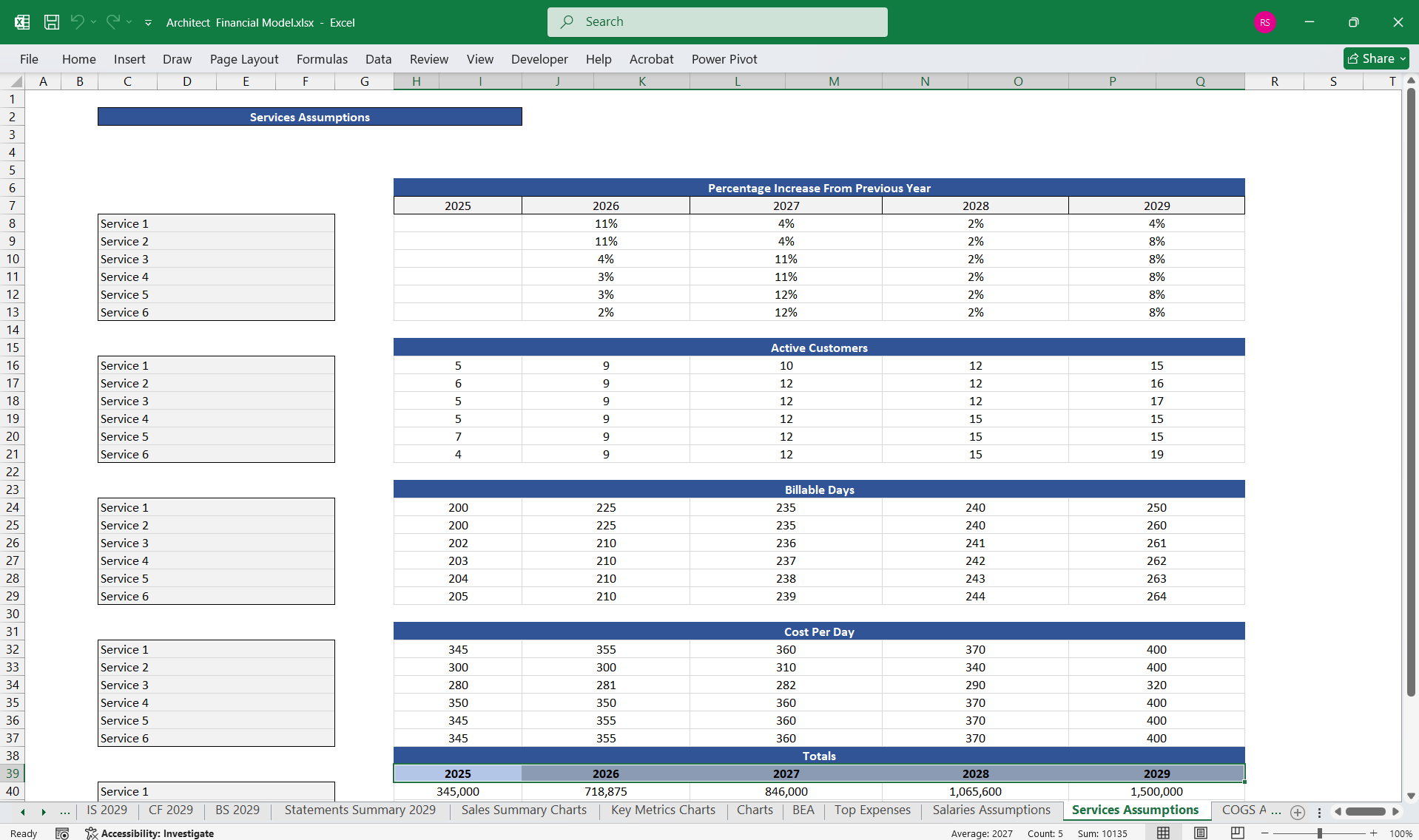

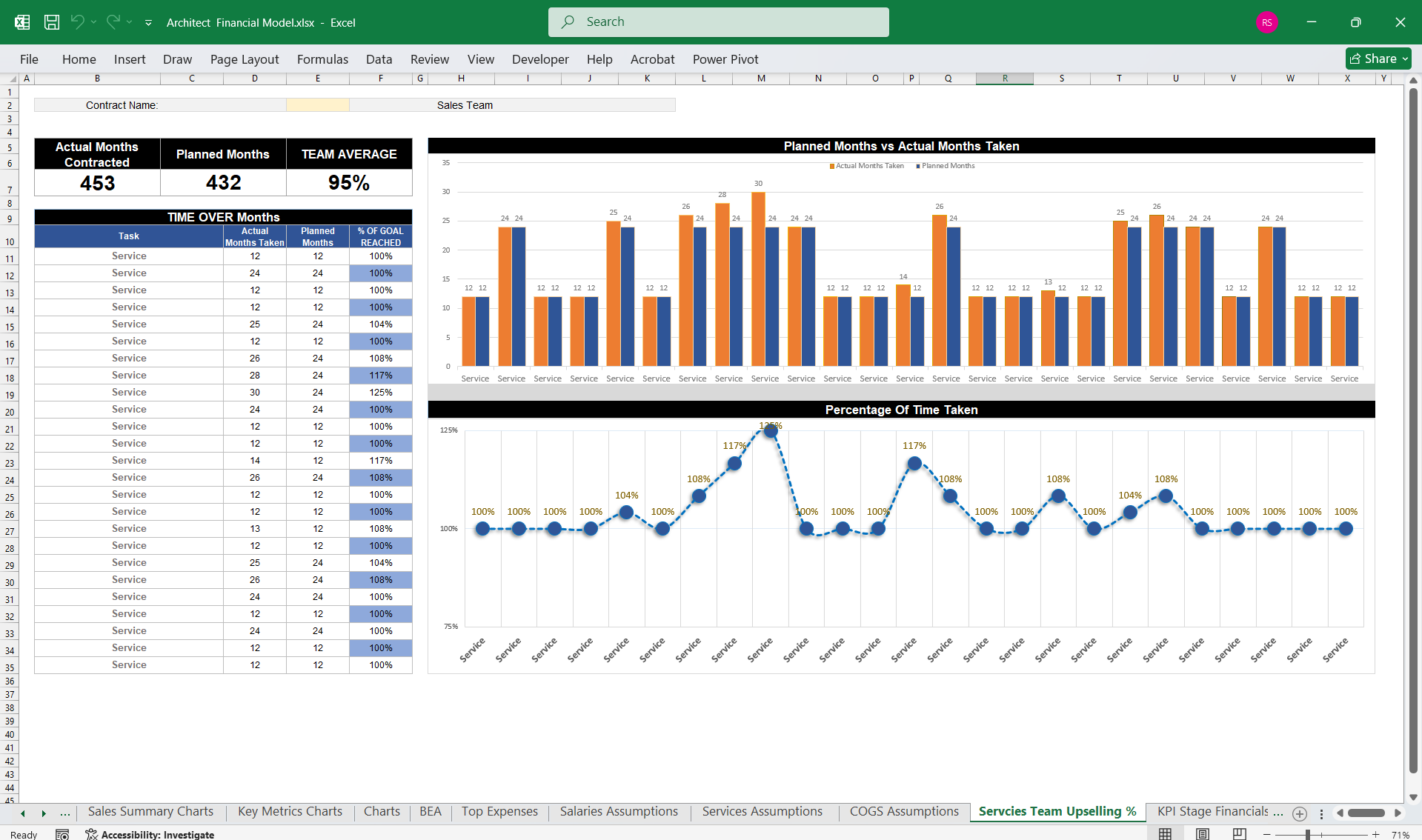

Architect Company Finance Model 5 Year 3 Statement

A comprehensive editable, MS Excel model for tracking Architect Company finances, Income Statements, Balance Sheets, & CF Statements & development revenue.

AllFinancialModels offer a curated selection of high-quality yet financial model templates designed to support a wide range of business needs.Follow

Further information

Provides thorough oversight, tracking, and reporting of architect company finances, including updates on budget utilisation and projections.