Originally published: 07/02/2025 14:27

Last version published: 08/01/2026 16:56

Publication number: ELQ-43728-4

View all versions & Certificate

Last version published: 08/01/2026 16:56

Publication number: ELQ-43728-4

View all versions & Certificate

LNG Plant (Terminal) Financial Model 20 Years 3 Statement

A comprehensive editable 20 Year 3 Statement, MS Excel spreadsheet for tracking an LNG Plant finances.

AllFinancialModels offer a curated selection of high-quality yet financial model templates designed to support a wide range of business needs.Follow

lnglng plantlng terminalliquefied natural gasgasfinancial modelfinancespreadsheettemplateexcel spreadsheet

Description

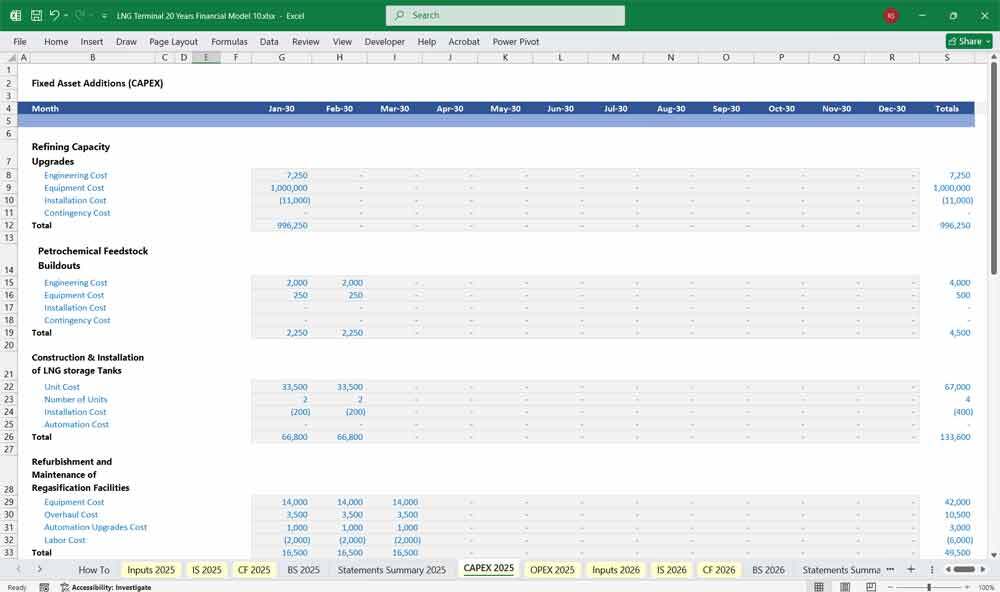

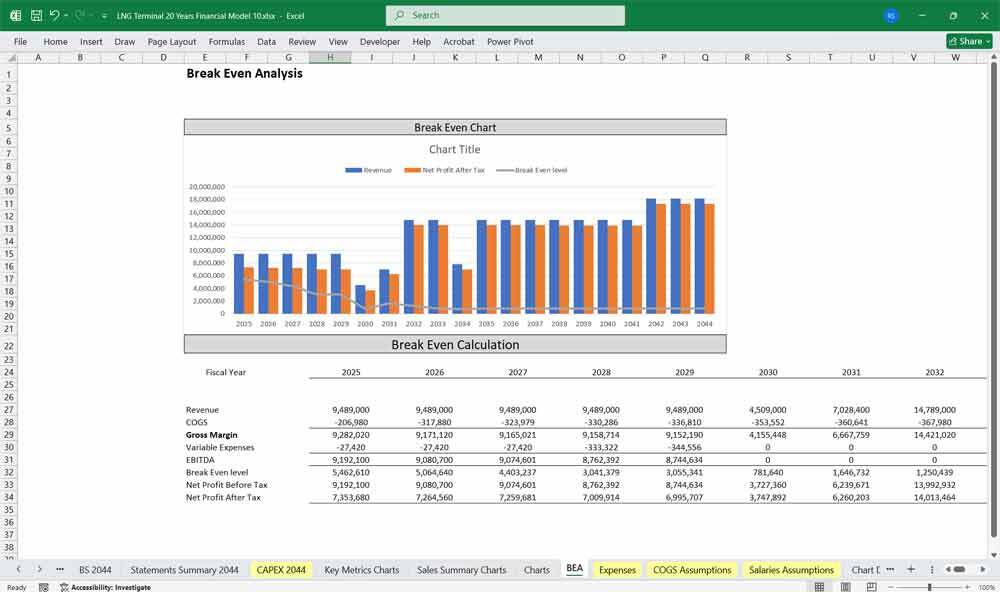

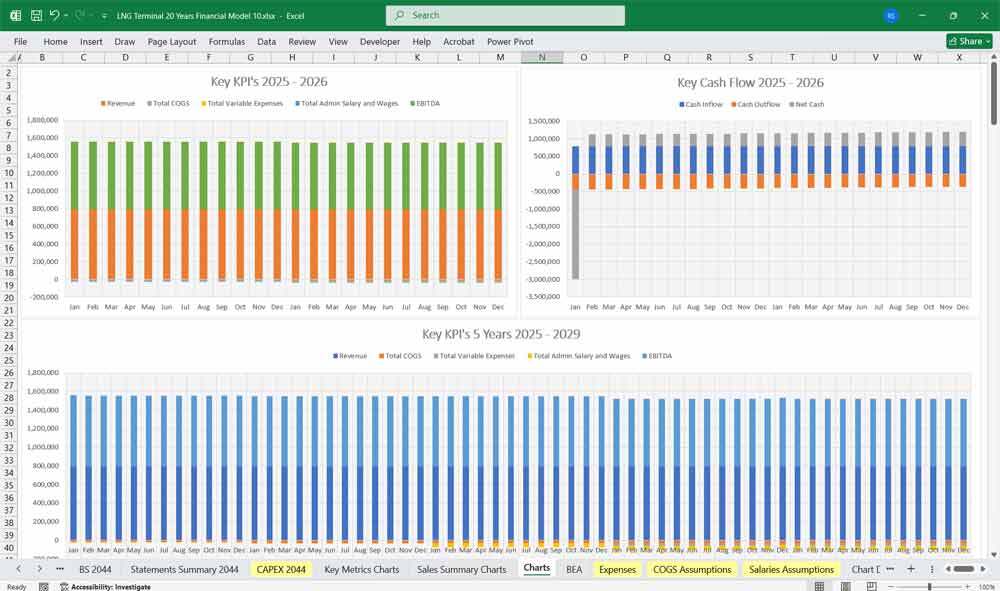

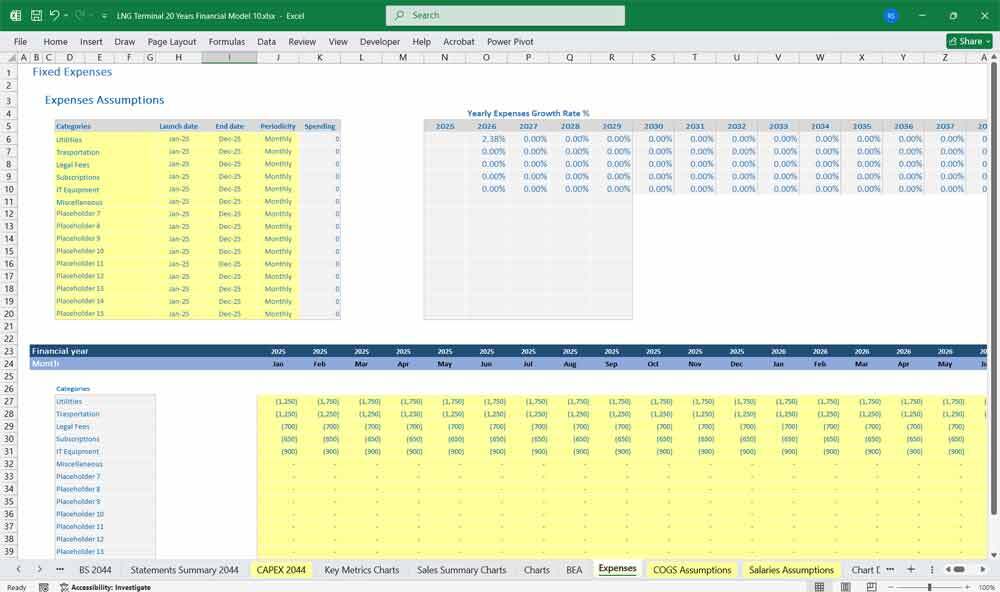

This 3-Statement Financial Model for an LNG (Liquefied Natural Gas) Terminal is a very comprehensive financial tool. 20x Income Statement, Cash Flow Statement, Balance Sheets, and CAPEX Tables to project the financial performance and position of your LNG terminal over 20 years.110-tab Excel Workbook, for unsurpassed financial modeling.

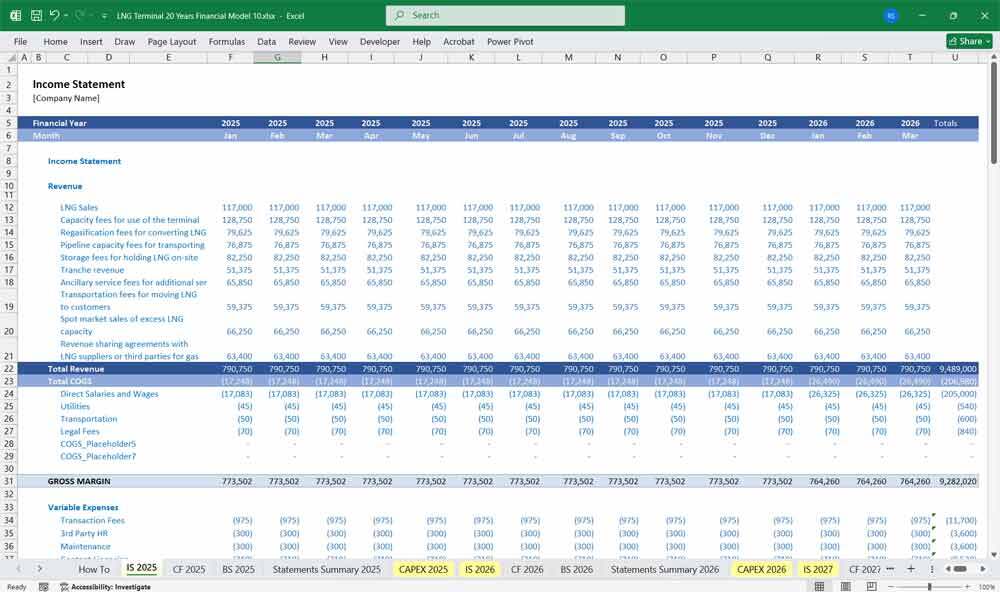

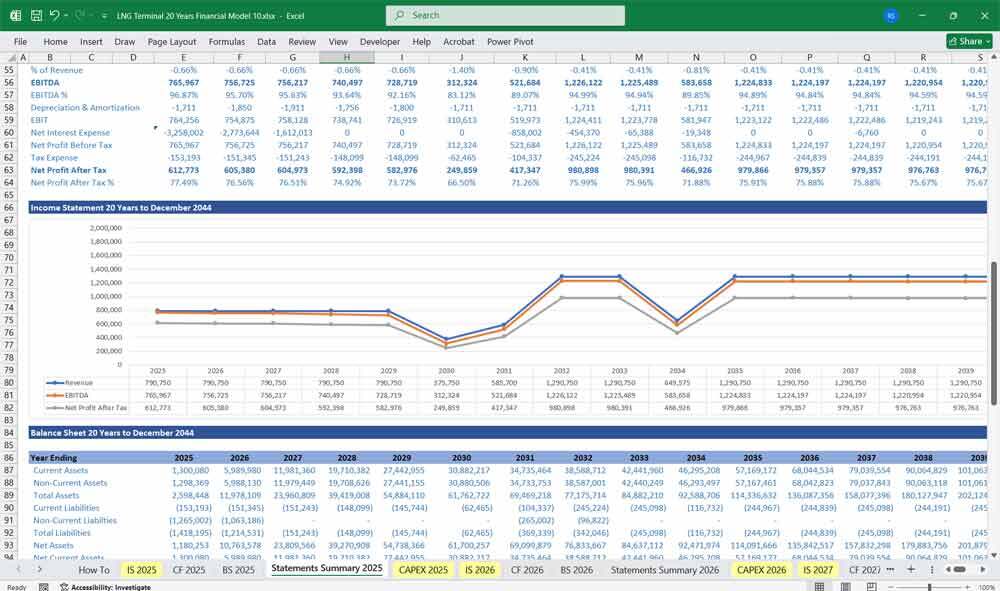

1. Income Statement

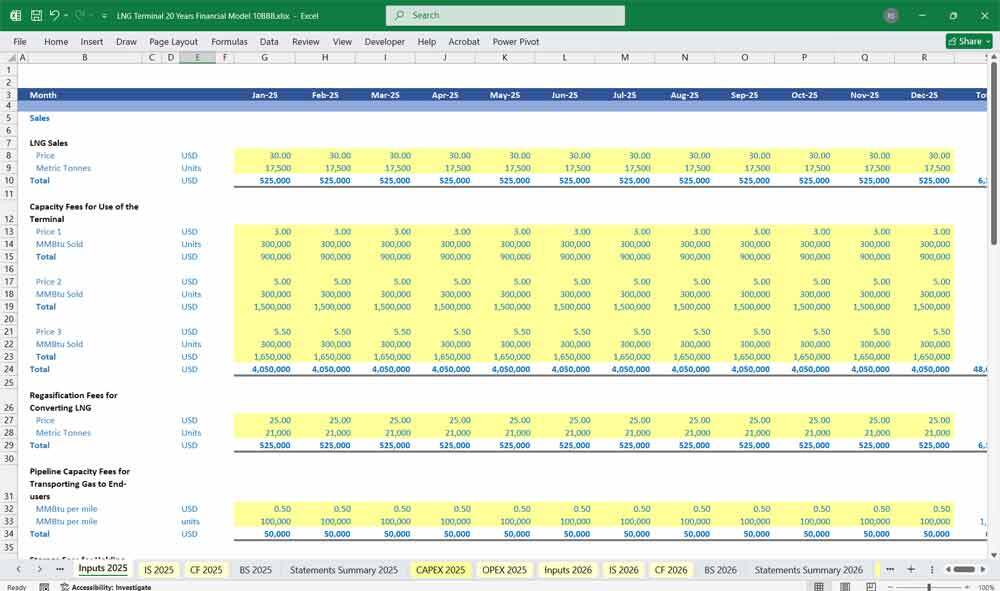

The Income Statement reflects the terminal's profitability over a given period, typically on an annual or quarterly basis. Key line items include:

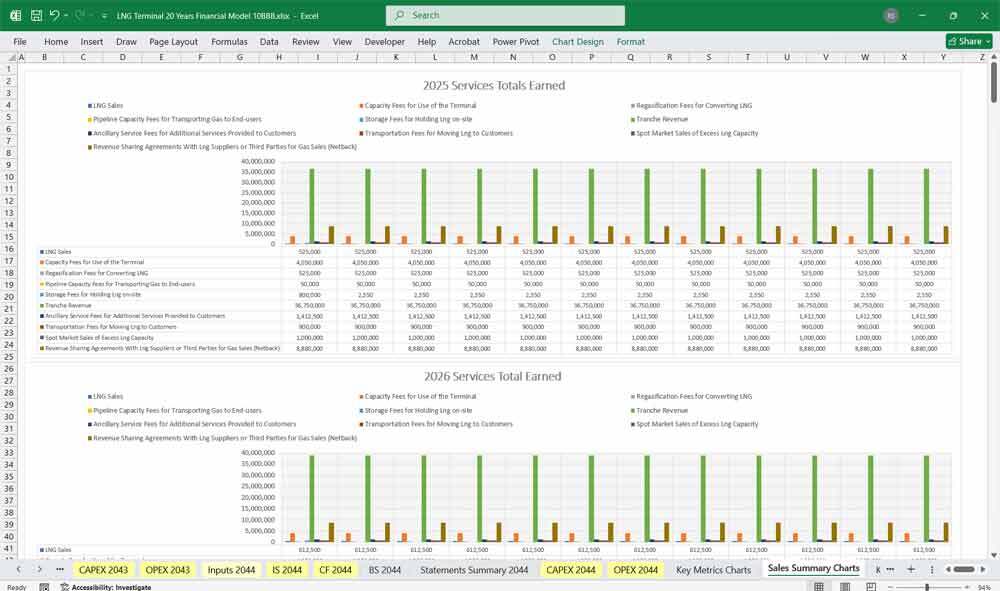

Revenue

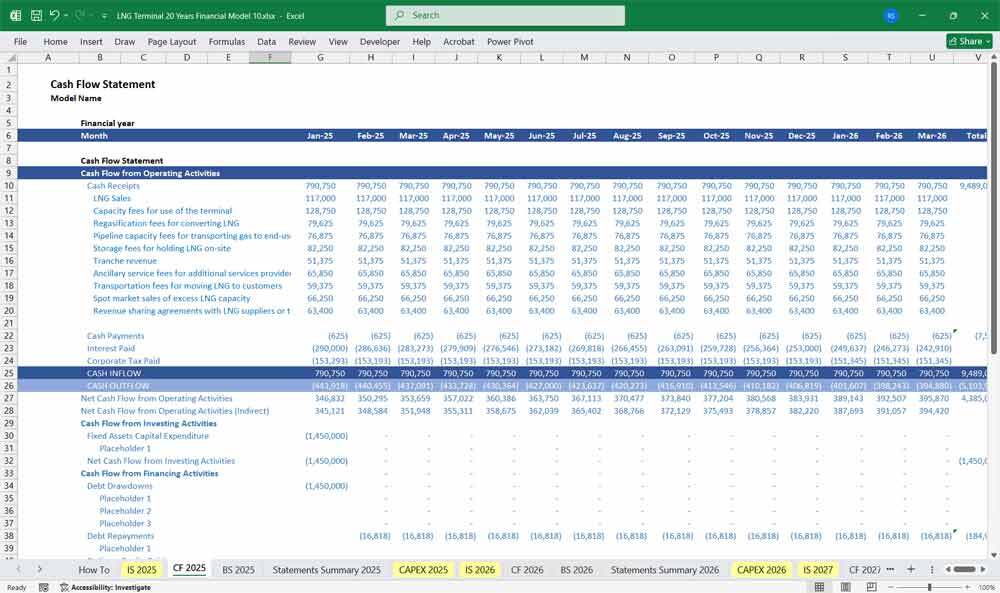

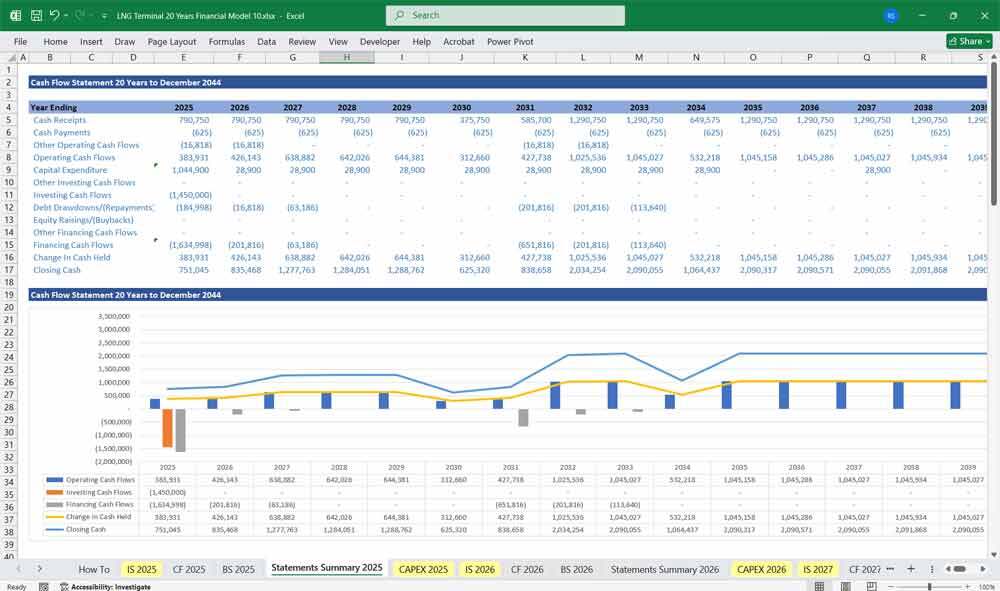

2. Cash Flow Statement

The Cash Flow Statement tracks the cash inflows and outflows, divided into three sections: Operating Activities, Investing Activities, and Financing Activities.

Operating Activities

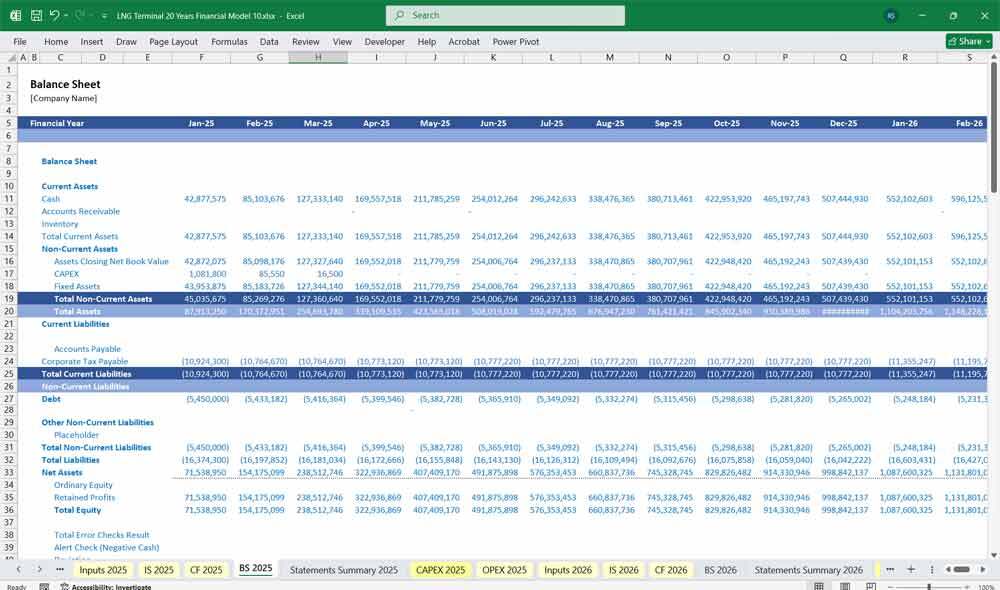

3. Balance Sheet

The Balance Sheet provides a snapshot of the terminal's financial position at a specific point in time, showing assets, liabilities, and equity.

Assets

To build the model, the following assumptions and drivers are critical:

This model provides a holistic view of the LNG Terminal's financial performance, liquidity, and solvency, enabling stakeholders to make informed decisions.

This 3-Statement Financial Model for an LNG (Liquefied Natural Gas) Terminal is a very comprehensive financial tool. 20x Income Statement, Cash Flow Statement, Balance Sheets, and CAPEX Tables to project the financial performance and position of your LNG terminal over 20 years.110-tab Excel Workbook, for unsurpassed financial modeling.

1. Income Statement

The Income Statement reflects the terminal's profitability over a given period, typically on an annual or quarterly basis. Key line items include:

Revenue

- Regasification Fees: Revenue from regasifying LNG for customers (often contracted under long-term agreements).

- Storage Fees: Revenue from storing LNG in the terminal's tanks.

- Tolling Fees: Revenue from processing LNG for third parties.

- Other Revenue: Ancillary services such as truck loading, bunkering, or pipeline access fees.

- Feedstock Costs: Cost of purchasing LNG (if the terminal is involved in trading).

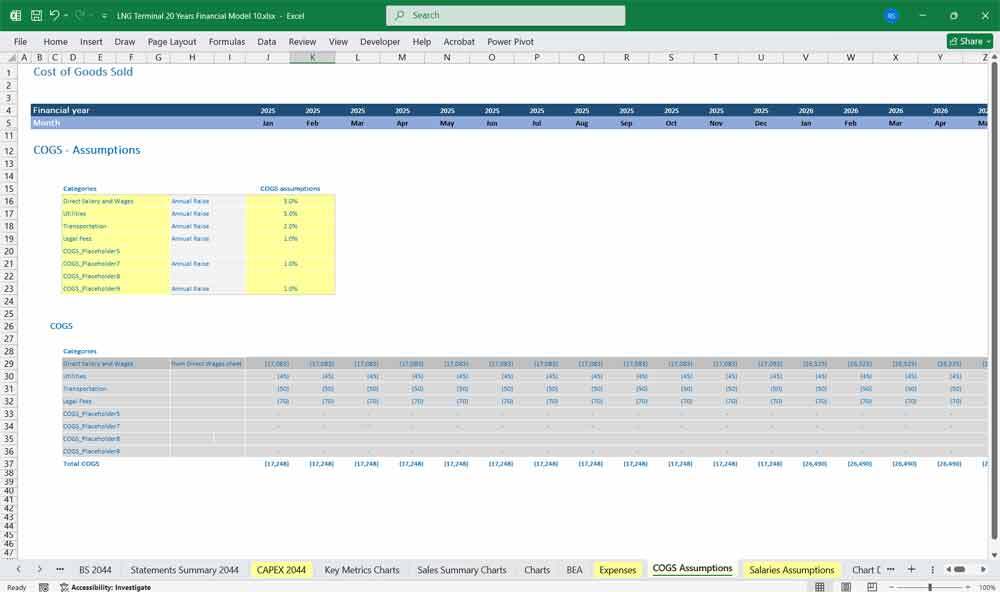

- Utilities: Costs of electricity, water, and other utilities required for operations.

- Maintenance Costs: Regular and scheduled maintenance of the terminal's infrastructure.

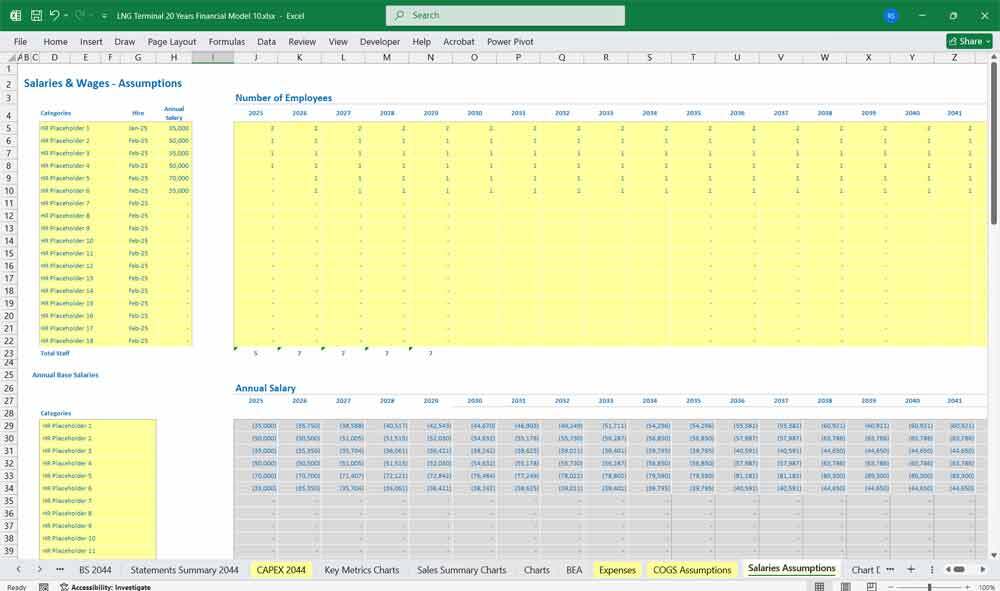

- Labor Costs: Salaries and wages for operational staff.

- Insurance: Coverage for the terminal's assets and operations.

- Depreciation: Amortization of the terminal's capital assets (e.g., storage tanks, regasification units).

- Gross Profit = Revenue - Operating Costs

- General & Administrative (G&A): Overhead costs such as management salaries, office expenses, and legal fees.

- Interest Expense: Interest on debt used to finance the terminal's construction or operations.

- Taxes: Corporate income taxes based on taxable income.

- Net Income = Gross Profit - Other Expenses

2. Cash Flow Statement

The Cash Flow Statement tracks the cash inflows and outflows, divided into three sections: Operating Activities, Investing Activities, and Financing Activities.

Operating Activities

- Cash from Operations: Net income adjusted for non-cash items (e.g., depreciation) and changes in working capital (e.g., accounts receivable, inventory, accounts payable).

- Working Capital Changes:

- Increase in receivables (cash outflow).

- Decrease in payables (cash outflow).

- Changes in inventory levels (if applicable).

- Increase in receivables (cash outflow).

- Capital Expenditures (CapEx):

- Initial construction costs for the terminal (if modeled in the early years).

- Ongoing investments in infrastructure upgrades or expansions.

- Initial construction costs for the terminal (if modeled in the early years).

- Asset Sales: Proceeds from selling any assets (if applicable).

- Debt Issuance: Cash inflows from borrowing to finance the terminal.

- Debt Repayment: Principal repayments on outstanding debt.

- Equity Issuance: Cash inflows from equity investors.

- Dividends: Cash outflows to shareholders (if applicable).

- Net Change in Cash = Cash from Operating Activities + Cash from Investing Activities + Cash from Financing Activities

3. Balance Sheet

The Balance Sheet provides a snapshot of the terminal's financial position at a specific point in time, showing assets, liabilities, and equity.

Assets

- Current Assets:

- Cash and Cash Equivalents: Ending cash balance from the Cash Flow Statement.

- Accounts Receivable: Revenue earned but not yet collected.

- Inventory: LNG stored in the terminal (if applicable).

- Cash and Cash Equivalents: Ending cash balance from the Cash Flow Statement.

- Non-Current Assets:

- Property, Plant, and Equipment (PP&E): Terminal infrastructure (e.g., storage tanks, regasification units) net of accumulated depreciation.

- Intangible Assets: Permits, licenses, or other non-physical assets.

- Property, Plant, and Equipment (PP&E): Terminal infrastructure (e.g., storage tanks, regasification units) net of accumulated depreciation.

- Current Liabilities:

- Accounts Payable: Amounts owed to suppliers or contractors.

- Short-Term Debt: Portion of long-term debt due within the year.

- Accounts Payable: Amounts owed to suppliers or contractors.

- Non-Current Liabilities:

- Long-Term Debt: Outstanding loans used to finance the terminal.

- Deferred Revenue: Payments received in advance for future services.

- Long-Term Debt: Outstanding loans used to finance the terminal.

- Shareholder Equity:

- Common Stock: Equity issued to investors.

- Retained Earnings: Cumulative net income less dividends paid.

- Common Stock: Equity issued to investors.

- Assets = Liabilities + Equity

To build the model, the following assumptions and drivers are critical:

- Capacity Utilization: Percentage of the terminal's capacity used for regasification, storage, and other services.

- Fee Structure: Regasification, storage, and tolling fees per unit of LNG.

- Cost Structure: Fixed and variable operating costs, including maintenance and labor.

- Capital Structure: A Mix of debt and equity used to finance the terminal.

- Depreciation Schedule: Useful life of assets and depreciation method (e.g., straight-line).

- Tax Rate: Applicable corporate tax rate.

- Working Capital: Days sales outstanding (DSO), days payable outstanding (DPO), and inventory turnover.

- Income Statement to Cash Flow Statement: Net income flows into the Cash Flow Statement as the starting point for operating activities.

- Cash Flow Statement to Balance Sheet: The ending cash balance from the Cash Flow Statement feeds into the Balance Sheet.

- Balance Sheet to Income Statement: Interest expense on debt (from the Balance Sheet) impacts the Income Statement.

This model provides a holistic view of the LNG Terminal's financial performance, liquidity, and solvency, enabling stakeholders to make informed decisions.

This Best Practice includes

1 Excel Financial Model

Further information

Provides thorough oversight, tracking, and reporting of LNG Plant finances, including budget utilisation and projections updates.