Originally published: 25/07/2020 12:43

Last version published: 27/07/2020 05:22

Publication number: ELQ-75687-3

View all versions & Certificate

Last version published: 27/07/2020 05:22

Publication number: ELQ-75687-3

View all versions & Certificate

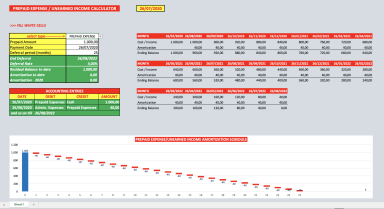

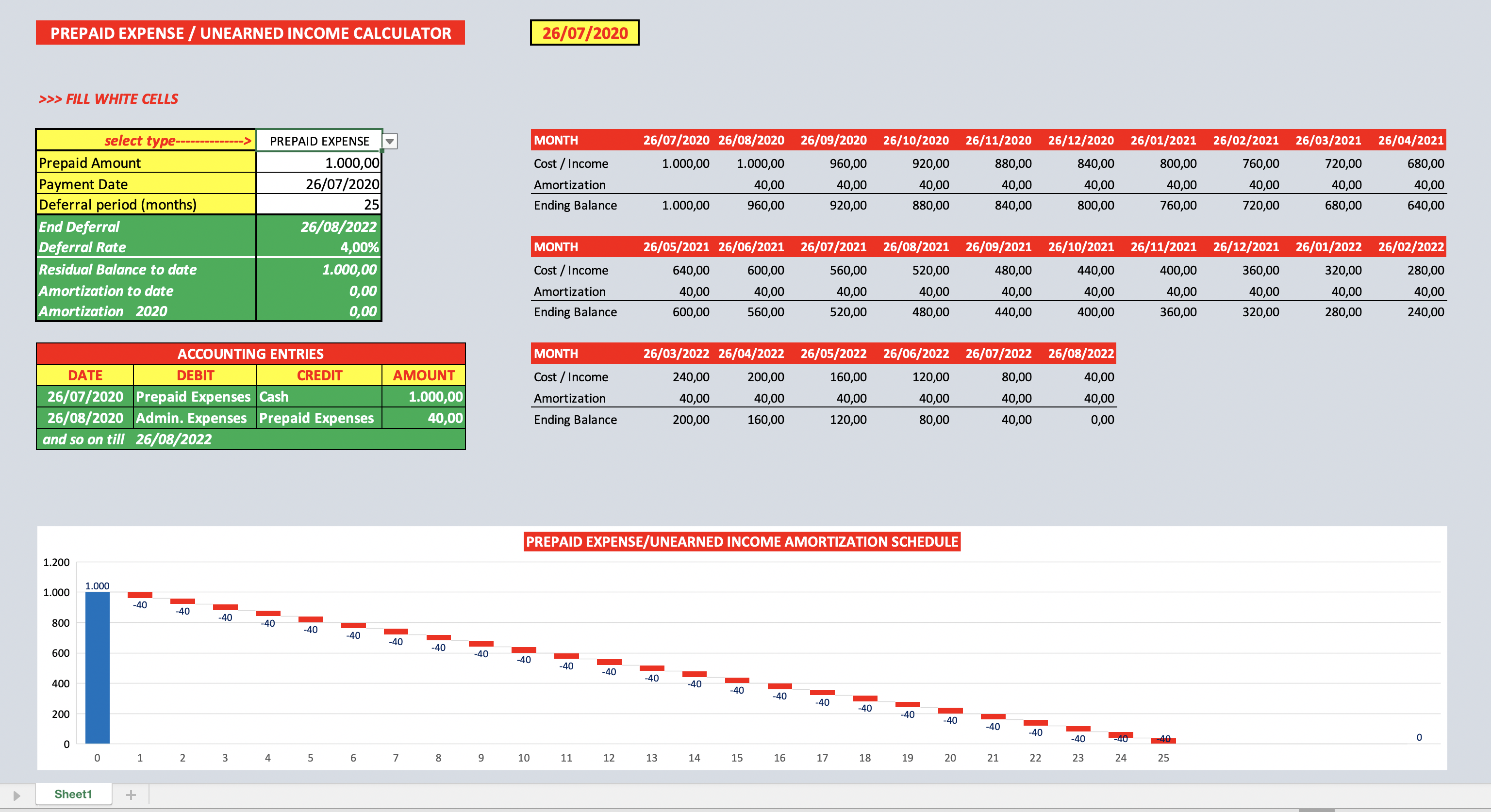

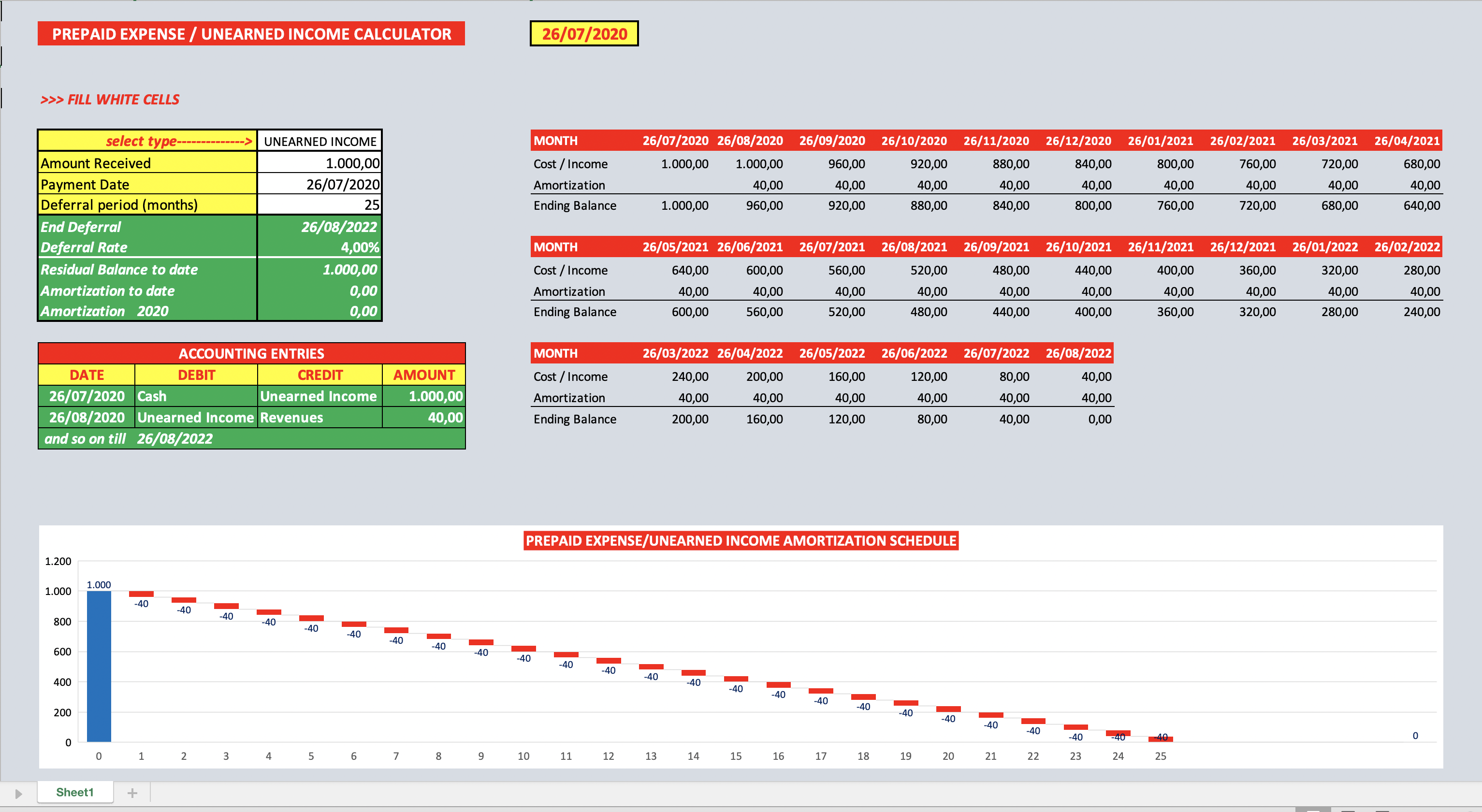

Prepaid Expense and Unearned Income Amortization Calculator

Prepaid Expense and Unearned Income Amortization Calculator with accounting entries, for Corporate Finance Professionals

Domenico Cristarella offers you this Best Practice for free!

download for free

Add to bookmarks