Publication number: ELQ-99495-1

View all versions & Certificate

A Bankable Macro Enabled Financial Model for Utility-Scale Solar PV Project Finance

A DSCR-sculpted solar PV project finance model with stress testing.

Further information

Objectives of the model:

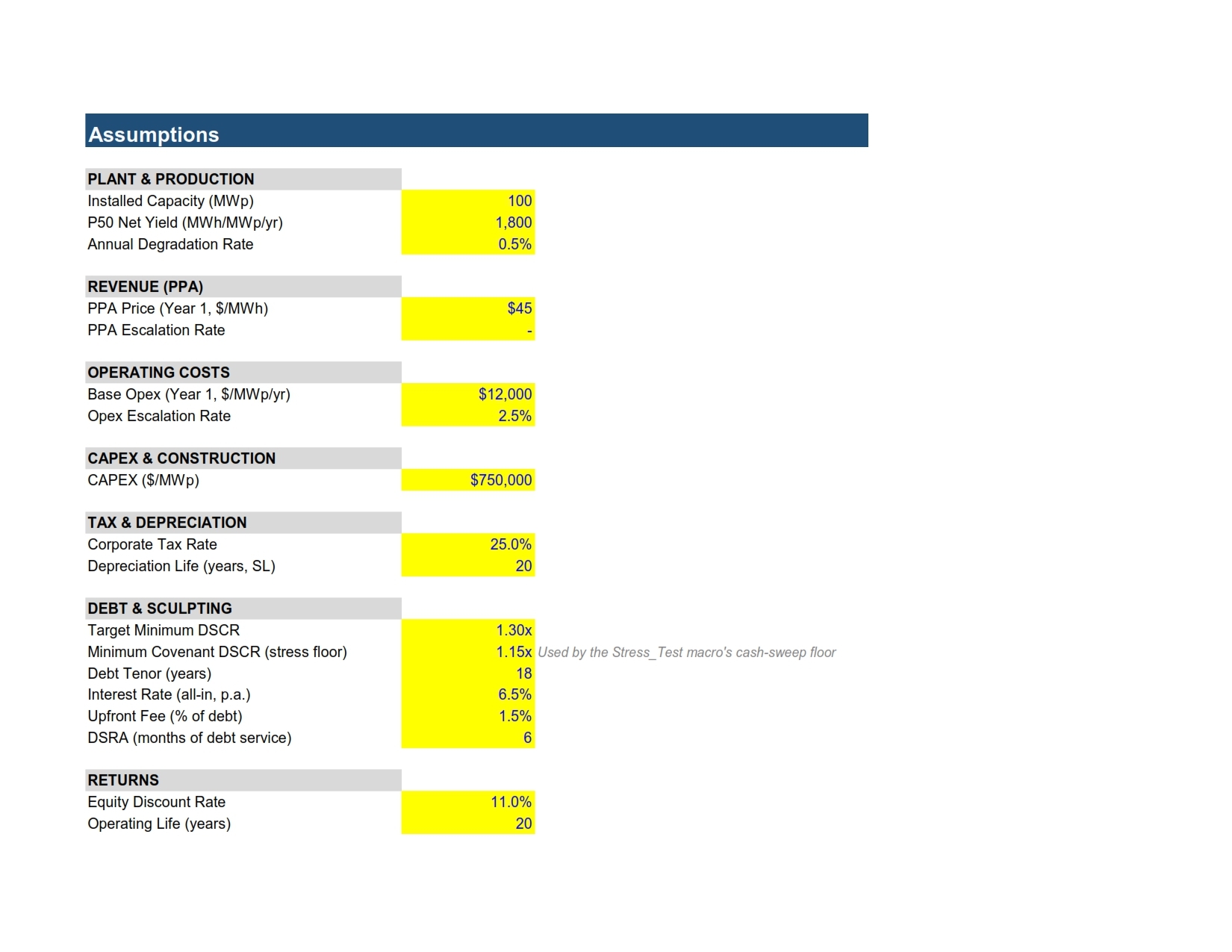

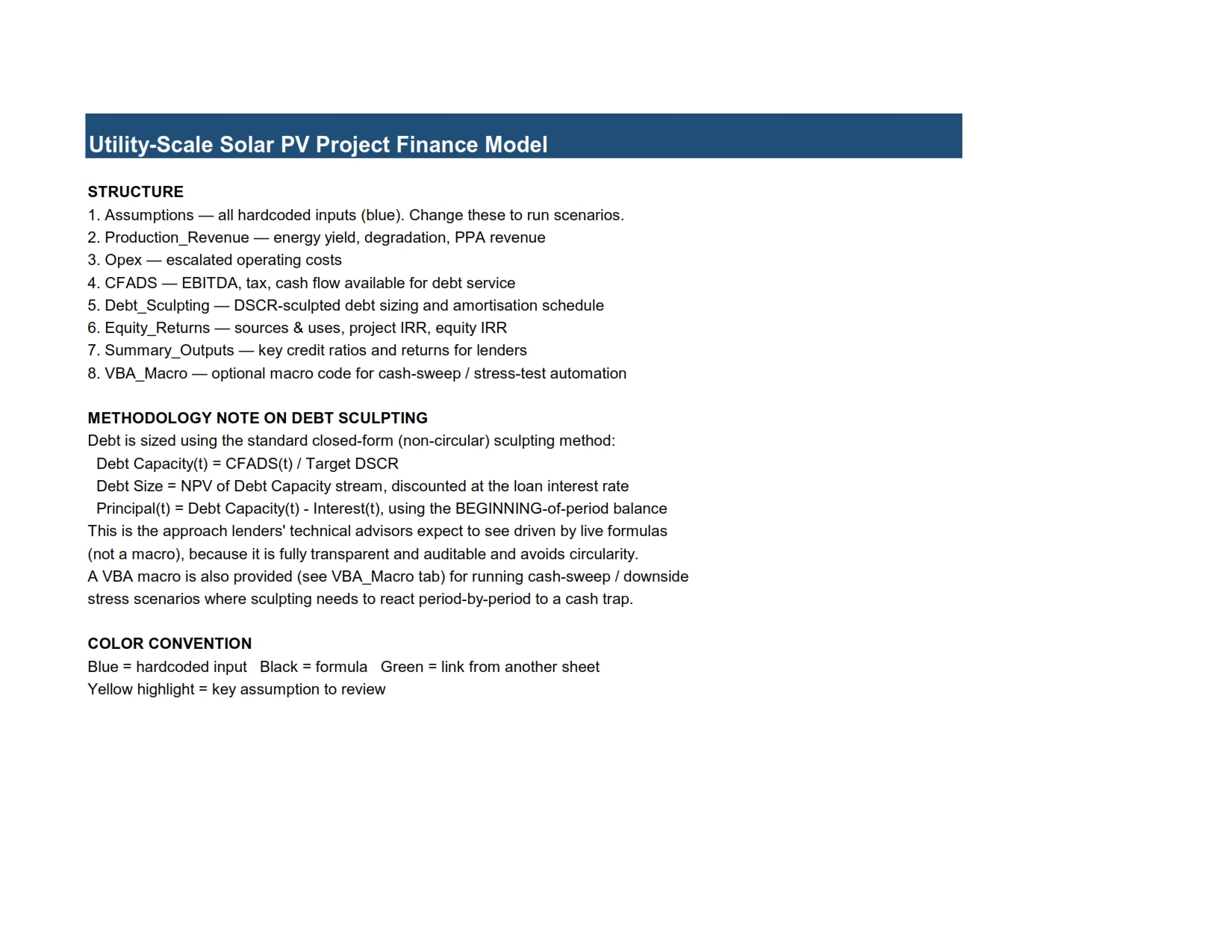

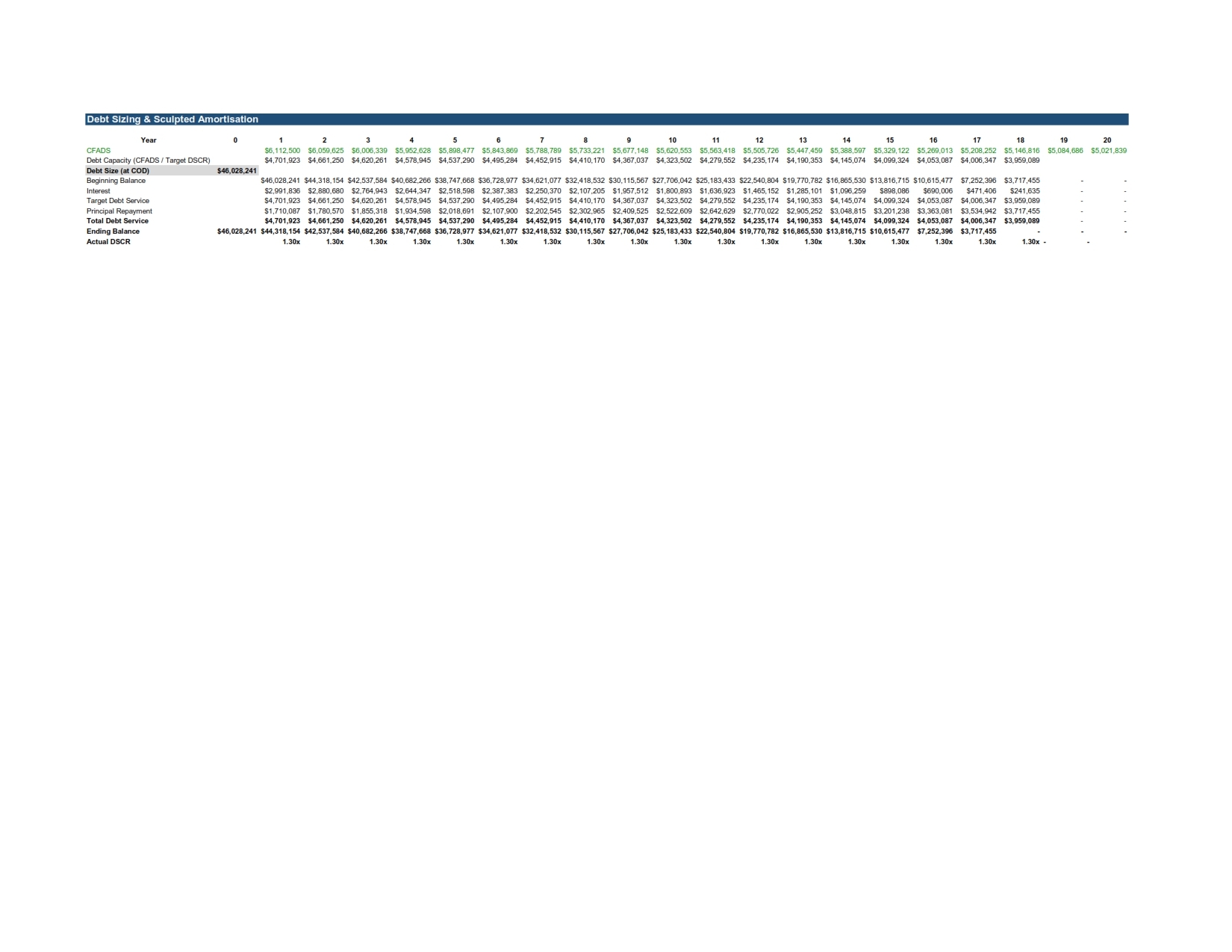

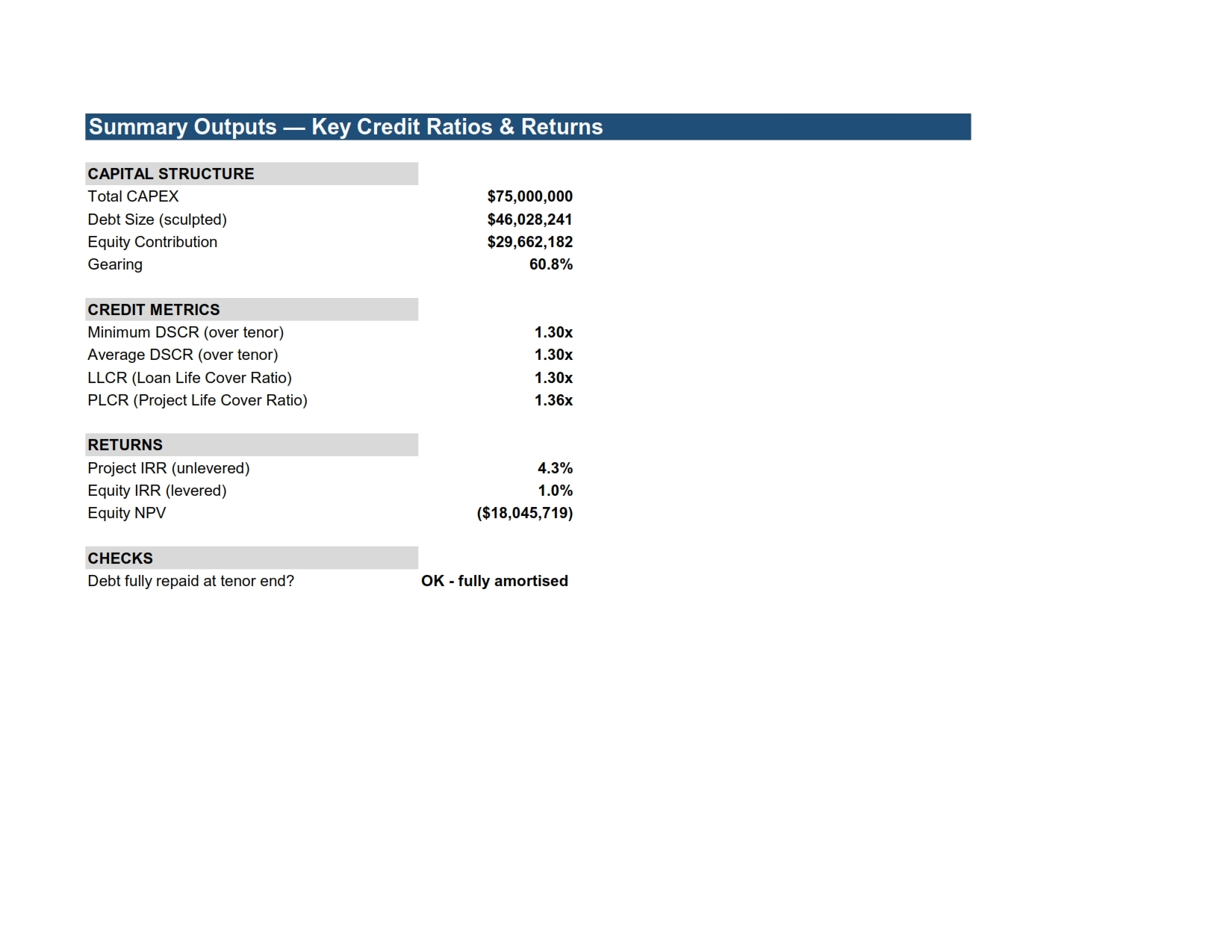

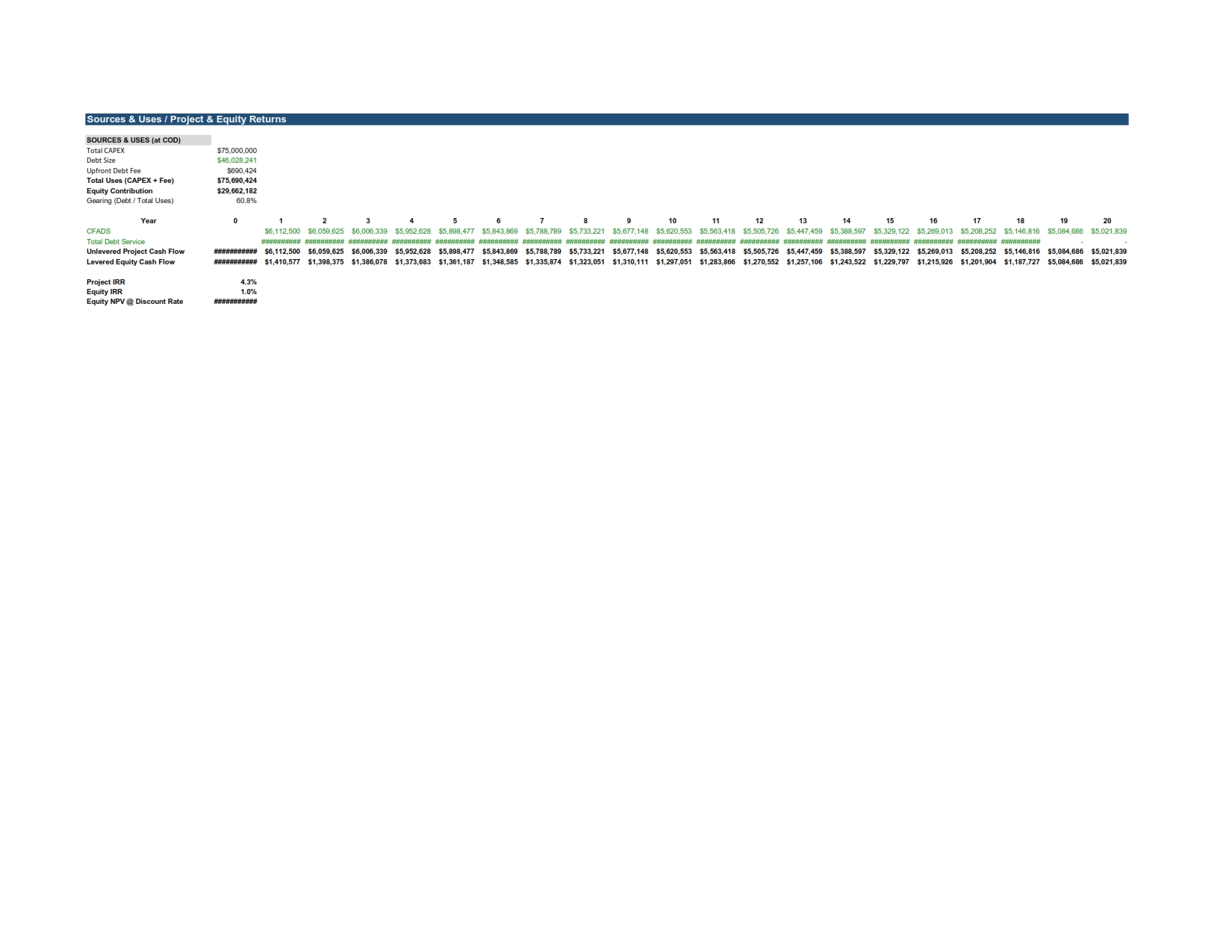

1. Size project debt defensibly — determine the maximum debt a lender could support using a DSCR-sculpted (not flat-annuity) repayment profile, sized off actual project cash flow rather than an assumed schedule.

2. Avoid circularity — calculate that debt size and its amortization using a closed-form NPV approach, so the file stays auditable and doesn't depend on iterative-calculation settings.

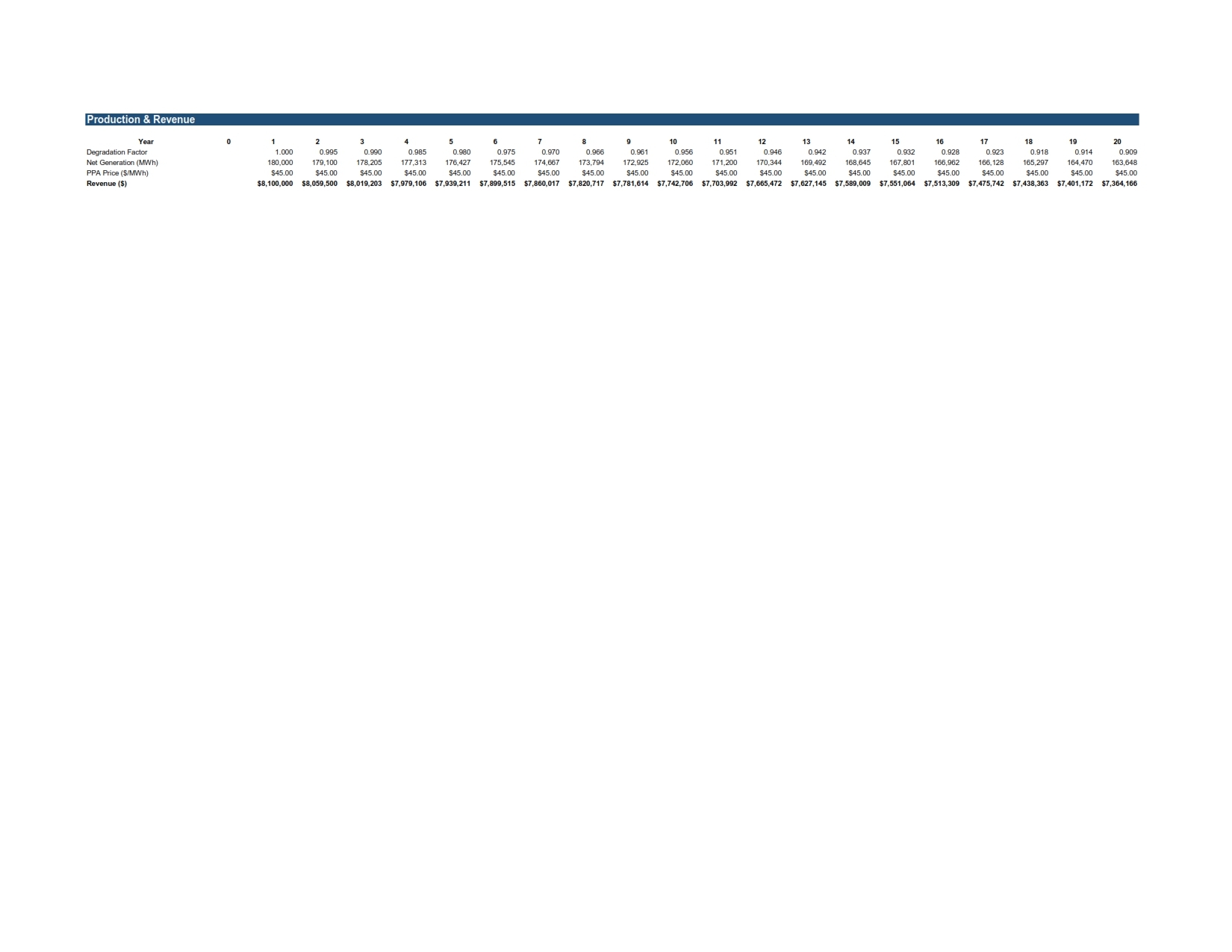

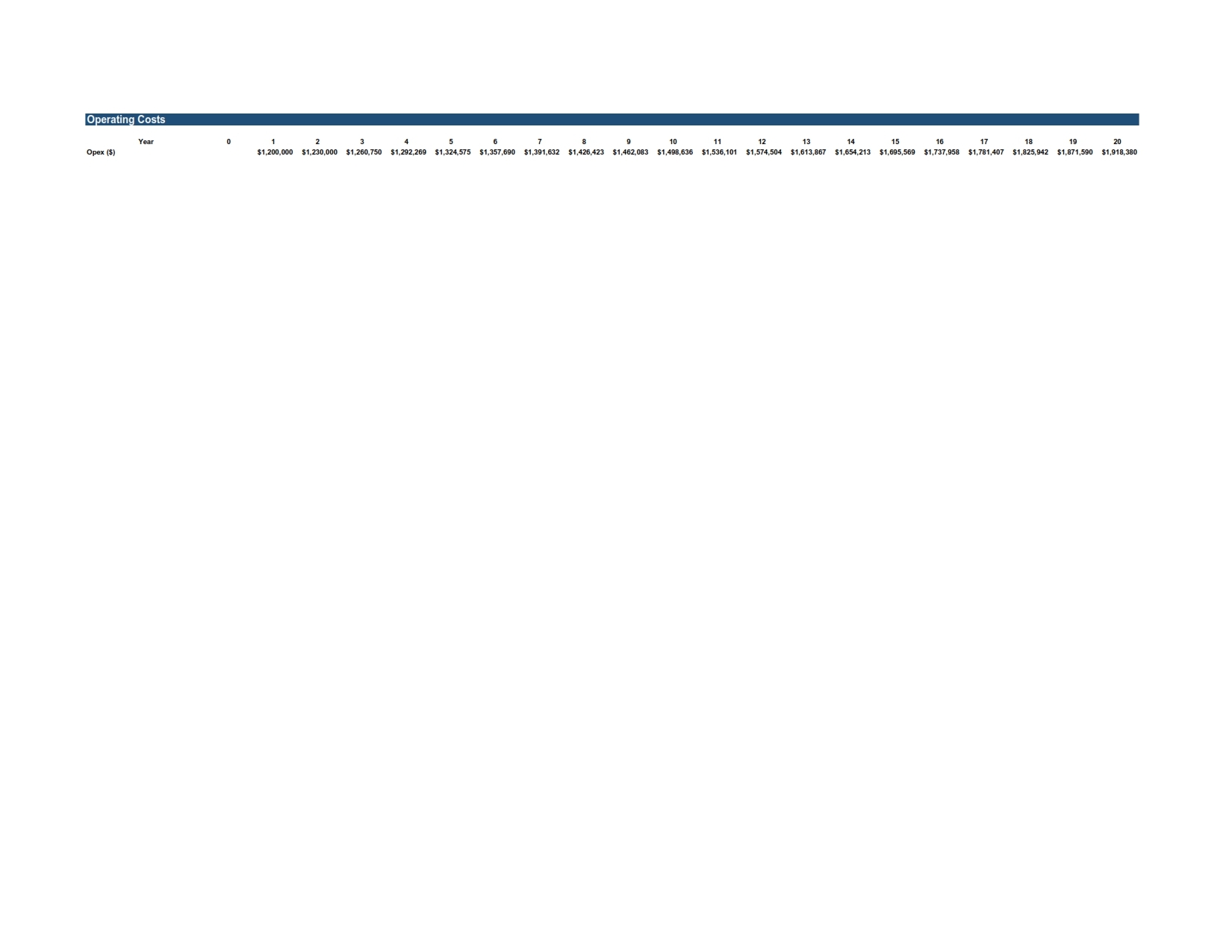

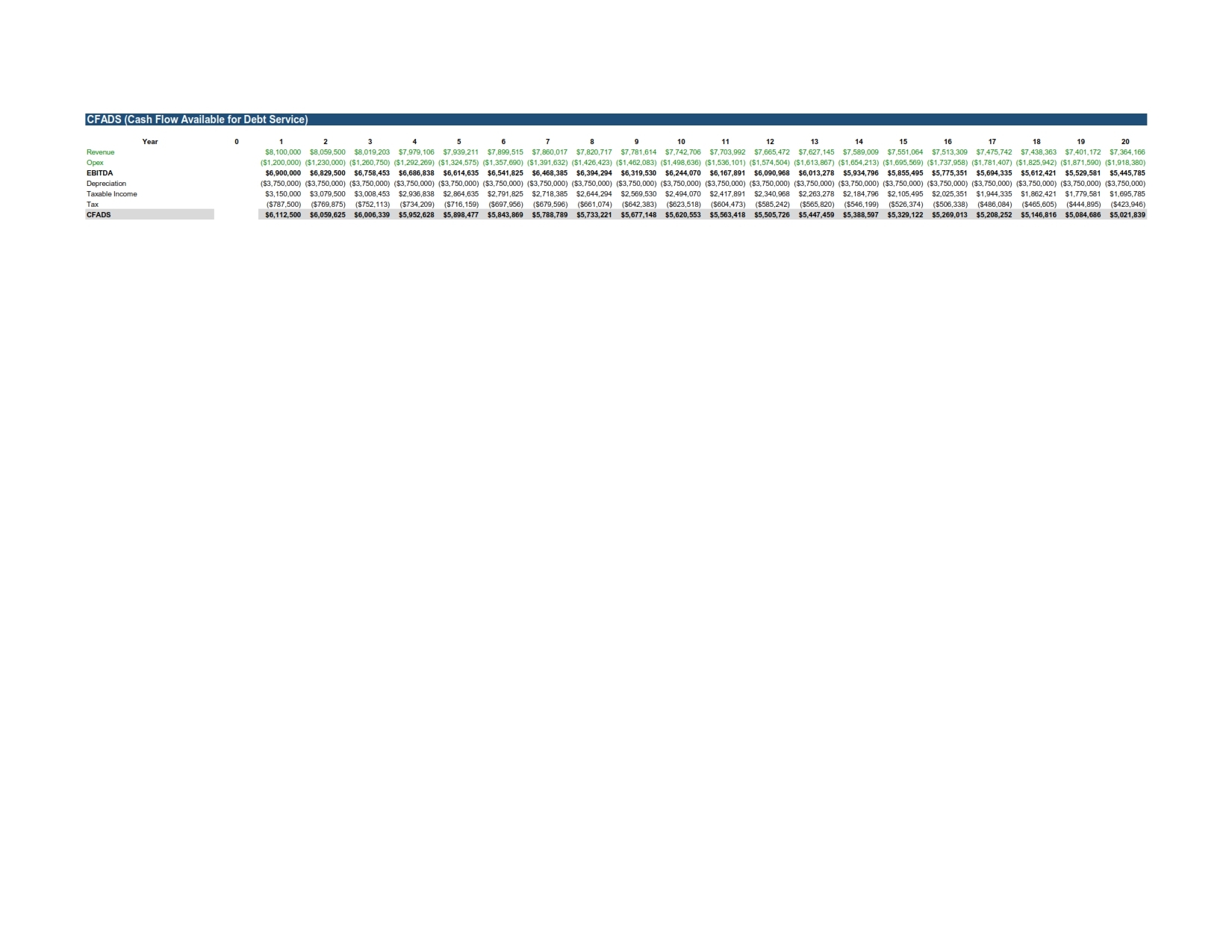

3. Derive CFADS transparently — build cash flow available for debt service up from first principles (generation → revenue → opex → EBITDA → tax) so every credit metric traces back to a single, visible chain of assumptions.

4. Produce lender-standard credit metrics — minimum/average DSCR, LLCR, and PLCR, calculated automatically rather than requiring manual derivation.

5. Quantify sponsor returns — project IRR (unlevered) and equity IRR/NPV (levered), so both sides of the capital stack can evaluate the deal from the same base case.

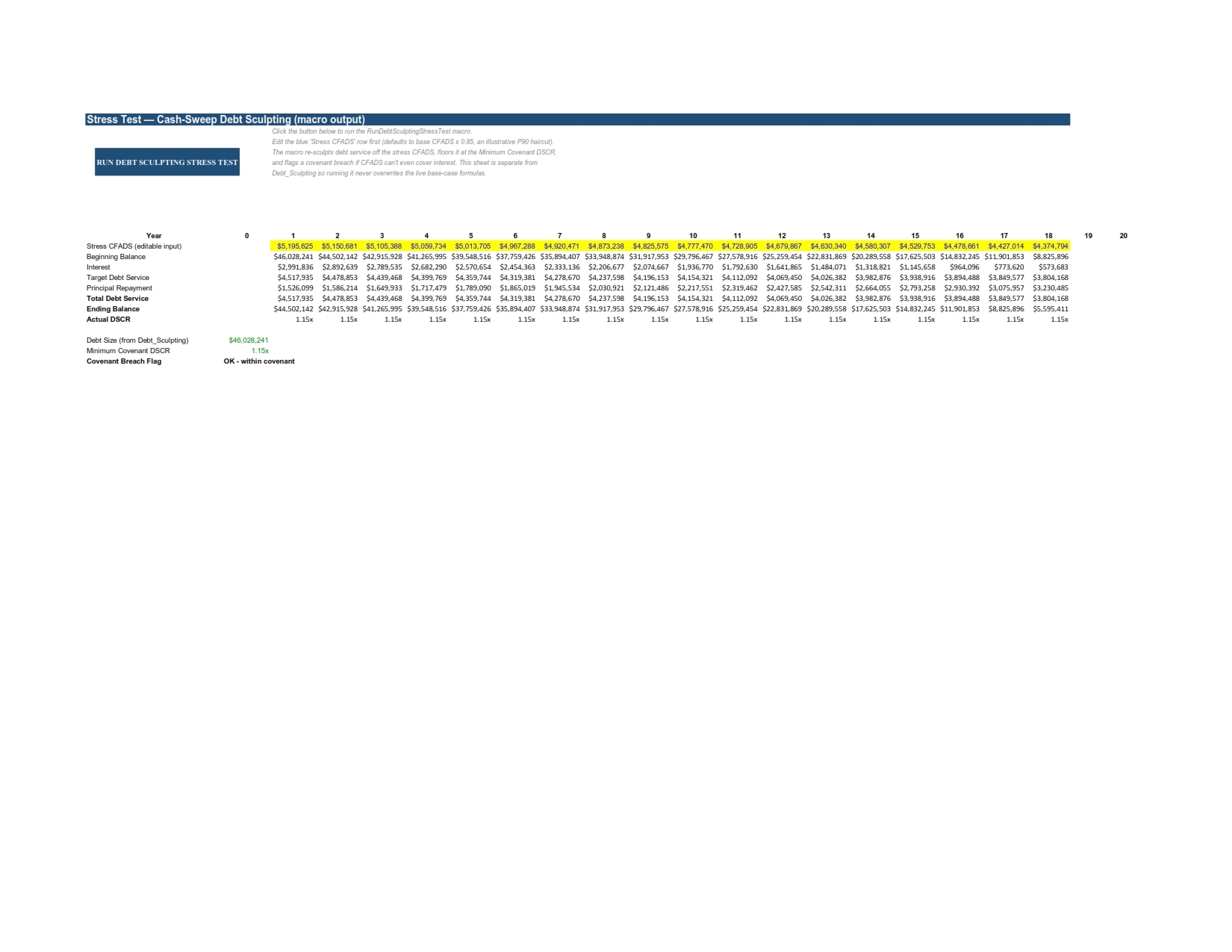

6. Separate sizing from stress-testing — keep the live base-case sculpting formulas isolated from downside scenario work, so running a stress case (e.g. P90 production) can never corrupt the underlying model.

7. Support covenant analysis — test whether a downside CFADS case would breach a minimum covenant DSCR, distinct from the DSCR used to size debt in the base case.

8. Keep every assumption a visible input — centralize all hardcoded drivers on one sheet so scenario changes and audits touch a single cell, not formulas scattered across tabs.

9. Enable one-click stress iteration — provide a macro-driven activation button so re-running a downside sculpting scenario doesn't require manually rebuilding the schedule each time.

10. Serve as an extensible template — demonstrate correct, bankable mechanics that can be adapted to a specific jurisdiction, technology, and offtake structure rather than being a finished deal-specific instrument.

This model is best suited to situations that match the structural assumptions actually built into it. It applies best when:

Project characteristics

- Utility-scale, grid-connected solar PV (not distributed/rooftop, not hybrid with storage or wind — those need added revenue/dispatch logic)

- A single-asset special purpose vehicle (SPV), not a portfolio with cross-collateralized debt or shared reserves

- Revenue from a fixed-price or fixed-escalation PPA — merchant/floating-price exposure would need a different revenue module (price curves, hedging, capture-rate discounts)

- Predictable, gradual output decline (standard PV degradation curves) rather than volatile output profiles

Capital structure

- Senior, amortizing project debt sized to a DSCR covenant — not a bond structure with bullet/balloon repayment, not mezzanine or PIK structures

- A single tranche of debt at one interest rate — multi-tranche structures (senior + subordinated, different currencies) would need parallel sculpting logic

- Annual periodicity — matches annual PPA escalation and reporting; would need modification for semi-annual/quarterly debt service (the standard in many real financings)

Tax and jurisdiction

- A straightforward corporate tax regime with straight-line depreciation — jurisdictions with accelerated depreciation (e.g. MACRS), tax equity structures, or investment/production tax credits would materially change the CFADS and equity waterfall and aren't currently modeled

- No import duties, currency mismatch between revenue/debt, or withholding tax considerations — cross-border financings would need an FX and hedging layer

Deal stage and purpose

- Best used at term sheet / early due diligence stage to establish indicative debt capacity and credit metrics, or as a teaching/template tool for building intuition around sculpted debt sizing

- Not a substitute for a full three-statement model with a balance sheet and cash waterfall, which most lenders will require before financial close

- Best where the sponsor wants a transparent, auditable sizing methodology rather than a black-box or heavily circular structure — this suits early-stage lender engagement or competitive financing processes where advisors need to independently re-derive numbers quickly

Where it would need extension before real use

- Construction-period drawdowns and interest during construction (currently a single Year-0 lump sum)

- A debt service reserve account cash flow line (the DSRA sizing input exists, but isn't yet flowing through the cash waterfall)

- P90/P99 production cases as formal scenario toggles, not just the illustrative stress sheet

- Multi-currency or inflation-indexed PPA structures, if applicable to the jurisdiction

Asset type and technology

- Distributed/rooftop or C&I solar (different scale economics, financing structures, and often no PPA at wholesale-style pricing)

- Hybrid projects (solar + storage, solar + wind) — the model has no dispatch, charge/discharge, or multi-revenue-stream logic

- Any technology with volatile or non-degrading output profiles (e.g. wind, where load factors vary significantly year to year rather than declining smoothly)

Revenue structure

- Merchant or wholesale-exposed revenue with no PPA — the model assumes a fixed-price, fixed-escalation contract; floating/merchant exposure needs price curves, capture-rate discounting, and hedging logic it doesn't have

- Multiple revenue streams (capacity payments, ancillary services, REC/green certificate sales modeled separately) — currently collapsed into a single PPA revenue line

- Take-or-pay structures with curtailment risk or availability penalties

Capital structure

- Bullet or balloon repayment structures — the model assumes full amortization by construction; a bullet at maturity would break the NPV-based sizing identity

- Multi-tranche debt (senior + mezzanine, or multiple currencies) — sculpting logic here only handles a single tranche at a single rate

- Bond financing with fixed coupon/covenant structures distinct from bank-style DSCR sculpting

- Portfolio or platform financings with cross-collateralization, shared reserves, or portfolio-level covenants — this is a single-asset SPV model only

Tax and jurisdiction

- Jurisdictions with accelerated depreciation, tax equity partnerships, or investment/production tax credits (US-style ITC/PTC structures in particular) — these fundamentally change the tax line and equity waterfall, and would need a dedicated tax equity module

- Cross-border deals with FX mismatch between revenue and debt currency, or withholding tax on distributions — no FX or hedging layer exists

- Jurisdictions where interest is tax-deductible in a way that matters materially — the model excludes interest from the tax calculation as a simplification to avoid circularity, which understates the tax shield

Deal stage

- Financial close or funding documentation — the model lacks a full balance sheet, cash waterfall, and DSRA mechanics that lenders require at that stage

- Refinancing or restructuring analysis on an operating asset with actual (not projected) historical cash flows — this is a greenfield sizing tool, not a workout tool

- Semi-annual or quarterly debt service conventions — the annual periodicity here would need rebuilding, not just reformatting, to match

Risk profile

- Projects with material construction risk, multi-year build periods, or phased COD — the model treats construction as a single Year-0 CAPEX outflow with no drawdown schedule or interest-during-construction capitalization

- Highly volatile or non-P50/P90-characterizable production risk, where a single degradation curve doesn't meaningfully describe the downside case