Originally published: 01/07/2022 15:21

Publication number: ELQ-13465-1

View all versions & Certificate

Publication number: ELQ-13465-1

View all versions & Certificate

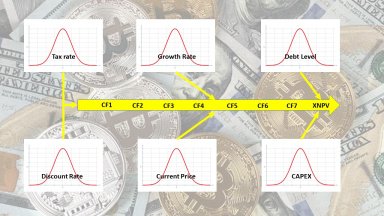

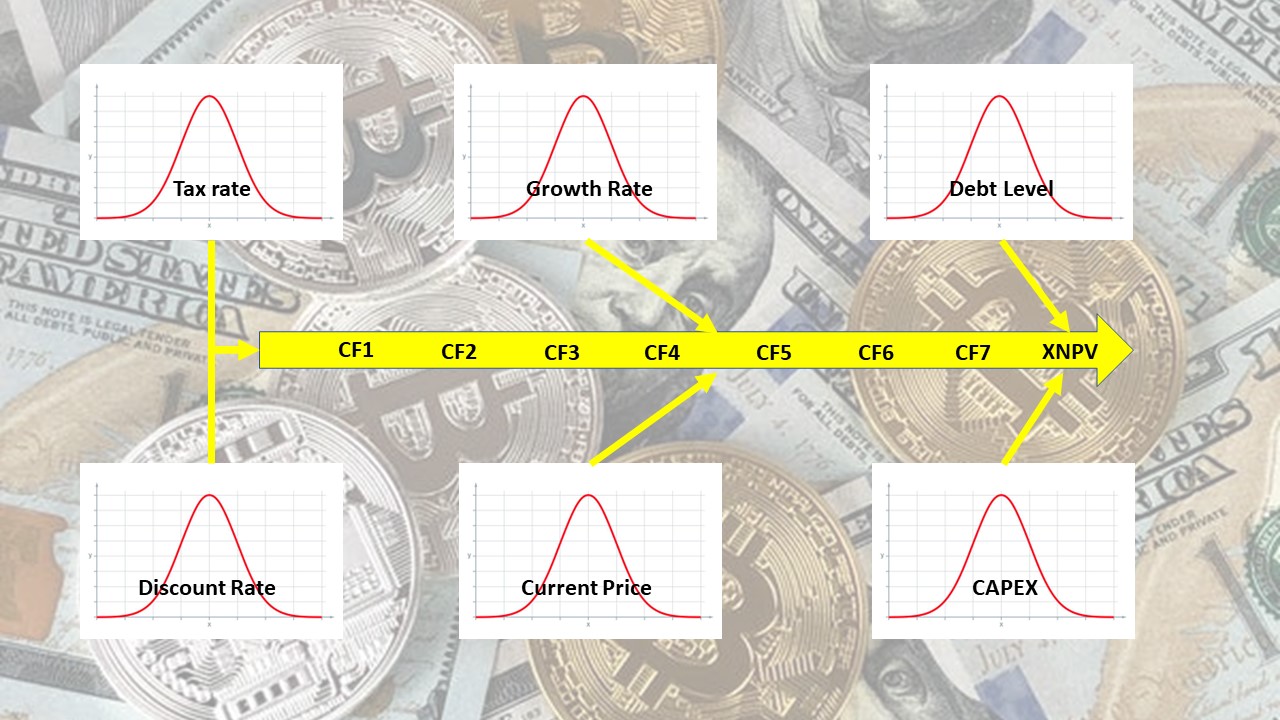

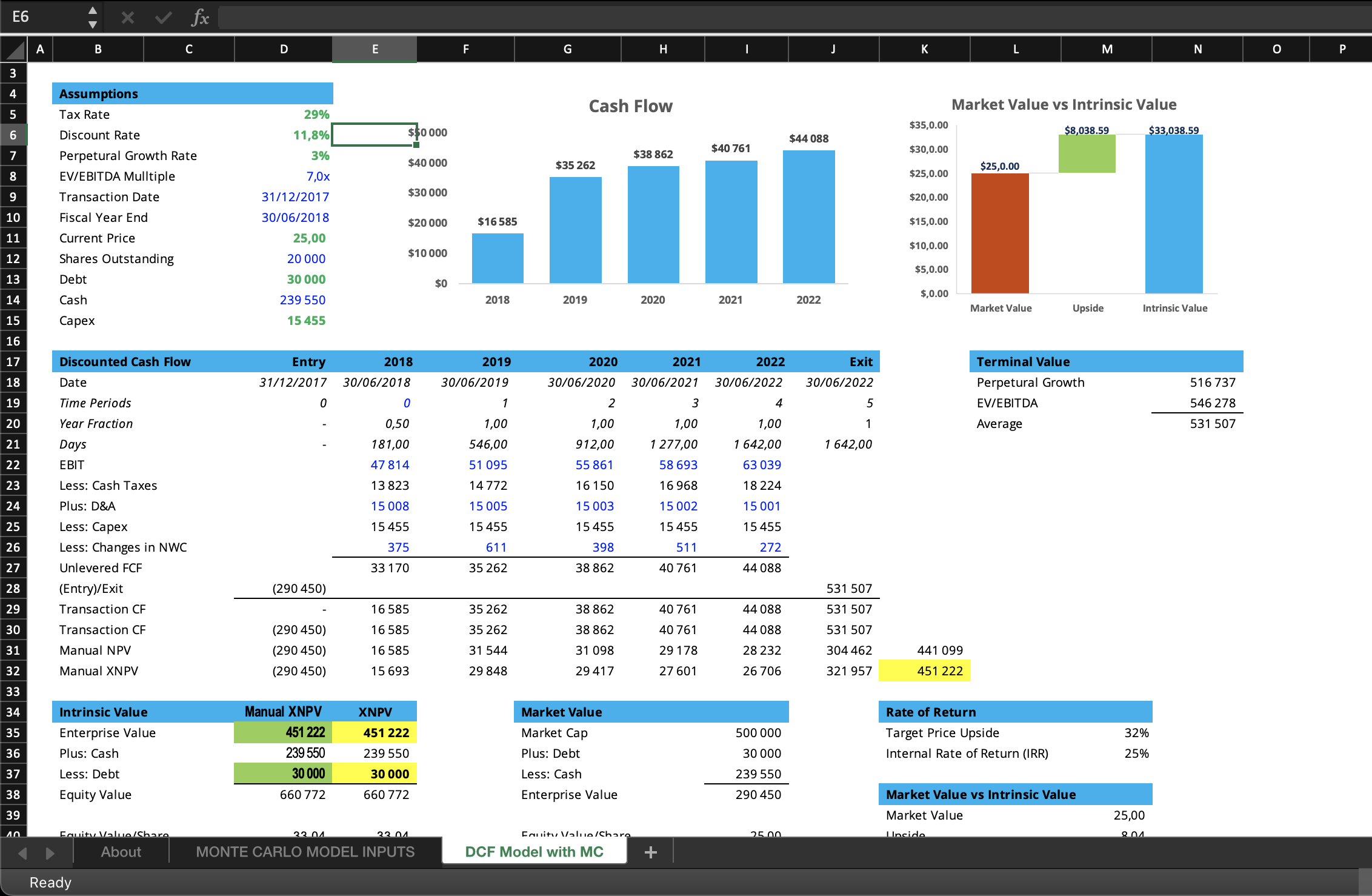

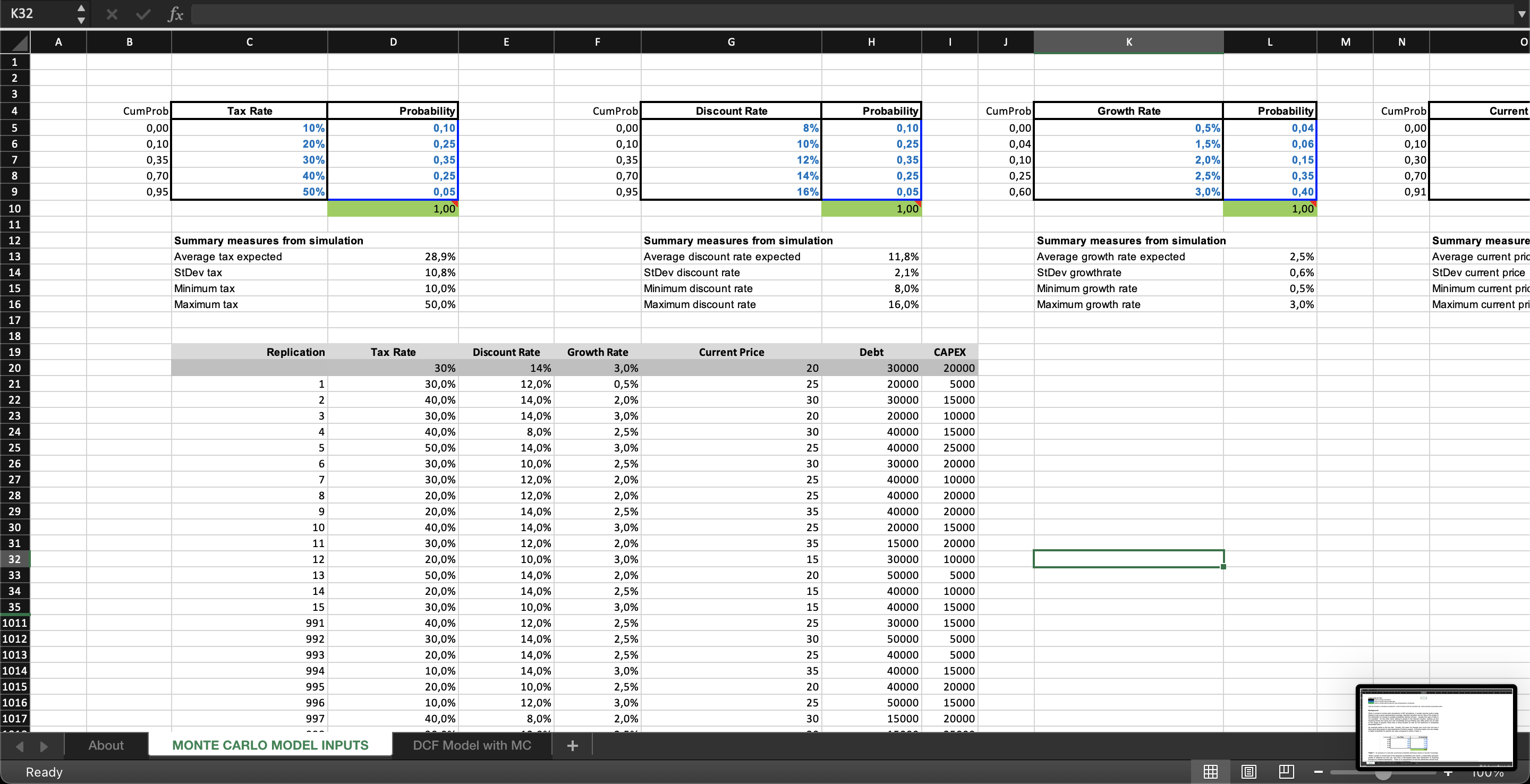

The use of Monte Carlo Simulation in DCF Analysis - A Simple Example

Simple user-generated Monte Carlo Simulation for Discounted Cash Flow

Further information

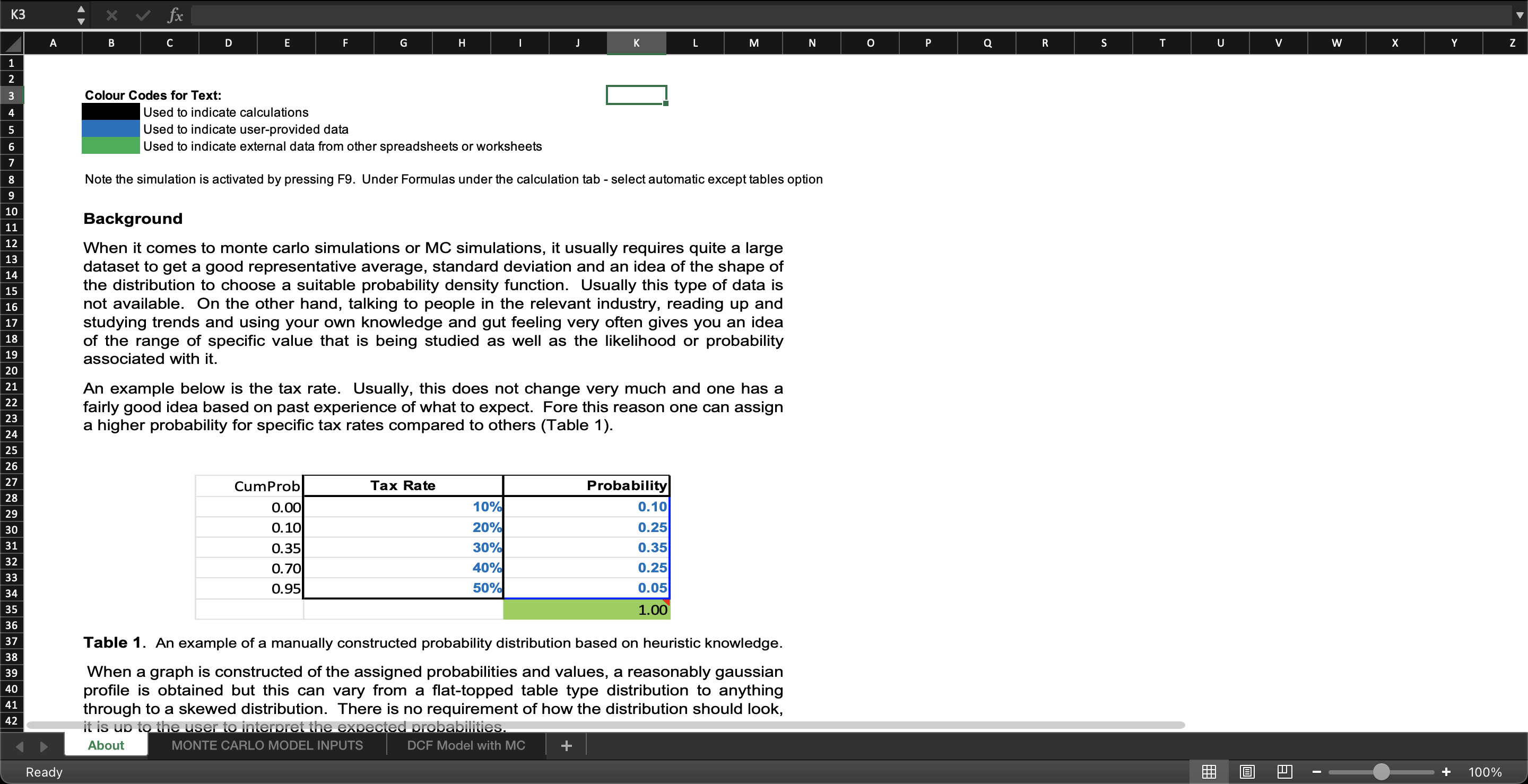

The simulation presented here is simply to demonstrate the use of a user-generated probability distribution in discounted cash flow analysis.

The simulation presented here is for demonstration purposes only and should not be used for any large scale simulations. The underlying principles may be used.