Originally published: 09/07/2018 08:55

Publication number: ELQ-37679-1

View all versions & Certificate

Publication number: ELQ-37679-1

View all versions & Certificate

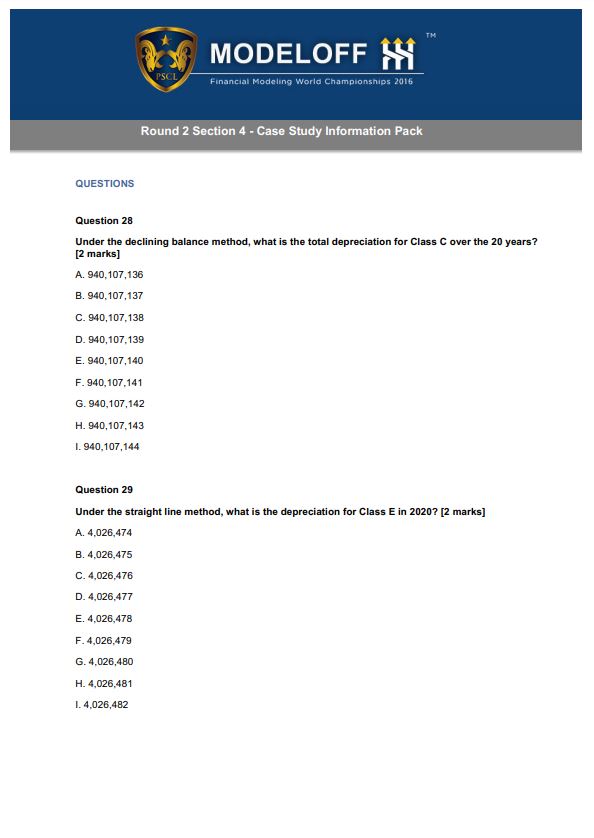

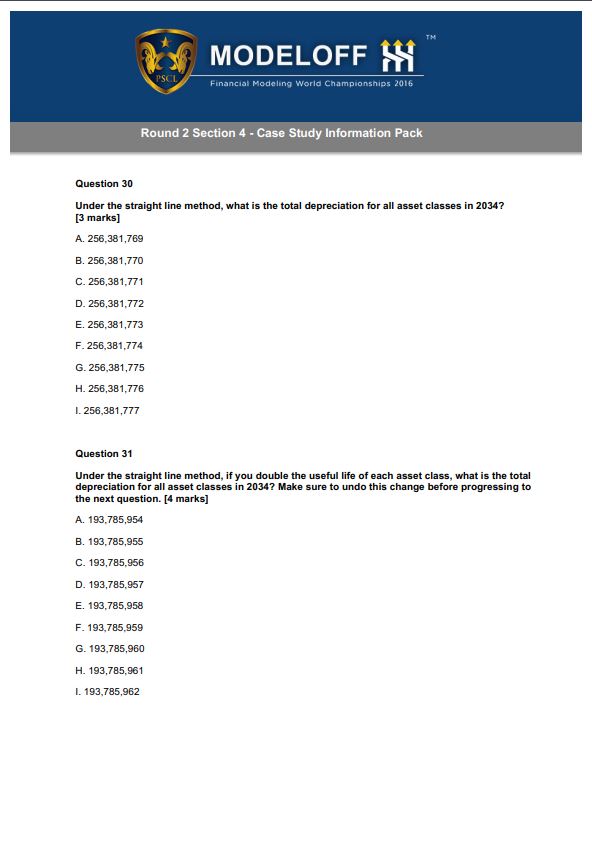

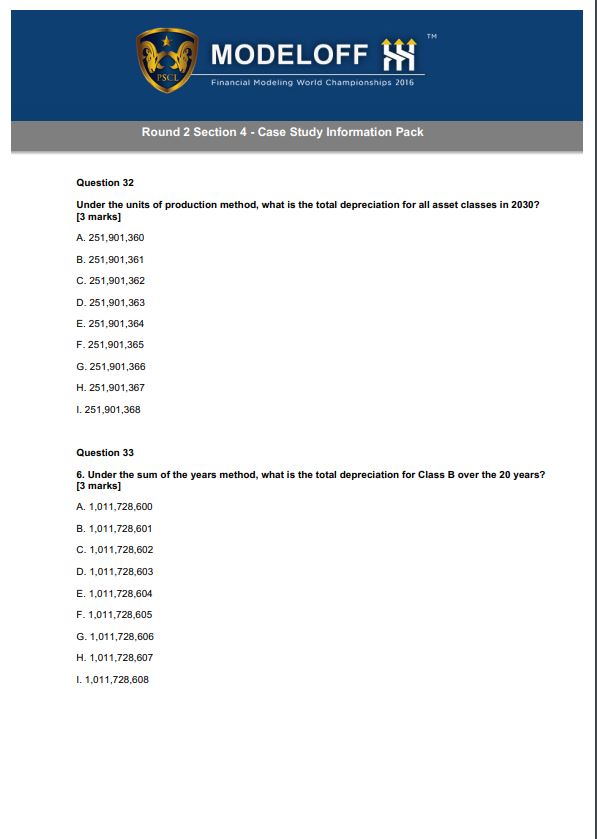

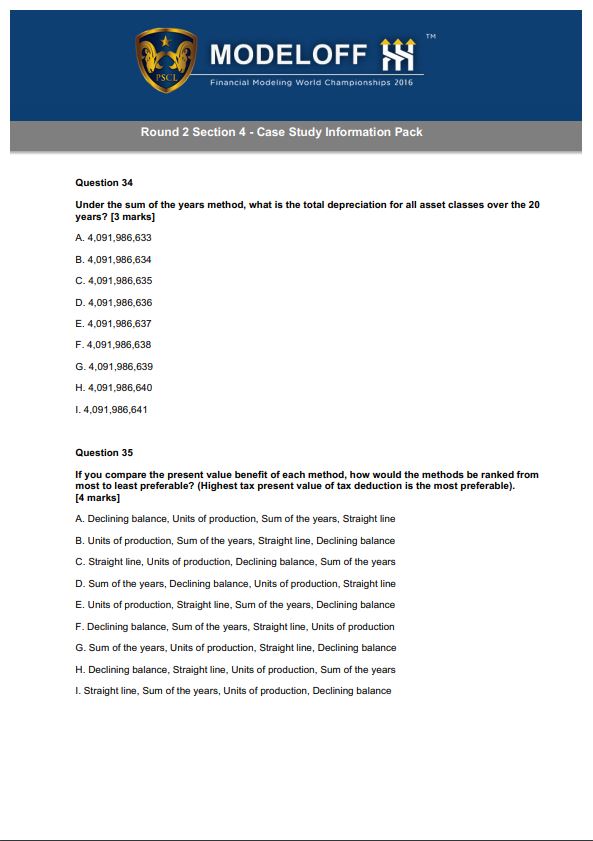

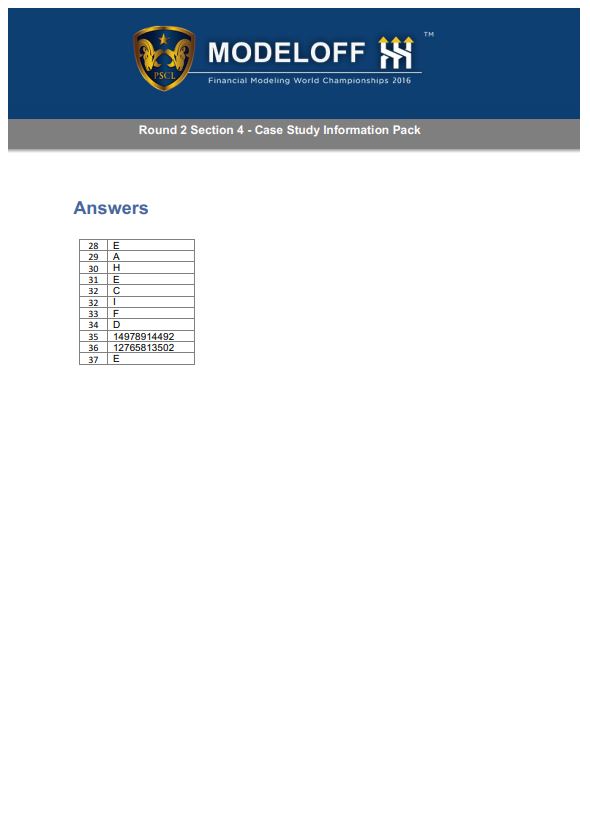

2016 Round 2, Section 4: Maximize the Benefit

Excel training/competition model from the 2017 Financial Modeling World Championships

To help finance professionals transform their Excel, financial modelling, data visualisation & analytics skillsFollow 82