Originally published: 22/10/2020 06:54

Last version published: 27/10/2020 08:24

Publication number: ELQ-72959-2

View all versions & Certificate

Last version published: 27/10/2020 08:24

Publication number: ELQ-72959-2

View all versions & Certificate

IFRS 9 Stage 1 ECL Estimation

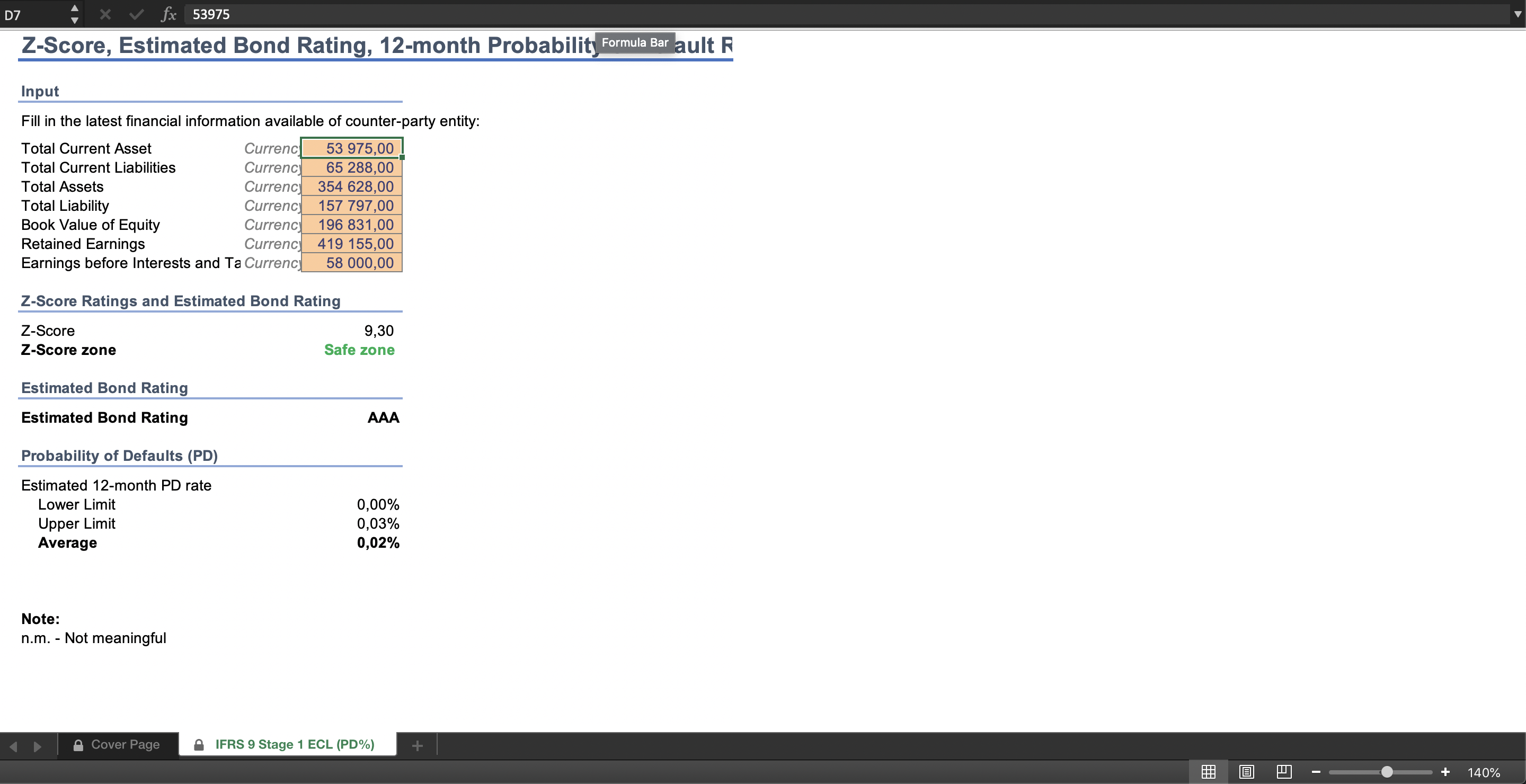

This model estimates the probability of defaults on financial instruments, for financing reporting purpose.

Business Valuation Expert | Advising Merger & Acquisitions | Working with Start-ups & Established BusinessesFollow 33