Originally published: 25/11/2024 08:39

Publication number: ELQ-93352-1

View all versions & Certificate

Publication number: ELQ-93352-1

View all versions & Certificate

EV Battery Recycling Centre Financial Model

A comprehensive 5 Year 3 Statement editable, MS Excel spreadsheet for tracking EV Battery Recycling Centre finances.

AllFinancialModels offer a curated selection of high-quality yet financial model templates designed to support a wide range of business needs.Follow

ev batteryrecycling centrefinance modelfinancial modelelectric vehicleexcelev battery recycling centrerecyclablerenewablelithium battery recycling

Description

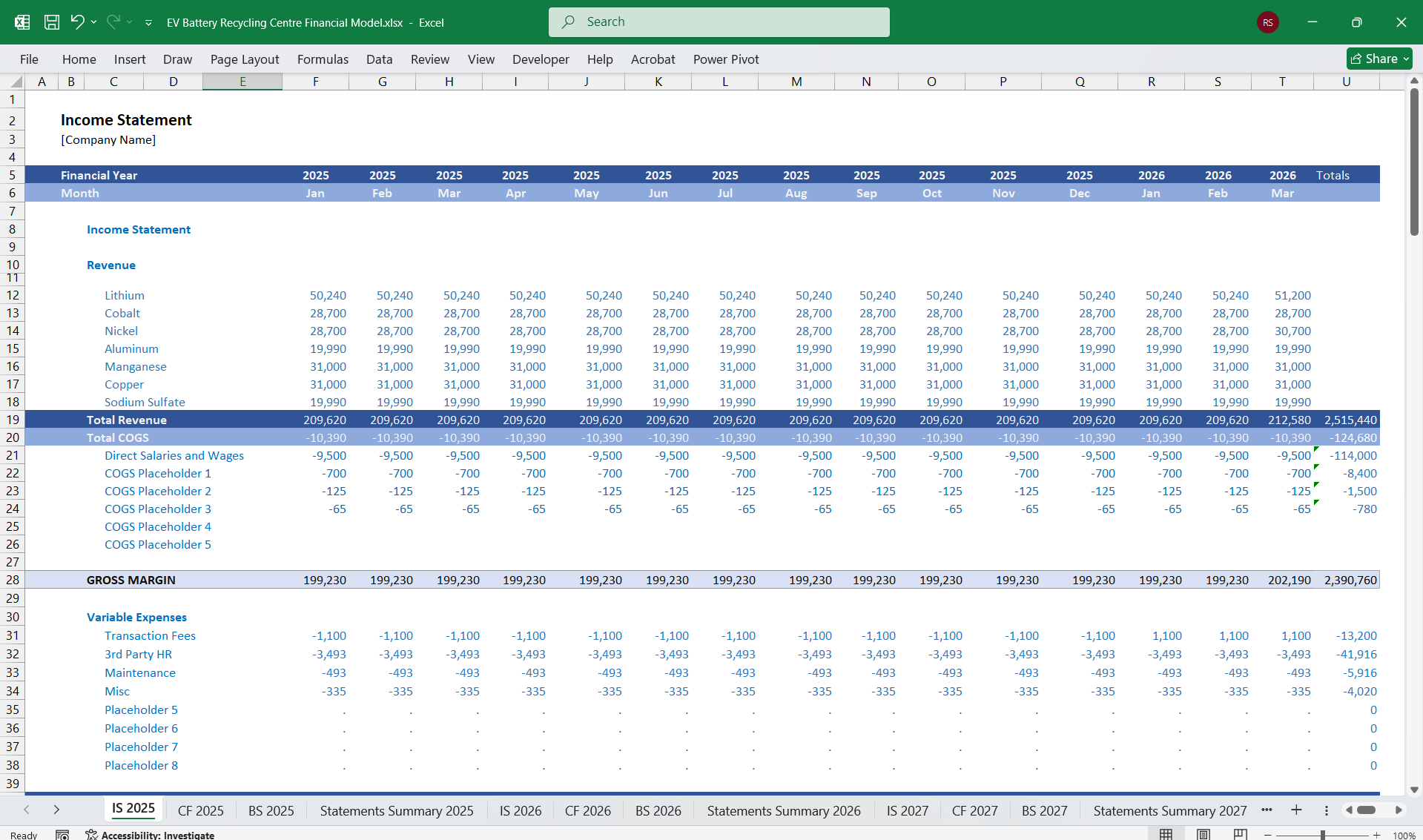

The financial model for an **EV Battery Recycling Company**, incorporates key revenue sections for materials: "Lithium", "Cobalt", "Nickel", "Aluminum", "Manganese", "Copper**, and "Sodium Sulfate*", as well as the three core financial statements: the "Income Statement", "Cash Flow Statement", and "Balance Sheet".

---

### **1. Income Statement**

The income statement will reflect the profitability of the recycling business by tracking revenues, costs, and net profit.

#### **Revenue**

The primary revenue sources are the sale of recovered materials:

- **Lithium Sales**: Revenue generated from extracting and refining lithium for reuse in new batteries.

- **Cobalt Sales**: High-value material due to its critical role in battery cathodes.

- **Nickel Sales**: Revenue from selling nickel, used extensively in battery production.

- **Aluminum Sales**: Revenue from recovered aluminum, often used in battery casings or other components.

- **Manganese Sales**: Revenue from selling manganese for cathode production.

- **Copper Sales**: Revenue from recovering copper, widely used in battery wiring and components.

- **Sodium Sulfate Sales**: Revenue from selling byproducts like sodium sulfate, which can be used in industrial or chemical applications.

#### **Cost of Goods Sold (COGS)**

- **Collection Costs**: Transportation, storage, and handling of used EV batteries.

- **Processing Costs**: Costs of dismantling, shredding, chemical extraction, and purification processes for the different materials.

- *Lithium Recovery Costs*: Specialized processes like hydrometallurgy or direct lithium extraction.

- *Cobalt Recovery Costs*: High energy costs for separating cobalt from other materials.

- *Nickel Recovery Costs*: Extraction costs specific to refining nickel for reuse.

- *Aluminum Recovery Costs*: Shredding and melting aluminum casings.

- *Manganese Recovery Costs*: Costs for separating and processing manganese.

- *Copper Recovery Costs*: Mechanical or chemical separation of copper.

- *Sodium Sulfate Costs*: Processing costs for neutralizing and converting waste into sodium sulfate.

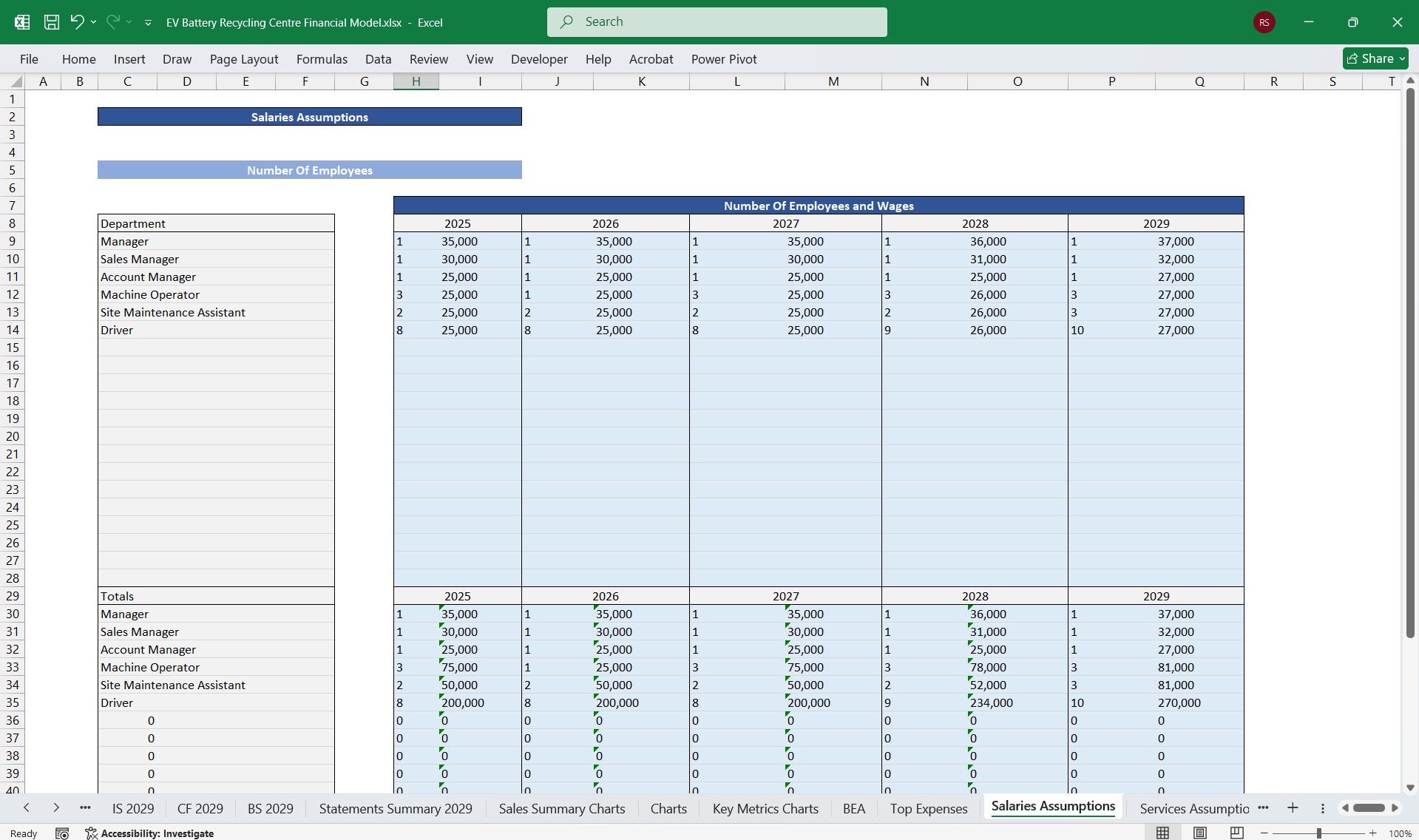

- **Labor Costs**: Salaries for skilled workers, engineers, and operators.

- **Utilities**: Energy and water costs, given the high-energy nature of recycling operations.

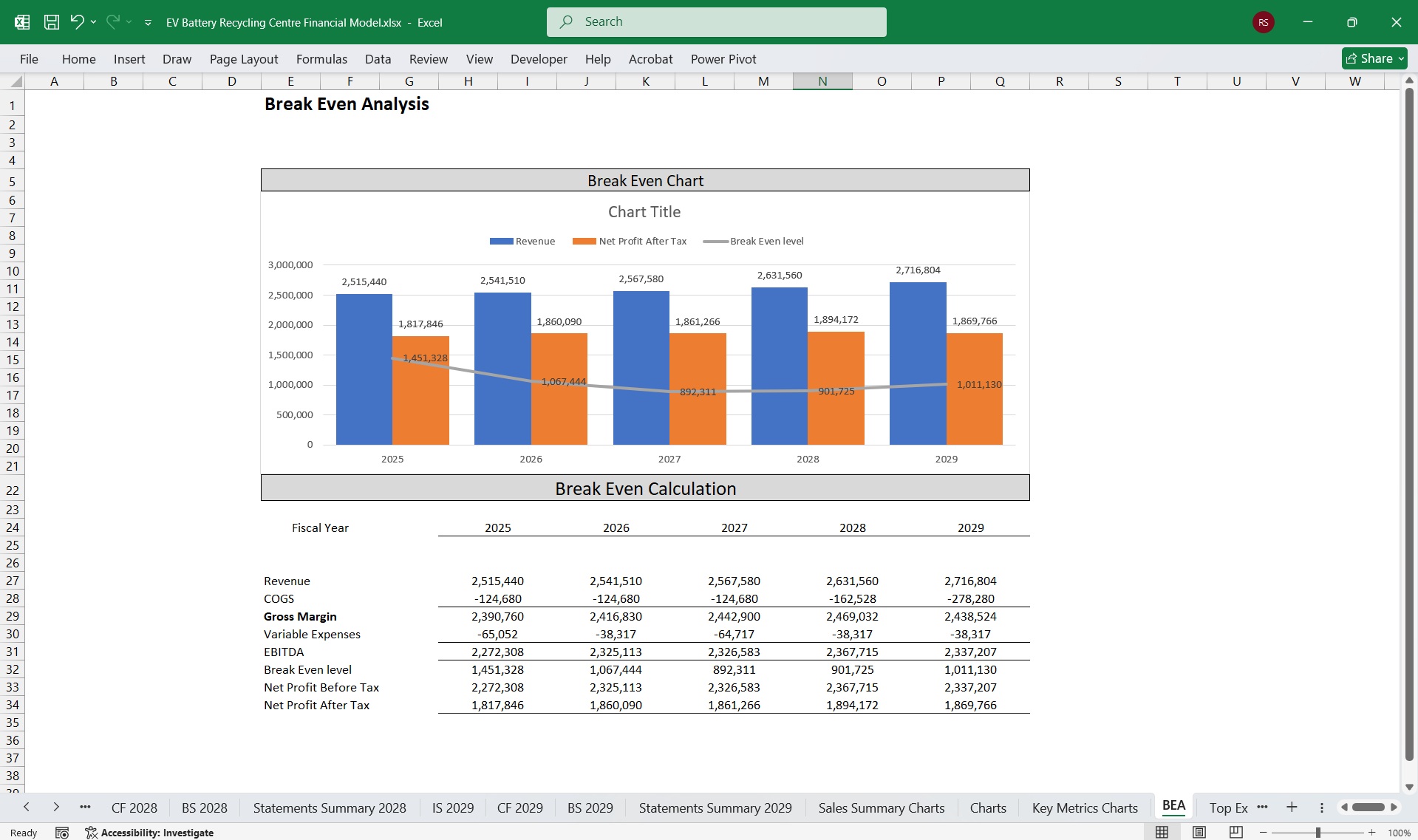

#### **Gross Profit**: Total Revenue - COGS.

#### **Operating Expenses**

- **Research & Development (R&D)**: Investments in improving battery recycling technologies and optimizing recovery rates for valuable materials.

- **Sales & Marketing**: Expenses to market recovered materials and build partnerships with EV manufacturers.

- **Administrative Expenses**: Overheads like salaries for administrative staff, office rent, and insurance.

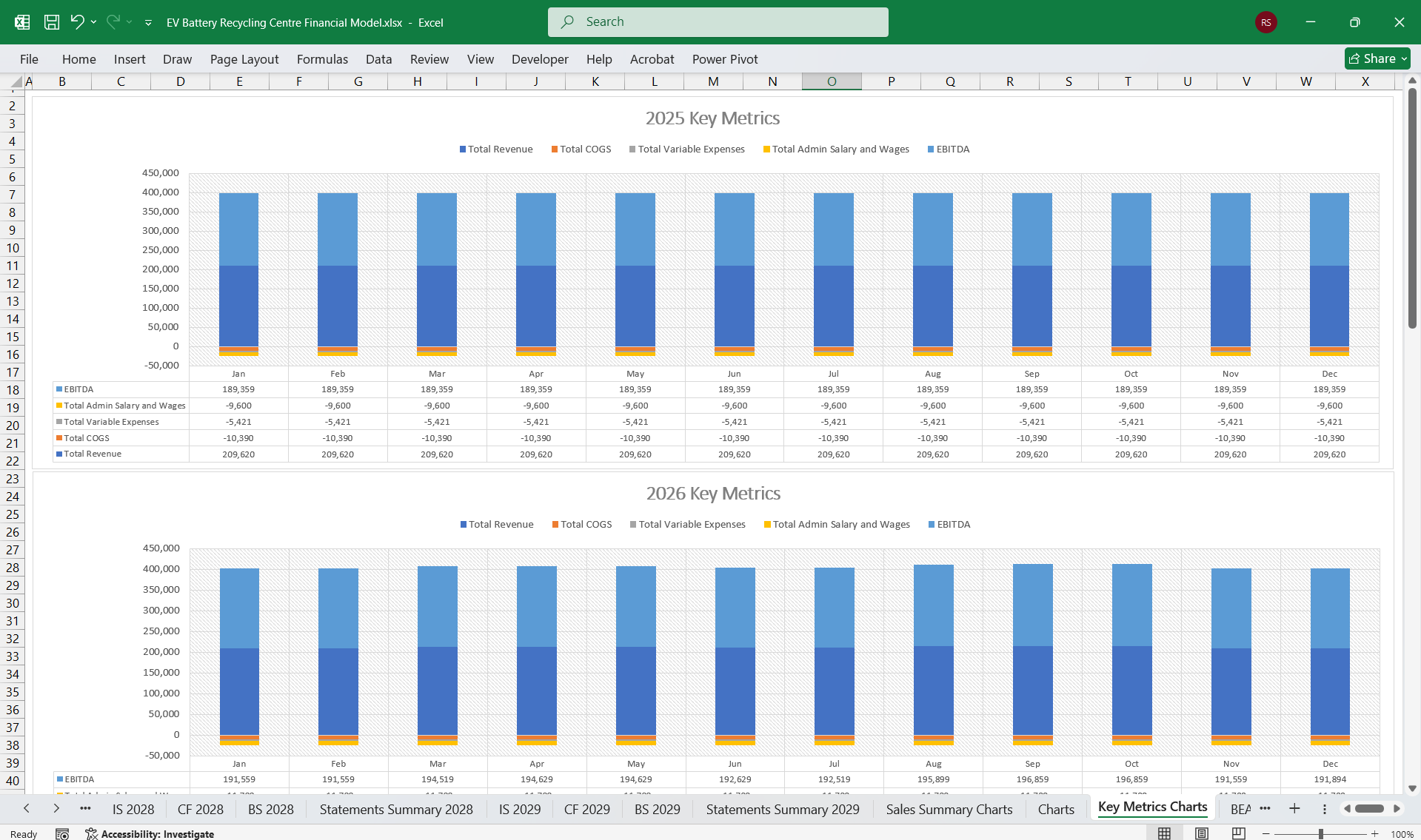

#### **EBITDA** (Earnings Before Interest, Taxes, Depreciation, and Amortization)

#### **Depreciation & Amortization**: Depreciation of recycling equipment and facilities.

#### **Operating Income (EBIT)**: EBITDA - Depreciation and Amortization.

#### **Interest Expense**: Costs of any debt used to finance operations or equipment.

#### **Income Taxes**: Tax obligations on profits.

#### **Net Income**: Bottom-line profitability.

---

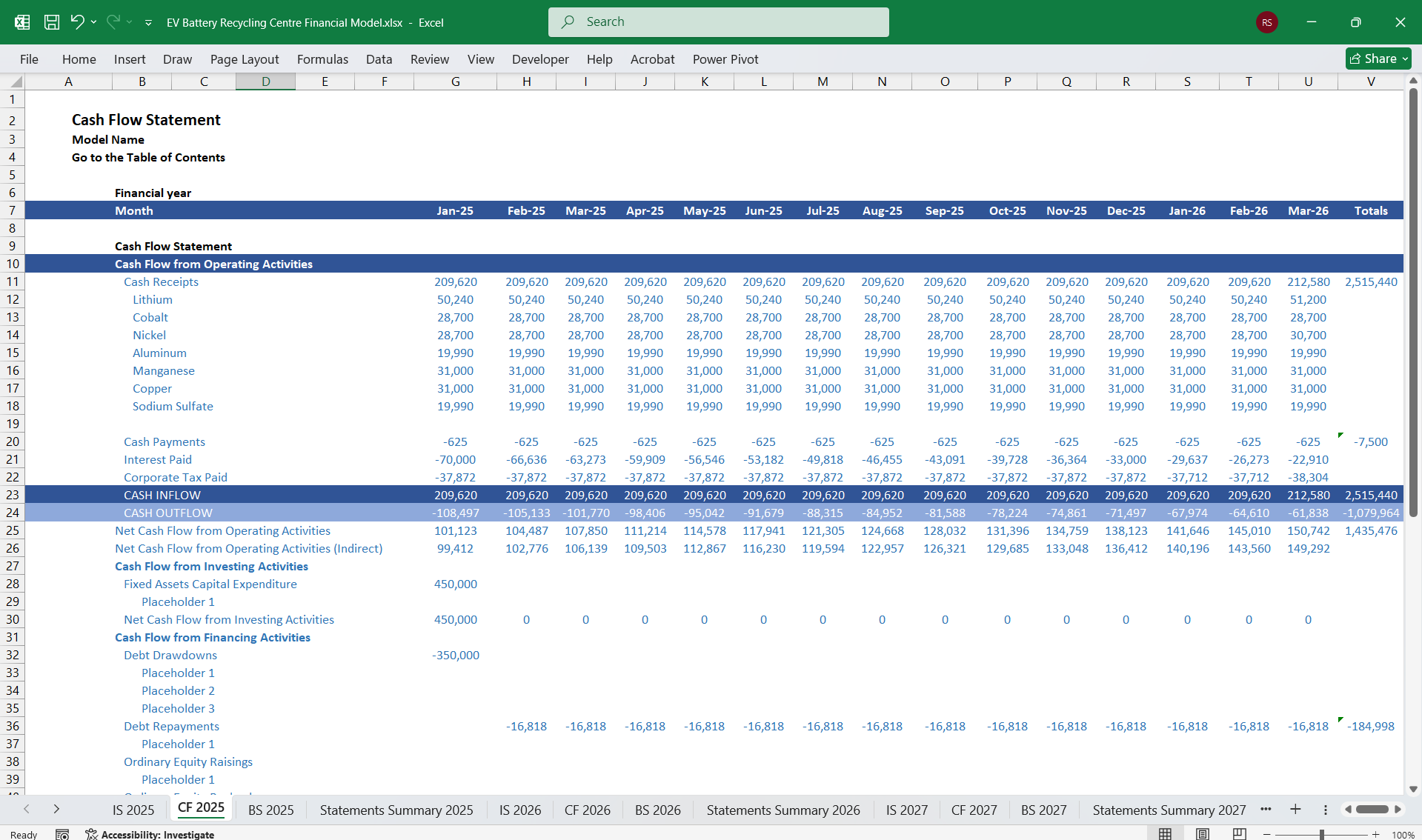

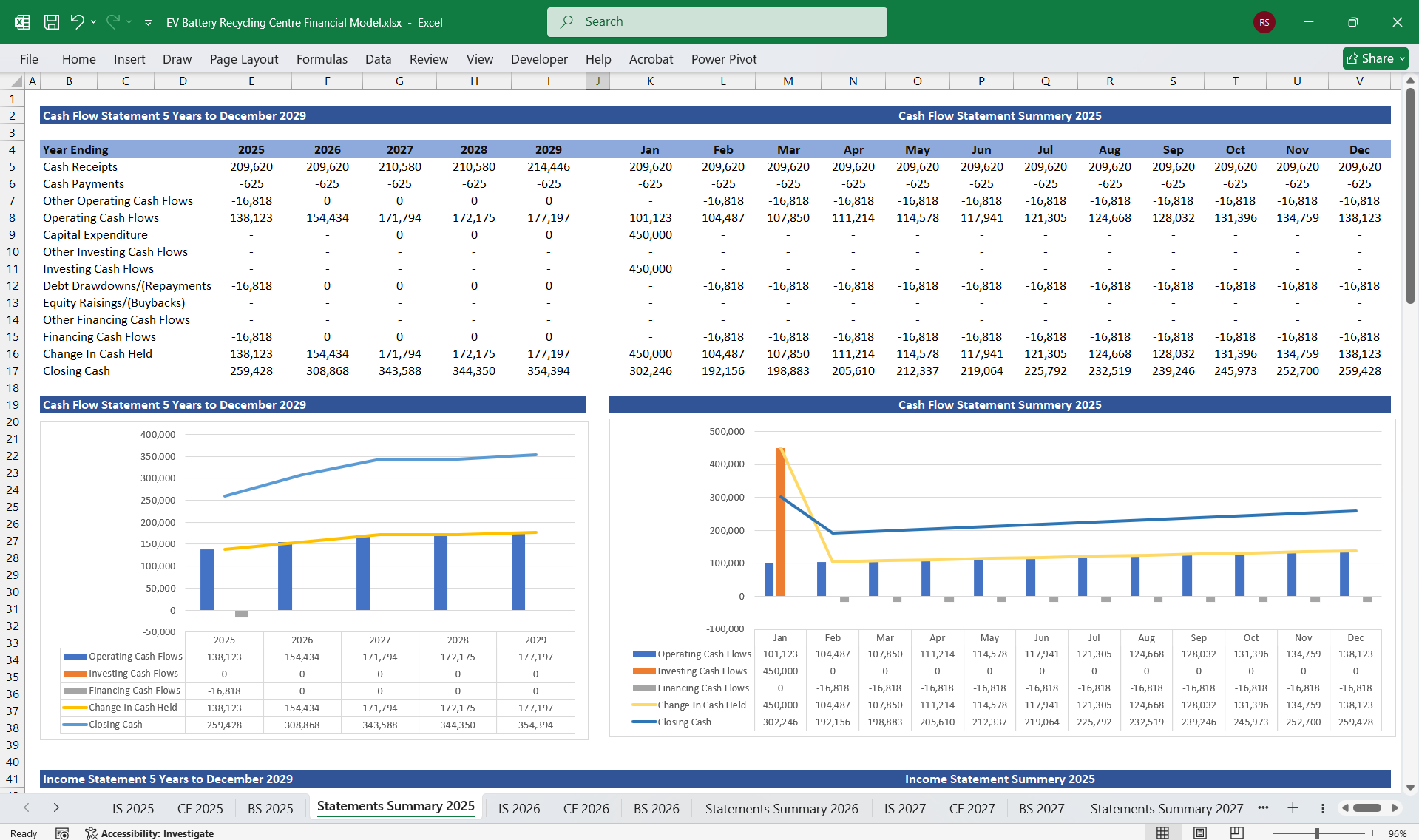

### **2. Cash Flow Statement**

The cash flow statement tracks cash inflows and outflows to measure liquidity and financial health.

#### **Cash Flow from Operating Activities**

- **Net Income**: Derived from the income statement.

- **Adjustments for Non-Cash Expenses**: Depreciation and amortization of assets.

- **Changes in Working Capital**:

- *Accounts Receivable*: Payments owed by buyers of recovered materials.

- *Inventory*: Value of recovered materials awaiting sale.

- *Accounts Payable*: Amounts owed to suppliers or utility providers.

- **Cash Received from Customers**: Inflows from selling recovered lithium, cobalt, nickel, etc.

- **Payments to Suppliers and Employees**: Outflows for labor, raw materials, utilities, and overhead costs.

#### **Cash Flow from Investing Activities**

- **Capital Expenditures (CapEx)**: Investments in recycling equipment, storage facilities, and technological upgrades.

- **Proceeds from Asset Sales**: Cash inflows from selling old or unusable machinery.

#### **Cash Flow from Financing Activities**

- **Debt Issuance**: Loans or bonds issued to fund expansion.

- **Equity Financing**: Capital raised by issuing shares.

- **Loan Repayments or Dividends**: Outflows for repaying debt or paying shareholders.

#### **Net Cash Flow**: Total from operating, investing, and financing activities.

---

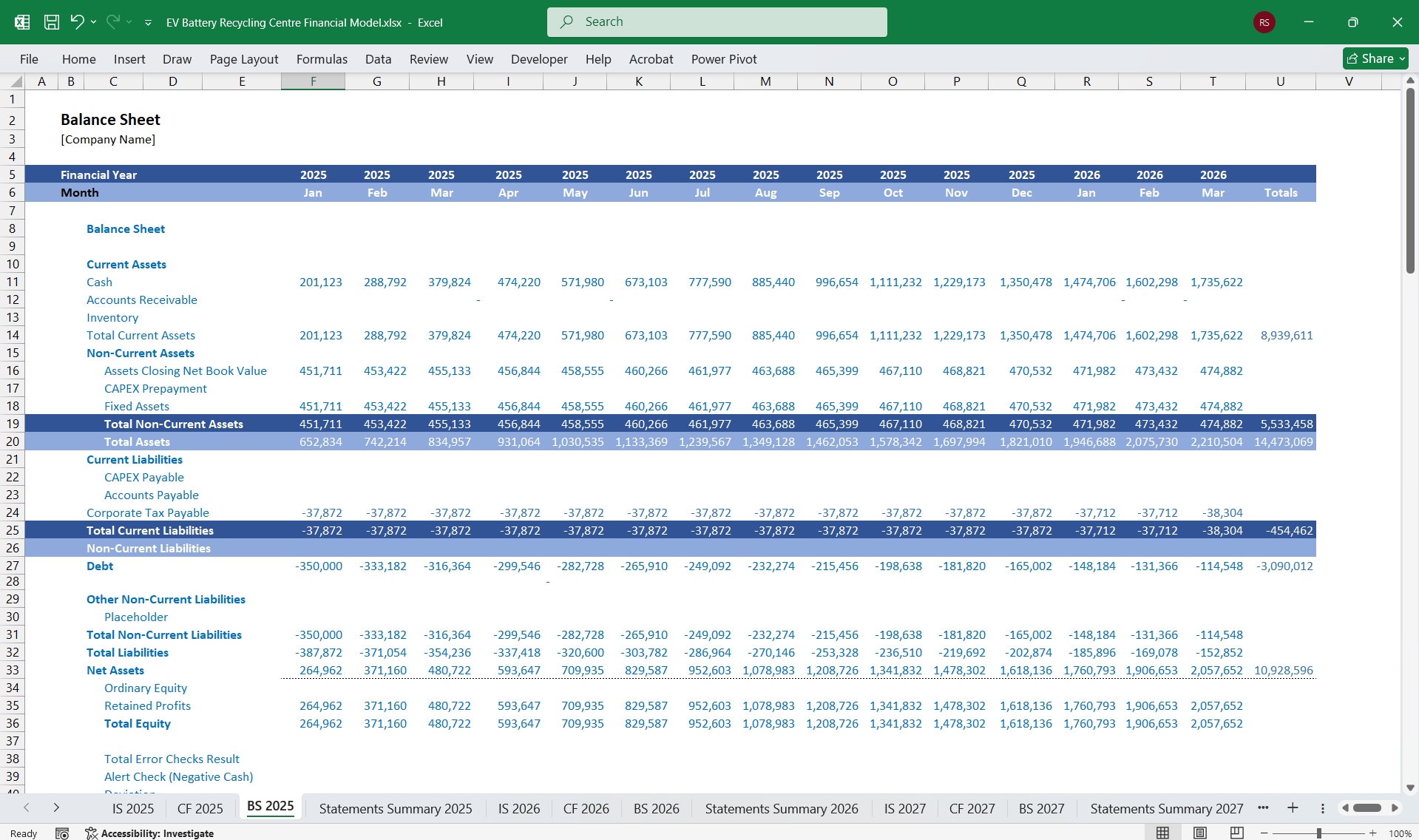

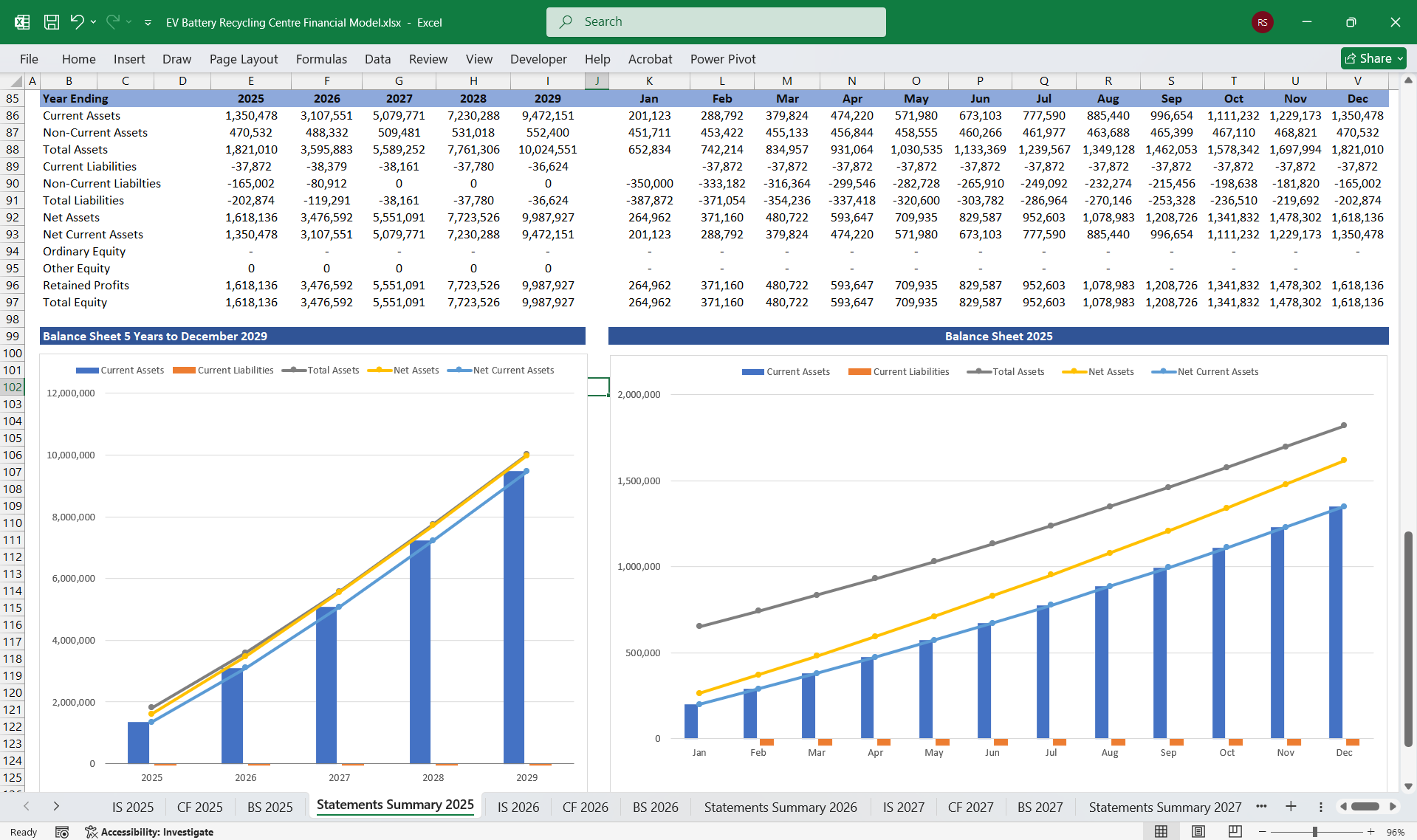

### **3. Balance Sheet**

The balance sheet provides a snapshot of the company’s assets, liabilities, and equity at a specific point in time.

#### **Assets**

- **Current Assets**

- *Cash and Cash Equivalents*: Funds available for operations.

- *Accounts Receivable*: Payments owed by customers for materials sold.

- *Inventory*: Recovered materials (lithium, cobalt, nickel, etc.) waiting for sale.

- **Non-Current Assets**

- *Property, Plant, and Equipment (PP&E)*: Recycling equipment, machinery, and facilities, net of depreciation.

- *Intangible Assets*: Patents or proprietary technologies for battery recycling.

#### **Liabilities**

- **Current Liabilities**

- *Accounts Payable*: Unpaid bills to suppliers and contractors.

- *Short-Term Debt*: Loans or credit lines due within the year.

- **Non-Current Liabilities**

- *Long-Term Debt*: Loans used for capital investments.

- *Deferred Tax Liabilities*: Tax obligations deferred to future periods.

#### **Equity**

- **Common Stock**: Value of shares issued.

- **Retained Earnings**: Accumulated profits reinvested into the business.

- **Additional Paid-In Capital**: Capital contributions from shareholders.

---

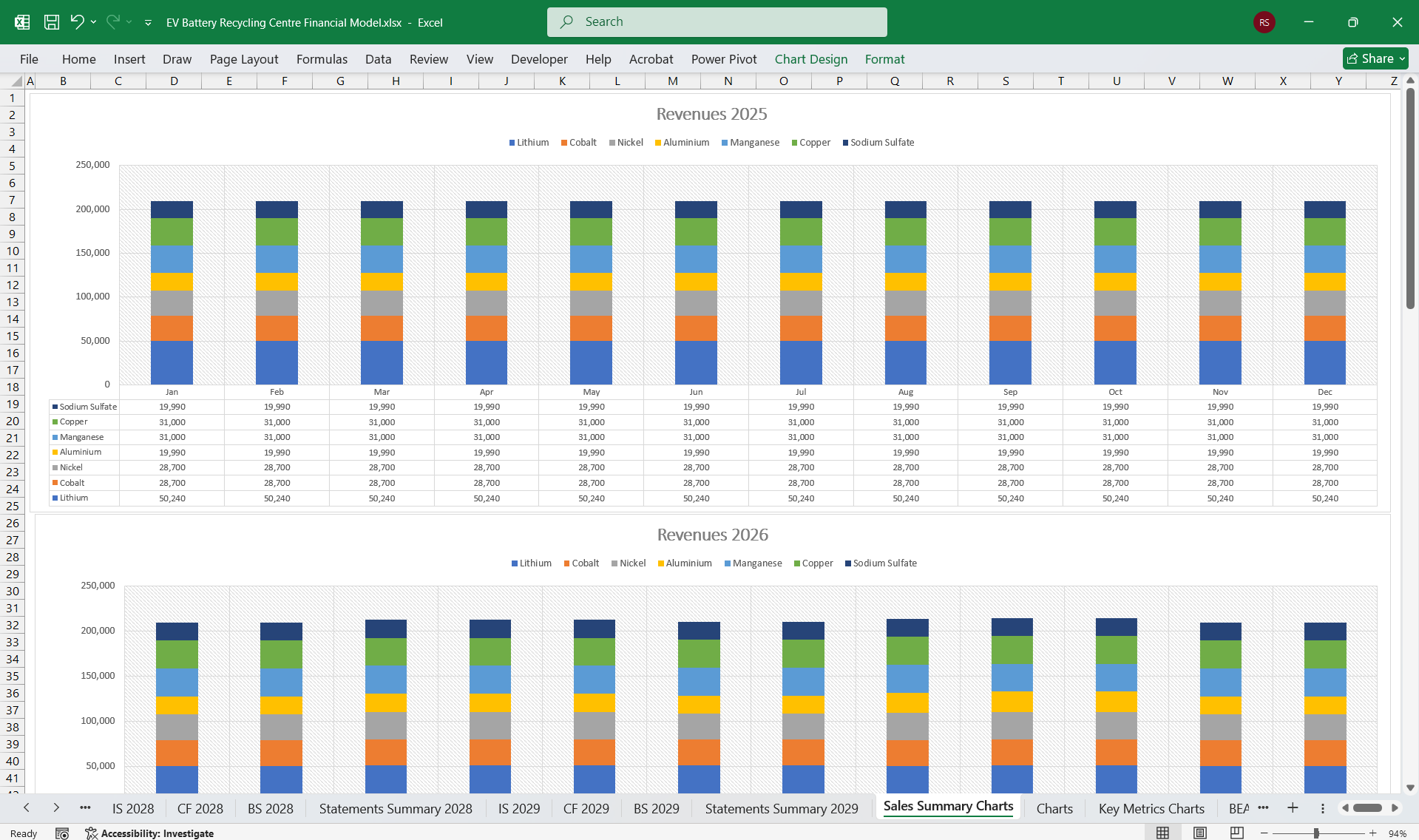

### **4. Material-Specific Financial Tracking**

Each material can be treated as a profit center, with its own revenue and cost analysis. Here’s how to track them:

#### **Lithium**

- *Revenue*: High demand for lithium due to its role in new EV batteries.

- *Costs*: High energy and chemical costs for lithium extraction.

#### **Cobalt**

- *Revenue*: Premium pricing due to limited global supply and high demand.

- *Costs*: Extraction costs influenced by technological complexity.

#### **Nickel**

- *Revenue*: Stable pricing, significant role in battery cathodes.

- *Costs*: Refining nickel from mixed materials.

#### **Aluminum**

- *Revenue*: Recovered aluminium is often sold for casing production.

- *Costs*: Lower compared to other materials.

#### **Manganese**

- *Revenue*: Used in cathodes, with moderate pricing.

- *Costs*: Refining manganese is relatively affordable.

#### **Copper**

- *Revenue*: High-value material with widespread use.

- *Costs*: Separation and refinement costs are moderate.

#### **Sodium Sulfate**

- *Revenue*: Byproduct of battery processing, sold for industrial uses.

- *Costs*: Low processing costs, derived from chemical neutralization.

---

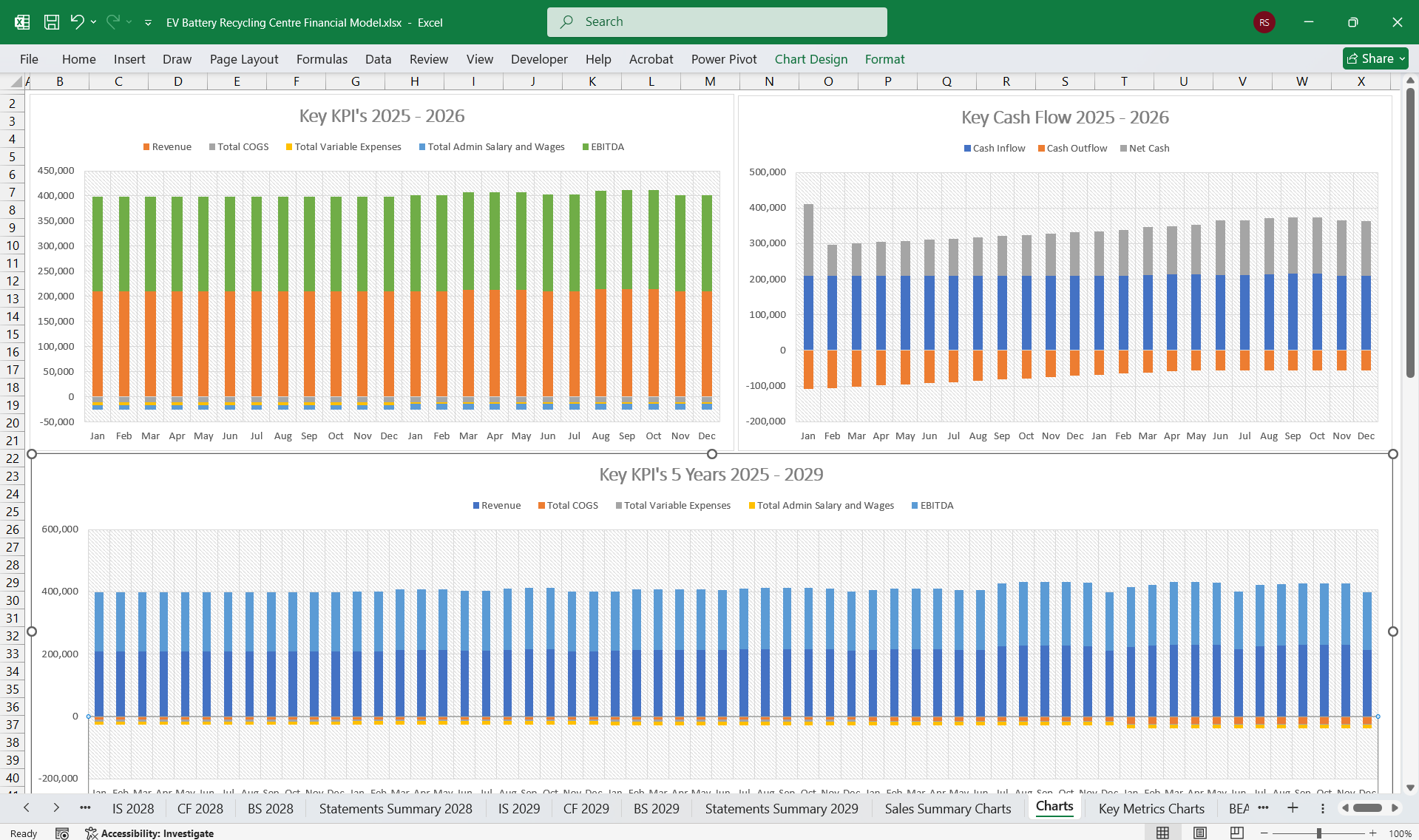

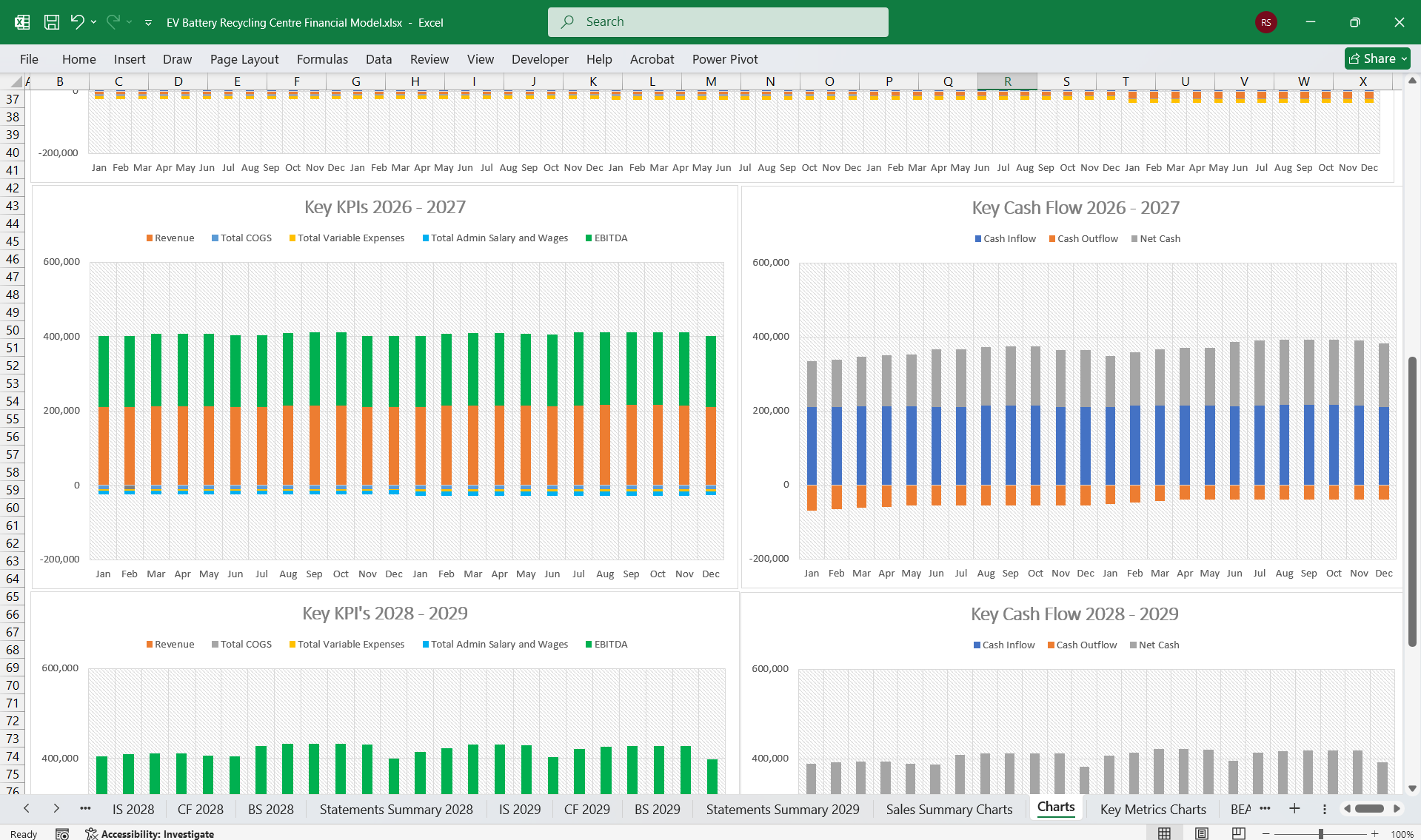

### **5. Key Performance Indicators (KPIs)**

To measure success and efficiency, include the following KPIs:

- **Recovery Rate per Material**: Percentage of lithium, cobalt, nickel, etc., recovered from each battery.

- **Revenue per Ton of Batteries Processed**: Tracks profitability based on input volume.

- **Gross Margin per Material**: Profitability of individual materials like lithium and cobalt.

- **Energy Consumption per Ton**: Efficiency of recycling processes.

- **Net Income Margin**: Overall profitability as a percentage of revenue.

---

This model ensures a comprehensive financial analysis of an EV battery recycling business, with detailed focus on key materials and operational processes.

The financial model for an **EV Battery Recycling Company**, incorporates key revenue sections for materials: "Lithium", "Cobalt", "Nickel", "Aluminum", "Manganese", "Copper**, and "Sodium Sulfate*", as well as the three core financial statements: the "Income Statement", "Cash Flow Statement", and "Balance Sheet".

---

### **1. Income Statement**

The income statement will reflect the profitability of the recycling business by tracking revenues, costs, and net profit.

#### **Revenue**

The primary revenue sources are the sale of recovered materials:

- **Lithium Sales**: Revenue generated from extracting and refining lithium for reuse in new batteries.

- **Cobalt Sales**: High-value material due to its critical role in battery cathodes.

- **Nickel Sales**: Revenue from selling nickel, used extensively in battery production.

- **Aluminum Sales**: Revenue from recovered aluminum, often used in battery casings or other components.

- **Manganese Sales**: Revenue from selling manganese for cathode production.

- **Copper Sales**: Revenue from recovering copper, widely used in battery wiring and components.

- **Sodium Sulfate Sales**: Revenue from selling byproducts like sodium sulfate, which can be used in industrial or chemical applications.

#### **Cost of Goods Sold (COGS)**

- **Collection Costs**: Transportation, storage, and handling of used EV batteries.

- **Processing Costs**: Costs of dismantling, shredding, chemical extraction, and purification processes for the different materials.

- *Lithium Recovery Costs*: Specialized processes like hydrometallurgy or direct lithium extraction.

- *Cobalt Recovery Costs*: High energy costs for separating cobalt from other materials.

- *Nickel Recovery Costs*: Extraction costs specific to refining nickel for reuse.

- *Aluminum Recovery Costs*: Shredding and melting aluminum casings.

- *Manganese Recovery Costs*: Costs for separating and processing manganese.

- *Copper Recovery Costs*: Mechanical or chemical separation of copper.

- *Sodium Sulfate Costs*: Processing costs for neutralizing and converting waste into sodium sulfate.

- **Labor Costs**: Salaries for skilled workers, engineers, and operators.

- **Utilities**: Energy and water costs, given the high-energy nature of recycling operations.

#### **Gross Profit**: Total Revenue - COGS.

#### **Operating Expenses**

- **Research & Development (R&D)**: Investments in improving battery recycling technologies and optimizing recovery rates for valuable materials.

- **Sales & Marketing**: Expenses to market recovered materials and build partnerships with EV manufacturers.

- **Administrative Expenses**: Overheads like salaries for administrative staff, office rent, and insurance.

#### **EBITDA** (Earnings Before Interest, Taxes, Depreciation, and Amortization)

#### **Depreciation & Amortization**: Depreciation of recycling equipment and facilities.

#### **Operating Income (EBIT)**: EBITDA - Depreciation and Amortization.

#### **Interest Expense**: Costs of any debt used to finance operations or equipment.

#### **Income Taxes**: Tax obligations on profits.

#### **Net Income**: Bottom-line profitability.

---

### **2. Cash Flow Statement**

The cash flow statement tracks cash inflows and outflows to measure liquidity and financial health.

#### **Cash Flow from Operating Activities**

- **Net Income**: Derived from the income statement.

- **Adjustments for Non-Cash Expenses**: Depreciation and amortization of assets.

- **Changes in Working Capital**:

- *Accounts Receivable*: Payments owed by buyers of recovered materials.

- *Inventory*: Value of recovered materials awaiting sale.

- *Accounts Payable*: Amounts owed to suppliers or utility providers.

- **Cash Received from Customers**: Inflows from selling recovered lithium, cobalt, nickel, etc.

- **Payments to Suppliers and Employees**: Outflows for labor, raw materials, utilities, and overhead costs.

#### **Cash Flow from Investing Activities**

- **Capital Expenditures (CapEx)**: Investments in recycling equipment, storage facilities, and technological upgrades.

- **Proceeds from Asset Sales**: Cash inflows from selling old or unusable machinery.

#### **Cash Flow from Financing Activities**

- **Debt Issuance**: Loans or bonds issued to fund expansion.

- **Equity Financing**: Capital raised by issuing shares.

- **Loan Repayments or Dividends**: Outflows for repaying debt or paying shareholders.

#### **Net Cash Flow**: Total from operating, investing, and financing activities.

---

### **3. Balance Sheet**

The balance sheet provides a snapshot of the company’s assets, liabilities, and equity at a specific point in time.

#### **Assets**

- **Current Assets**

- *Cash and Cash Equivalents*: Funds available for operations.

- *Accounts Receivable*: Payments owed by customers for materials sold.

- *Inventory*: Recovered materials (lithium, cobalt, nickel, etc.) waiting for sale.

- **Non-Current Assets**

- *Property, Plant, and Equipment (PP&E)*: Recycling equipment, machinery, and facilities, net of depreciation.

- *Intangible Assets*: Patents or proprietary technologies for battery recycling.

#### **Liabilities**

- **Current Liabilities**

- *Accounts Payable*: Unpaid bills to suppliers and contractors.

- *Short-Term Debt*: Loans or credit lines due within the year.

- **Non-Current Liabilities**

- *Long-Term Debt*: Loans used for capital investments.

- *Deferred Tax Liabilities*: Tax obligations deferred to future periods.

#### **Equity**

- **Common Stock**: Value of shares issued.

- **Retained Earnings**: Accumulated profits reinvested into the business.

- **Additional Paid-In Capital**: Capital contributions from shareholders.

---

### **4. Material-Specific Financial Tracking**

Each material can be treated as a profit center, with its own revenue and cost analysis. Here’s how to track them:

#### **Lithium**

- *Revenue*: High demand for lithium due to its role in new EV batteries.

- *Costs*: High energy and chemical costs for lithium extraction.

#### **Cobalt**

- *Revenue*: Premium pricing due to limited global supply and high demand.

- *Costs*: Extraction costs influenced by technological complexity.

#### **Nickel**

- *Revenue*: Stable pricing, significant role in battery cathodes.

- *Costs*: Refining nickel from mixed materials.

#### **Aluminum**

- *Revenue*: Recovered aluminium is often sold for casing production.

- *Costs*: Lower compared to other materials.

#### **Manganese**

- *Revenue*: Used in cathodes, with moderate pricing.

- *Costs*: Refining manganese is relatively affordable.

#### **Copper**

- *Revenue*: High-value material with widespread use.

- *Costs*: Separation and refinement costs are moderate.

#### **Sodium Sulfate**

- *Revenue*: Byproduct of battery processing, sold for industrial uses.

- *Costs*: Low processing costs, derived from chemical neutralization.

---

### **5. Key Performance Indicators (KPIs)**

To measure success and efficiency, include the following KPIs:

- **Recovery Rate per Material**: Percentage of lithium, cobalt, nickel, etc., recovered from each battery.

- **Revenue per Ton of Batteries Processed**: Tracks profitability based on input volume.

- **Gross Margin per Material**: Profitability of individual materials like lithium and cobalt.

- **Energy Consumption per Ton**: Efficiency of recycling processes.

- **Net Income Margin**: Overall profitability as a percentage of revenue.

---

This model ensures a comprehensive financial analysis of an EV battery recycling business, with detailed focus on key materials and operational processes.

This Best Practice includes

1 Excel Financial Model

Further information

Provides thorough oversight, tracking, and reporting of EV Battery recycling company finances, including updates on budget utilisation and projections.