Originally published: 27/04/2023 15:09

Publication number: ELQ-32516-1

View all versions & Certificate

Publication number: ELQ-32516-1

View all versions & Certificate

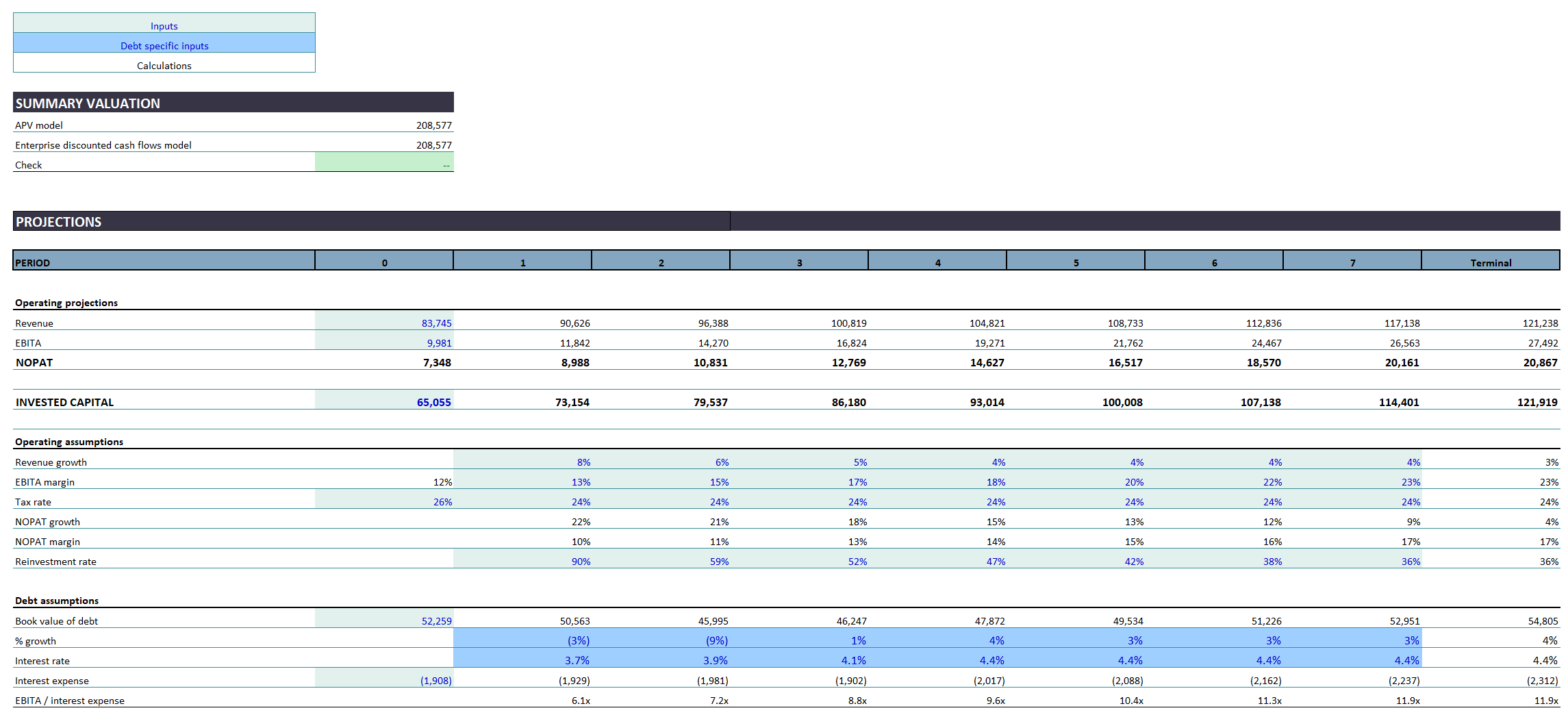

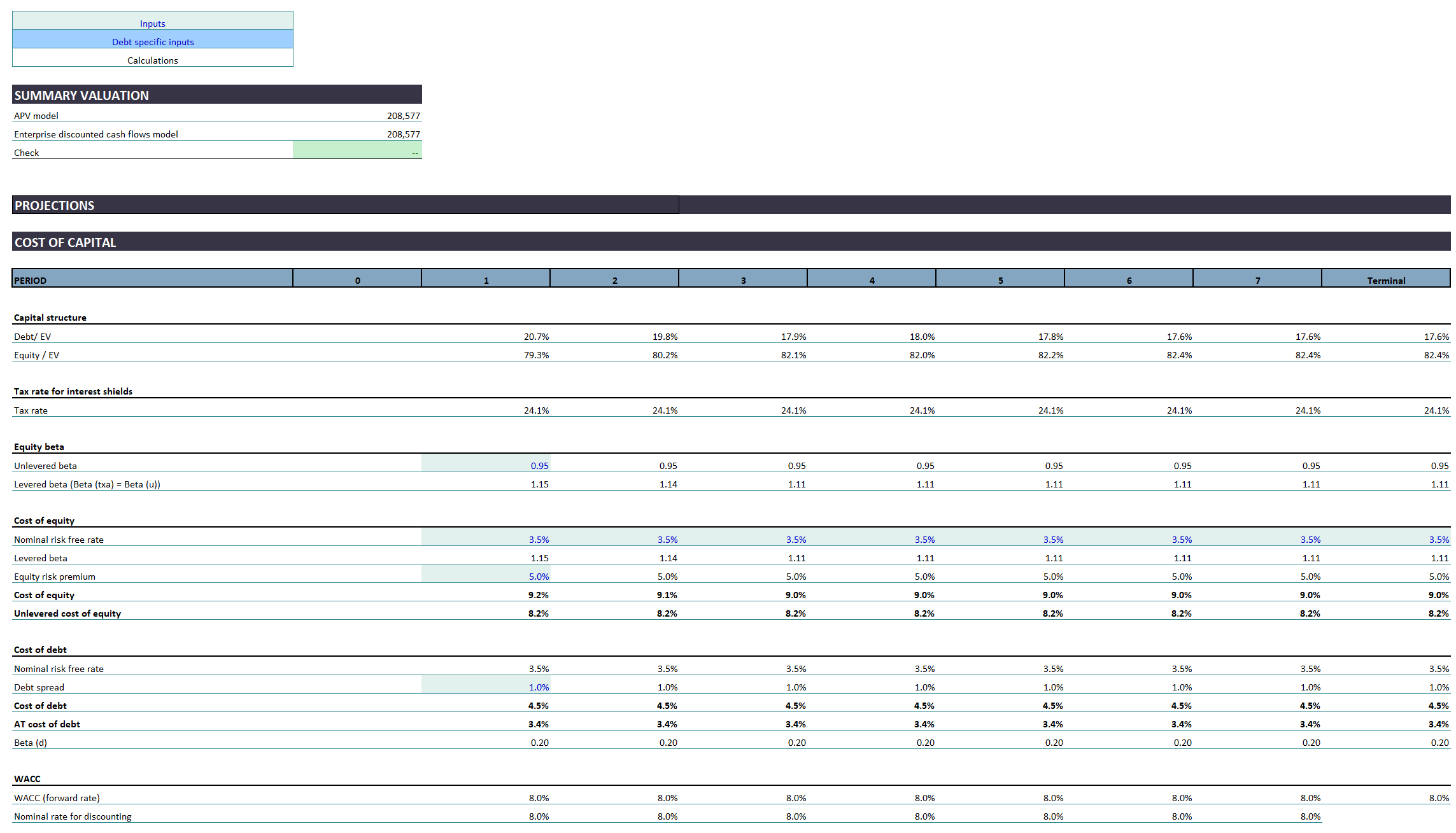

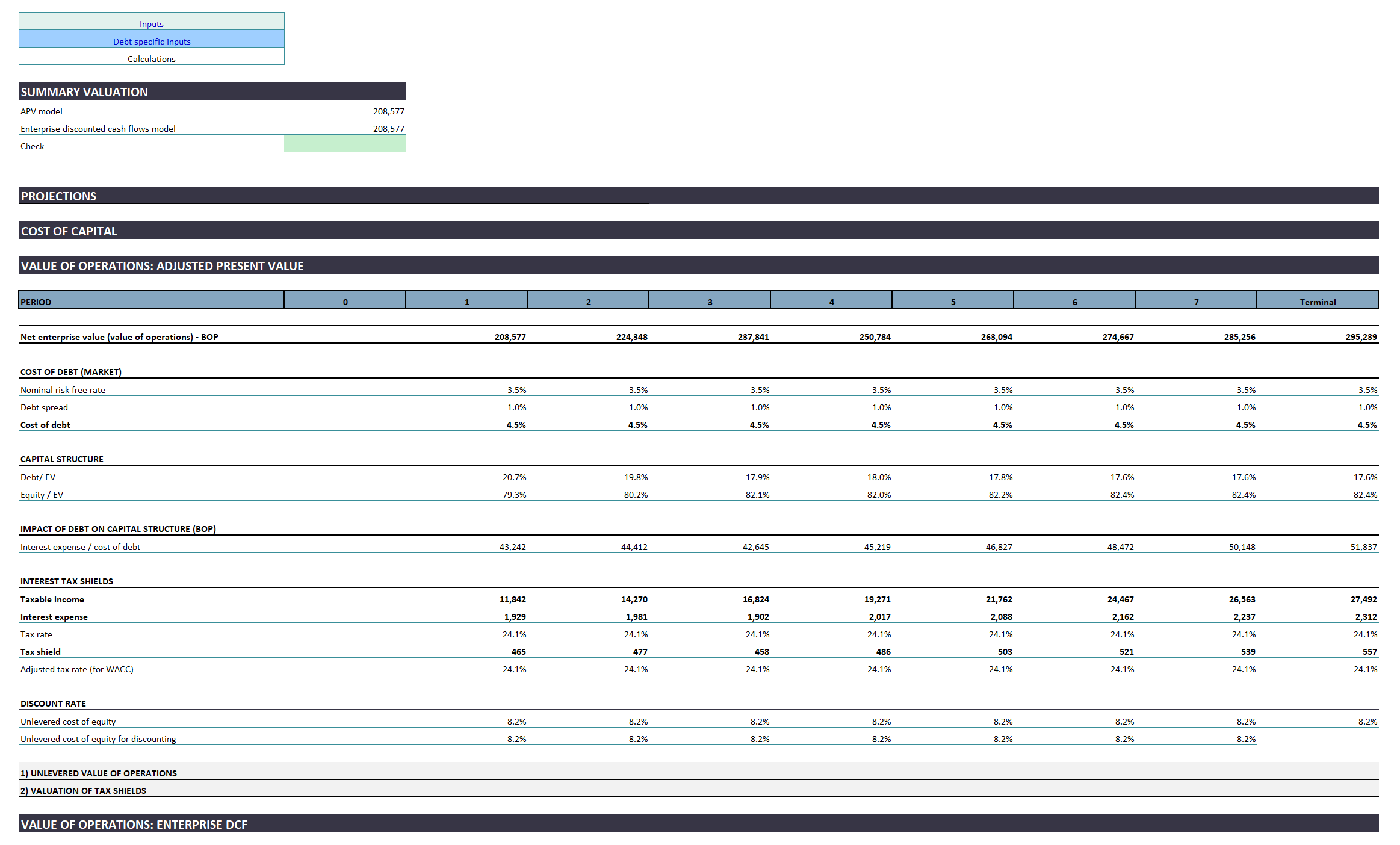

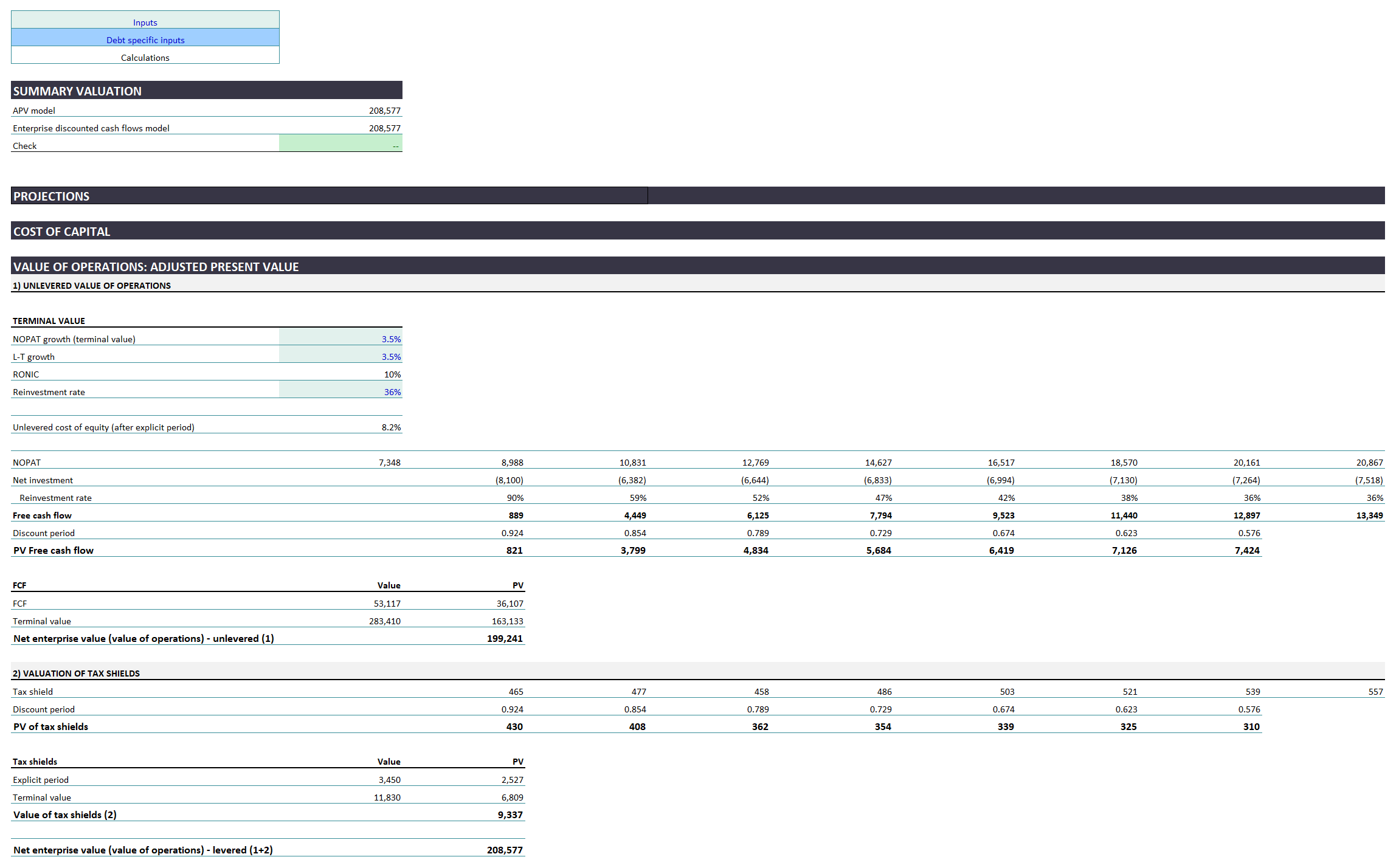

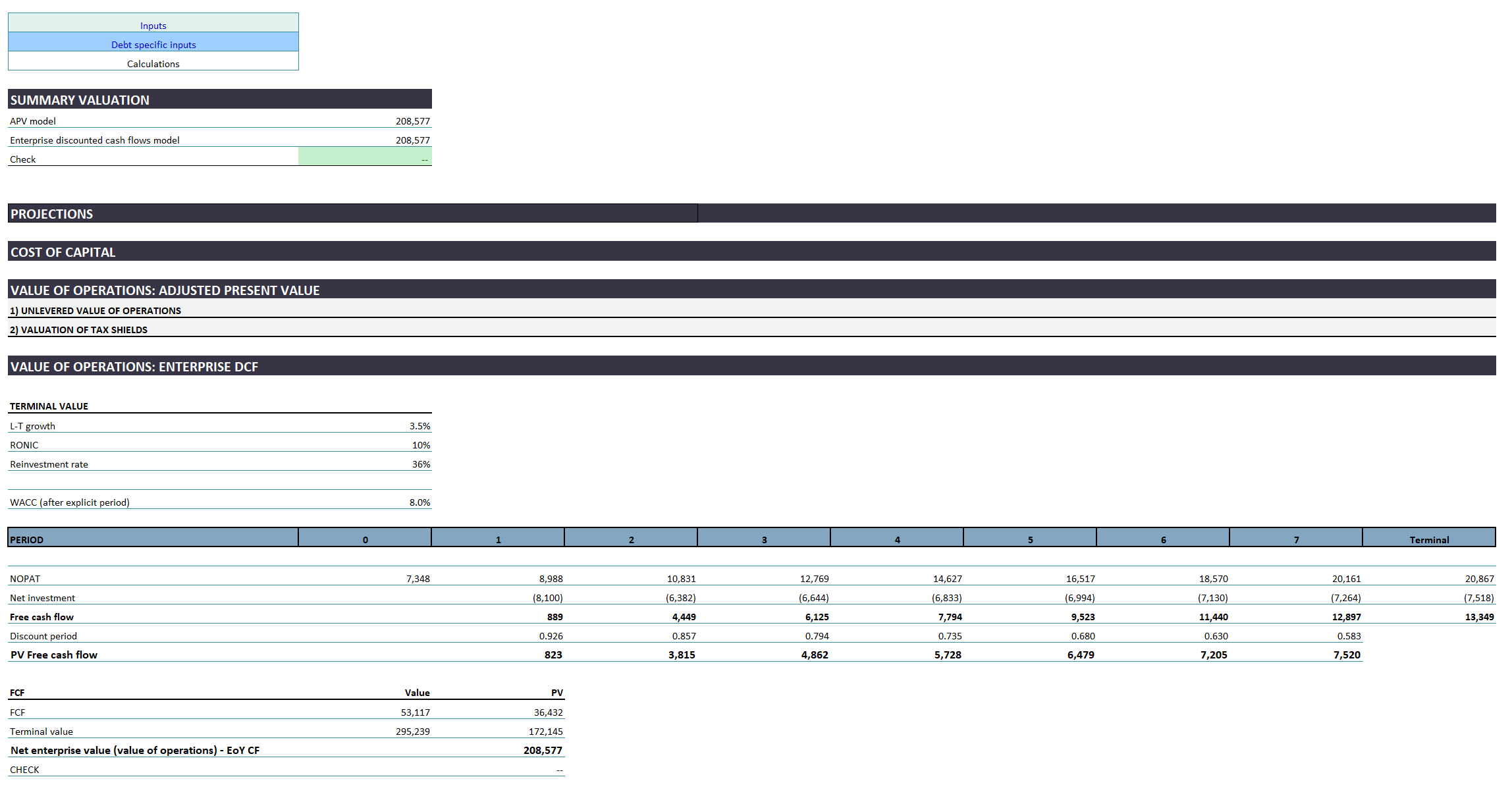

Adjusted present value (APV) valuation

Estimating unlevered value of operations and value of tax shields to calculate the impact of different capital structures on company valuation

Diverse background in finance, policy-making, and international affairs, with a focus on investment banking, corporate finance, public finance, and multilateral development finance.Follow