Originally published: 24/12/2018 09:19

Last version published: 22/03/2019 11:42

Publication number: ELQ-70866-2

View all versions & Certificate

Last version published: 22/03/2019 11:42

Publication number: ELQ-70866-2

View all versions & Certificate

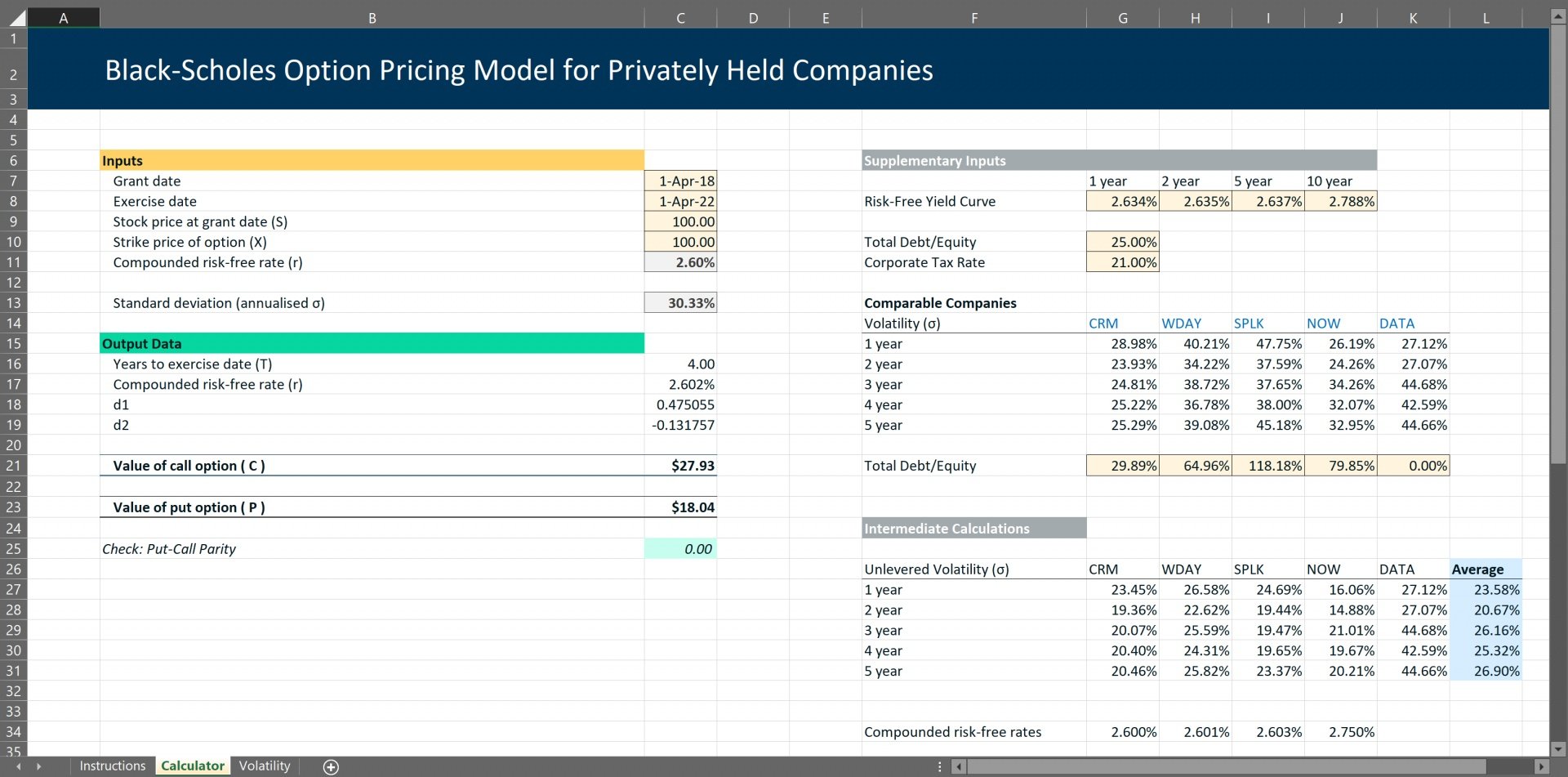

Black-Scholes Option Pricing Excel Model (with add-on for Privately Held Companies)

An Excel Black-Scholes option pricing model with volatility estimator for privately held companies