Originally published: 17/07/2026 12:53

Publication number: ELQ-94203-1

View all versions & Certificate

Publication number: ELQ-94203-1

View all versions & Certificate

Staffing / Recruiting Agency Acquisition & SBA Underwriting Financial Model

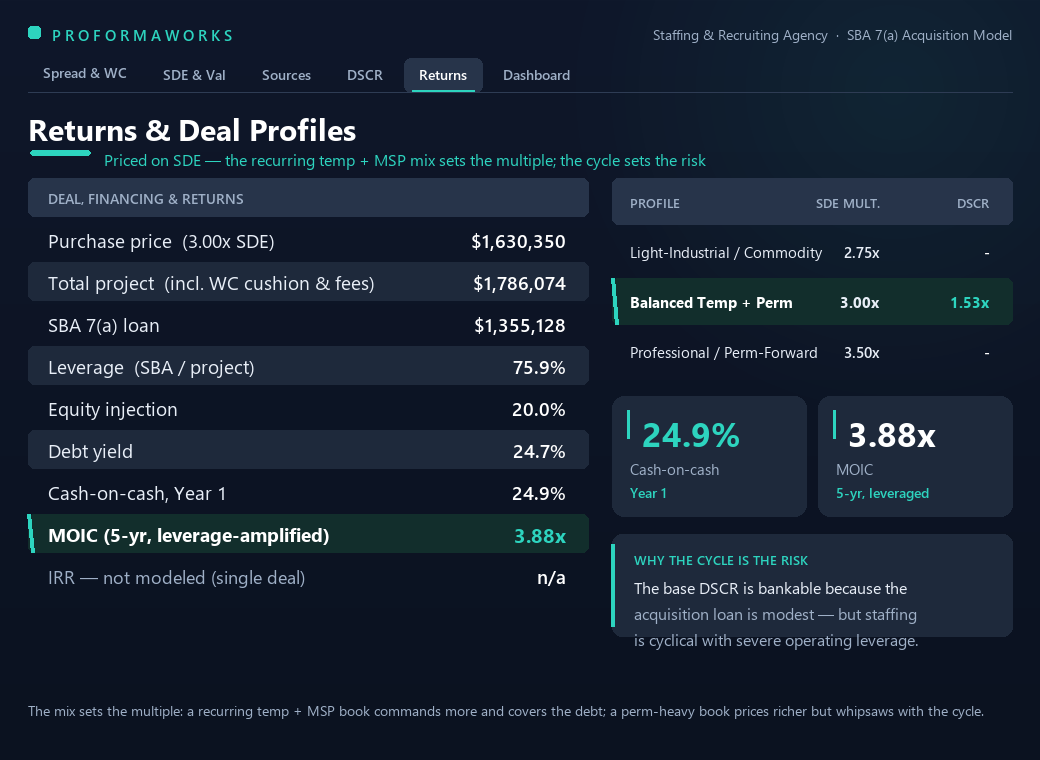

A 5-year SBA 7(a) model to buy a staffing / recruiting agency: underwrite the bill-pay spread and the DSO payroll-funding gap, not the pass-through revenue.

Further information

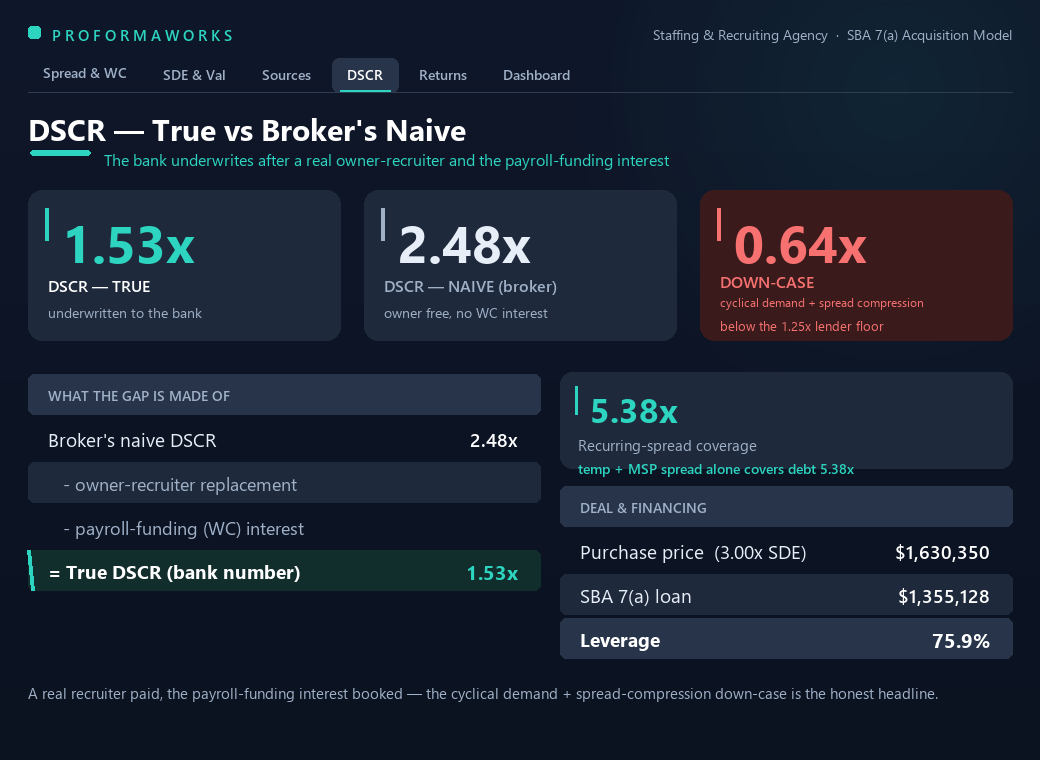

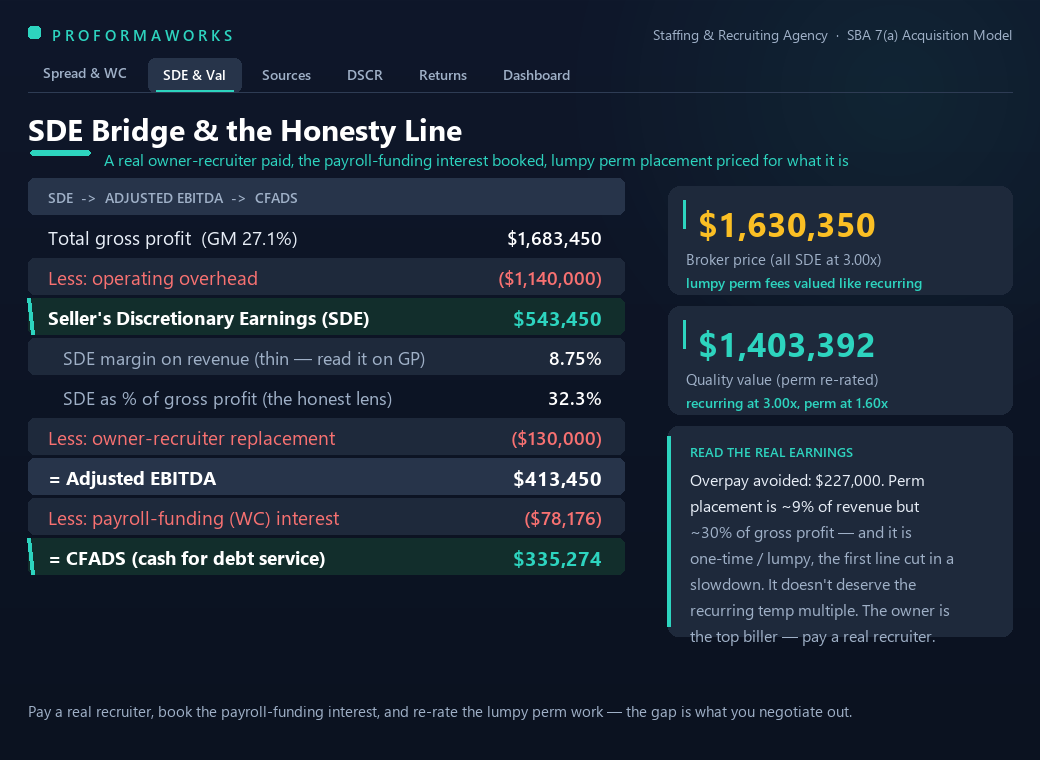

Underwrite a staffing / recruiting agency acquisition to an SBA lender's DSCR — on the spread and the working-capital gap, not the pass-through revenue.

You are buying an independent staffing / recruiting agency with an SBA 7(a) loan and need a lender-ready underwrite of the spread and the payroll-funding gap.

You want a simple operating budget or a startup projection — this is an acquisition underwriting model, not a general P&L forecast.