Originally published: 15/05/2024 06:02

Publication number: ELQ-24915-1

View all versions & Certificate

Publication number: ELQ-24915-1

View all versions & Certificate

Audit Substantive Procedures

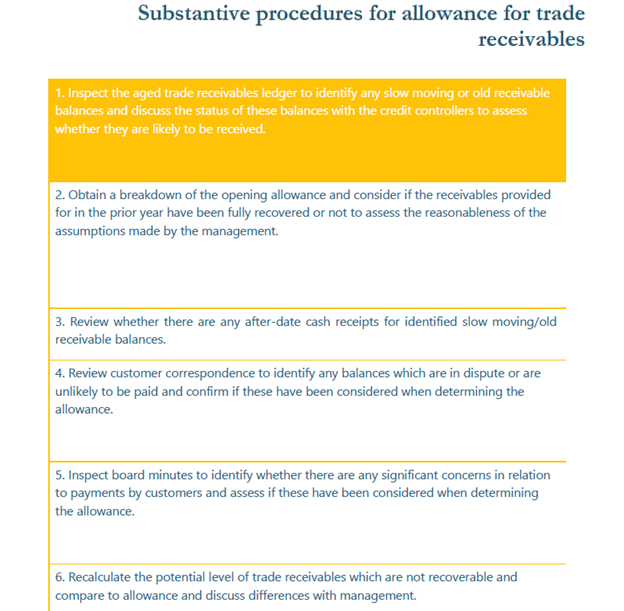

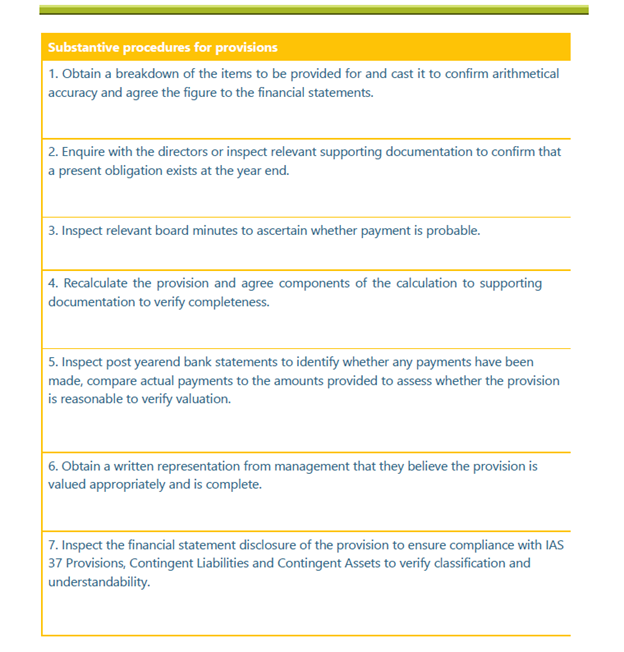

Substantive Audit Procedures to download in PDF format.

A Preofessional CA with 10+ Years Experience in MENA & Big 4 - Financial Analysis, Accounting & Regulatory ComplianceFollow 10