Publication number: ELQ-45416-1

View all versions & Certificate

PV Hybridisation Model — Evaluate Co-located BESS on an Existing Solar PV Plant Across 8 Markets

Production-ready Excel model for financial evaluation of BESS co-location on an existing solar PV plant. 8 countries, 3 revenue streams

Further information

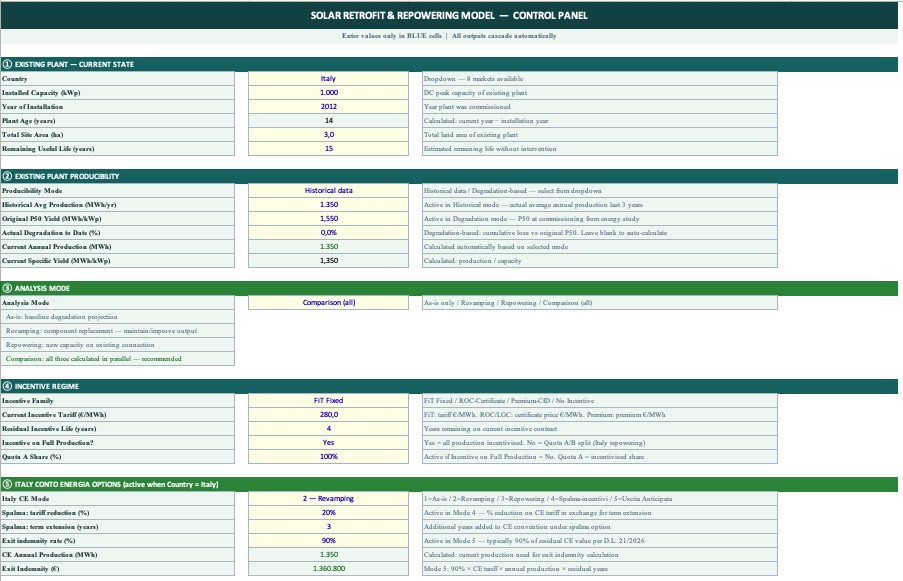

This model enables developers, advisors and asset managers to evaluate the incremental financial value of adding co-located BESS to an existing solar PV plant across 8 international markets, producing a direct comparison between the FV as-is baseline and the FV+BESS hybrid scenario. It models the connection constraint that physically limits BESS dispatch during peak solar hours, calculates incremental BESS IRR against the FV baseline rather than against zero, applies country-specific incentive interaction logic — including all five Italy D.L. 21/2026 CE options — and structures separate BESS financing to produce a standalone BESS DSCR alongside the combined FV+BESS project metrics. BESS revenue streams cover Arbitrage, Ancillary Services and Capacity Market with country-specific benchmarks and a 5% haircut, across Conservative, Base and Aggressive scenarios.

This model is best suited to utility-scale solar PV plants of 10 MWp and above that have available headroom on their grid connection — typically plants where the authorised connection capacity in MW AC exceeds the average output during off-peak and night hours, creating dispatchable capacity for BESS during those windows. It works particularly well for Italian CE plants under D.L. 21/2026 where the regulatory interaction between the existing incentive and the BESS co-location decision has five distinct paths, and for German EEG plants approaching expiry where the combination of expiring FiT and co-located BESS creates a transition strategy worth quantifying. It is also well suited to portfolio-level screening where multiple existing PV assets need to be ranked for hybridisation priority using a consistent financial methodology.

This model evaluates BESS co-location on existing solar PV plants and is not designed for greenfield PV+BESS projects, which should use the Solar PV Ultimate Model with its integrated BESS module. The connection constraint is modelled as a fixed derating factor — for sites where the constraint is particularly binding or where an hourly dispatch profile is available, the derating should be replaced with a site-specific calculation before any investment decision. It does not model grid import charging for the BESS — the battery charges from the FV plant only — and is therefore not appropriate for configurations where grid arbitrage is a primary revenue source. It should not be used as the sole basis for a final investment decision without a grid connection assessment, a BESS sizing study and legal review of the applicable incentive co-location rules in the relevant market.