Last version published: 12/05/2020 15:08

Publication number: ELQ-89233-2

View all versions & Certificate

How to work with VCs — 5 Step Early Stage Founders Guide

This complete guide is intended for founders who plan to raise their first round with “institutional” VCs.

Building MemoHub.io a learning platform for aspiring and junior analysts/VCsFollow

We’re an early-stage venture capital firm primarily focused on SaaS and online marketplaces. We’re based in Berlin, but we invest all over the world.Follow

Introduction

For many early stage founders it’s unclear what working with VCs means and how they should prepare for it. It’s perfectly fine, after all, it’s better for a founder to be an expert in its field rather than in Venture Capital.

This guide is intended for founders who plan to raise their first round with “institutional” VCs (a.k.a VC firms and not business angels) which is, most of the times, a Seed or Series A round. I’ll try to answer the question “What does it mean to work with VCs?” by describing the different interactions you’ll have with investors throughout the whole process:

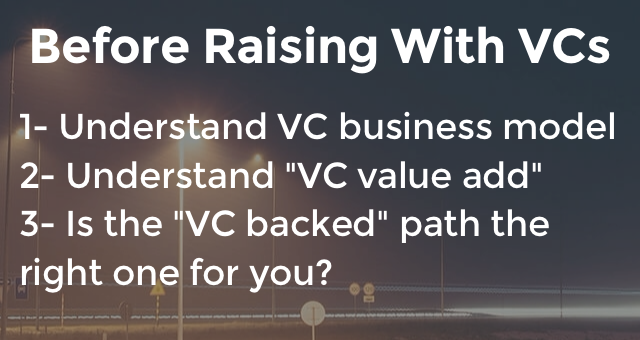

Part 1 (Steps 1-3): Before working with VCs.

• 1.1 - Understand how the VC model works.

• 1.2 - Define the most important values that you expect from VCs: money, mentorship, branding, network.

• 1.3 - Think whether the VC model is aligned with your aspirations as an entrepreneur or not.

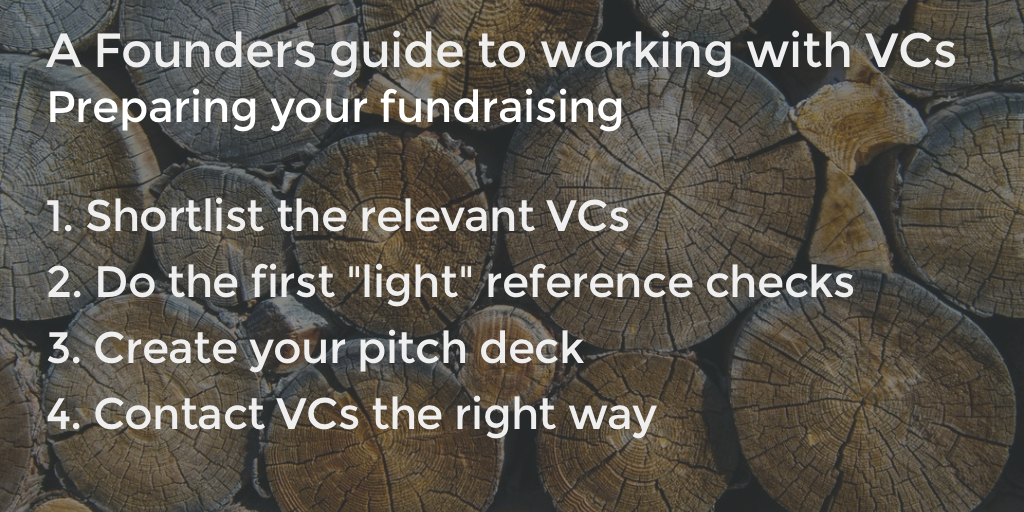

Part 2 (Steps 4-7): Preparation and introduction.

• 2.1 - Shortlist the relevant VCs.

• 2.2 - Do your first “light” reference checks.

• 2.3 - Create your fundraising material.

• 2.4 - Contact them.

Part 3 Steps 8-11): First contact & assessment phase.

• 3.1 - What happens in a VC firm during the assessment phase?

• 3.2 - You quickly receive a “No, we’re not interested”.

• 3.3 - You quickly receive a “Thanks, we’re looking at your company”.

• 3.4 - You don’t receive any answer.

Part 4: From term sheet to signed deal.

• 4.1 - The Term Sheet

• 4.2 - Deal Finalization

Part 5: Post investment.

• 5.1 - After the investment is made, when and how am I going to interact with my investors?

• 5.2 - How can I make the most out of my relationship with my investors?

• 5.3 - What is it like when things go wrongs?

This guide is not a “technical” guide that will teach you how to create a pitch deck or how to read a term sheet. Plenty of great posts already cover in details these aspects — some of which are linked in this guide. I’ll focus more on describing the interactions that you’ll have with the VCs during this journey.

I also insist on the fact that what follows is just a “framework.” Your own particular experience with VCs will depend on a myriad of factors such as who you are interacting with, the structure of the deal, the industry you’re operating in, your location, how “hot” your company is and many other factors.

- Step n°1 |

1.1 - How does the VC model work?

Why do VC firms invest money in startups?

To get a return on investment.

Most VCs you probably know are middlemen. They raise money from various sources (sovereign funds, foundations, family offices, large corporations, etc.), which are called LPs for Limited Partners, to invest in startups they believe can grow enough to provide a healthy return on investment. They invest X$ to acquire Y% of a startup and if the startup grows its value increases, and as a consequence, the X$ initially invested become XX$ dollars. The VC firm gets its cash once an “exit” happens meaning that the startup is either acquired by another company or goes public. Then the VC firm splits the result between their LPs and themselves.

Some firms invest their own money. It’s the case of family offices or corporate funds (Ex: Google Venture).

It’s an important aspect to keep in mind because it’s what drives their incentive.

The primary goal of “middlemen VCs” is to invest in companies which have the potential to provide a significant return on investment. That way they make their LPs happy from which they can raise more money to invest in more startups. If they don’t provide a good enough return on investment to their LPs, these VC firms won’t be able to raise more money and will eventually die or become zombies.

For firms which invest their “own money,” such as corporate funds, the incentives are a bit different. For instance, SalesForce Ventures or Google Ventures have other goals such as making “strategic” investments to get access to new markets, explore tech trends, help startup grow their ecosystem or to acquire them later.

When you start fundraising it’s important to understand what are the aims/incentive of the funds you want to work with because it will impact your relationship with them in the long term. Always be aware that they don’t give away money just for the sake of it but because they have their own goals too.

If you want to dig deeper on this topic here are some great posts:

The second aspect which is useful to understand before fundraising is how a fund structures his org chart.

Job titles in VC firms are something very complicated (and quite funny). There are so many variations that it’s impossible to list them all and the same job title might cover different responsibilities from one firm to the other. To be honest after two years working on the VC side I gave up trying to understand it.

The simplest way to picture it is to distinguish two hierarchy levels — for the investment team at least:

• People who have the power to make an investment decision: generally the “partner” level (Partner, Senior Partner, Managing Partner, Founding Partner, etc…)

• People who don’t have this power and need to convince the ones who have it: Analysts, Associates, Principals, etc.

It’s an important aspect to understand especially during the “first contact” phase that we’ll cover in more details in Part 3.

- Step n°2 |

1.2 - What value add should I expect from VCs?

Another important question that you should ask yourself before raising your first round with an institutional VC is: what values do you expect beyond money?

Obviously, the main aim of fundraising is to get money to grow your business, but what makes a great VC is not only the money it brings but also the value it can add:

• Expertise/knowledge: whether it’s because they have invested in many great companies and could build unique insights or because they are a “specialized” fund with industry specific knowledge.

• Network/mentorship: VCs can grant you access to a network of founders, big corporations or other investors that might be critical to your success.

• Operational support: more and more VC firms offer operational support through HR, marketing or design in residence teams or through a network of advisors.

• Branding: being backed by a firm with a great brand can open a lot of doors.

These four aspects are crucial because it’s what differentiates top VCs from the rest.

Defining what’s important depends on your particular situation and is worth thinking about. Depending on the business category or vertical you operate in the choice of your investor, beyond money, is a strategic one.

Nowadays every single VC firm advertises itself as “value-added.” By setting up your expectations before raising money it’ll be easier to assess whether a VC is bullshitting or not when you’ll “due diligence” them. - Step n°3 |

1.3 - Is the VC model aligned with my aspirations as an entrepreneur?

Once you’ve understood the two aspects above, it’s important to check whether the VC model is aligned with your aspirations as an entrepreneur. When you commit to the VC way, it’s almost impossible to go backward. This is why beyond money and support you should think whether the VC model fits you or not.

Quoting Steve Blank here: “The minute you take money from someone their business model now becomes yours.”

The VC model is not an “evil model”, but if it’s not aligned with your personal beliefs and if you haven’t made an effort to understand it, things can go horribly wrong. It’s essential to come prepared and to avoid going the “VC backed” way if you don’t believe in it (don’t do it just for the money).

I’ve written a post covering this topic in more details: “The rise of non VC compatible SaaS companies.” If you value control over speed, then you should consider other financing options. If you want to grow as fast as possible, the VC option is probably the best one.

Main takeaways from Part 1:

Before fundraising:

• Try to understand how the VC model works and what could be the implications when growing your business.

• Set your expectations regarding VC “value-add” before you raise.

• Thoroughly think whether building a VC backed company fits your aspirations as an entrepreneur. If not, don’t follow that path. - Step n°4 |

2.1 - Shortlisting the relevant VCs

If the core concept of the VC model is quite simple — money against company ownership to generate an ROI — many variations exist: large VC firms which have hundreds of millions of dollars, or even billions, under management versus micro VCs which raise less money and are leaner. Early stage VCs versus late stage VCs. Specialized VCs — investing in specific industries/verticals only — versus generalists. “Hands-on” VCs which are offering a lot of operational support to their startups versus “hands-off” VCs. Etc.

It’s the reason why rather than contacting every VC you’ll find; you need to shortlist the ones which are relevant for your startup AND for which your startup is relevant (it works both ways). In that perspective be sure to check for each VC firm:

1. The stage they invest in (seed, Series A, B, C…). The first thing to check is whether a fund invests in companies at your stage. If you’re an early stage company looking for a seed round, there is no need to contact funds investing in series B and more. This information is usually visible on their website.

2. Their Investment scope: the majority of VC firms limit their investments to specific types of companies and specific geographies. For instance, at Point Nine, we only invest in SaaS and Marketplaces (we don’t invest in social or gaming apps), mostly in Europe and North America even if we have some exceptions. Before contacting a VC, you need to check whether you fit their scope or not.

3. Their Investment thesis: most VCs have what they call an “investment thesis” which details precisely what they look for: the characteristics of the founding teams they like to back, the technologies they find exciting, the markets they think are promising… This document is the hardest to find as it’s not often accessible on their website. USV is an excellent example of a “thesis driven” fund.

4. Their “value add” / operational support: if during the “Before working with VCs” phase you’ve concluded that, beyond money, particular value-adds will be critical to your success, you need to find the investors who offer that. It’s key when you operate in specific industries or verticals as industry focused VCs can help tremendously: for examples funds specialized in Healthcare tech or Government Tech can provide operational support, network, and knowledge that non-specialized can’t.

Where do I find lists of VCs?

• Network: first ask fellow founders in your city. If they have already raised, it’s very likely that they have such a list.

• Incubators and Accelerators: if you’re part of an incubator don’t forget to ask them for a list of investors (if they don’t have one it’s a huge warning).

• A Google search: simple but effective, just Google “VC in your area” and you’ll probably find a spreadsheet created by a local investor or by a founder (this is what I found by Googling “VC in Paris” or “VC in NY”).

Startup directories: whether it’s on Crunchbase, AngelList, Dealroom or other directories you can filter VCs by geography.

How do I understand an investment scope and thesis?

Obviously, the first thing to do is to check their website. In most cases, you’ll be able to understand their investment scope: stage, types of companies and geographies they invest in.

Regarding their investment thesis, it can be trickier. If you are lucky, they’ll have shared it on their website. If it’s not the case check:

• Their blogs: reading what investors write on their blog is the best way to have a good idea of their investment thesis. Some of them even publish whole investment thesis.

• Their latest investments: by checking the latest investments of a VC firm on Crunchbase you can also get a rough idea of the trends they follow / the types of companies they like to back. - Step n°5 |

2.2 - Do your first “light” reference checks

Like in any industry you have bad VCs and good VCs. Good VCs can be a huge part of your success, and bad VCs can kill your business. It’s why it’s important to do a minimum of reference checks at that stage.

When shortlisting the VCs, you should try to collect the opinion of people who have worked with them:

• Other founders: whether it’s founders from their portfolio or who have tried to raise with them don’t hesitate to ask their opinion (during an event, through your network): what is it like to work with them? How did the fundraising process go? Do they recommend working with this VC firm? Are they known for harming startups?

Business angels: if you have business angels don’t forget to ask their opinion too.

Incubators and accelerators: they should be able to give you some feedback based on the experience of other incubated projects. Many accelerators and incubators have a private ranking of the VCs they have worked with.

At that stage, it’s probably not worth doing “deep reference checks” (which we will cover in part 4), but you should at least be aware of the reputation of the different funds you’ll approach. Don’t skip this phase.

Building MemoHub.io a learning platform for aspiring and junior analysts/VCsFollow