Publication number: ELQ-64921-1

View all versions & Certificate

Wind Hybridisation Model — Evaluate Co-located BESS on an Existing Onshore Wind Farm Across 8 Markets

Wind Hybridisation Model — Evaluate Co-located BESS on an Existing Onshore Wind Farm Across 8 Markets, Including Curtailment Recovery

Further information

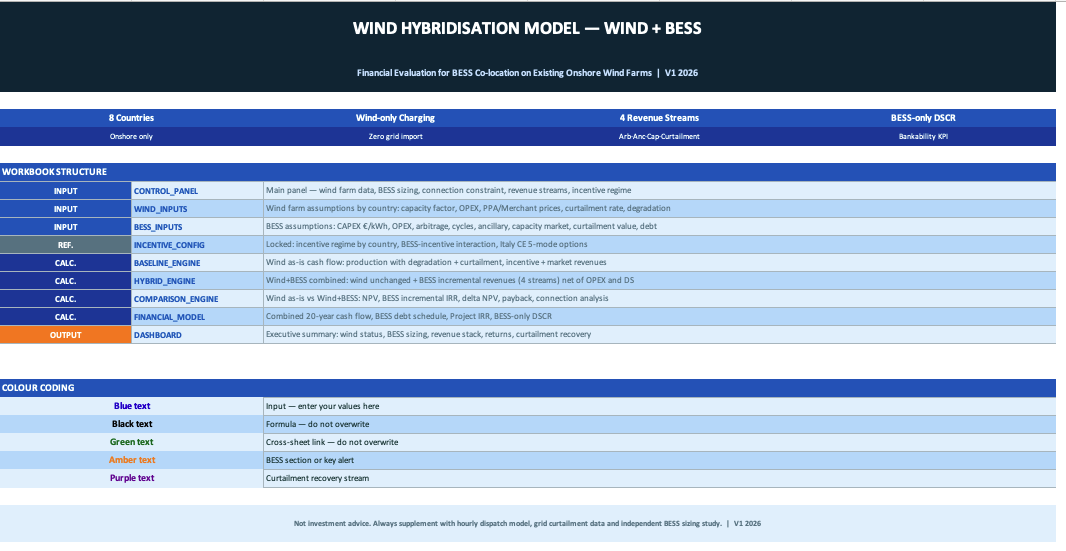

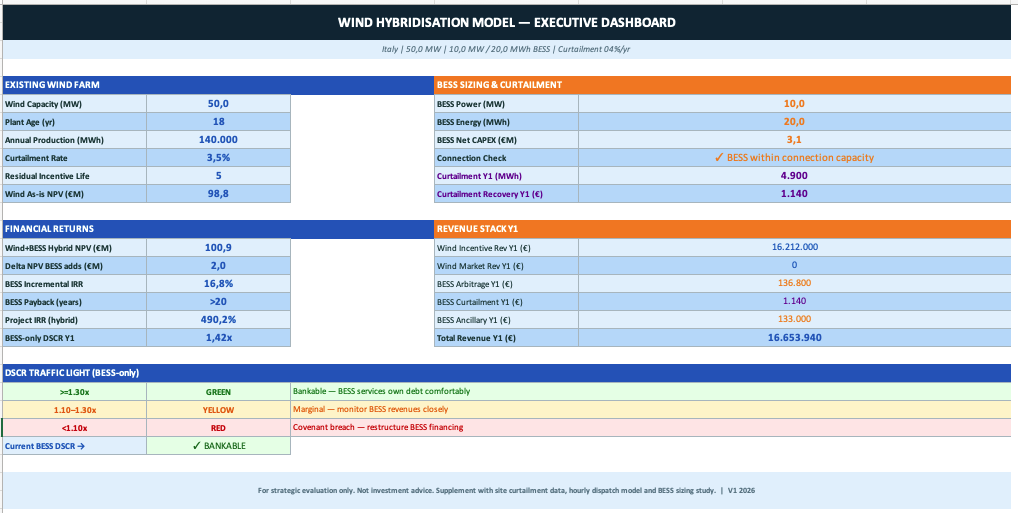

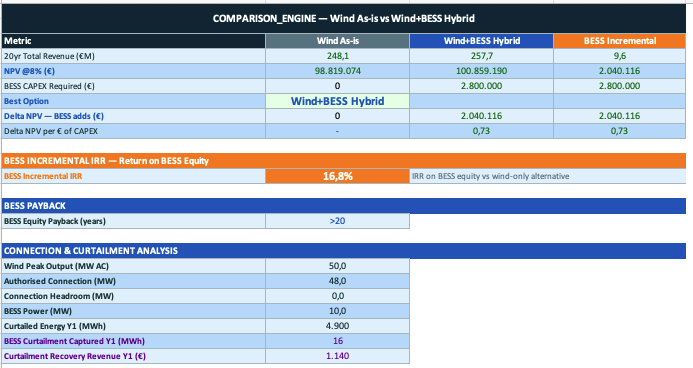

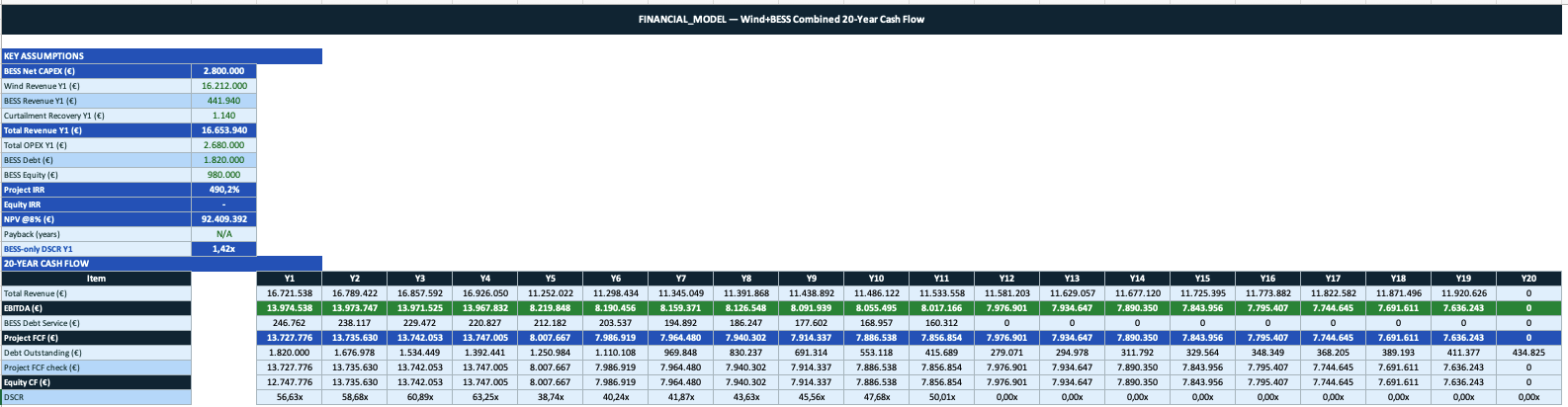

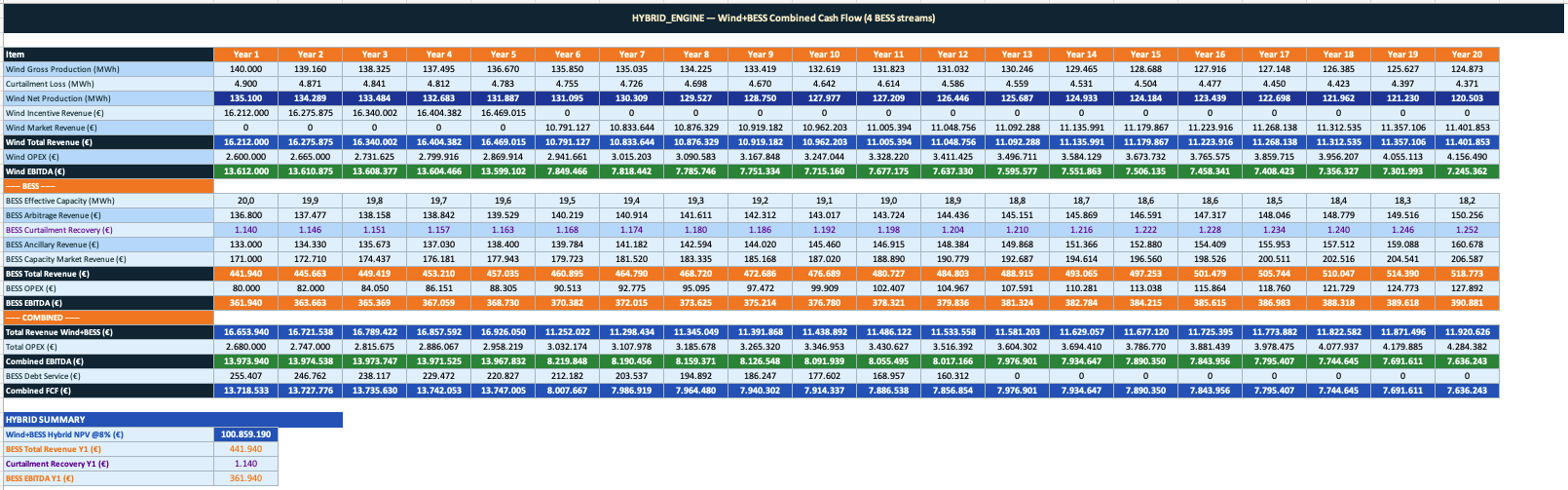

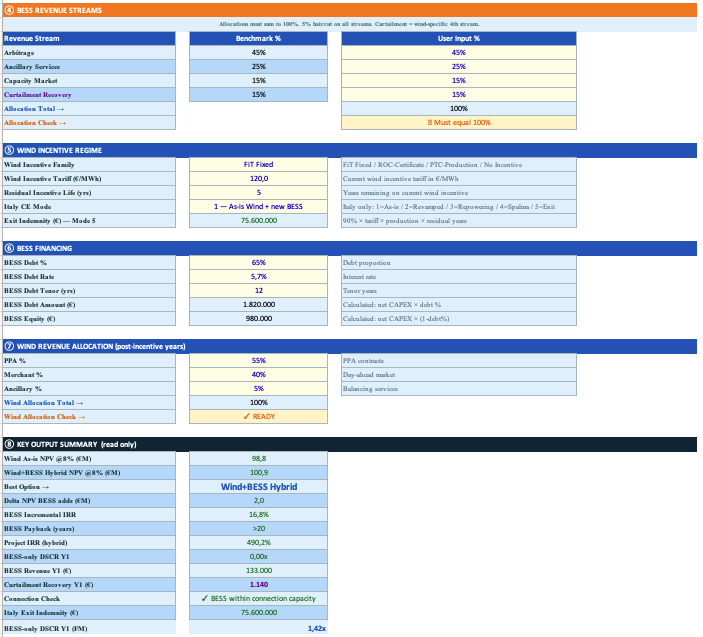

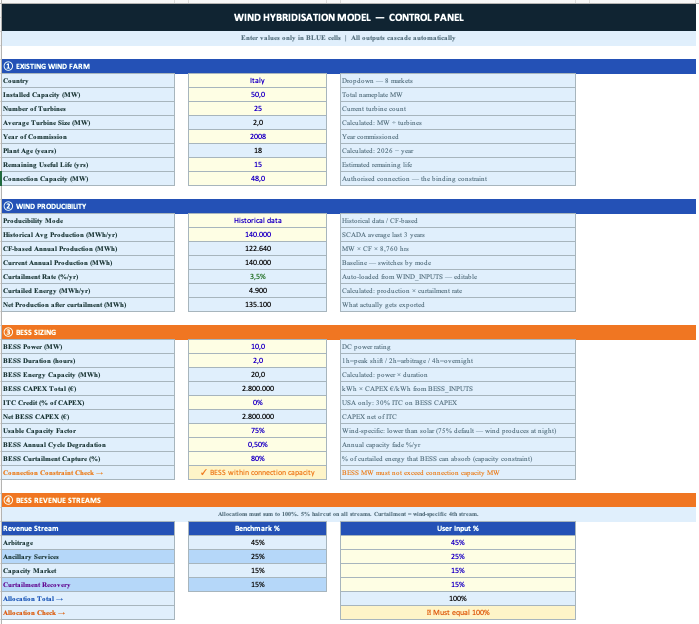

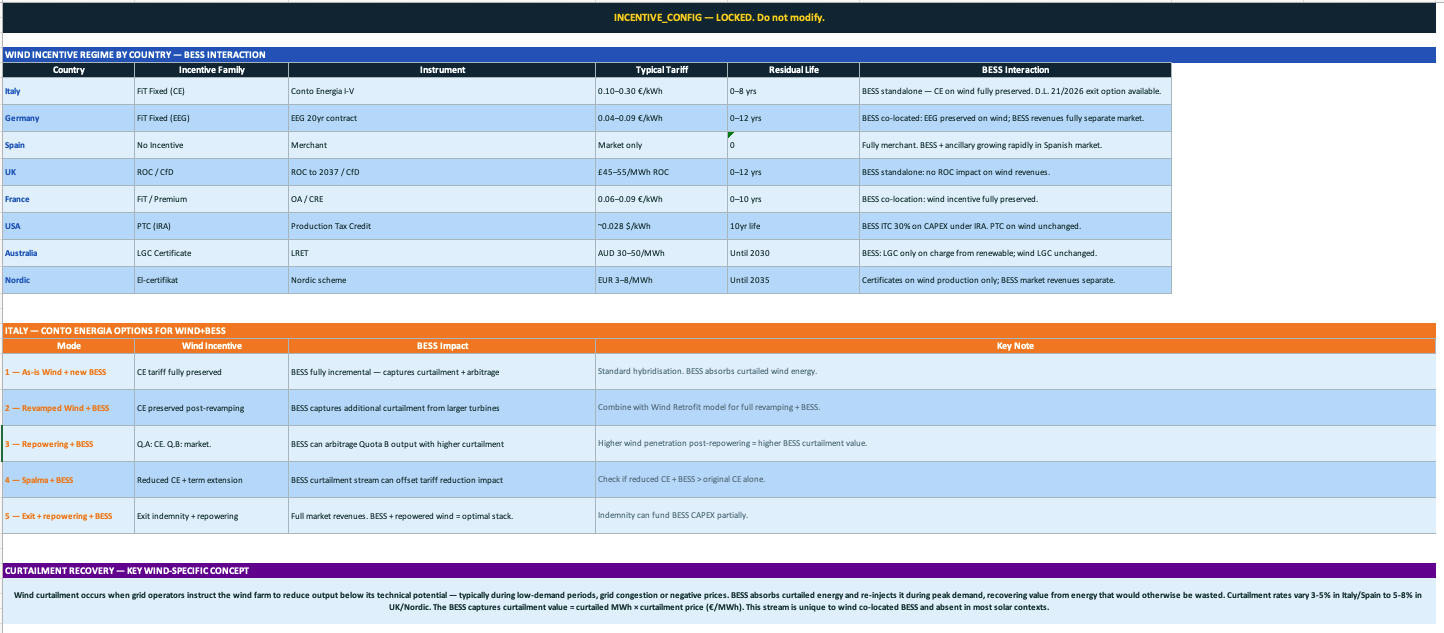

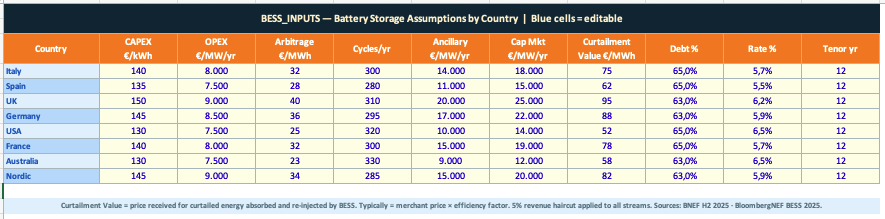

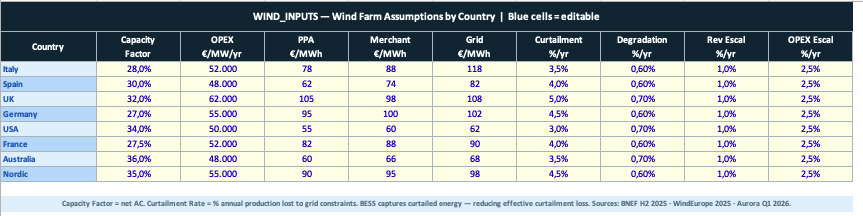

This model enables developers, advisors and asset managers to evaluate the incremental financial value of adding co-located BESS to an existing onshore wind farm across 8 international markets, producing a direct comparison between the wind as-is baseline and the Wind+BESS hybrid scenario. It models curtailment recovery as a fourth BESS revenue stream specific to wind co-location — capturing value from energy curtailed by grid operator instruction — alongside Arbitrage, Ancillary Services and Capacity Market. It applies a wind-specific usable capacity factor reflecting the different dispatch profile of wind versus solar, calculates incremental BESS IRR against the wind baseline rather than against zero, applies country-specific incentive interaction logic including all five Italy D.L. 21/2026 CE options and USA ITC mechanics, and produces a standalone BESS DSCR alongside the combined Wind+BESS project metrics from a full 20-year DCF.

This model is best suited to onshore wind farms of 10 MW and above where curtailment is a quantifiable and recurring source of production loss — typically in congested grid areas in the UK, Germany, Nordic markets or Italian regions with high renewable penetration. It works particularly well for German EEG plants approaching the 20-year contract expiry, where the combination of expiring FiT, growing curtailment and available connection capacity creates a strong case for BESS co-location that this model quantifies directly. It is also well suited to Italian CE plants under D.L. 21/2026 where the mode selection — particularly Modes 3 and 5 — interacts with the BESS sizing and curtailment recovery calculation in ways that need to be modelled explicitly before a regulatory decision is made.

This model covers onshore wind only and is not suited to offshore wind, which has a different curtailment profile, connection structure and regulatory framework. The curtailment recovery stream is modelled using an annual average curtailment rate — for sites where curtailment is highly seasonal or concentrated in specific hours, an hourly dispatch model will produce a more accurate result and the annual derating in this model should be treated as a screening estimate. It does not model grid import charging for the BESS — the battery charges from the wind farm only — and is therefore not appropriate for configurations where grid arbitrage from external charging is a primary revenue source. It should not be used as the sole basis for a final investment decision without a grid curtailment data study, BESS sizing analysis and legal review of the applicable incentive co-location rules in the relevant market.