Originally published: 28/09/2025 20:37

Publication number: ELQ-30577-1

View all versions & Certificate

Publication number: ELQ-30577-1

View all versions & Certificate

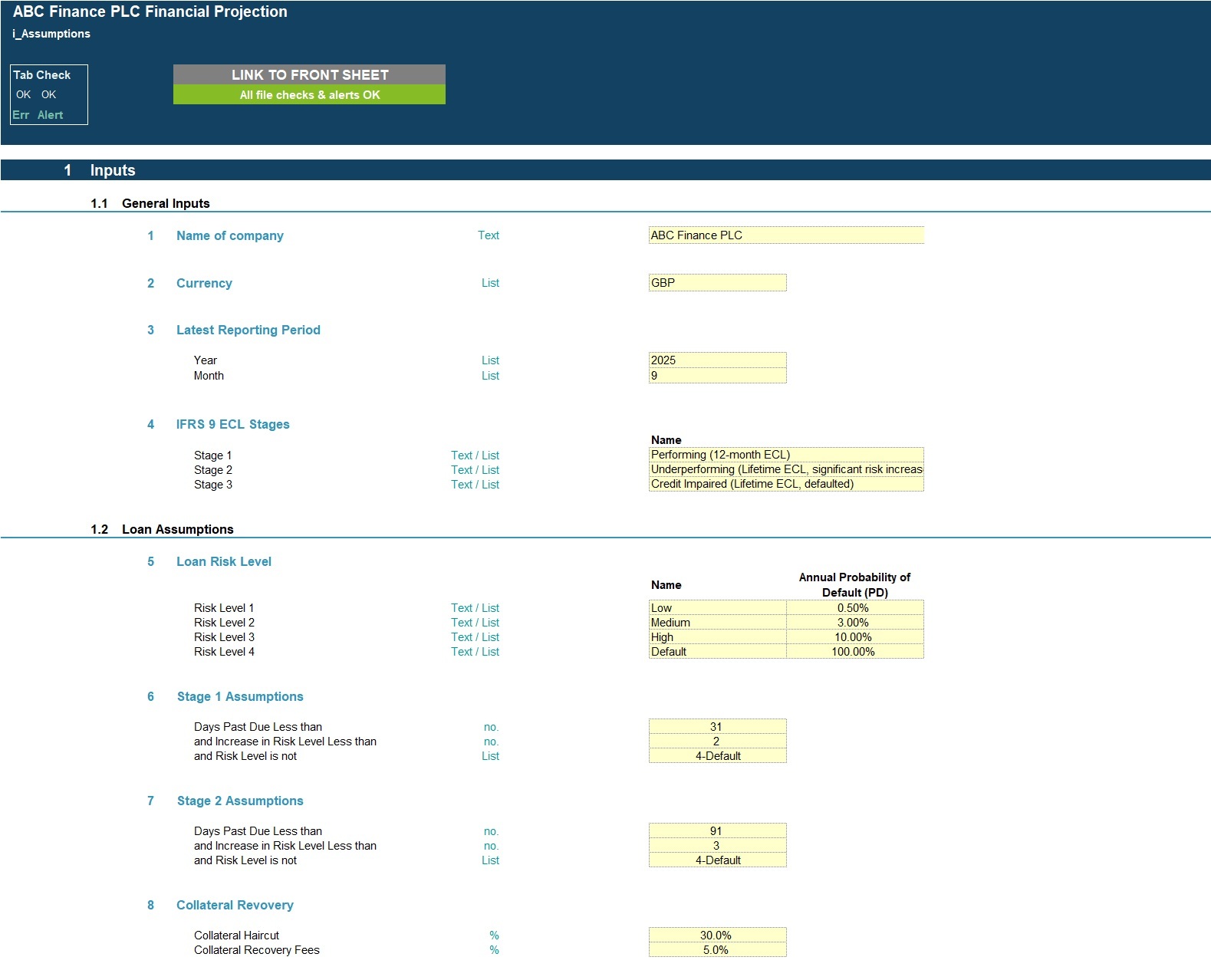

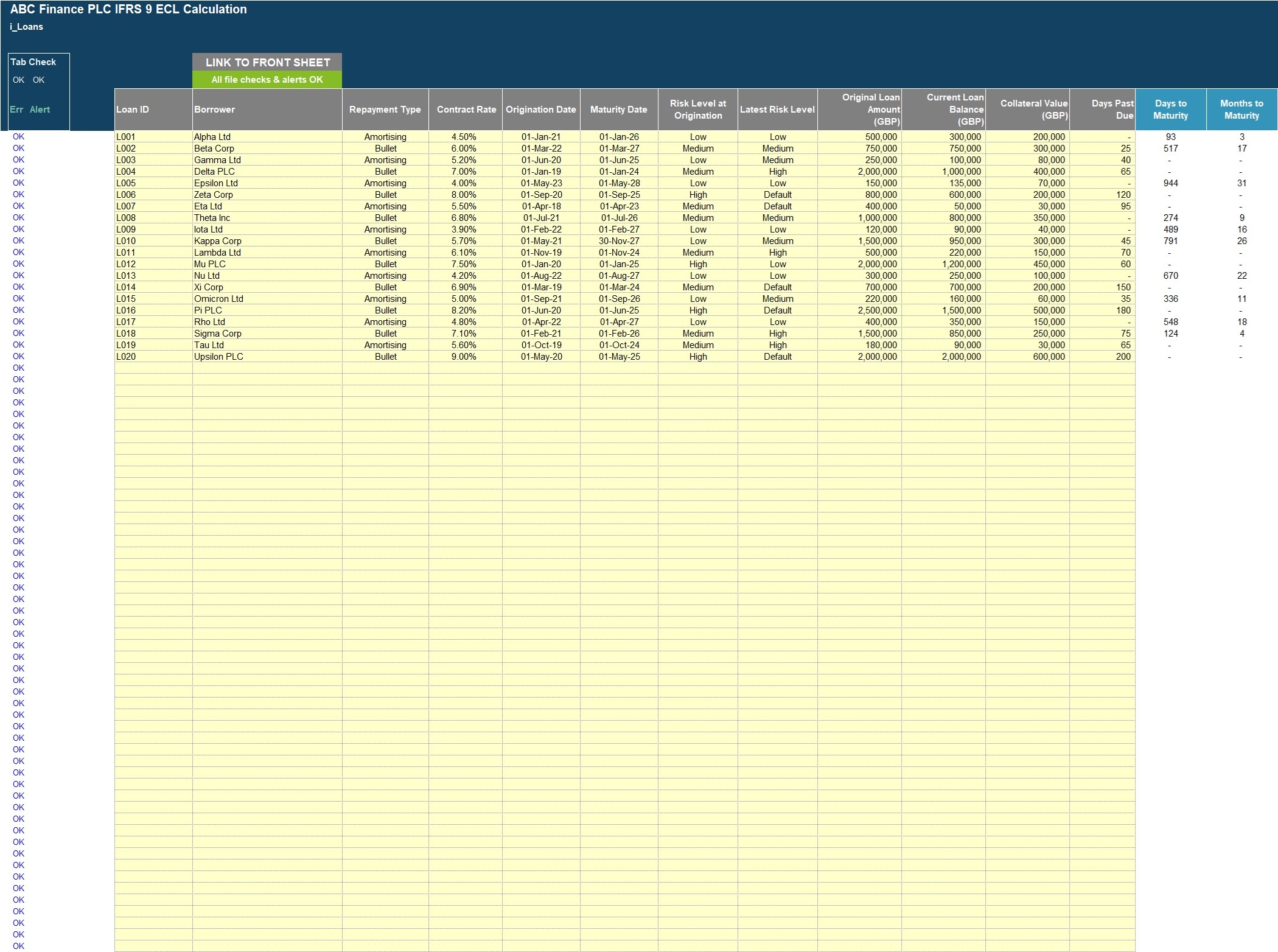

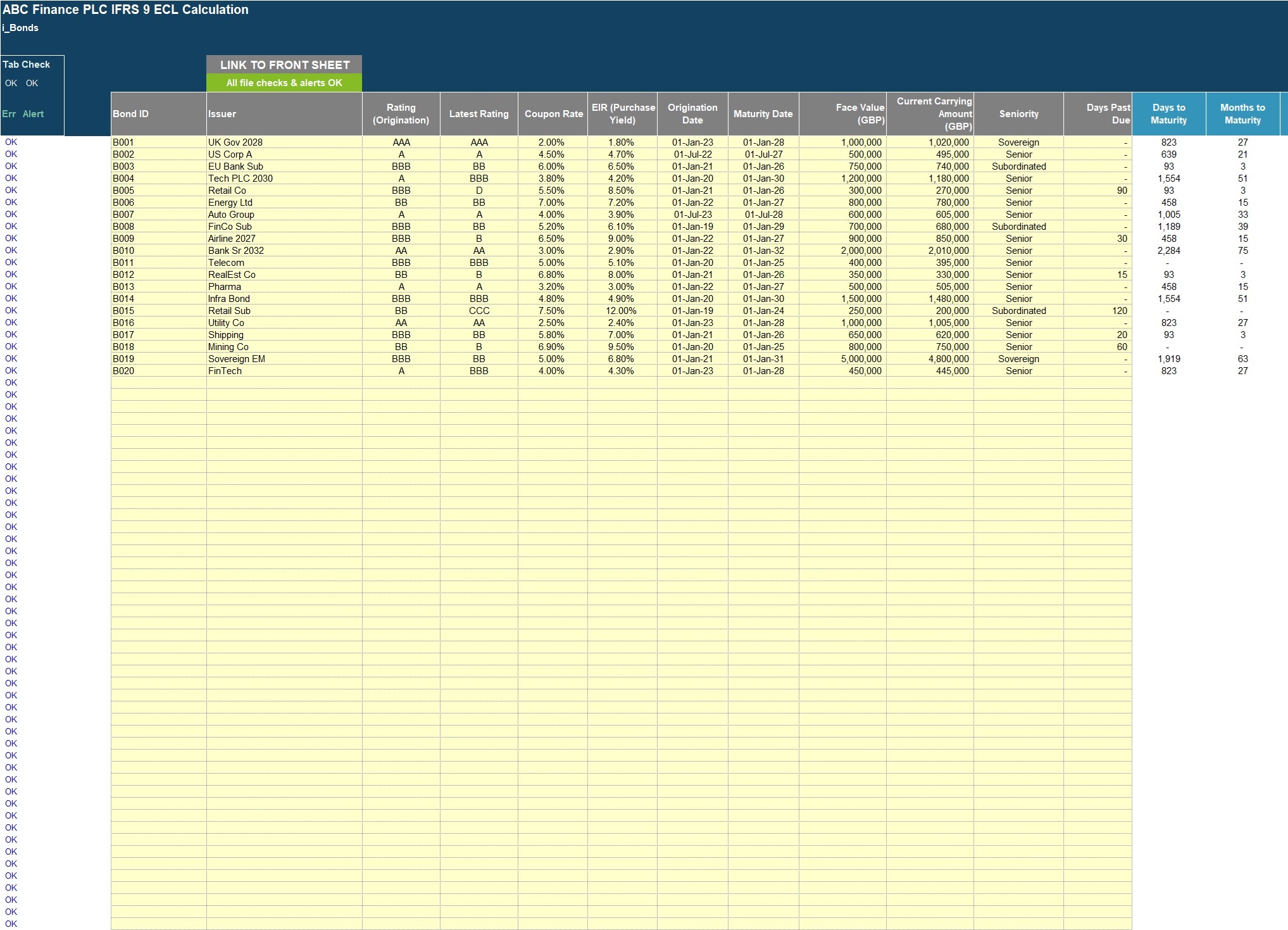

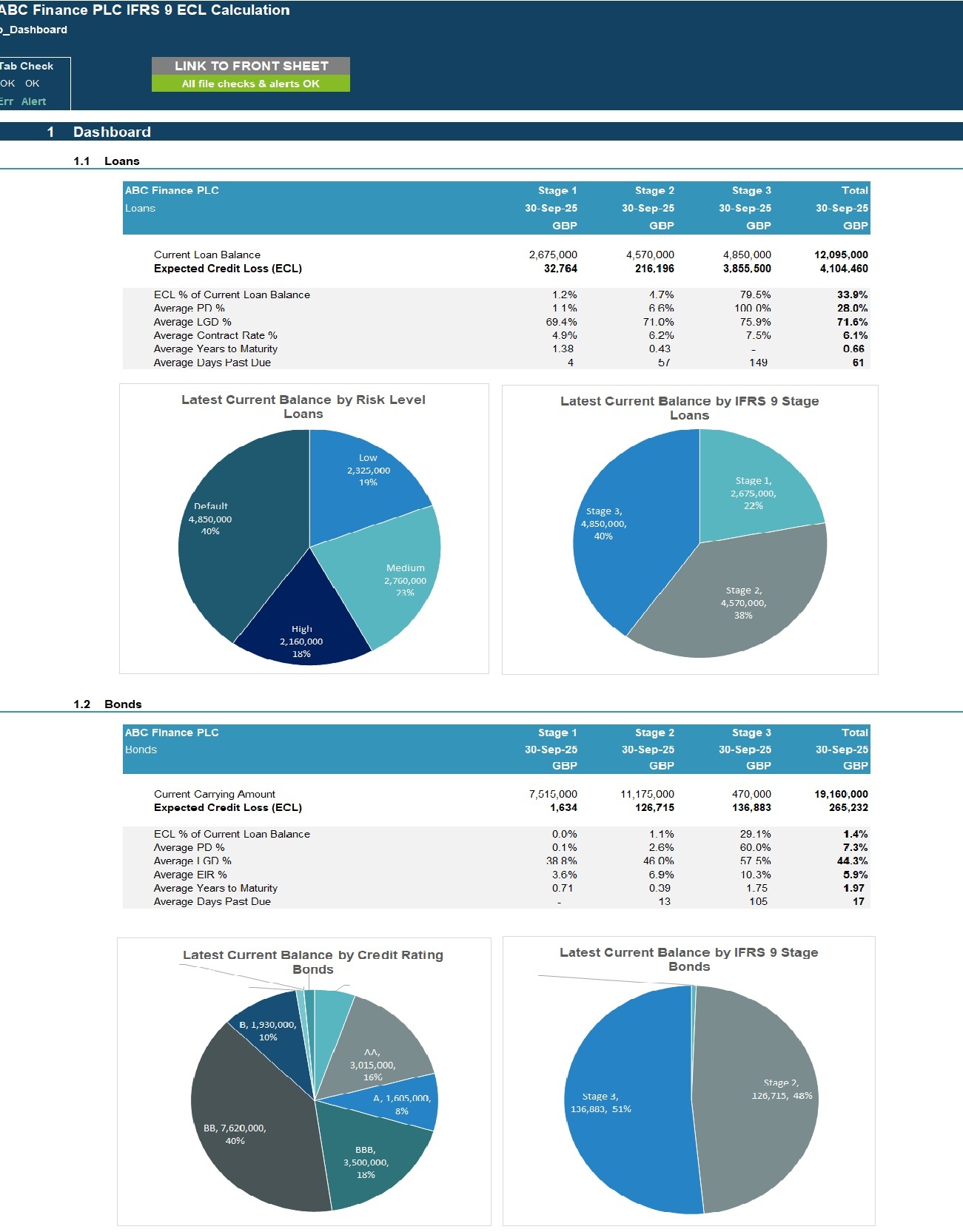

IFRS 9 Expected Credit Loss (ECL) Calculation Model

IFRS 9 Excel template for calculation of ECL for up to 1,000 loans & bonds with user-defined assumptions, automated ECL calculation and dashboard insights.

Further information

- Calculate Expected Credit Losses (ECL) – Apply IFRS 9 methodology using PD, LGD, and EAD to estimate 12-month and lifetime losses across Stages 1–3.

- Ensure Compliance & Transparency – Provide clear, auditable, and consistent calculations with built-in checks, validations, and structured inputs.

- Support Portfolio Monitoring & Reporting – Aggregate results, generate dashboards and summaries to track credit risk and inform management decisions.