Originally published: 01/05/2018 09:15

Last version published: 03/04/2019 13:03

Publication number: ELQ-66154-5

View all versions & Certificate

Last version published: 03/04/2019 13:03

Publication number: ELQ-66154-5

View all versions & Certificate

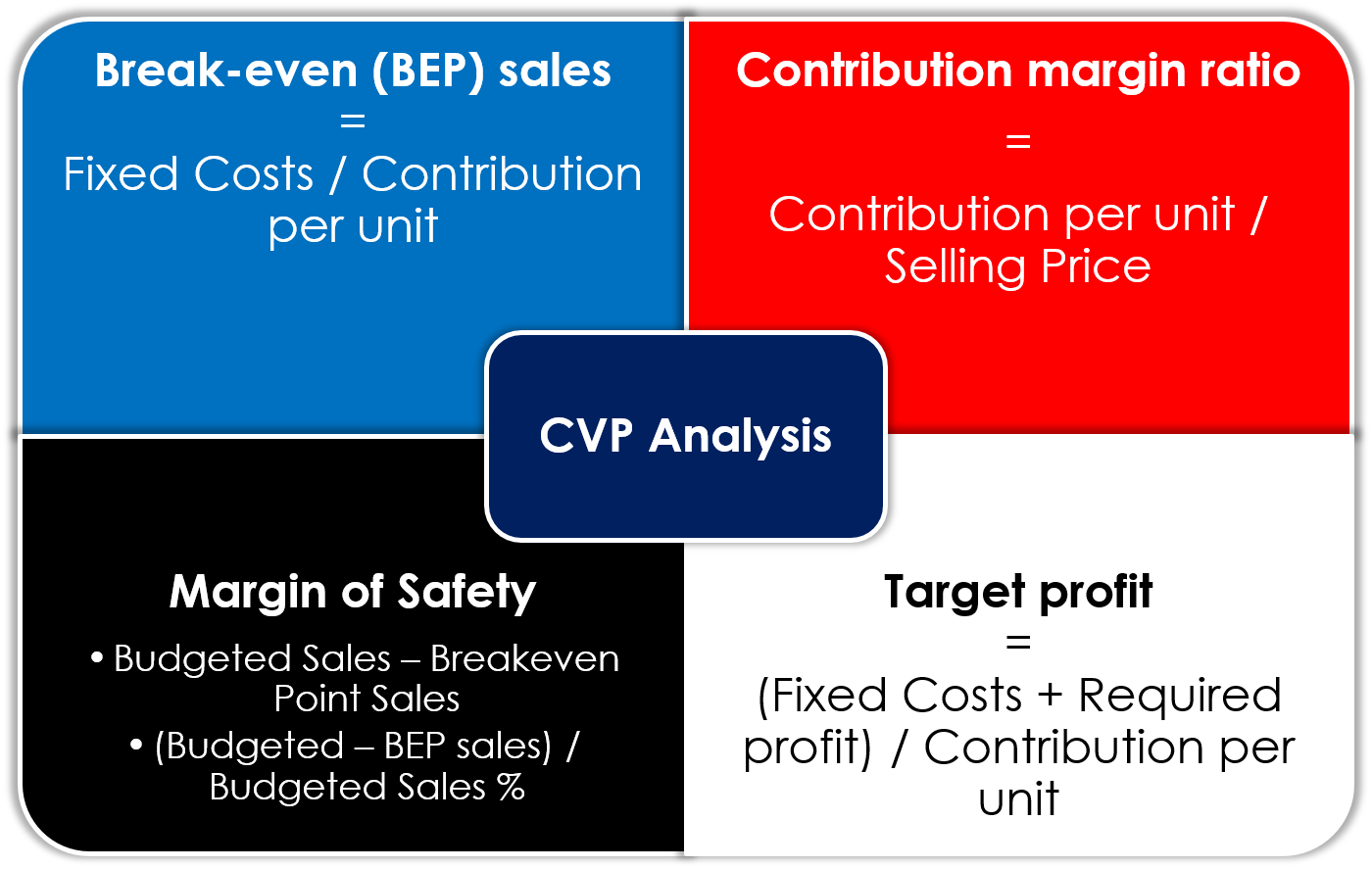

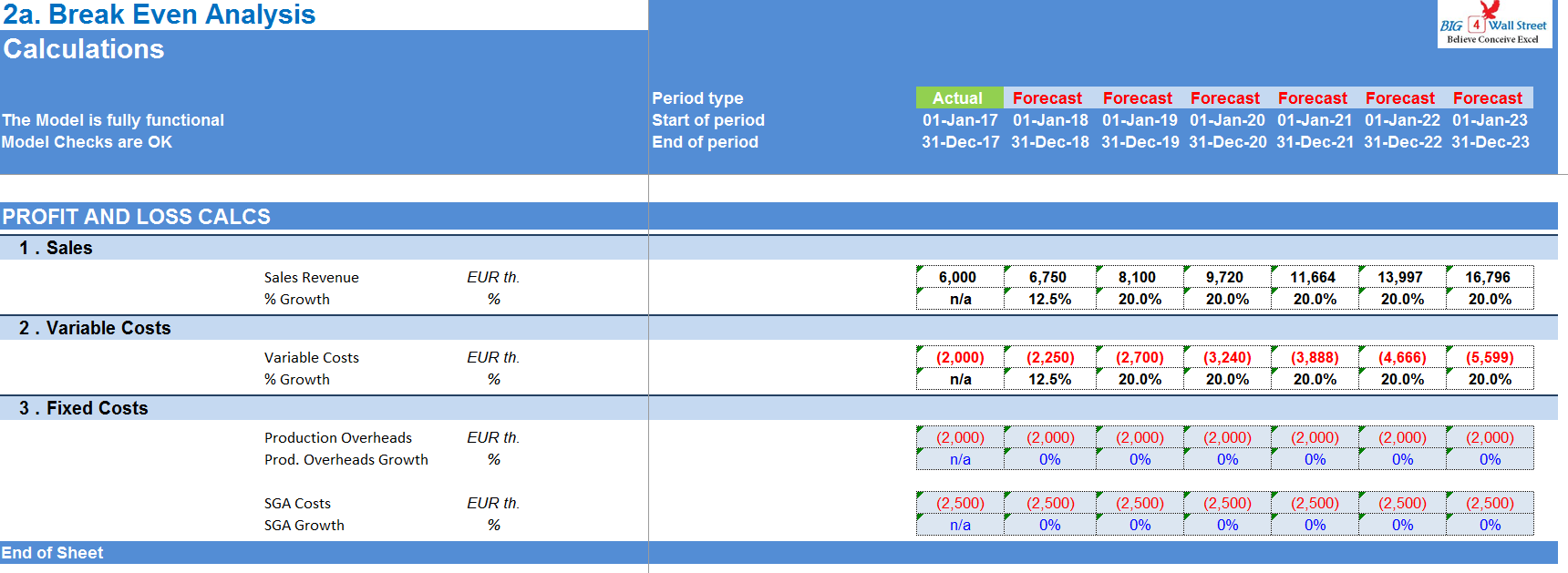

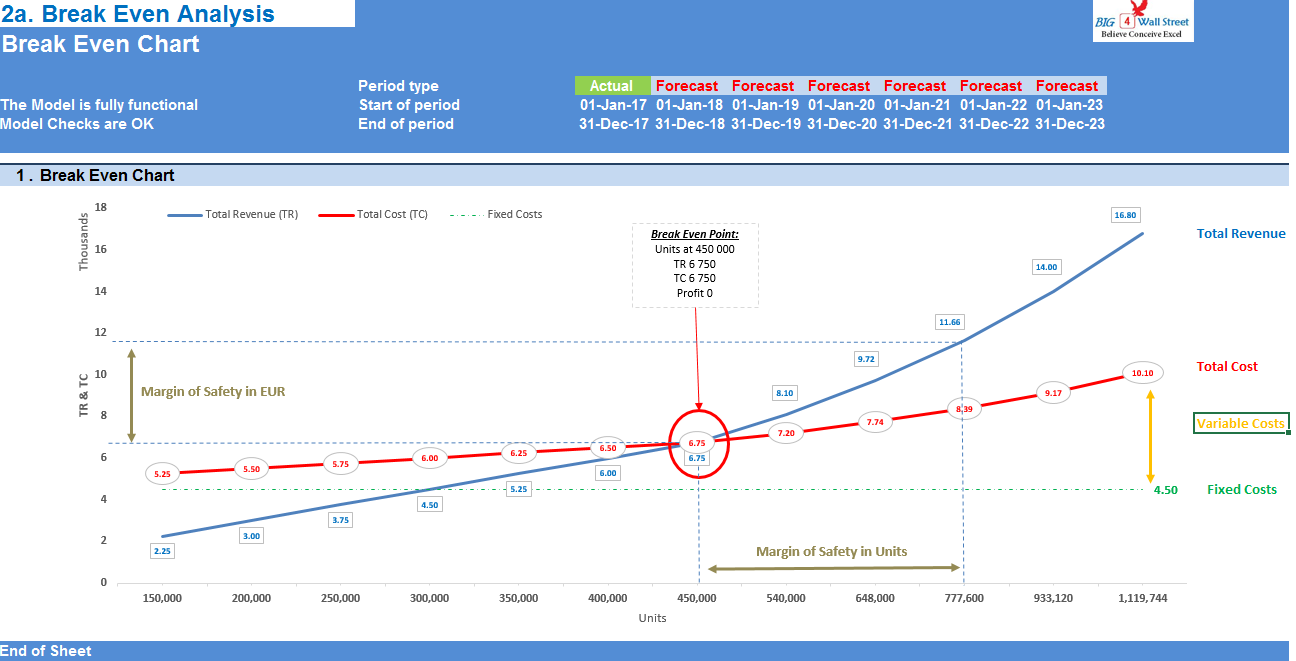

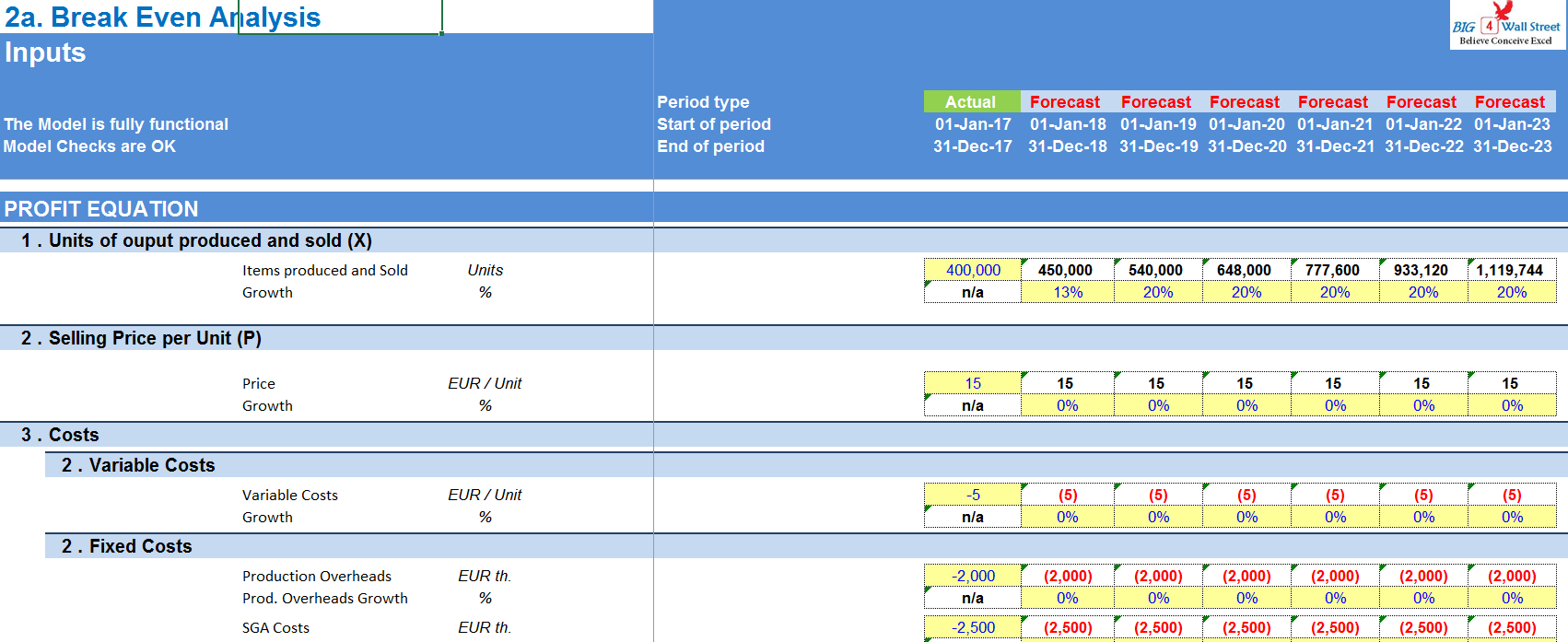

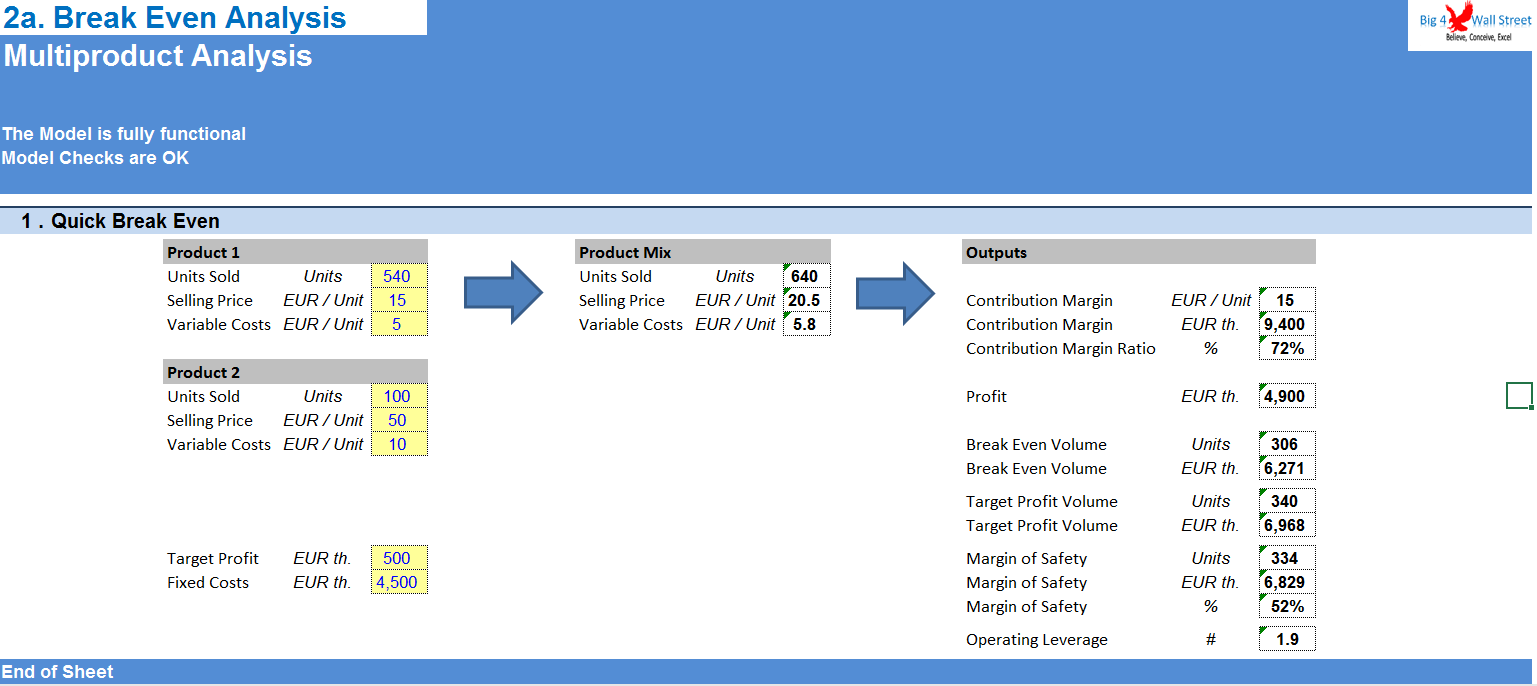

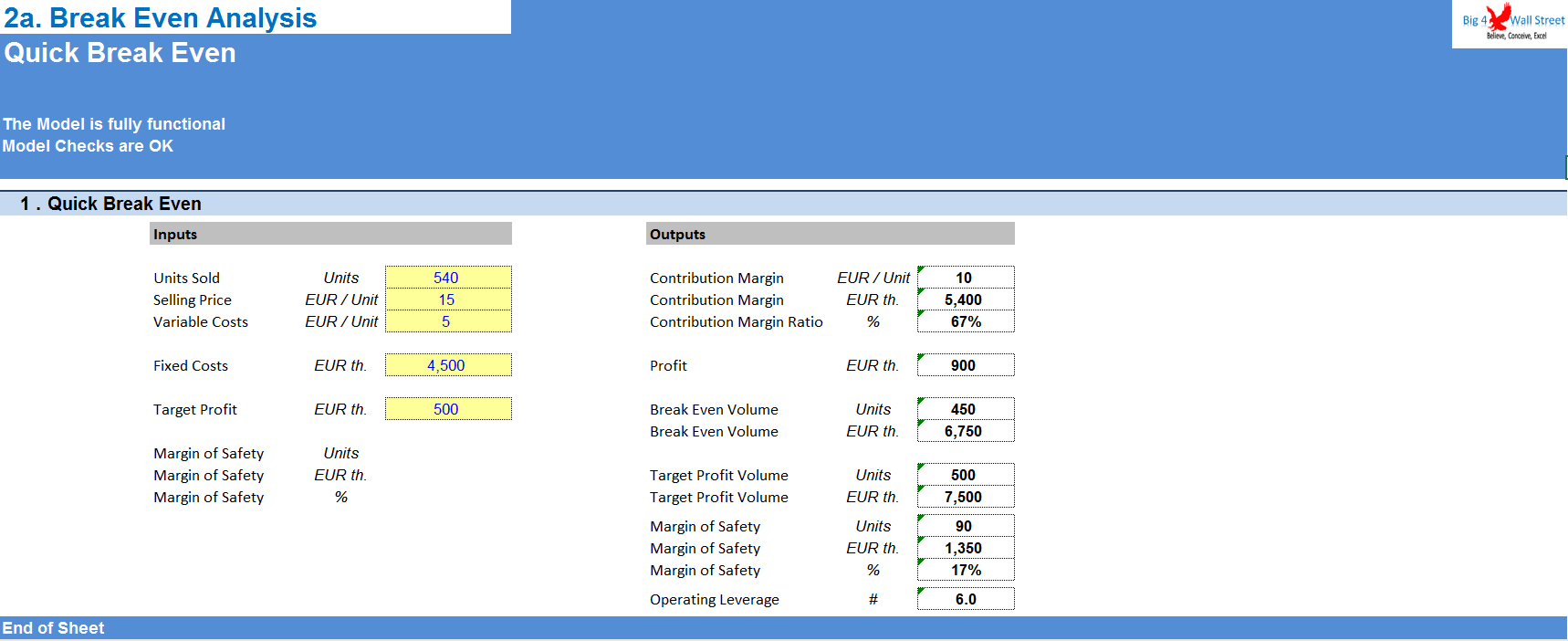

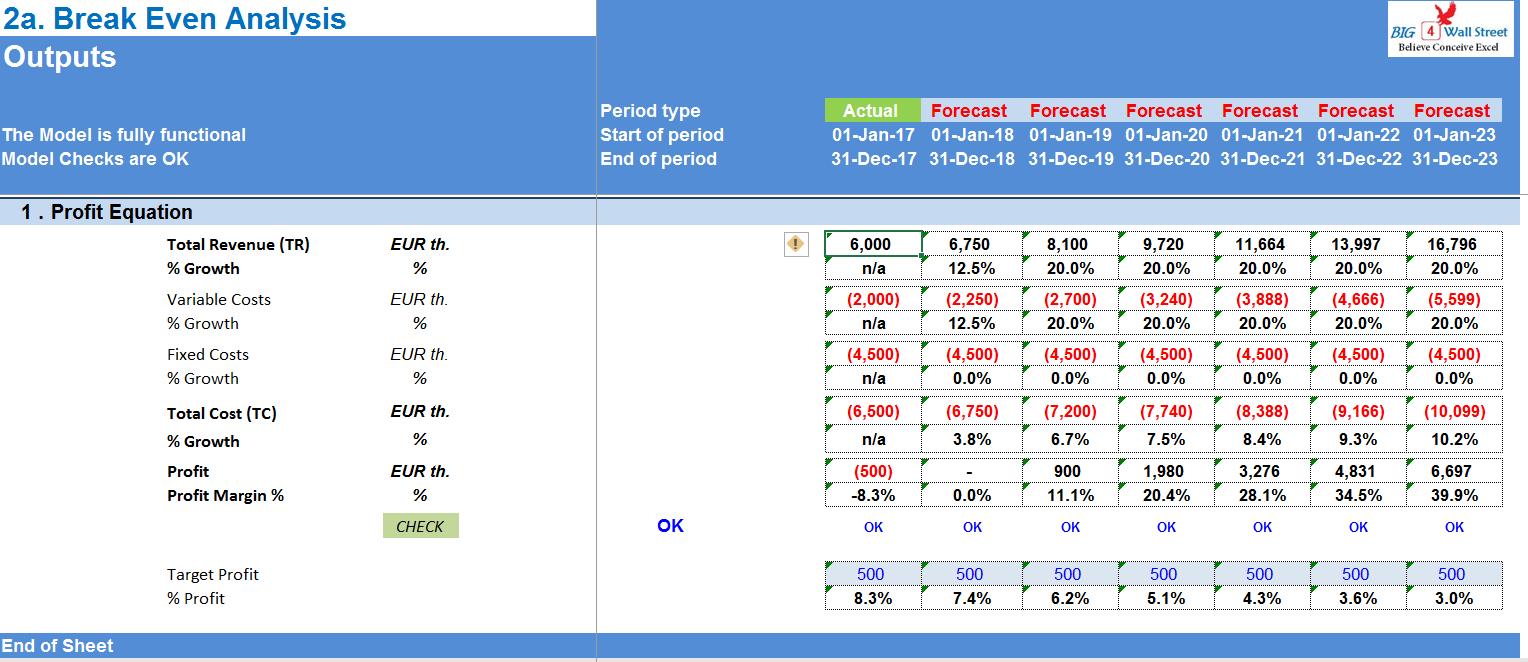

Break Even Analysis / Cost Volume Profit Analysis Excel Model

A full Break-even analysis Excel Model to analyse when your product/service reaches profitability.

Further information

To help the user perform a break even analysis to see the point above which he is able to make a profit.

Simple linear assumptions for costs

Does not apply to economies of scale