Originally published: 15/09/2020 07:01

Last version published: 15/09/2020 08:17

Publication number: ELQ-56635-2

View all versions & Certificate

Last version published: 15/09/2020 08:17

Publication number: ELQ-56635-2

View all versions & Certificate

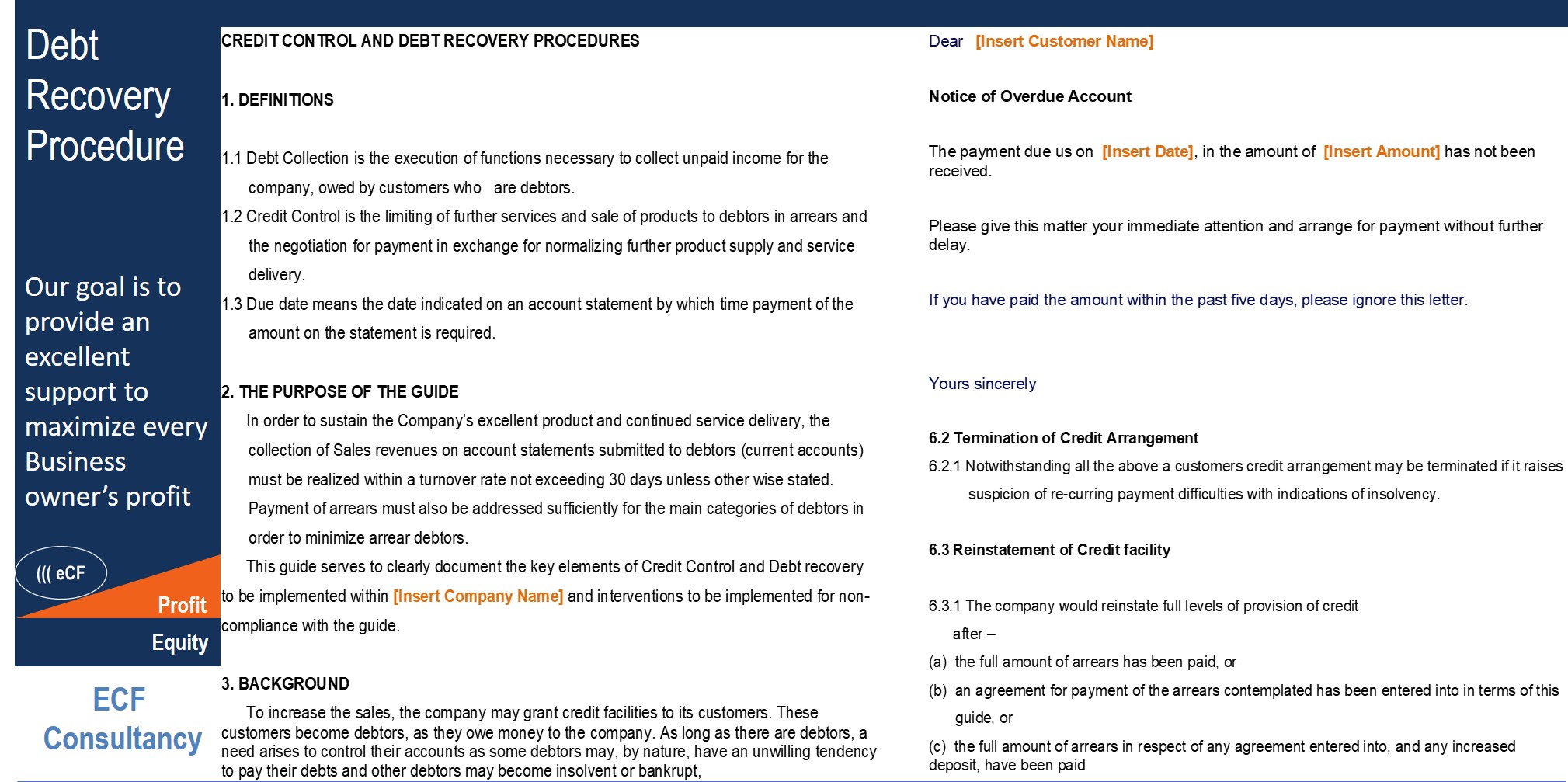

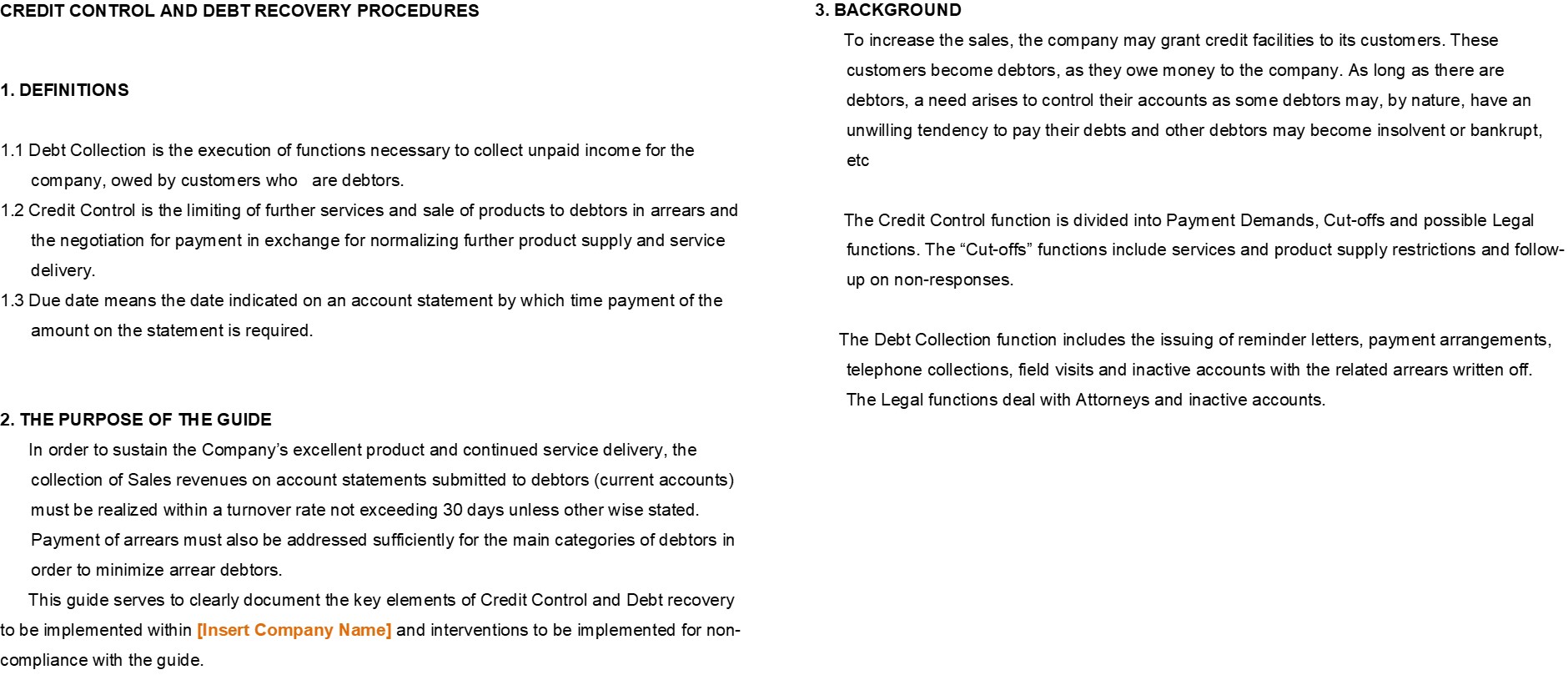

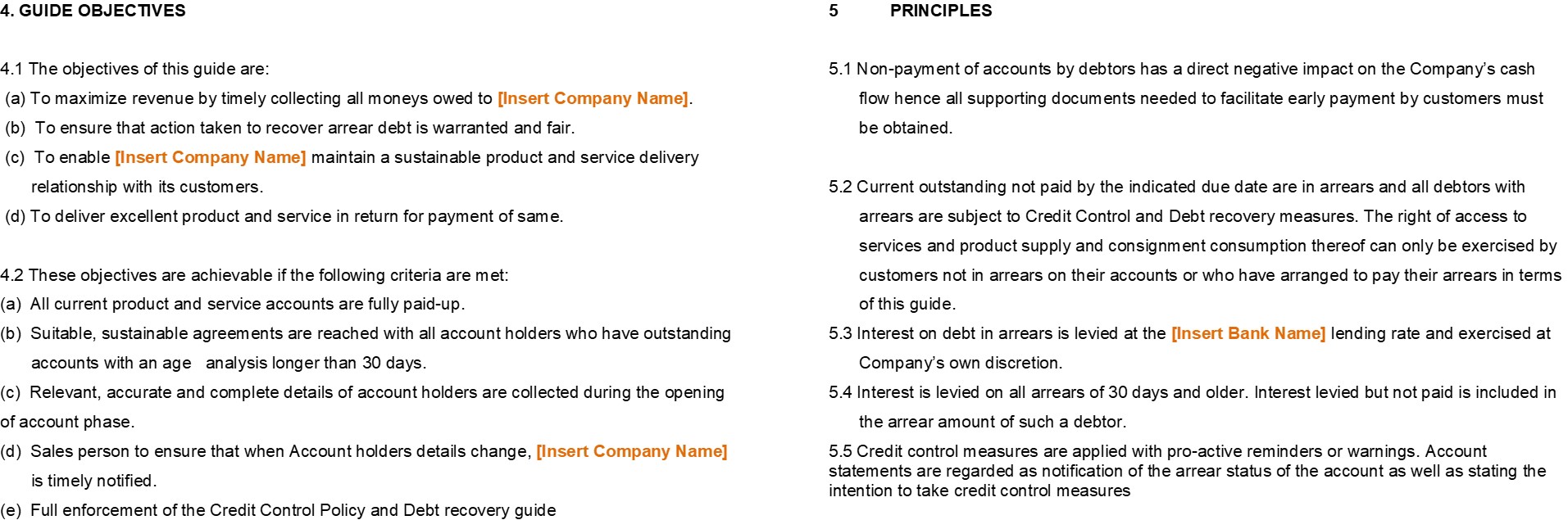

Credit Control & Debt Recovery Procedures

A Word Document outlining Best Practices for Credit Control & Debt Recovery.