Originally published: 14/04/2020 12:50

Last version published: 14/04/2020 12:56

Publication number: ELQ-65950-2

View all versions & Certificate

Last version published: 14/04/2020 12:56

Publication number: ELQ-65950-2

View all versions & Certificate

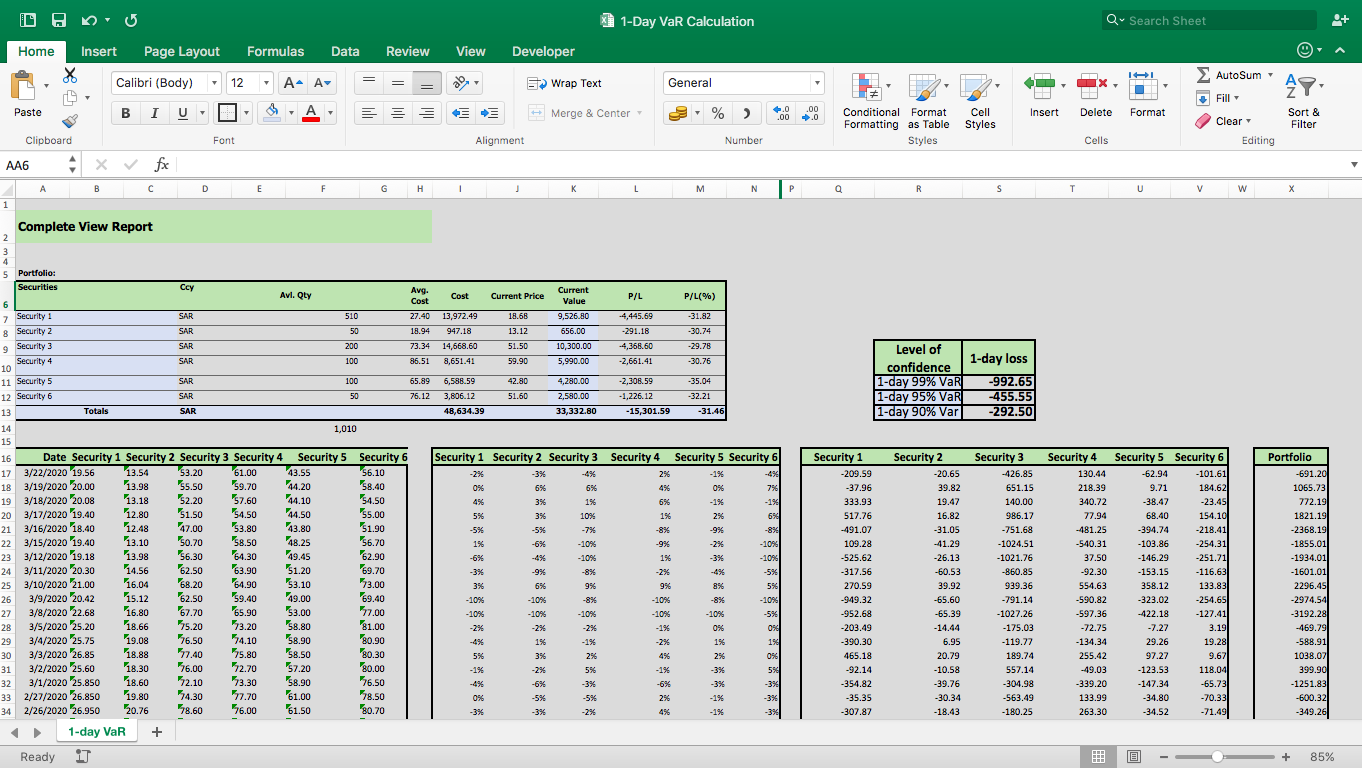

1-Day VaR - Value at Risk Calculation

1-Day VaR Calculation using Historical Method - in Microsoft Excel.