Originally published: 29/04/2024 06:41

Publication number: ELQ-77692-1

View all versions & Certificate

Publication number: ELQ-77692-1

View all versions & Certificate

Zenith Bank of Nigeria business valuation using DCF approach

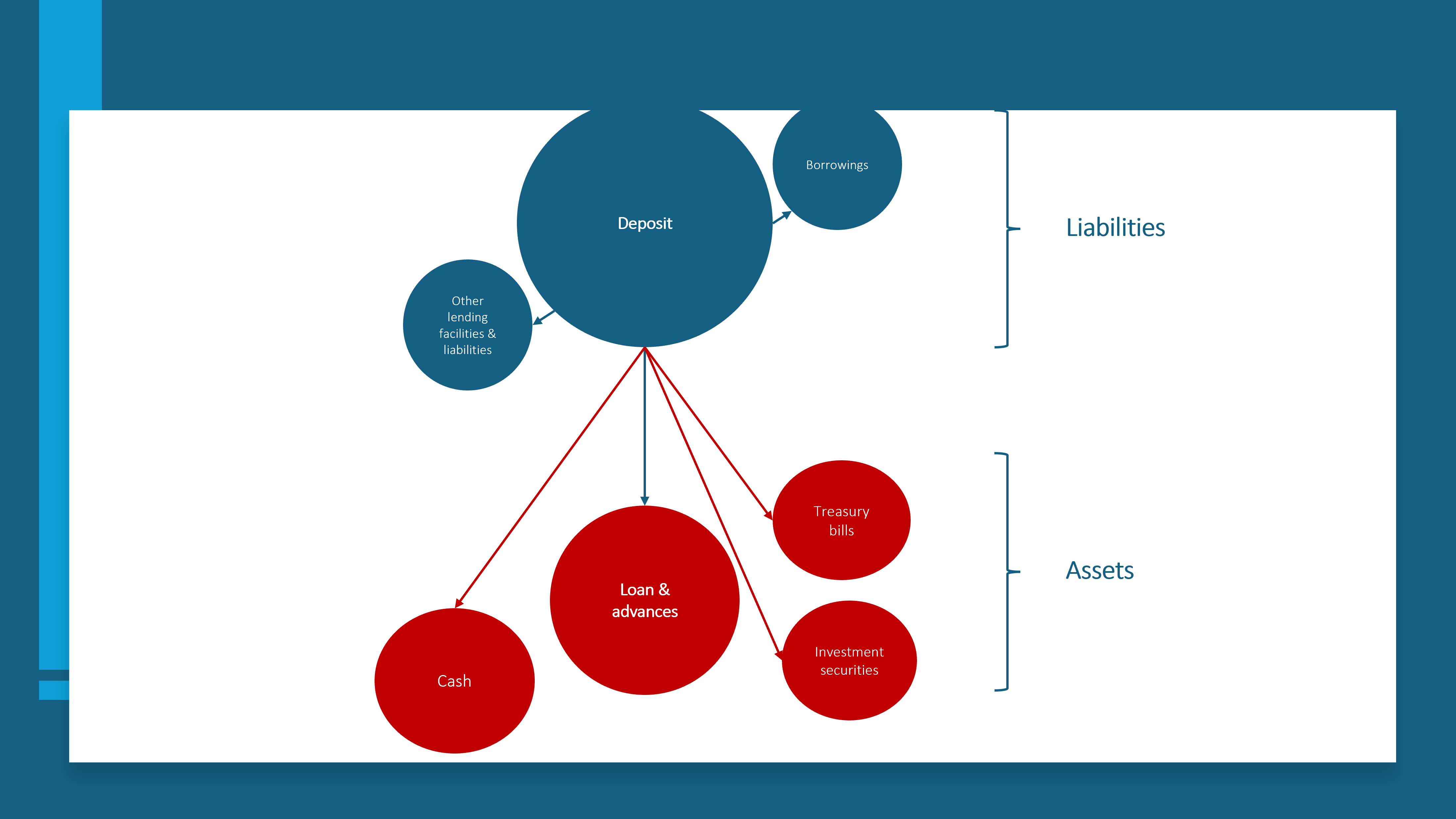

Bank's business valuation operational flow, forecasting and business valuation review using the DCF approach

Financial Modeler & Analyst | Project & Infrastructure Modeler | MVP | Corporate TrainerFollow 28

Description

Business valuation for banks is a critical process that involves determining the financial worth of a bank entity. Given the unique nature of banking operations, several key factors come into play when valuing a bank.

Business valuation for banks is a critical process that involves determining the financial worth of a bank entity. Given the unique nature of banking operations, several key factors come into play when valuing a bank.

- Financial Performance: Assessing a bank's financial health is fundamental. Metrics such as net income, return on assets (ROA), return on equity (ROE), and efficiency ratio are scrutinized to gauge profitability and operational efficiency.

- Asset Quality: The quality of a bank's assets, including loans and investments, is crucial. Evaluating asset quality involves analyzing loan portfolios, non-performing assets (NPAs), and risk management practices to ascertain the bank's ability to generate sustainable income.

- Capital Adequacy: Banks must maintain adequate capital to absorb potential losses and support growth. Regulatory capital ratios, such as the Tier 1 capital ratio and the Common Equity Tier 1 (CET1) ratio, are assessed to ensure compliance with regulatory requirements and to gauge the bank's capacity to withstand adverse economic conditions.

- Market Position and Competitive Advantage: Understanding a bank's market position and competitive advantages is essential. Factors such as market share, brand strength, customer base, and geographic reach contribute to assessing the bank's competitive positioning and growth prospects.

- Regulatory Environment: Banks operate within a highly regulated environment. Evaluating compliance with regulatory requirements and assessing the potential impact of regulatory changes on the bank's operations and profitability are integral parts of the valuation process.

- Economic Outlook: The macroeconomic environment significantly influences a bank's performance and valuation. Factors such as interest rates, inflation, economic growth, and regulatory policies shape the operating environment and impact the bank's financial performance and future prospects.

- Risk Management Practices: Effective risk management is essential for maintaining financial stability and mitigating potential risks. Evaluating risk management practices, including credit risk, liquidity risk, and operational risk management, provides insights into the bank's ability to navigate challenging market conditions.

- Future Growth Prospects: Assessing the bank's growth potential is critical for determining its intrinsic value. Factors such as expansion opportunities, innovation initiatives, and strategic partnerships contribute to evaluating the bank's future earnings potential and long-term value creation.

This Best Practice includes

Excel Document