Publication number: ELQ-73665-1

View all versions & Certificate

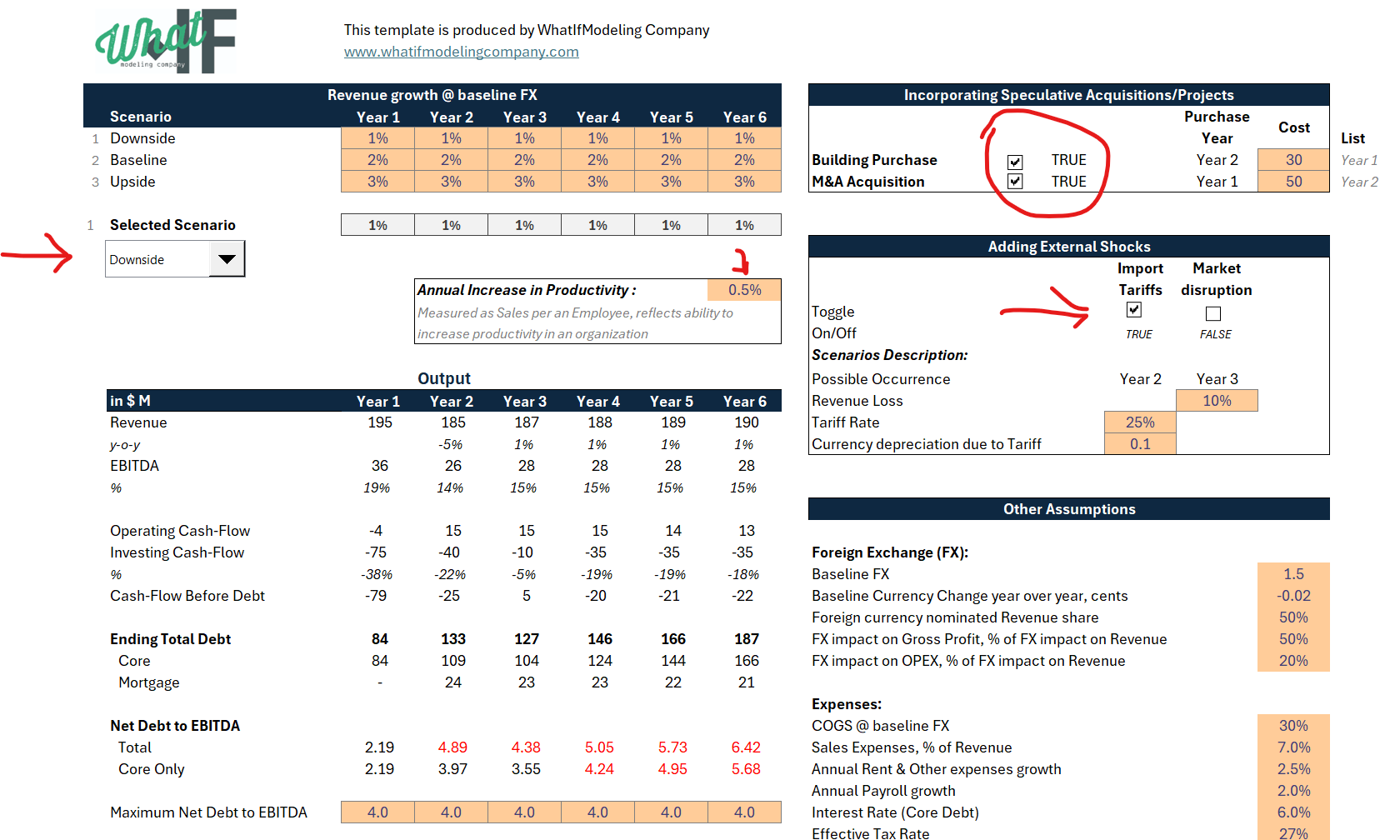

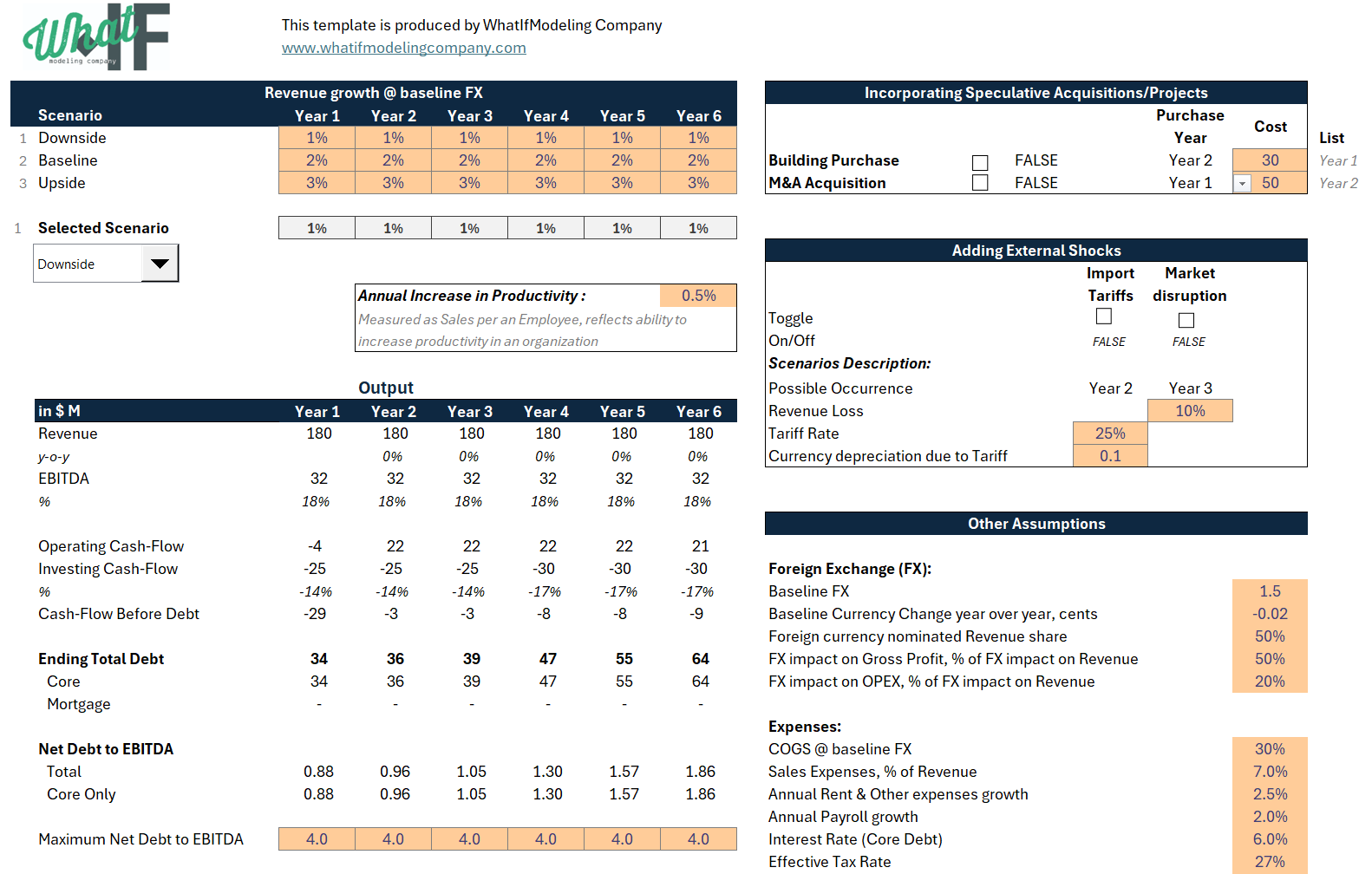

Export Tariff, FX-impact & Strategic Investment (Real Estate + M&A) Model of a hypothetical exporting company

A multi-scenario model of an exporter that captures the impact of import tariff, FX, and strategic investment decisions (M&A + real estate) on debt covenants.

Further information

To demonstrate how to build a scenario-driven financial model for an exporting company operating under uncertainty

To illustrate the impact of import tariffs, FX movements, and market disruptions on revenue, EBITDA, and capital structure

To show how to integrate macroeconomic scenarios into a coherent, toggle-driven modelling approach

To highlight best practices in modelling FX sensitivity and its interaction with external shocks

To incorporate operational drivers such as productivity, headcount planning, and restructuring costs

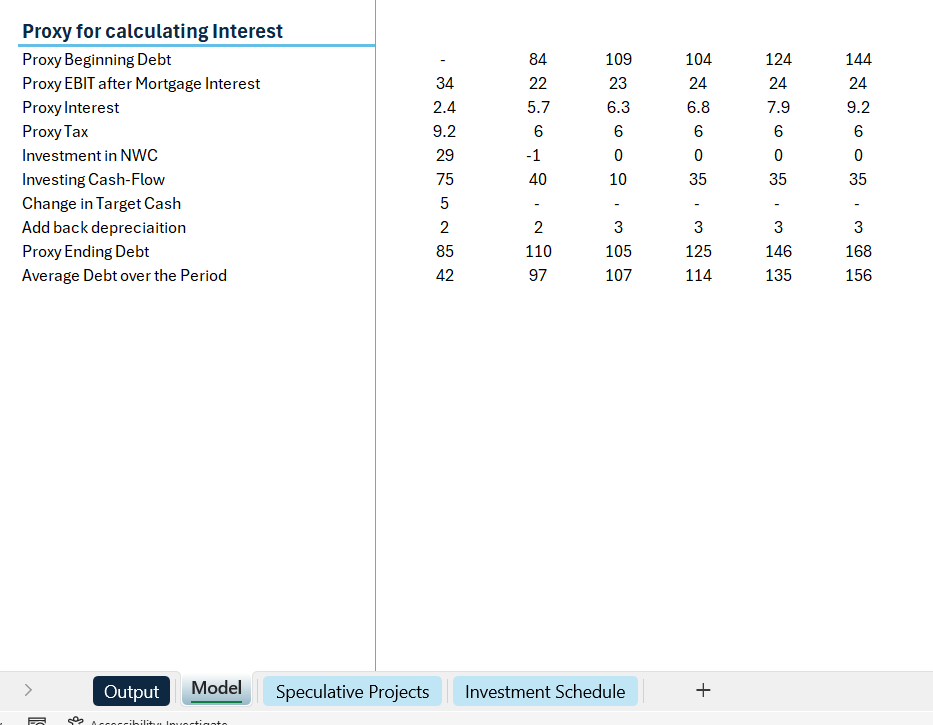

To present an approach to modelling interest expense that avoids circularity while maintaining accuracy

Companies with meaningful export exposure and sensitivity to FX movements

Businesses operating under macroeconomic uncertainty, including potential import tariffs or demand disruptions

Situations requiring evaluation of alternative strategic investments (e.g., M&A vs. organic expansion or real estate acquisition)

Companies with active debt facilities where covenant compliance (e.g., Net Debt / EBITDA) is a key consideration

Teams looking to integrate operational drivers (e.g., productivity, headcount) into financial forecasting

Use cases where a forward-looking, flexible modelling framework is preferred over static budgeting approaches

Situations requiring a fully detailed financial model with full three-statement outputs (Income Statement, Balance Sheet, and Cash Flow)

Use cases where high granularity and accounting precision are required