Originally published: 11/07/2019 08:55

Last version published: 12/09/2019 13:10

Publication number: ELQ-31542-6

View all versions & Certificate

Last version published: 12/09/2019 13:10

Publication number: ELQ-31542-6

View all versions & Certificate

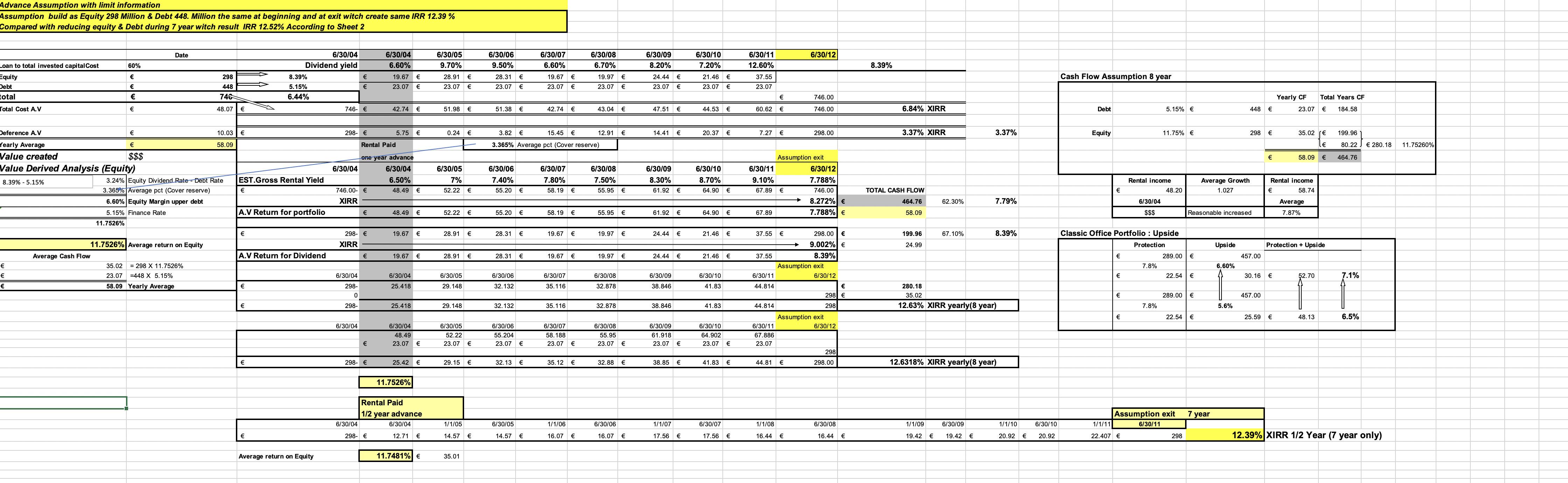

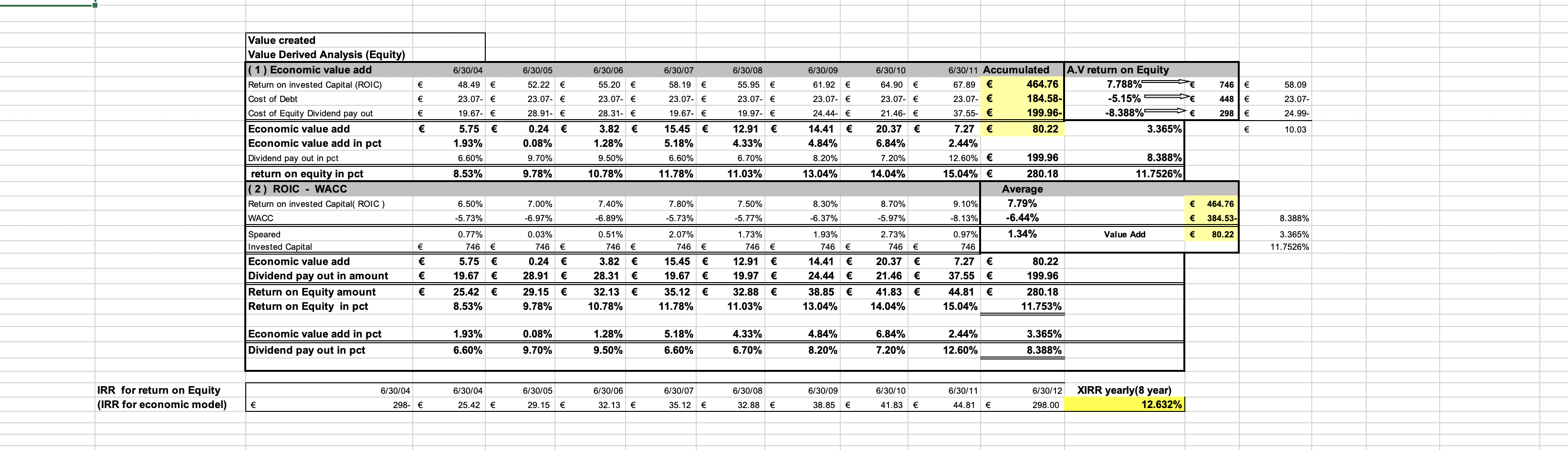

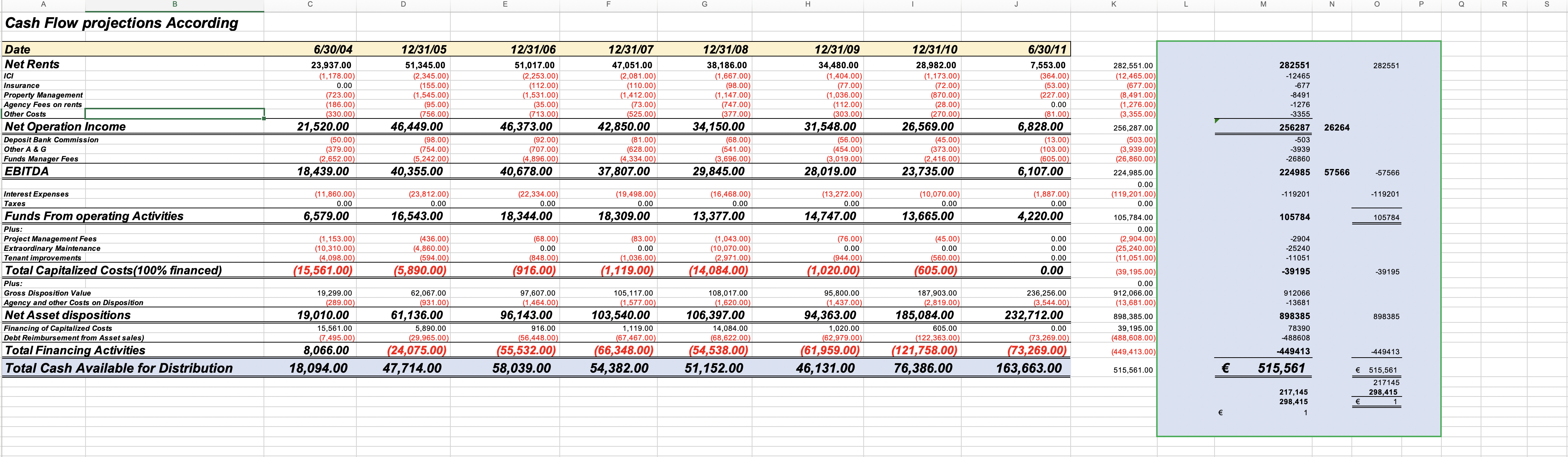

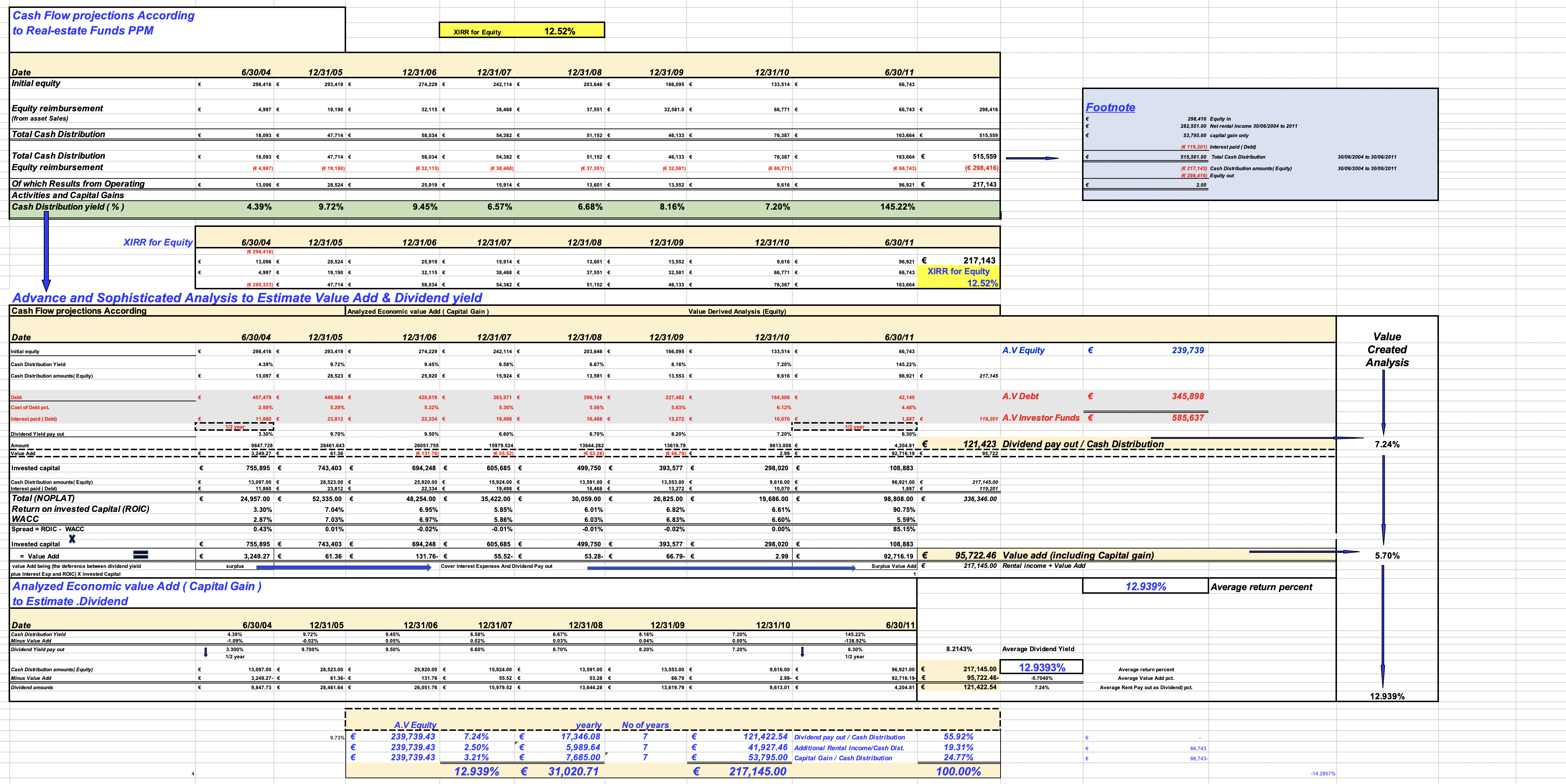

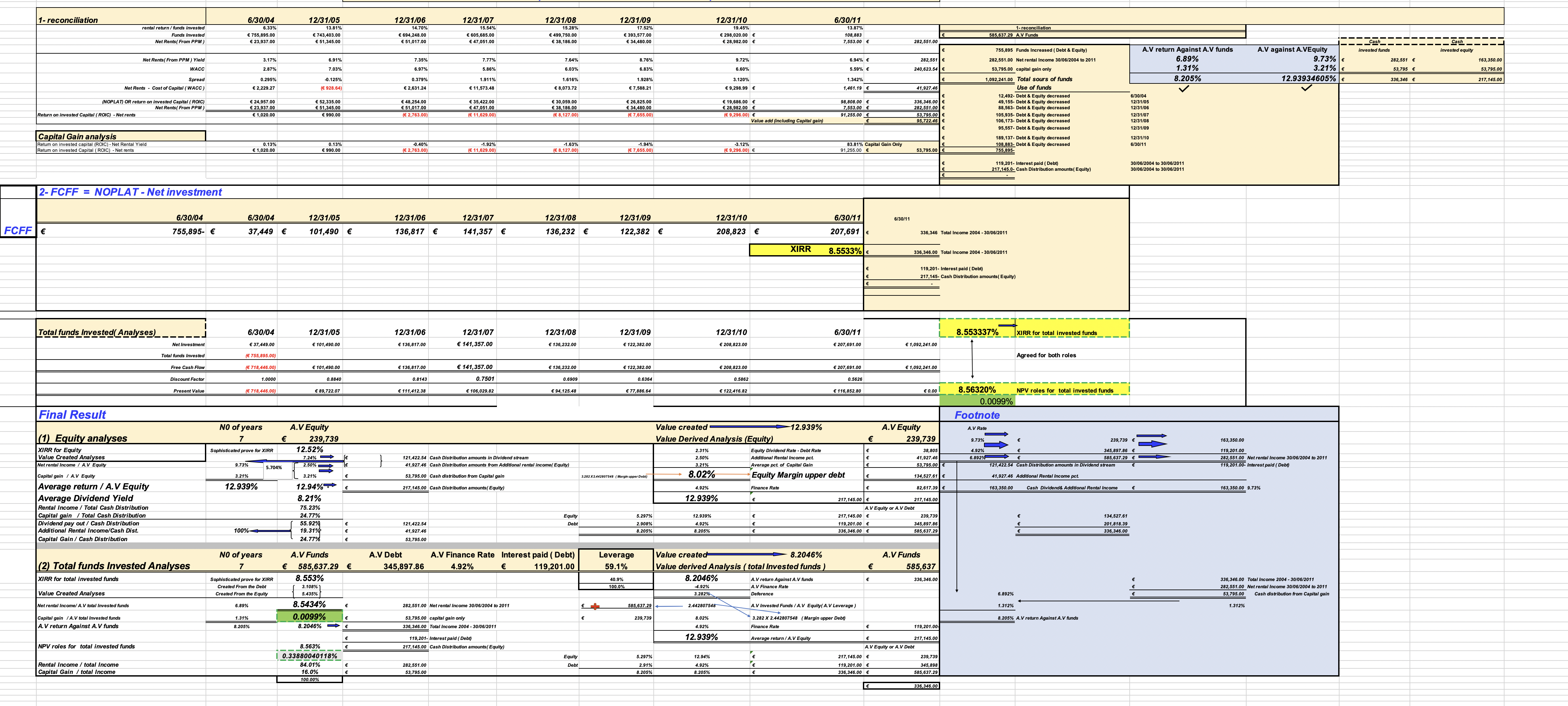

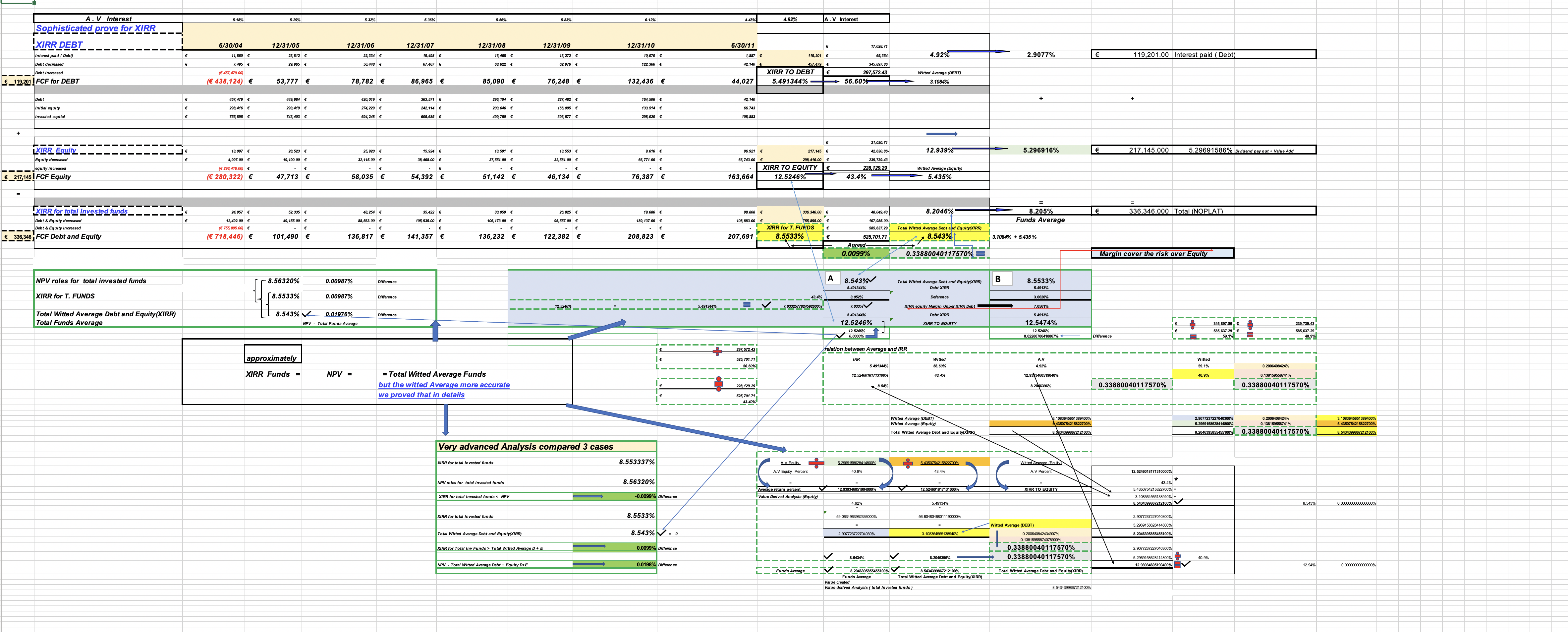

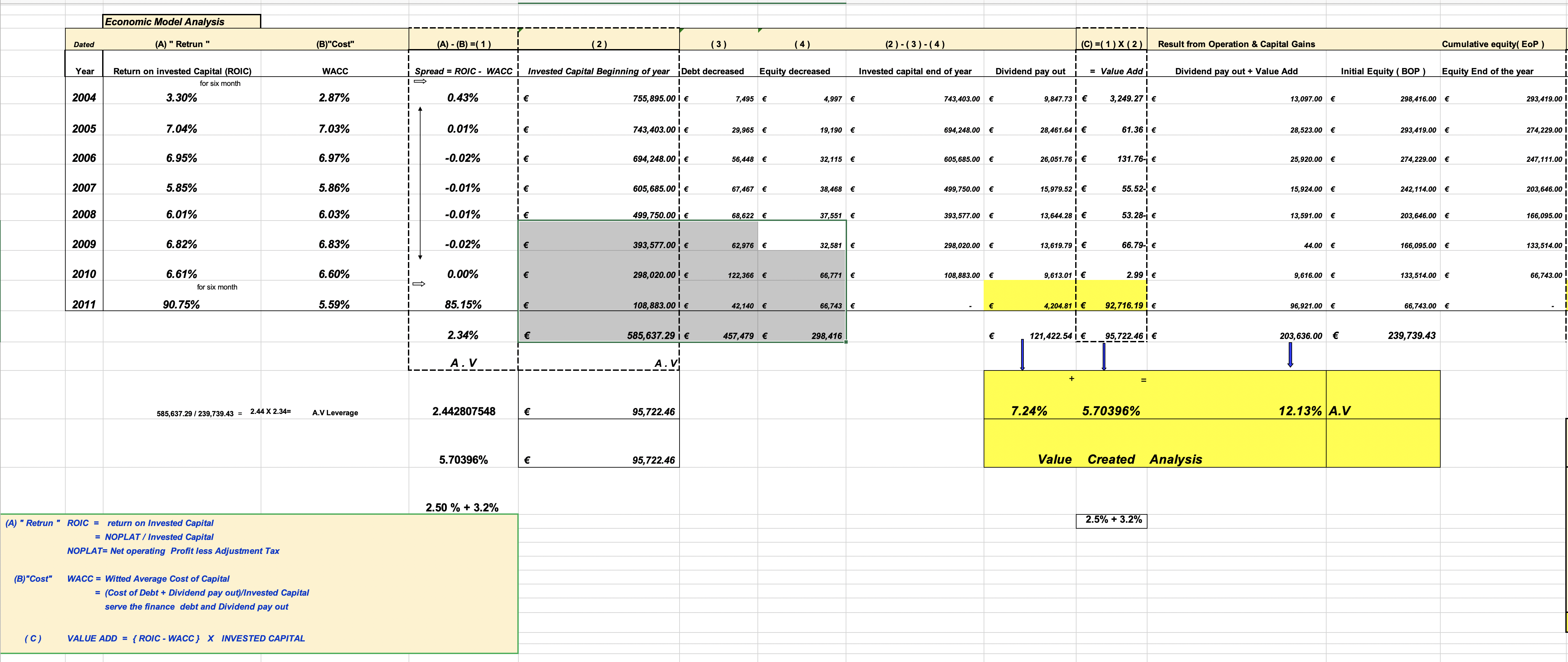

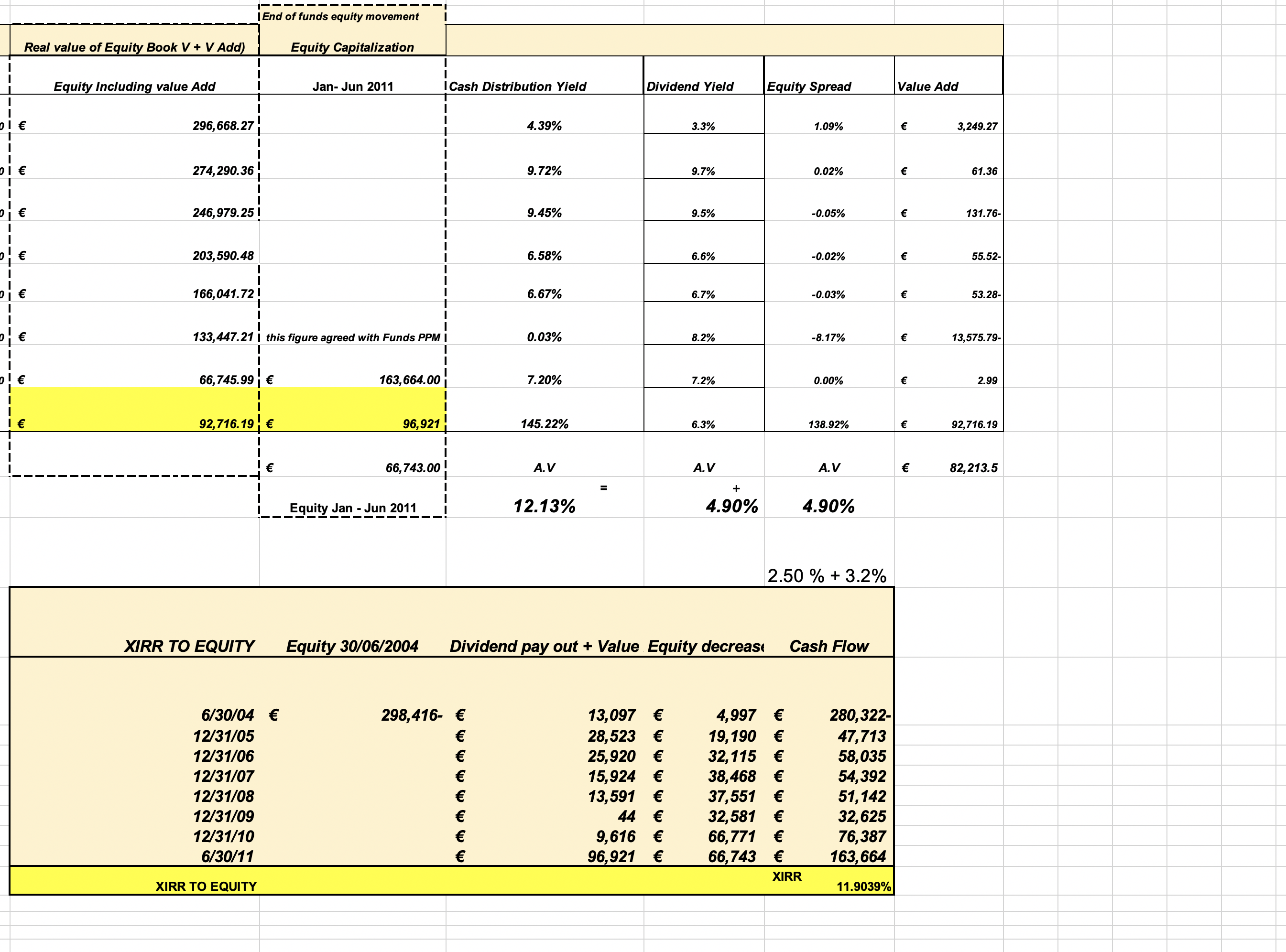

Real Estate funds Model

The new technique to evaluate Real Estate funds ( discount cash flow & economic value add )

Professional banker specializing in treasury and investment, valuation and corporate financeFollow 15