Originally published: 05/06/2018 15:24

Last version published: 22/08/2018 16:54

Publication number: ELQ-31439-3

View all versions & Certificate

Last version published: 22/08/2018 16:54

Publication number: ELQ-31439-3

View all versions & Certificate

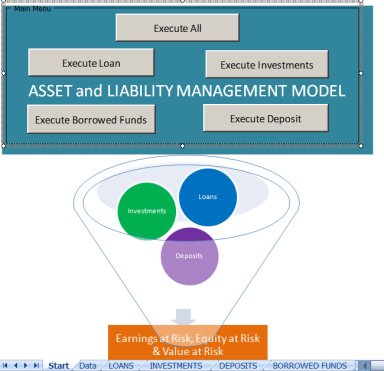

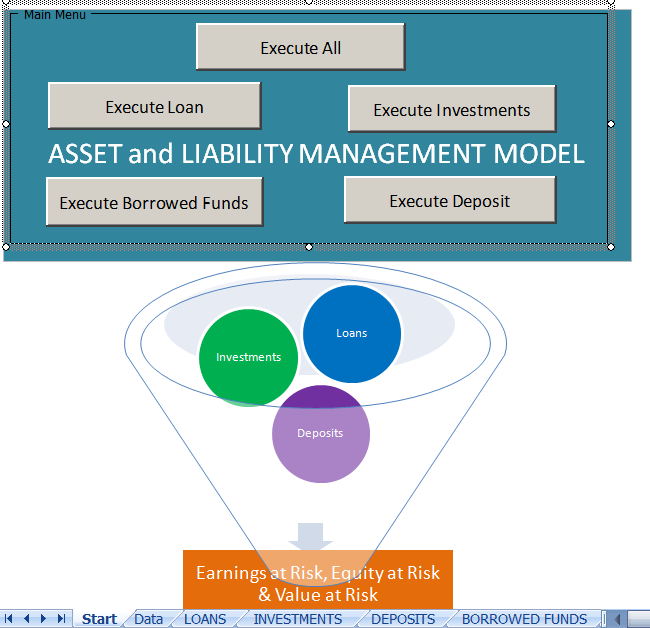

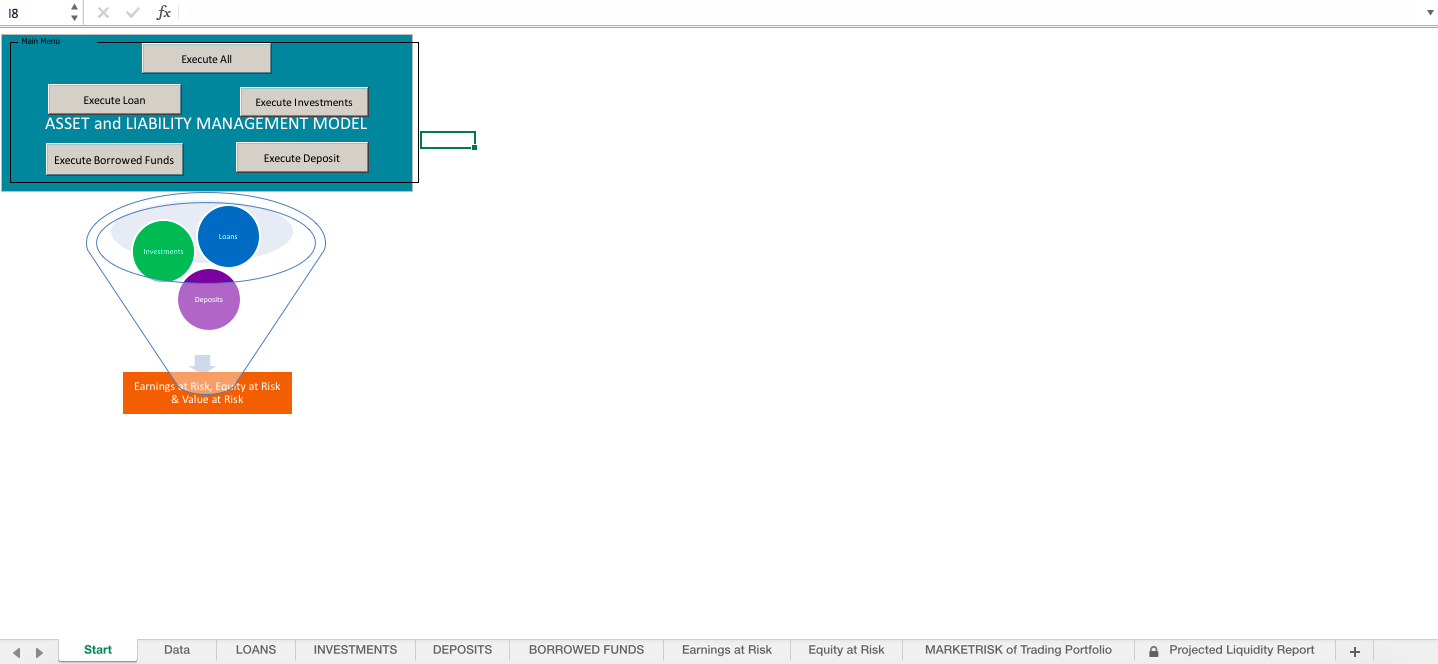

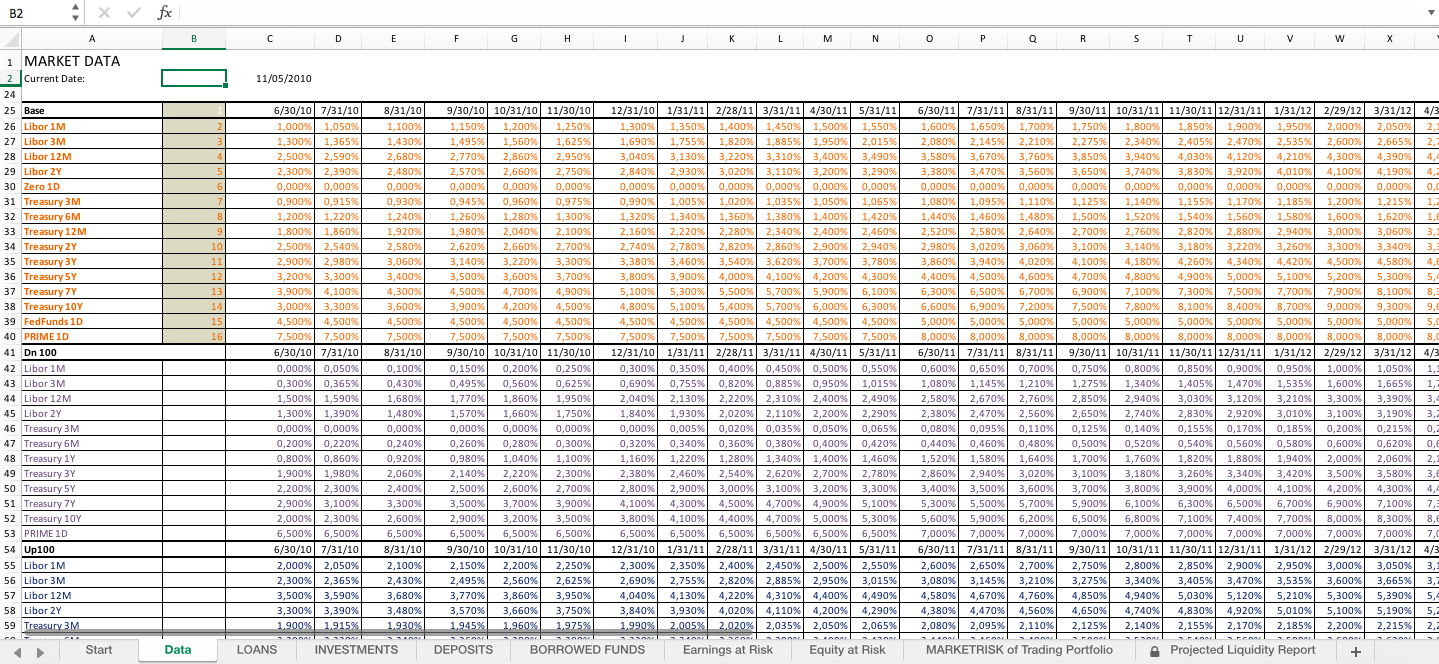

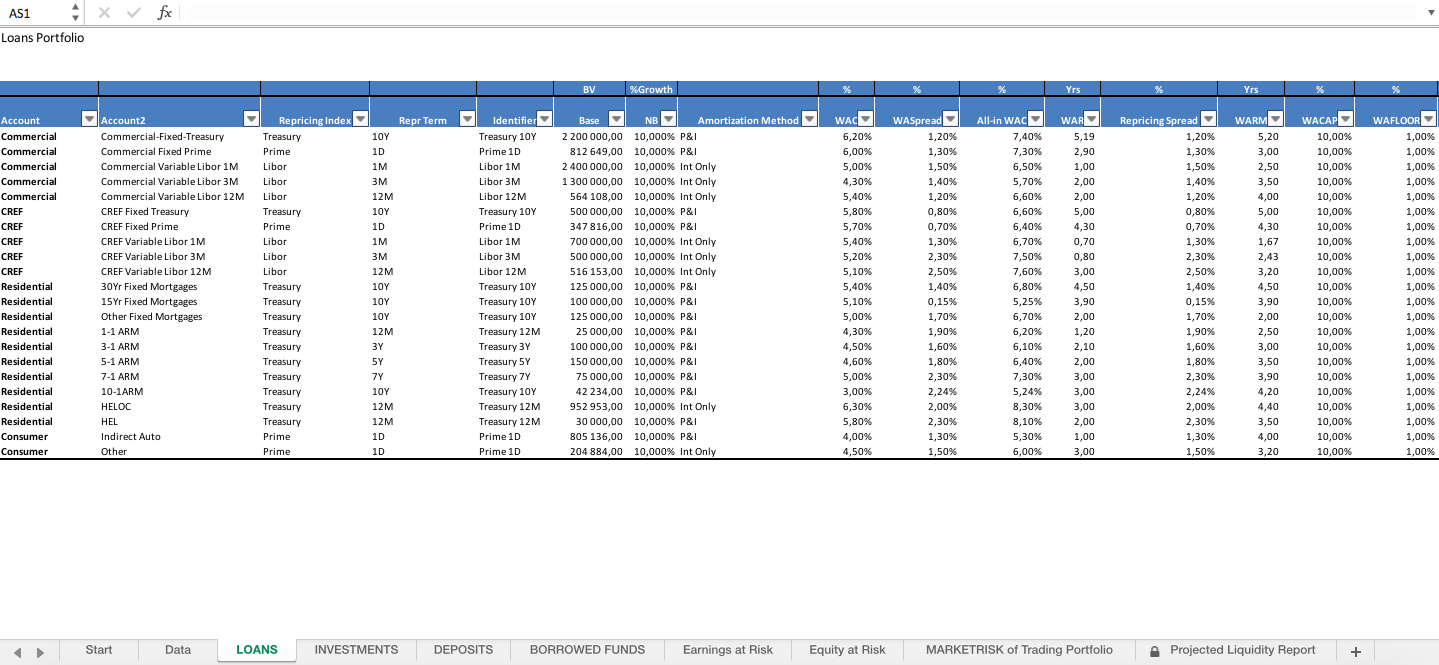

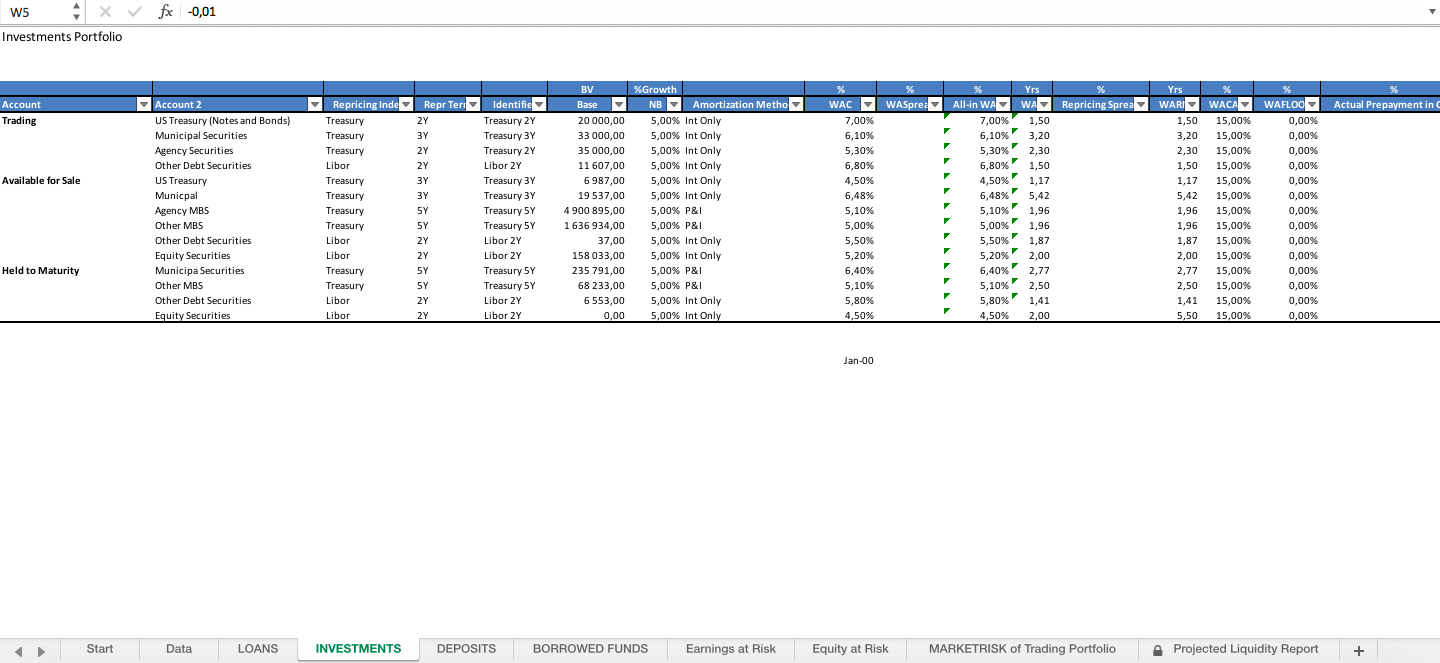

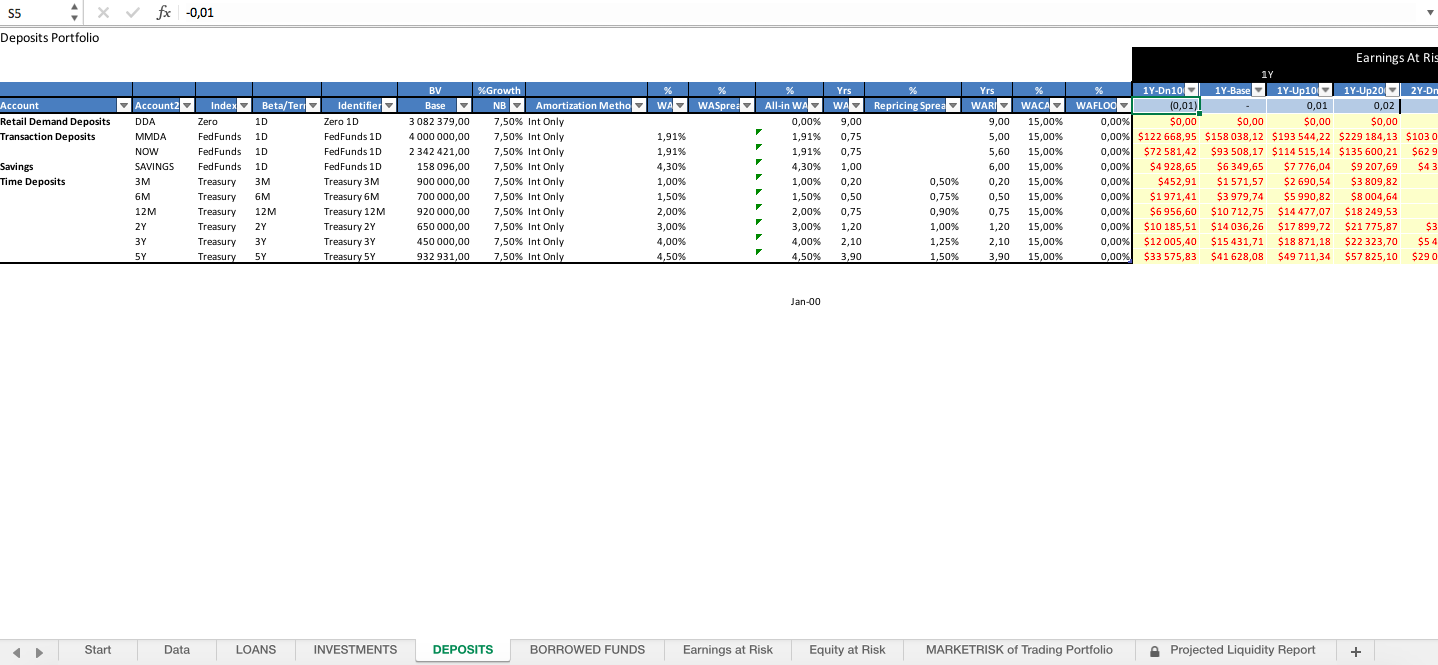

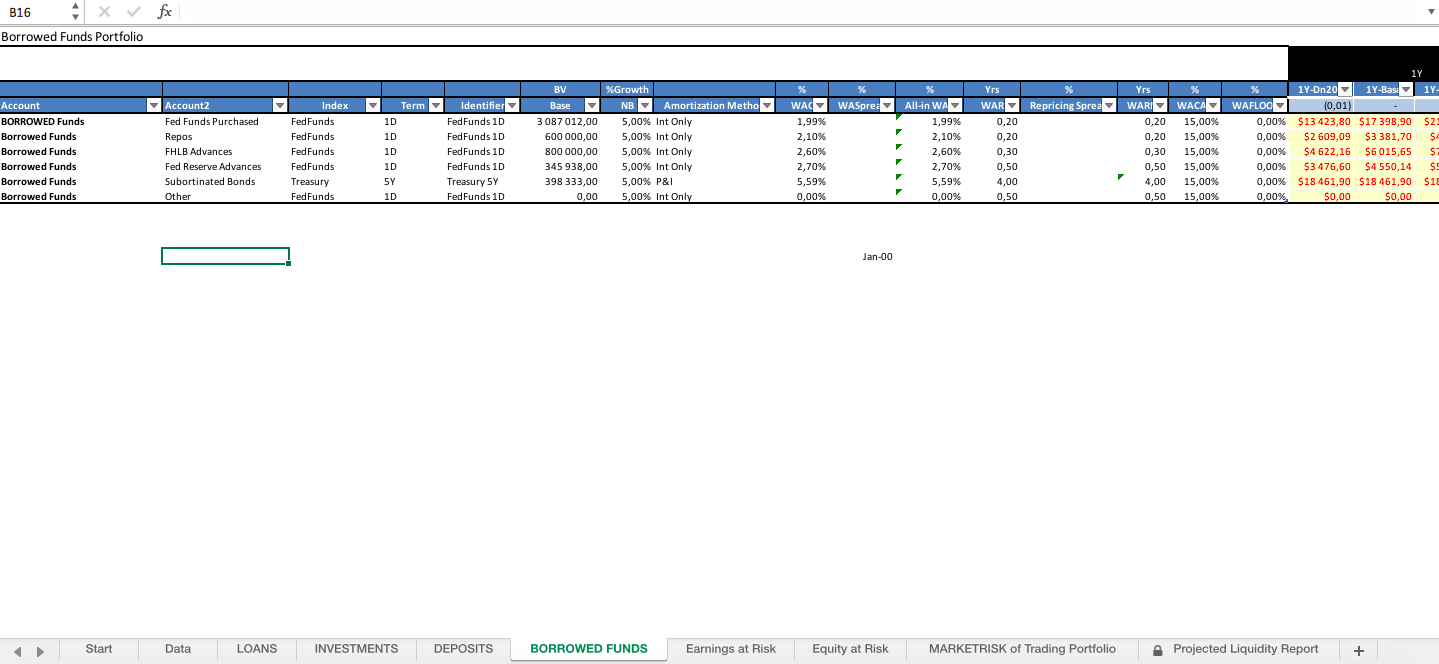

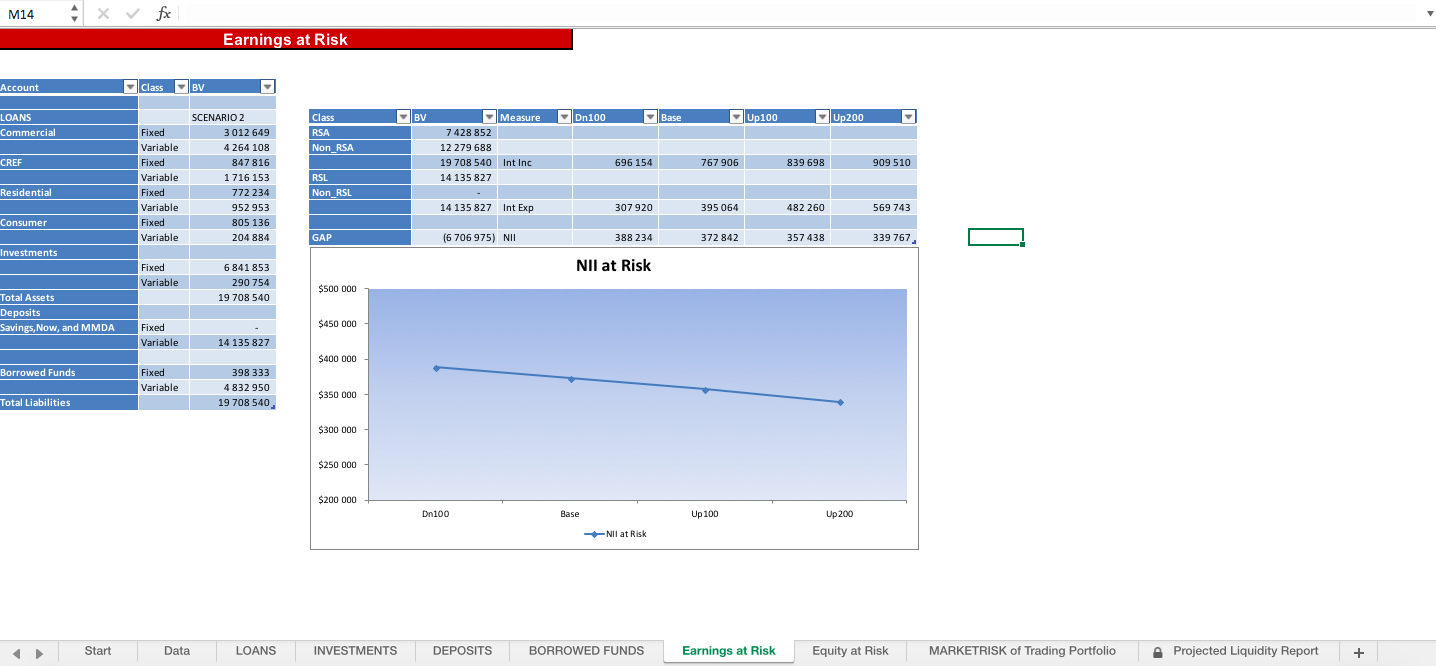

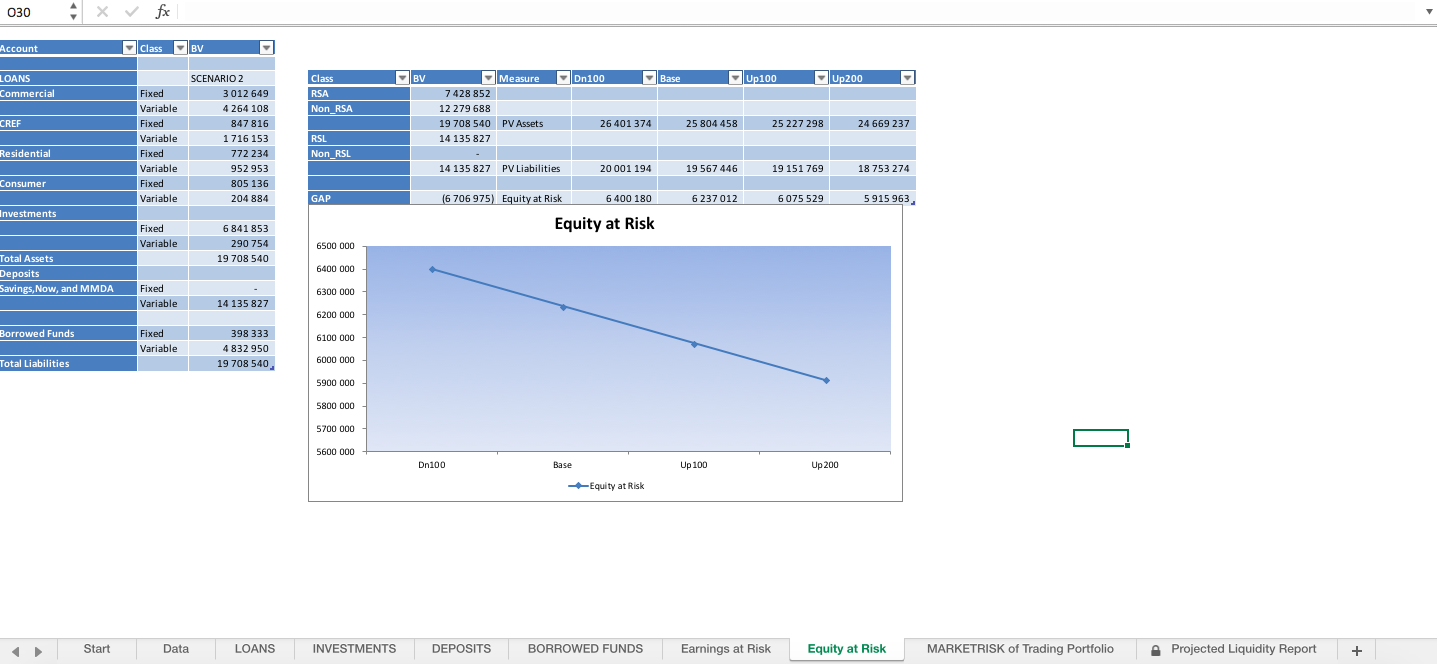

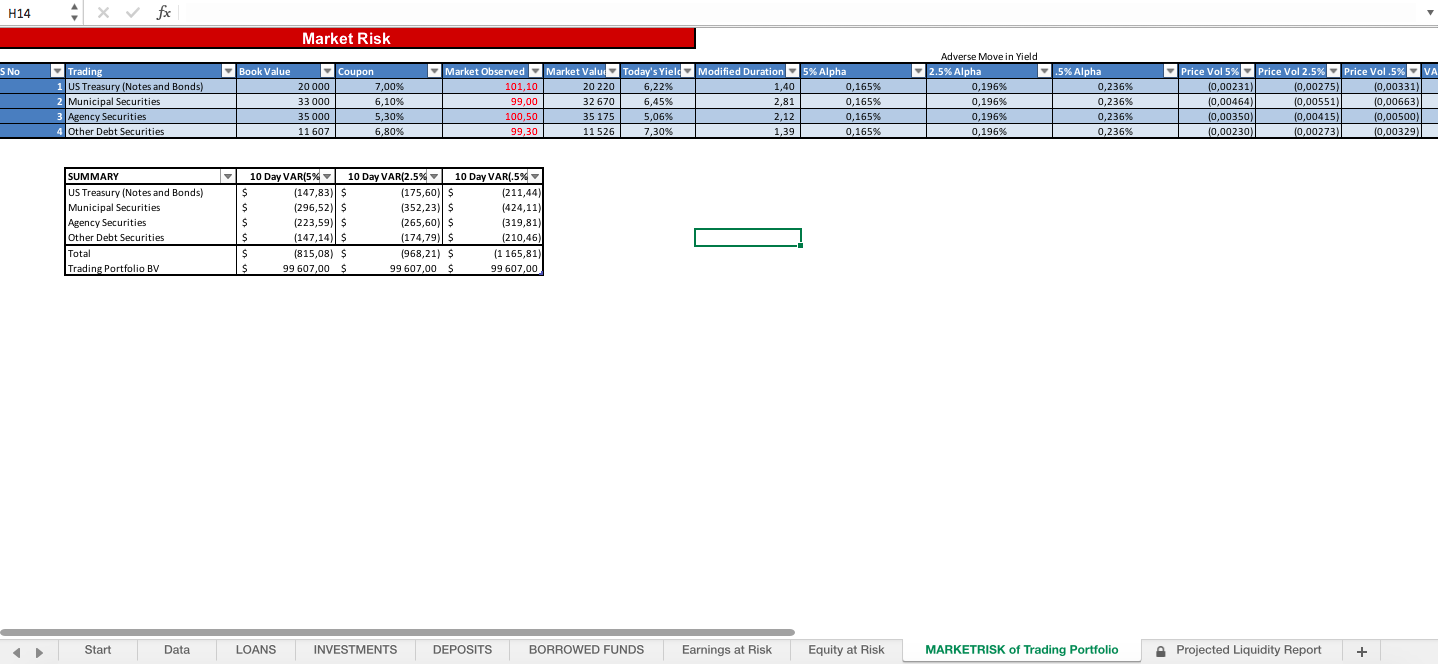

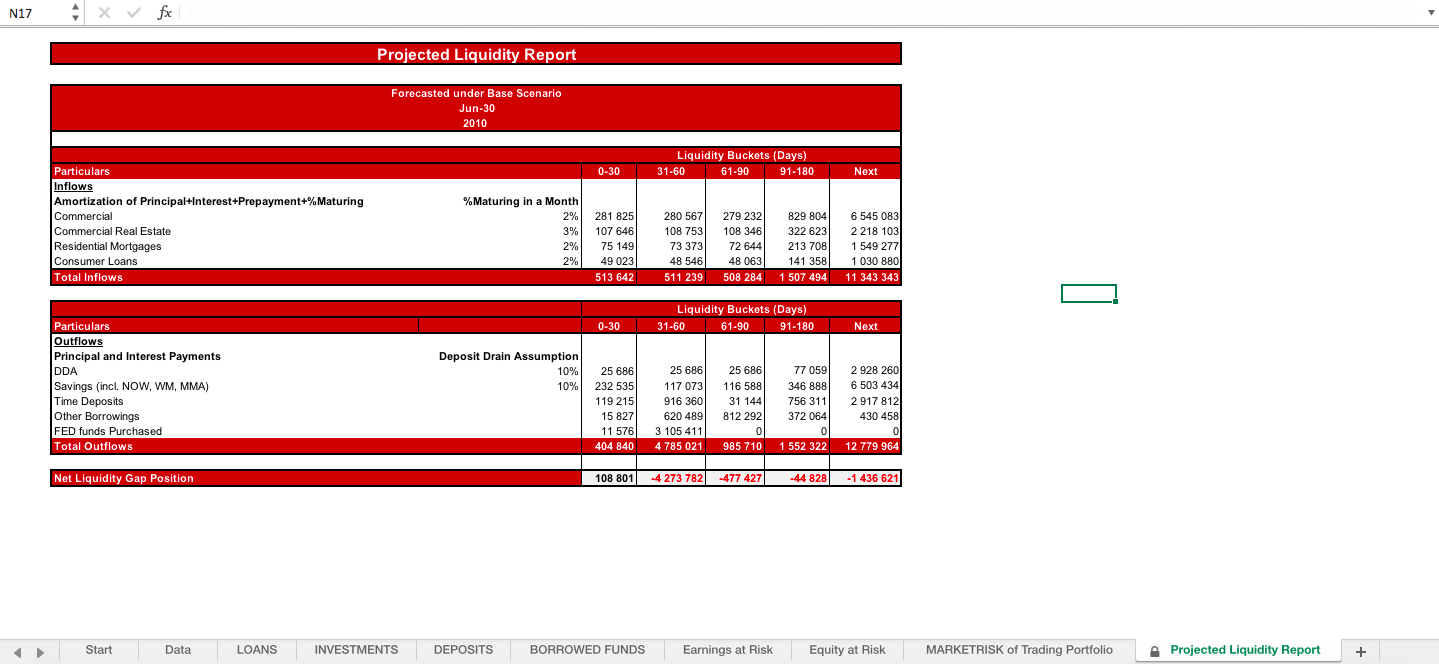

Asset and Liability (ALM) Excel Model

ALM Model to compute Earnings at Risk and Equity at Risk for a TIER 3 bank or Credit Union

Further information

Computes the first cut Earnings at Risk and Equity at Risk for a Bank

The tool is meant for inputs calculated at the balance weighted average of portfolio level of the Bank

No account level information