Originally published: 04/11/2020 15:18

Publication number: ELQ-19862-1

View all versions & Certificate

Publication number: ELQ-19862-1

View all versions & Certificate

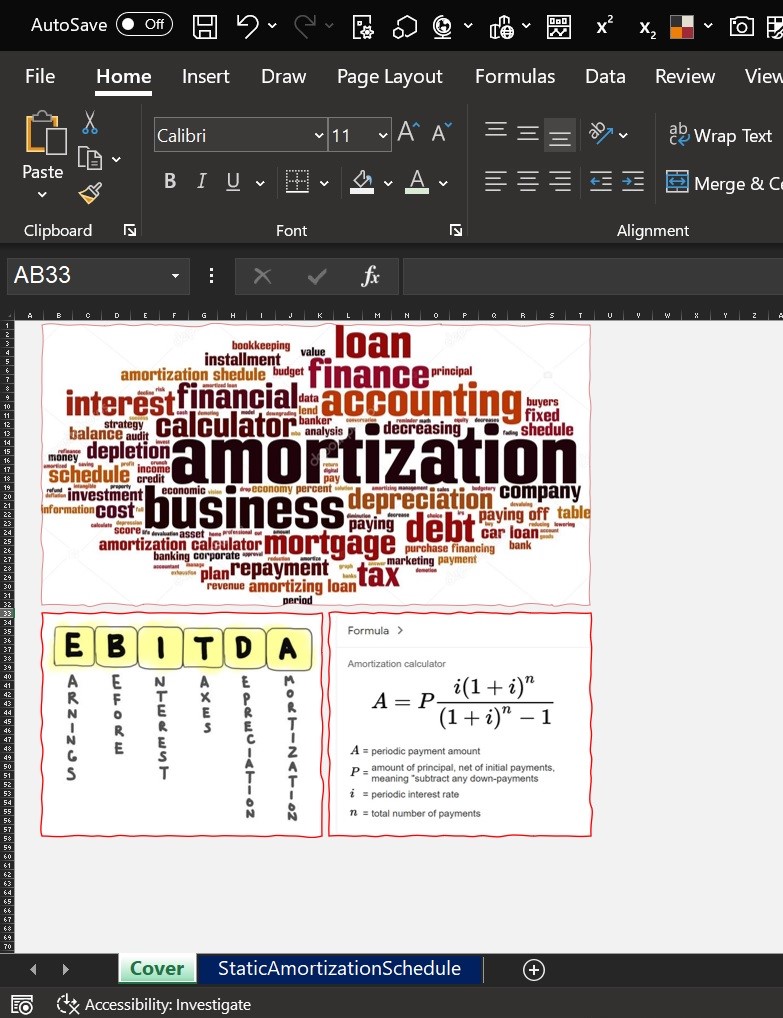

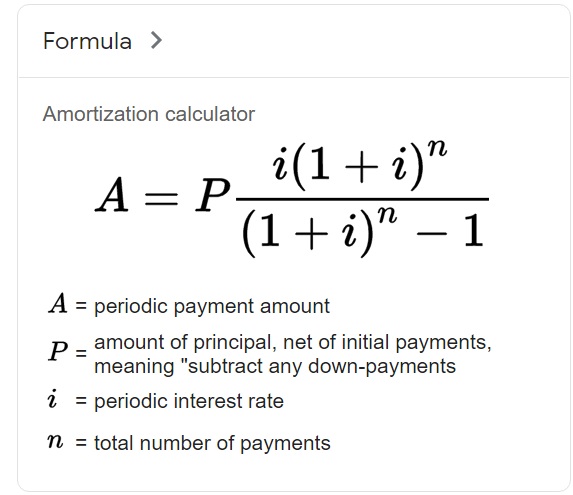

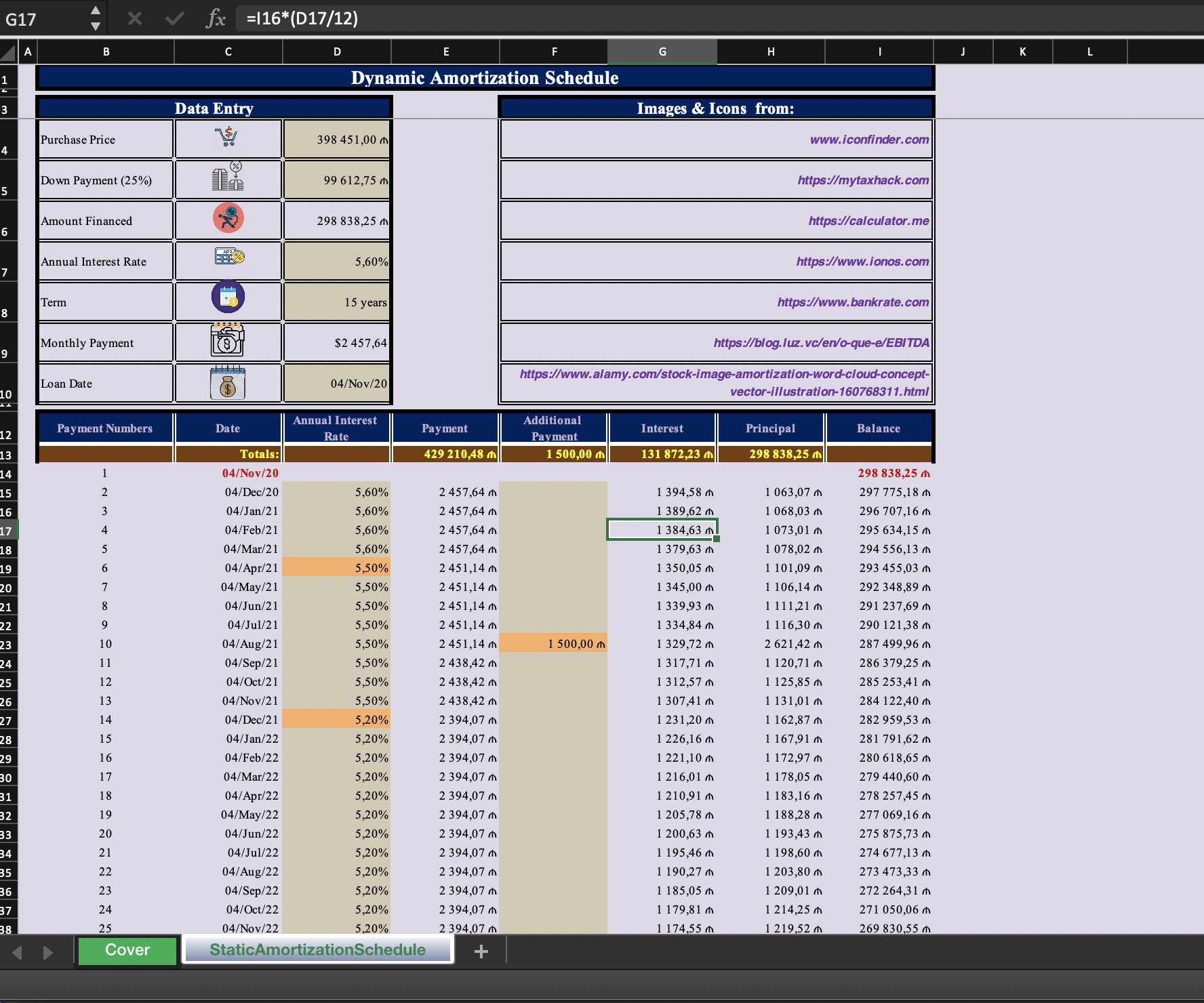

Dynamic Amortization Schedule

Dynamic Amortization Schedule in Microsoft Excel.

Further information

Financial Modelers are recommended to use this template

Two additional columns: Annual Interest Rate and Additional Payment differentiate make this template dynamic

Dynamic Array Functions would improve the quality of template