Publication number: ELQ-55584-1

View all versions & Certificate

Advanced Securitization Financial Model with Floating-Rate Corridor (Cap & Floor) Mechanism

An institutional-grade Securitization Financial Model featuring an automated Interest Rate Corridor (Cap & Floor) mechanism. Perfectly designed for DCM professi

In a highly volatile macroeconomic environment, managing interest rate risk is a critical priority for structural finance professionals. When structuring asset-backed securitization (ABS) transactions with floating-rate tranches, issuers risk surging funding costs, while investors demand protection against falling yields.

This Premium, Institutional-Grade Securitization Financial Model bridges that gap. It features a fully automated, dynamic Interest Rate Corridor (Cap & Floor) Mechanism built directly into the cash flow architecture. Designed by an experienced Debt Capital Markets (DCM) professional, this model provides investment bankers, corporate treasurers, and credit analysts with a robust, market-ready framework to structure, price, and stress-test complex debt issuances.

The file "Securtization Professional Financial Model with Corridor Cap-Floor Mechanism.xlsx" is designed following strict financial modeling best practices—fully dynamic, color-coded, and completely formula-driven (no hardcoded numbers in the calculation sheets).

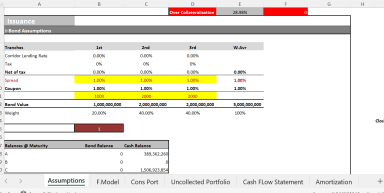

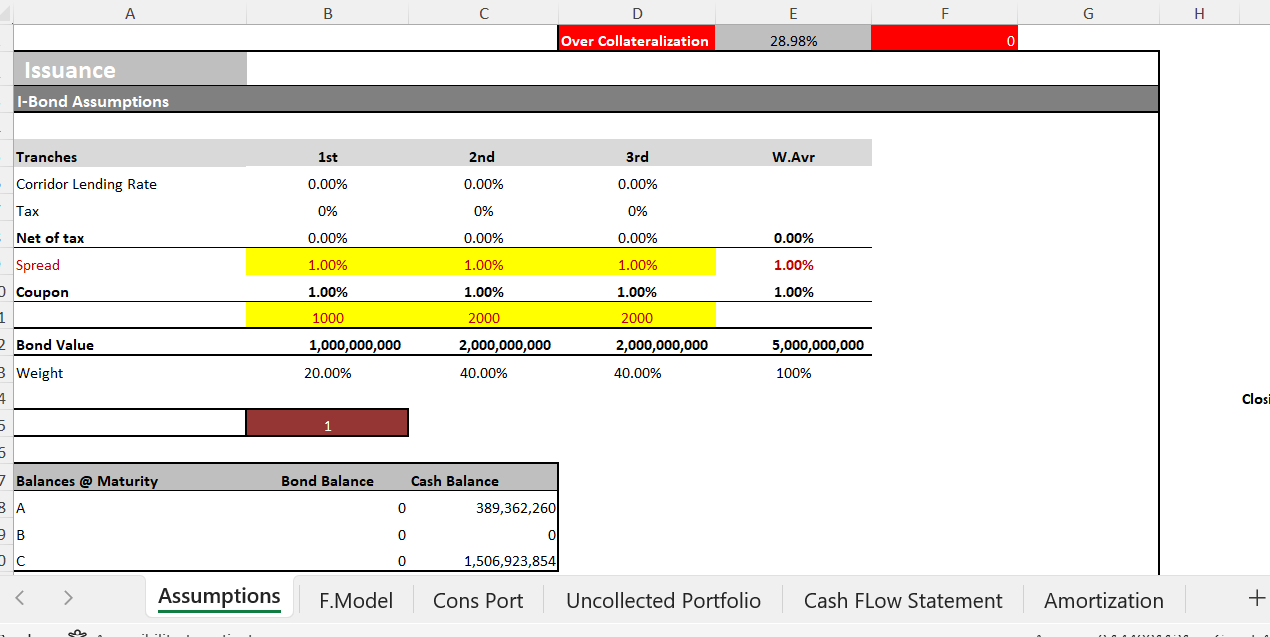

Portfolio Parameters: Total portfolio size, weighted average interest rate, remaining maturity, and historical prepayment/default assumptions.

Tranche Structuring: Sizing, baseline pricing spreads, and initial definitions for the floating benchmark rate.

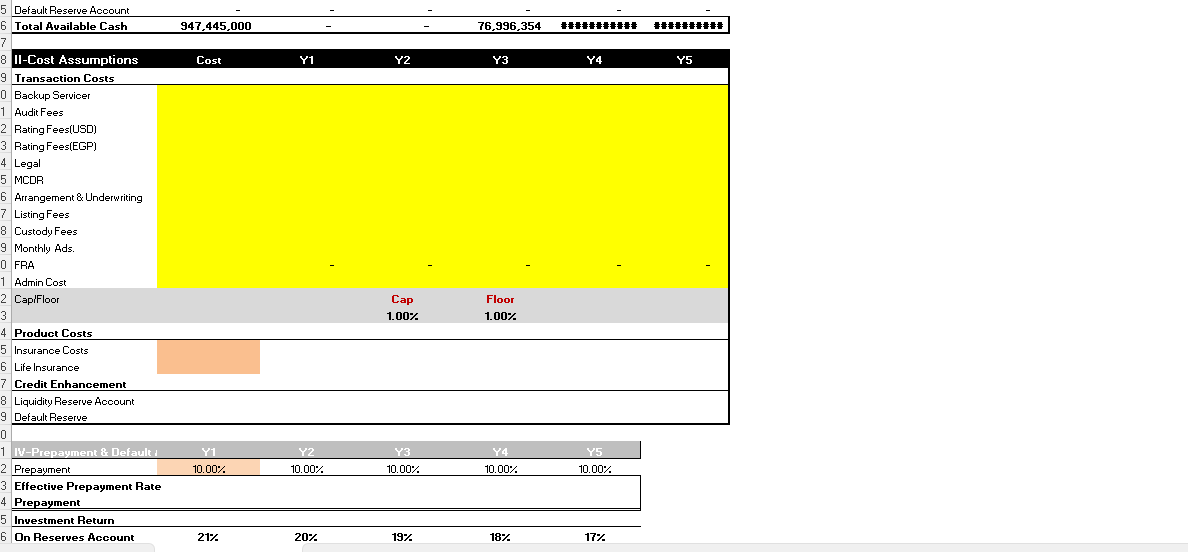

Corridor Setup: Explicit input fields to set the Upper Cap and Lower Floor percentages to drive the hedging mechanism.

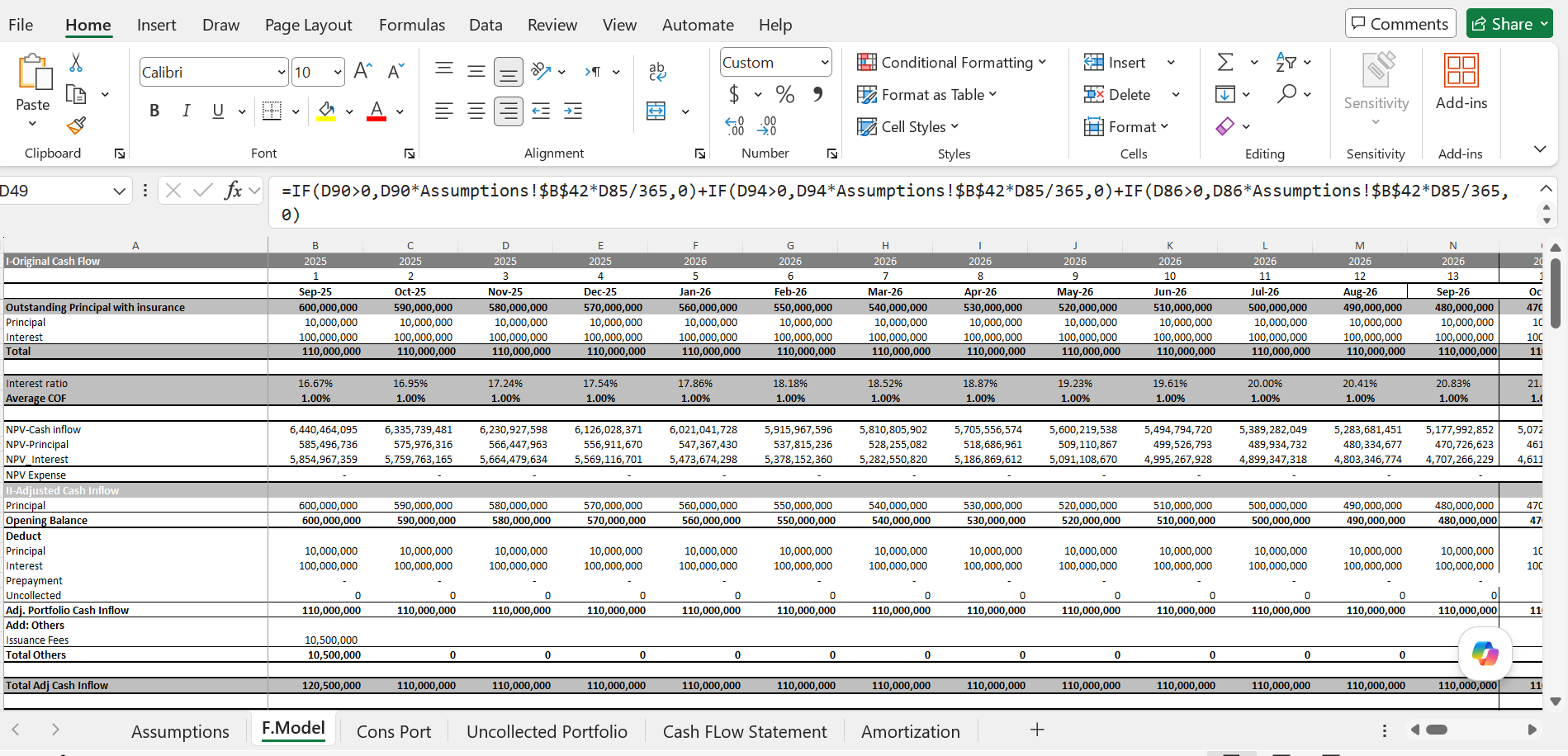

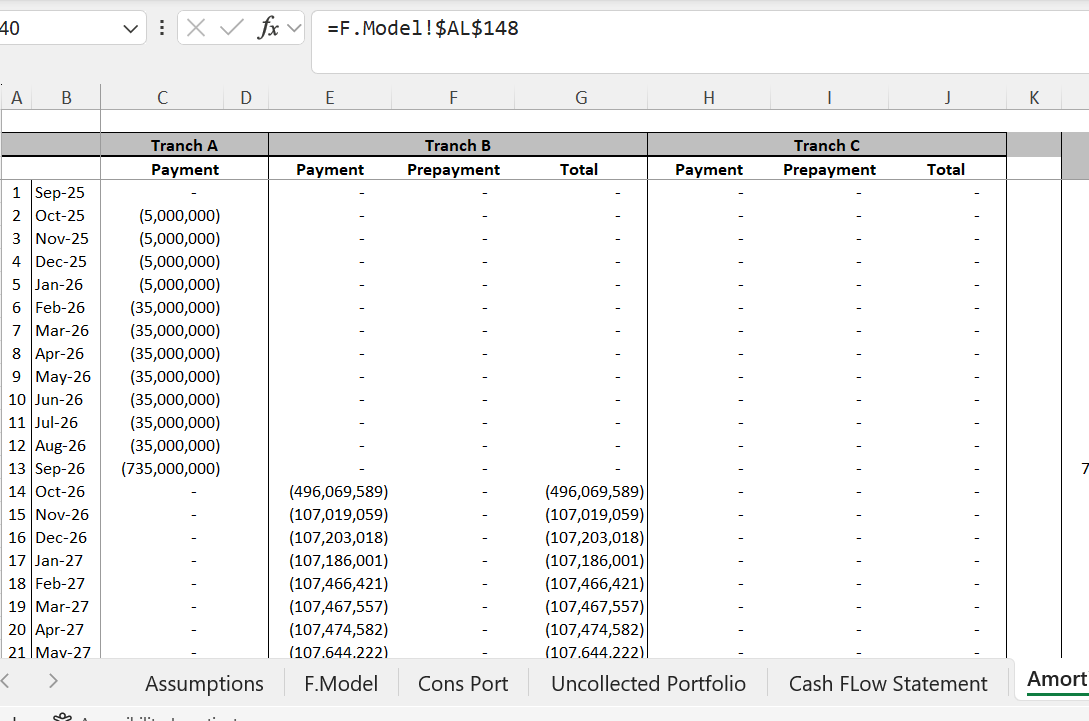

Generates the monthly asset-side cash flows, breaking down regular principal collections, interest income, prepayments, and defaults to establish the net liquidity flowing into the structure.

The Core Engine: Uses optimized IF, MIN, and MAX logic to determine the exact effective interest rate per period.

The Waterfall: Simulates the waterfall hierarchy, ensuring senior expenses and interest are paid before filling reserve accounts and releasing excess spread.

Toggle between a Base Case, Rate Spike (Cap Activation), and Rate Drop (Floor Activation) to evaluate structural integrity and coverage ratios under macroeconomic stress.

Executive-ready charts illustrating the benchmark rate vs. the effective capped/floored rate, alongside portfolio vs. liability amortization curves. Perfect for direct copying into investment committee pitchbooks.

Investment Banking & DCM Teams: Speed up transaction structuring and avoid building complex ABS models from scratch.

Corporate Treasury Directors: Evaluate securitization as an optimized alternative funding tool and understand how to negotiate pricing structures.

Credit Risk Analysts & Portfolio Managers: Audit and verify structured debt products by reverse-engineering stress scenarios.

Who is this Model for?

This Best Practice includes

Several Excel support