Publication number: ELQ-32392-1

View all versions & Certificate

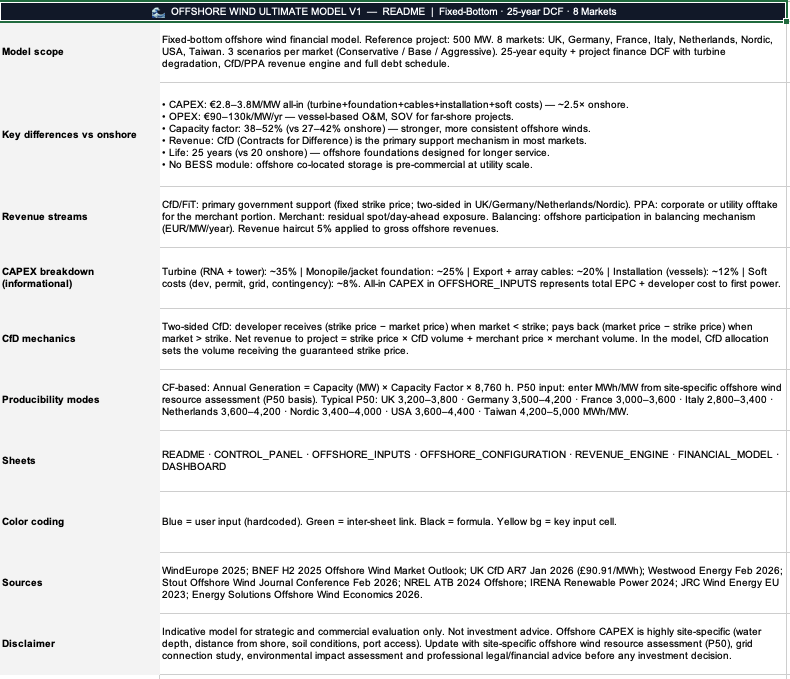

Offshore Wind Ultimate Model — Fixed-Bottom · 8 Markets · CFD Mechanics · 25-Year DCF

You have an offshore wind project to evaluate. This production-ready Excel model gives you a fully calibrated 25-year DCF across 8 markets with correct CFD

Further information

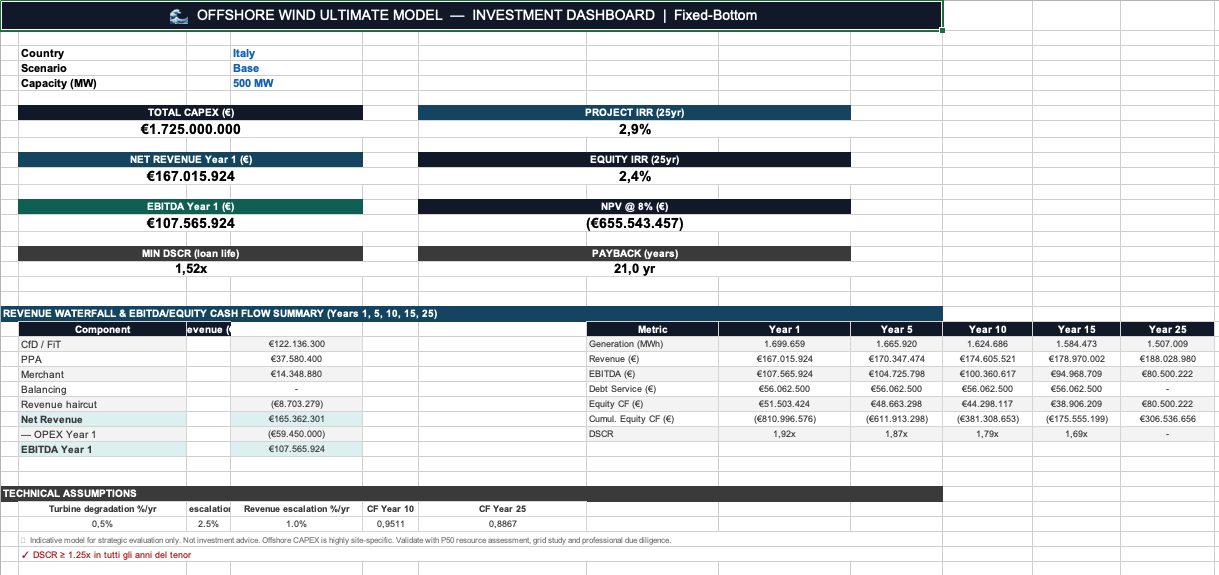

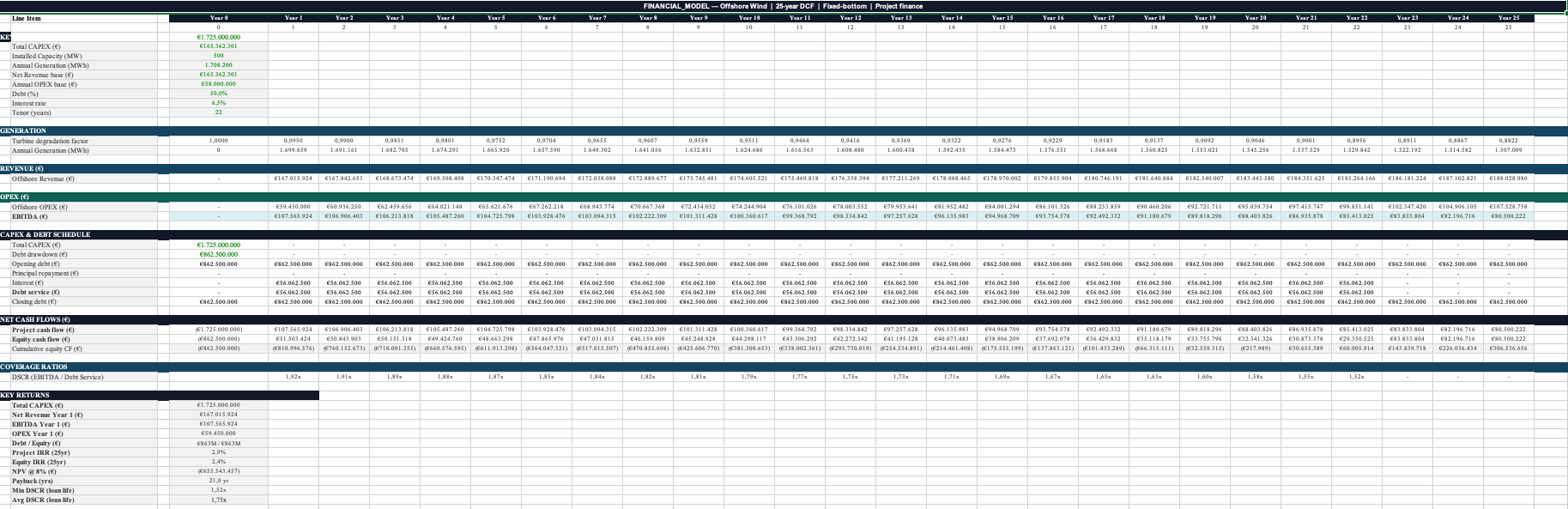

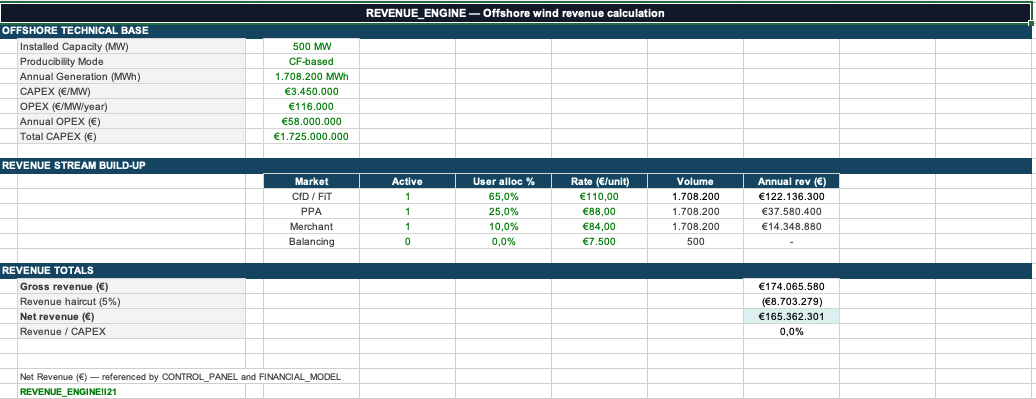

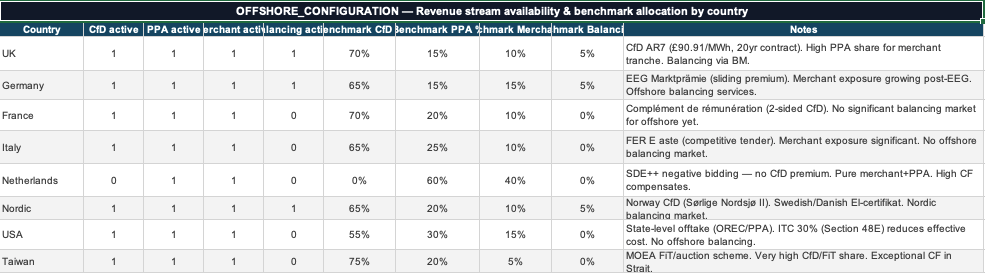

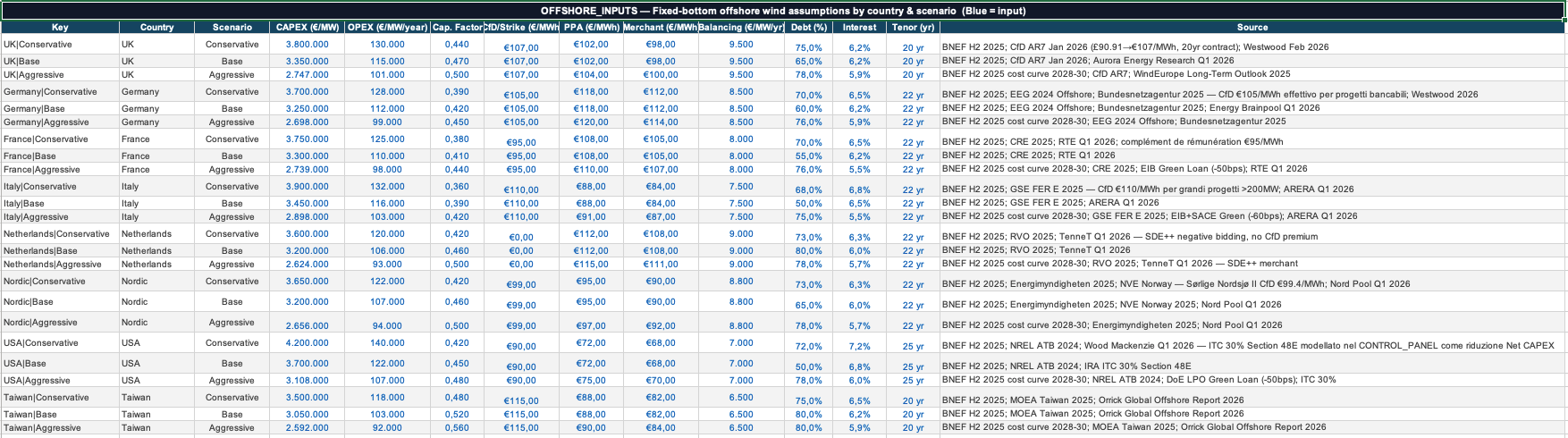

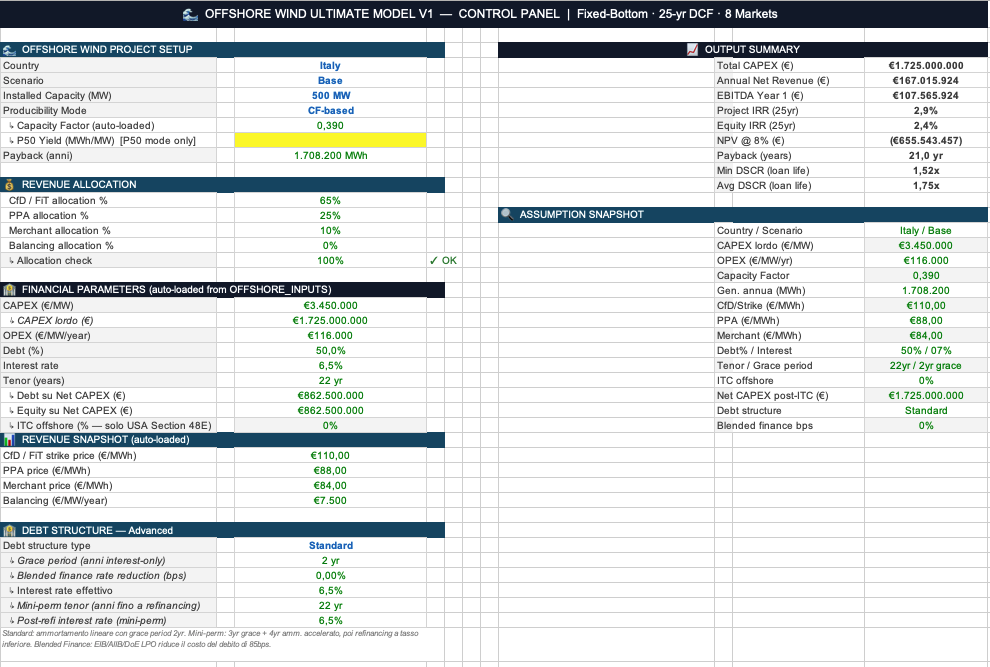

This model enables developers, advisors and investors to evaluate the financial viability of a fixed-bottom offshore wind project across 8 international markets with correctly modelled two-sided CfD mechanics, without building a specialist model from scratch. It supports comparison across Conservative, Base and Aggressive scenarios, handles the market-specific revenue configurations that differ significantly across countries, and produces a full set of project finance returns — Project IRR, Equity IRR, NPV, minimum DSCR and average DSCR — from a 25-year cash flow that reflects the actual design life of offshore foundations. It also enables evaluation of three distinct debt structures — Standard, Mini-perm and Blended Finance — from a single CONTROL_PANEL selector.

This model is best suited to fixed-bottom offshore wind greenfield projects in the 200–1,000 MW range at early-stage feasibility, strategic screening or commercial evaluation, prior to full technical due diligence. It is calibrated for UK, Germany, France, Italy, Netherlands, Nordic, USA and Taiwan, and works particularly well when a P50 offshore wind resource assessment is available — typical P50 ranges by market are provided in the model. It is also well suited to structured finance contexts where mini-perm or blended finance structures need to be evaluated alongside standard project finance, and to M&A and advisory contexts requiring a rigorous, auditable Excel model.

This model covers fixed-bottom offshore wind only and is not designed for floating offshore wind, which has materially different CAPEX structures, mooring and dynamic cable costs, and financing terms that are not yet standardised at utility scale. It does not include a co-located BESS module, as offshore battery storage at utility scale remains pre-commercial. It is not suited to markets outside the 8 pre-loaded countries without manual customisation of the assumption sets. It should not be used as the sole basis for a final investment decision — offshore CAPEX is highly site-specific, driven by water depth, distance from shore, soil conditions and port access, and must be validated with a site-specific offshore wind resource assessment, grid connection study, environmental impact assessment and professional legal and financial advice. Projects below 100 MW will likely see different cost structures than the benchmark assumptions in the model.