Publication number: ELQ-88821-1

View all versions & Certificate

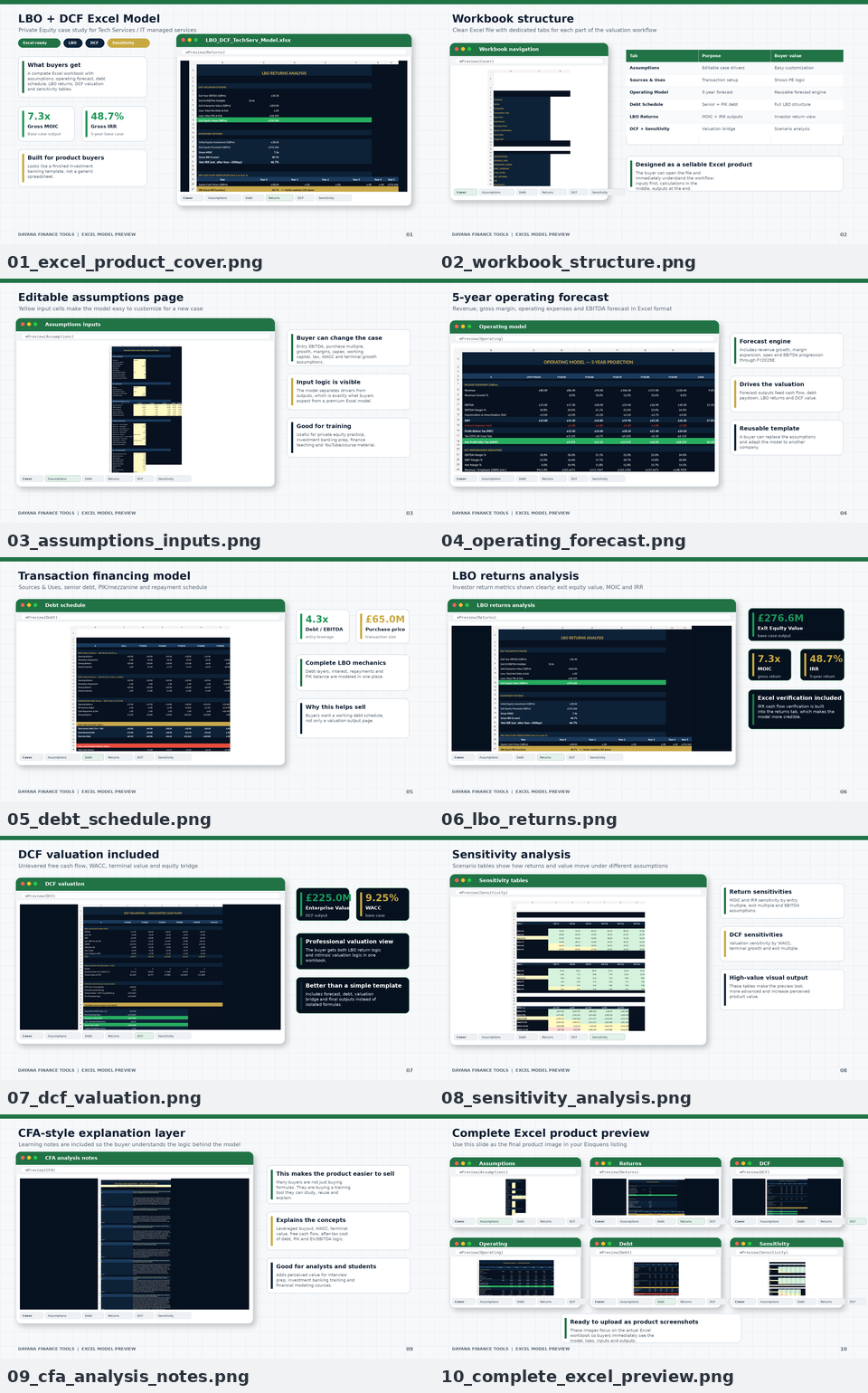

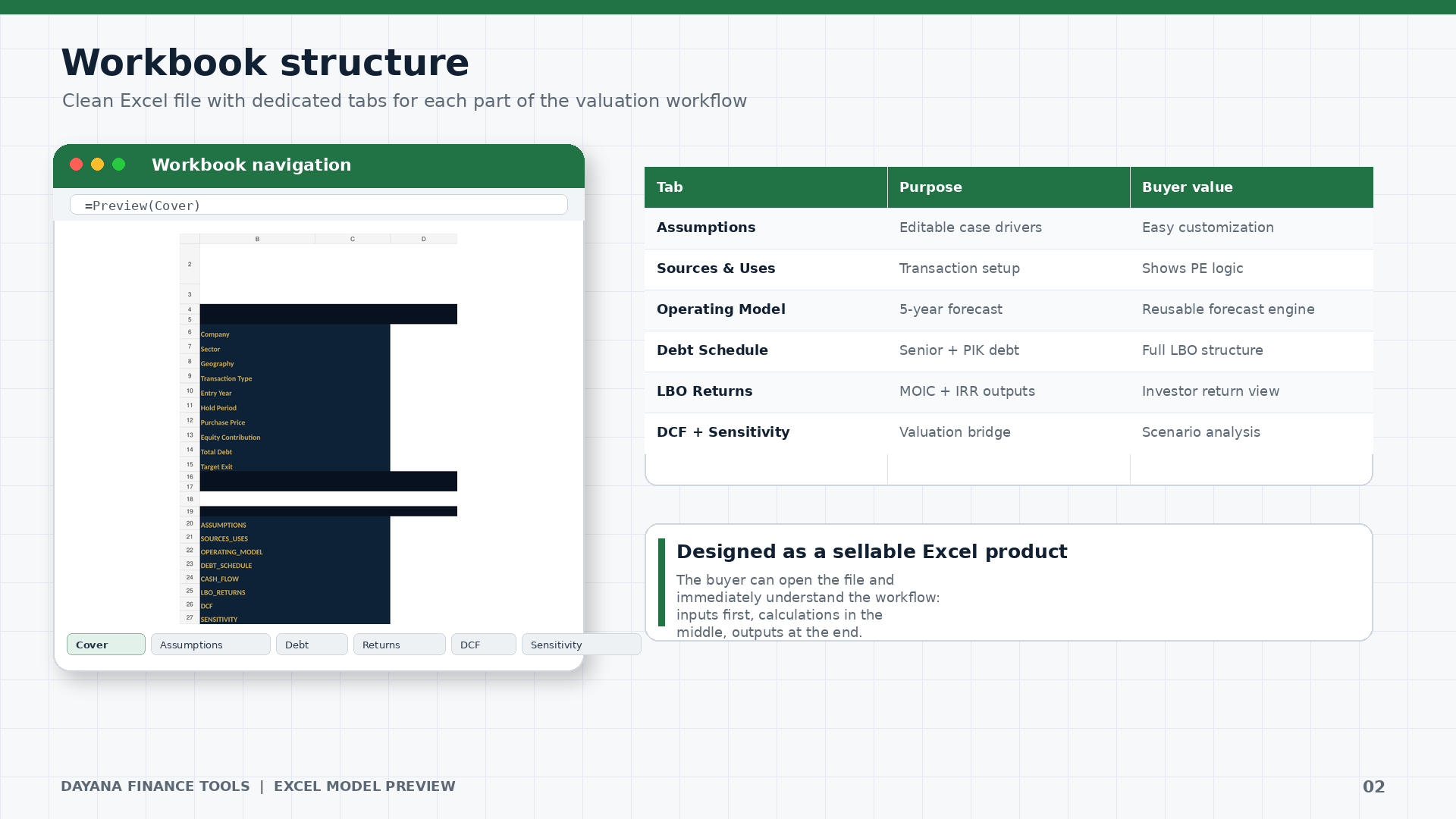

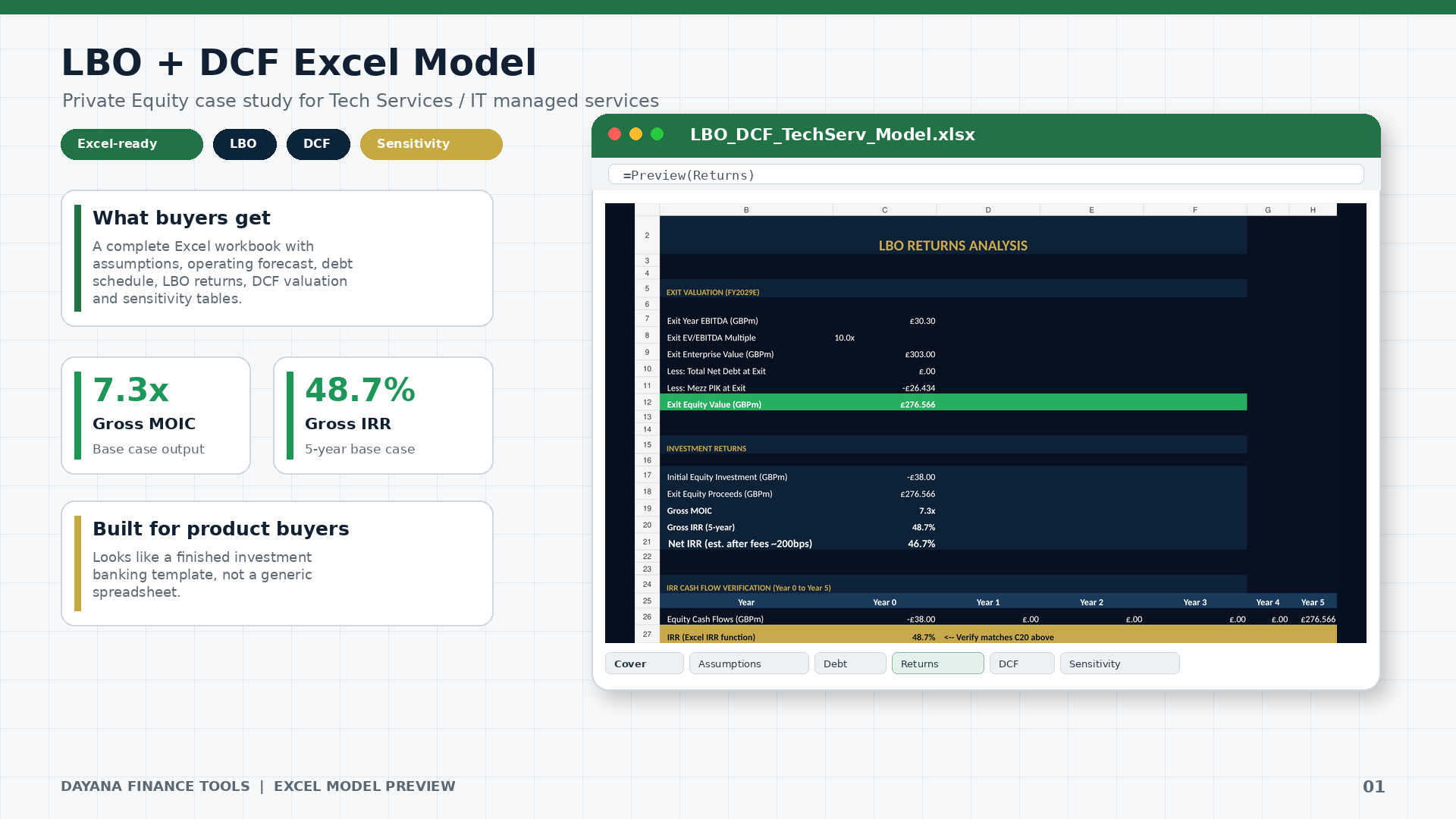

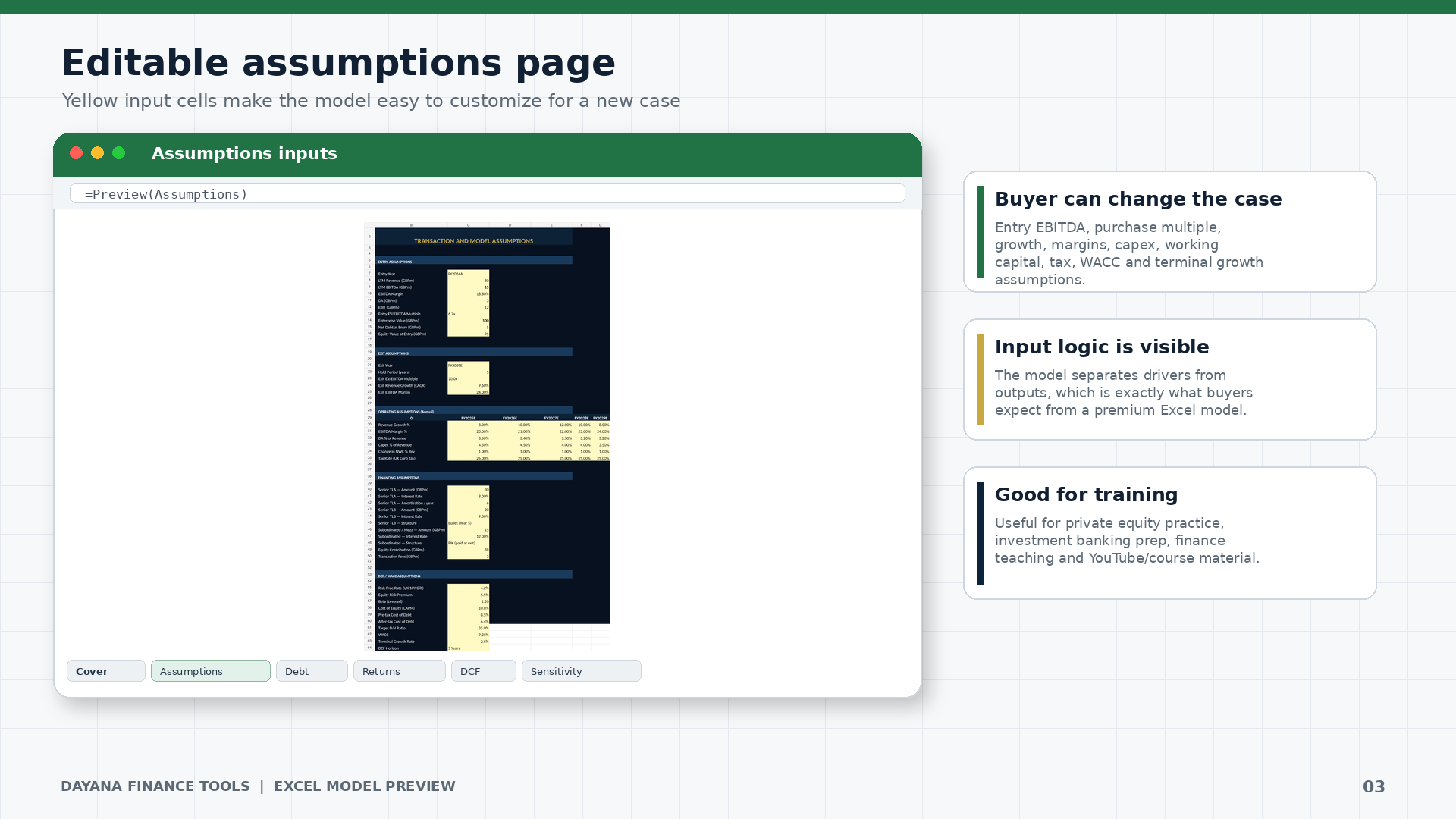

LBO & DCF Valuation Model - TechServ Holdings (Excel + Investment Memo) | CFA Prep

Advanced LBO & DCF financial model plus Investment Memo Word guide, perfectly aligned with CFA Level 2/3 prep.

I design professional bilingual (ES/EN) Excel budget planners and financial spreadsheets for small and medium businesses. Automatic charts, cash flow tracking, and deficit alerts included —Follow

Further information

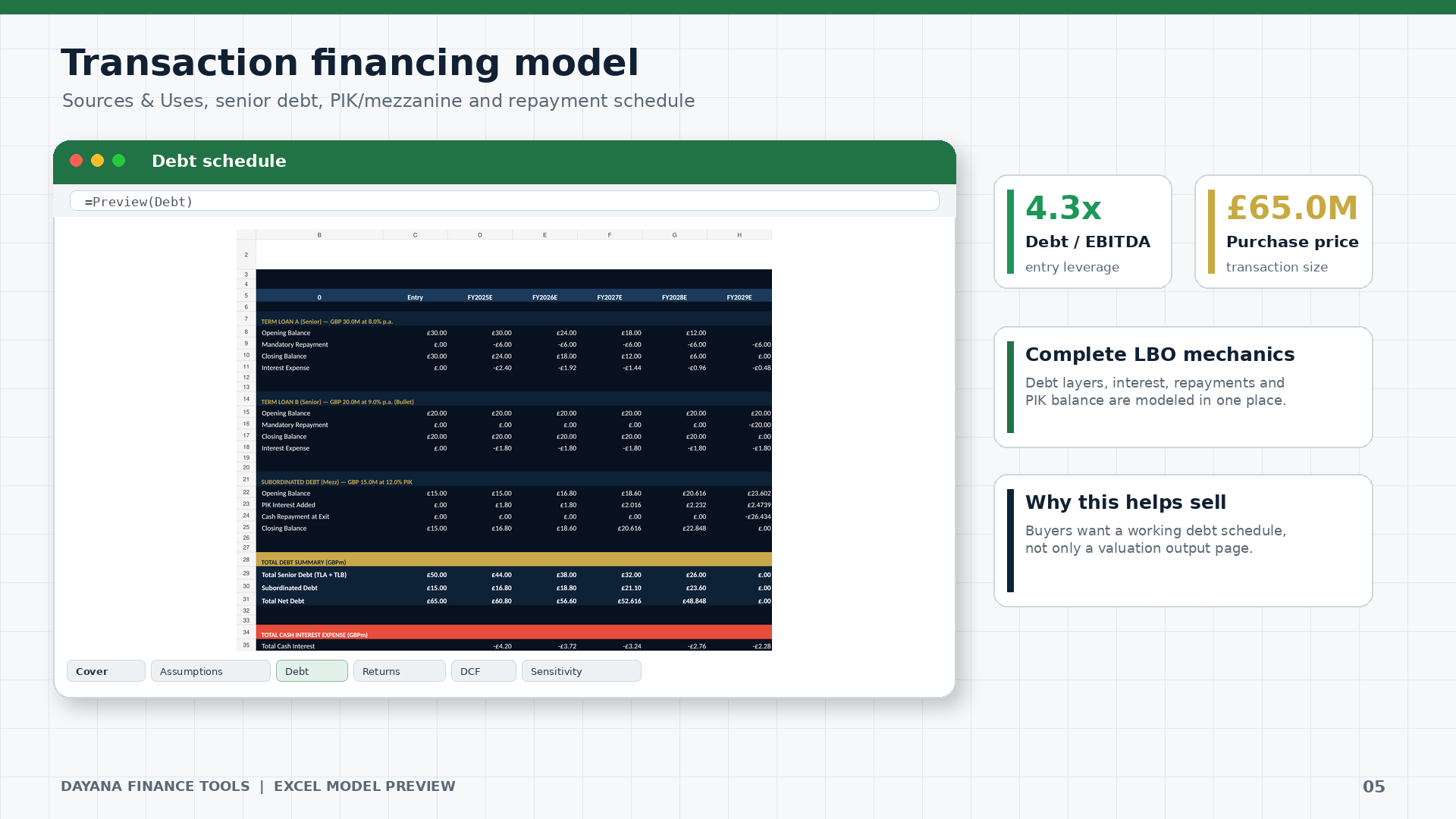

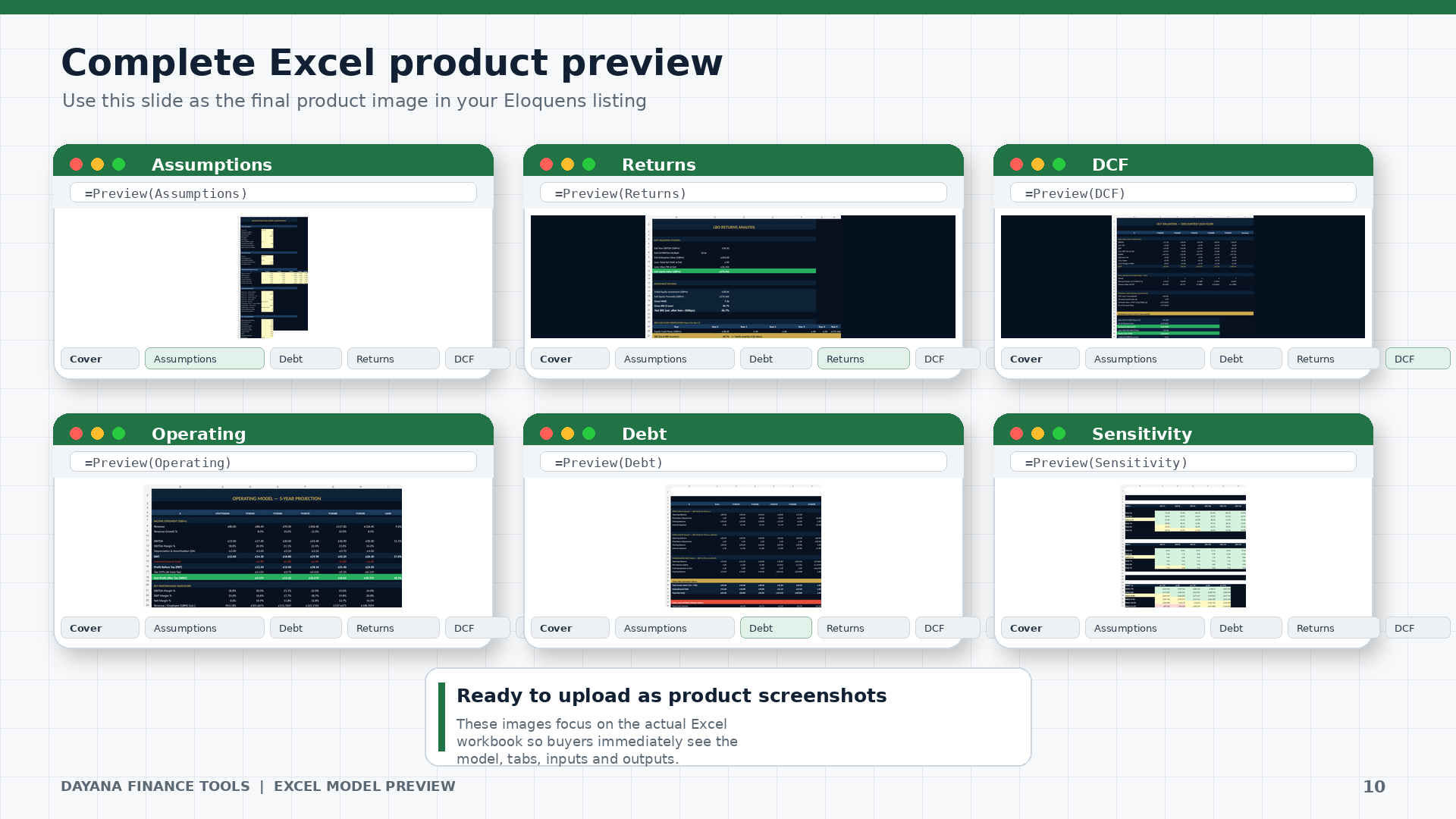

Master Capital Structure Tranches: Understand how to structure and model multi-tiered LBO financing, including Senior Term Loan A (amortizing), Senior Term Loan B (bullet), and Subordinated Mezzanine debt with Payment-in-Kind (PIK) interest mechanics.

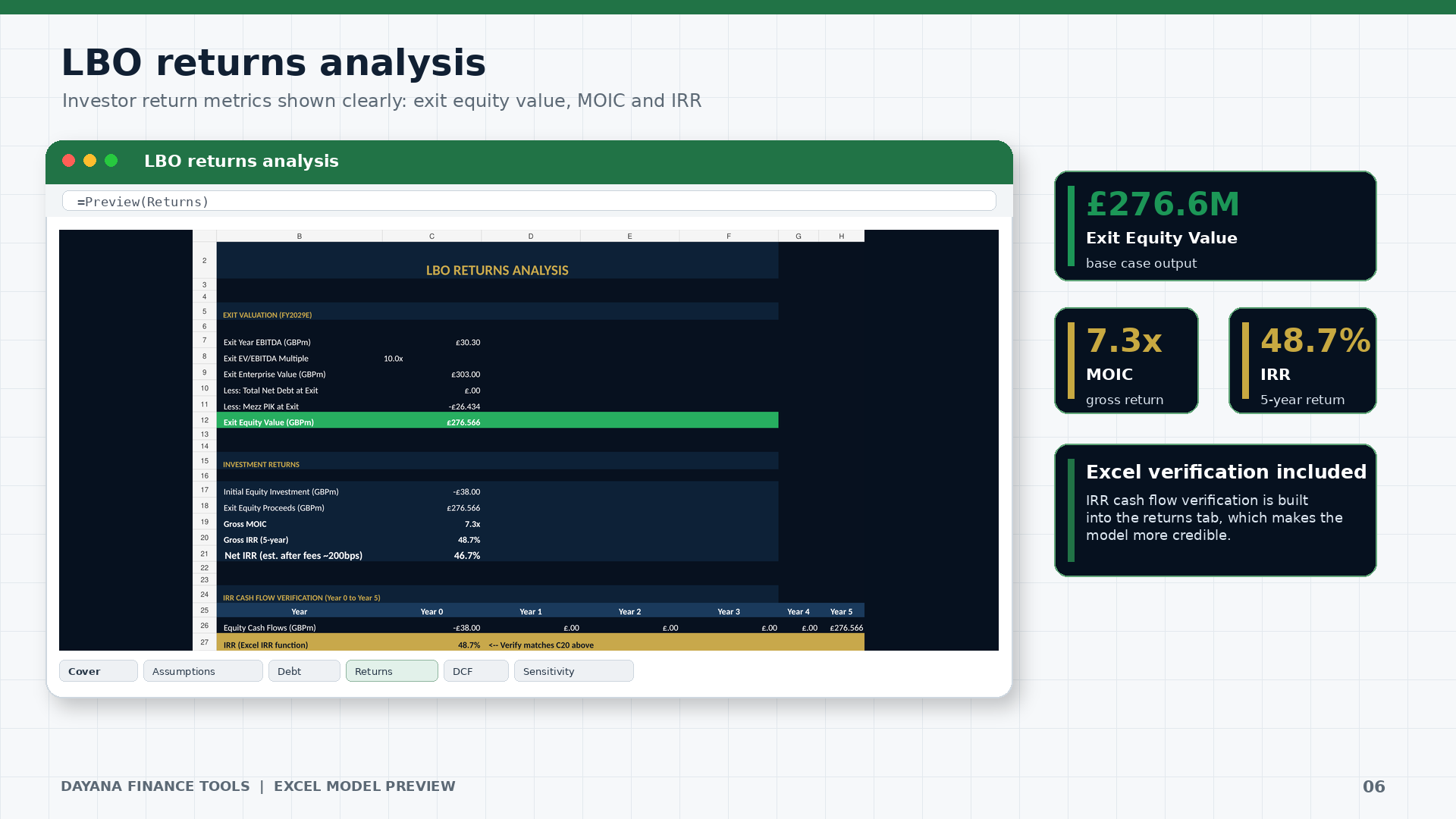

Deconstruct Value-Creation Levers: Quantify and analyze how operational EBITDA growth, multiple expansion (arbitrage), and systematic debt paydown (deleveraging) directly drive sponsor equity returns.

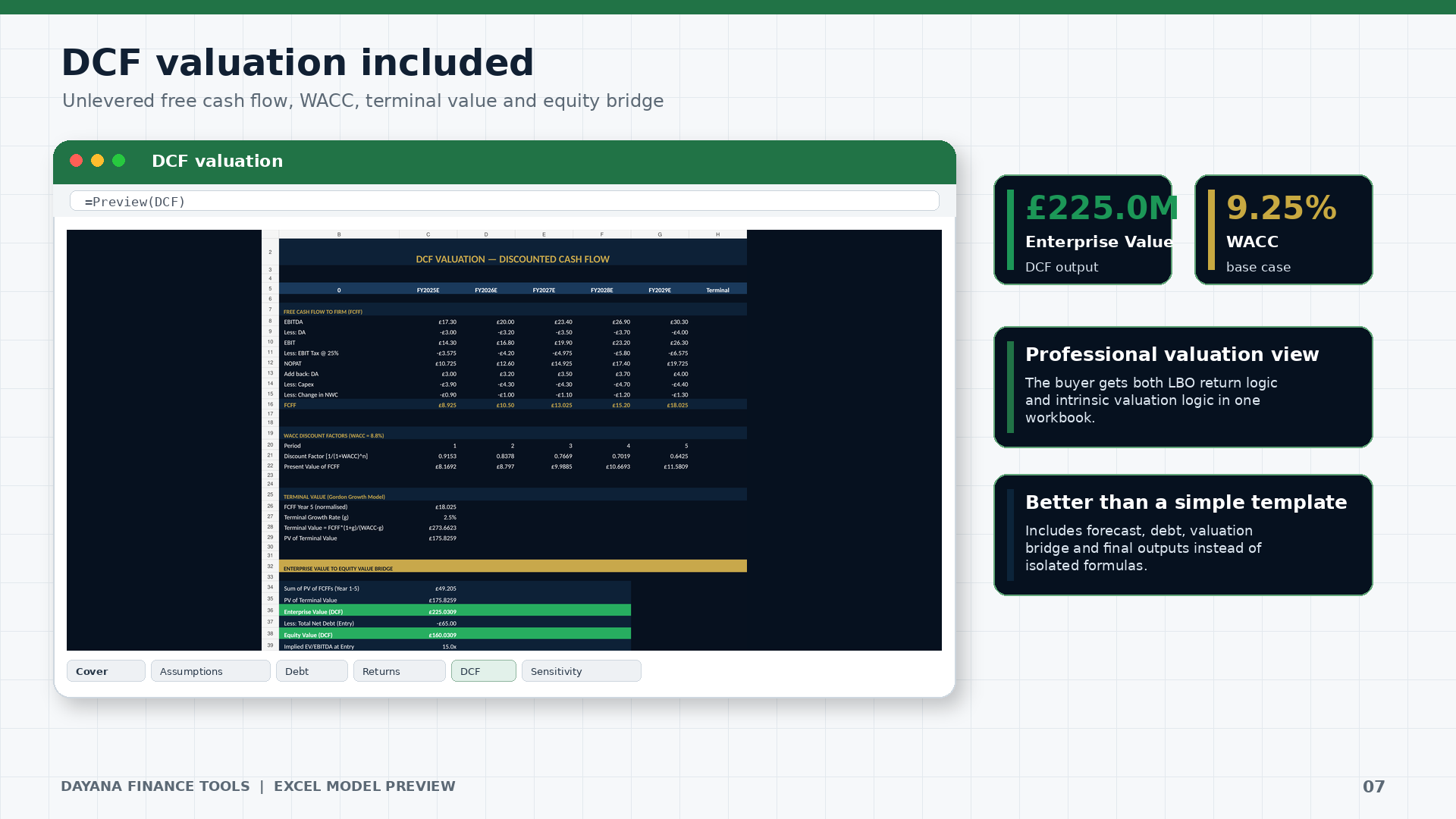

Bridge Intrinsic and Transactional Valuation: Learn how to perform side-by-side comparisons between intrinsic standalone value (via a Discounted Cash Flow framework) and financial sponsor return-driven pricing thresholds.

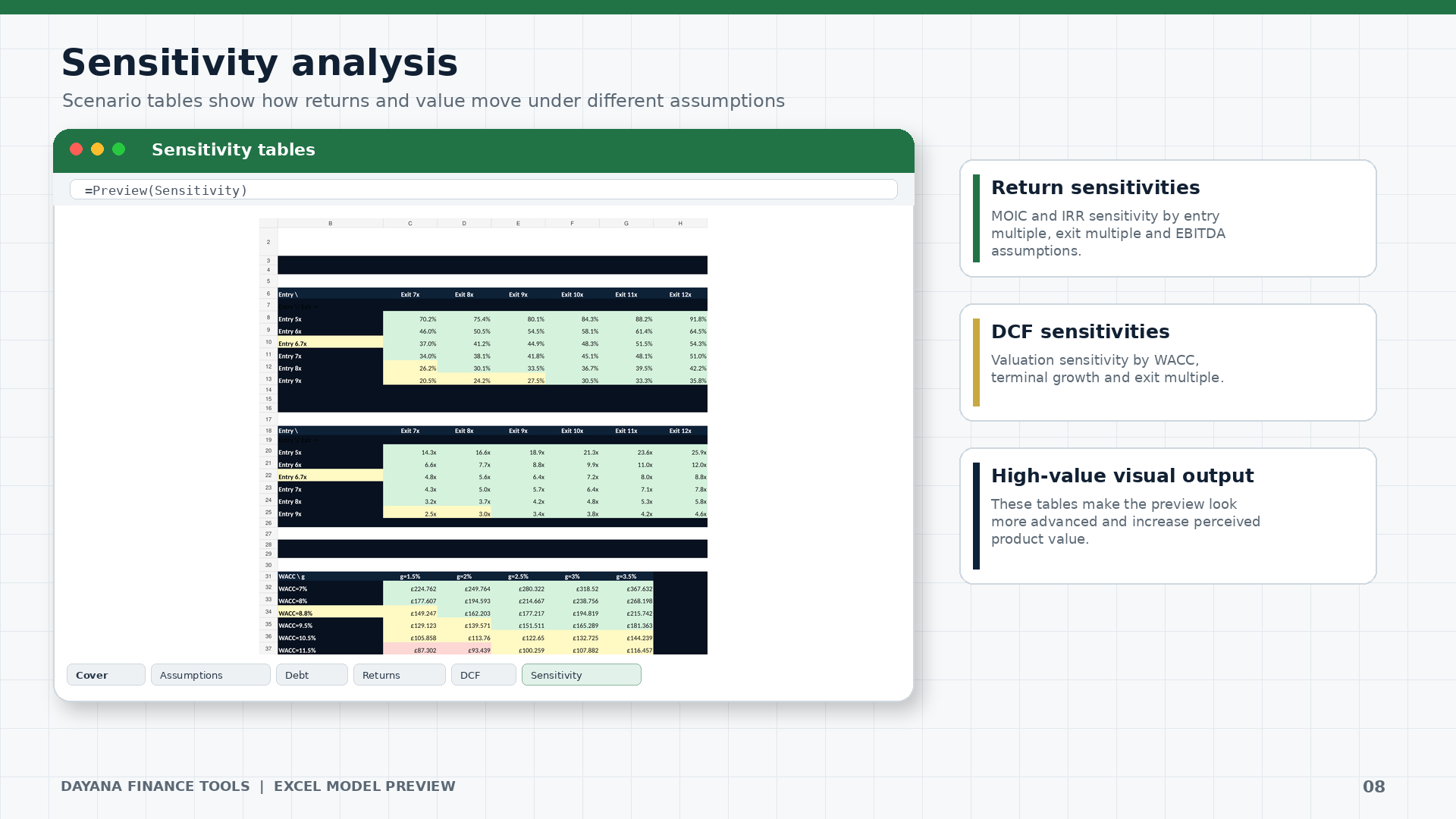

Conduct Dynamic Risk Sensitivities: Build and interpret dual-variable sensitivity tables to evaluate the impact of changing Entry and Exit valuation multiples on Gross/Net IRR and MOIC.

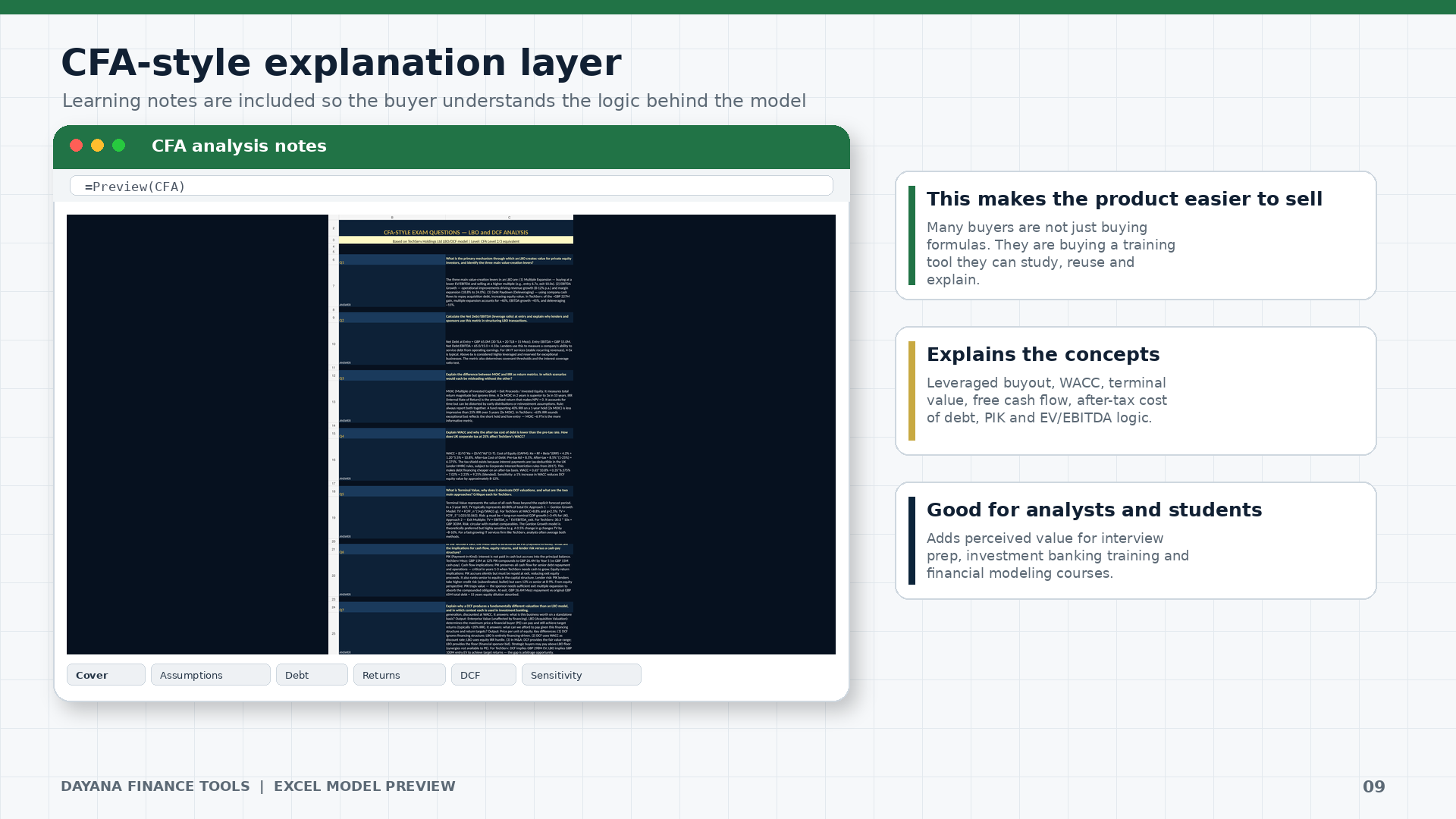

Prepare for Elite Technical Screenings: Accelerate preparation for Private Equity and Investment Banking technical interviews, or master real-world corporate finance applications tested throughout the CFA Level II and III curricula.

Institutional Private Equity & Investment Banking Prep: Perfectly suited for candidates preparing for elite private equity modeling tests, case studies, or investment banking technical interviews that demand multi-tier capital structure modeling.

CFA Level II & III Exam Review: Highly applicable for CFA candidates seeking a concrete, spreadsheet-based application of corporate finance theory, specifically regarding leverage buyouts, debt capacities, and intrinsic valuation differences.

Mid-Market IT Services & Tech Sector Deal Flow: Tailored for corporate development teams, advisors, or financial sponsors evaluating transactions in asset-light, high-operating-leverage industries characterized by recurring revenues (e.g., Managed IT, Cybersecurity, SaaS).

Multi-Tranche Debt Structuring Analyses: Ideal for financial professionals who need to evaluate capital structures that go beyond senior debt, specifically incorporating Bullet Term Loans and Subordinated Mezzanine debt with complex PIK compounding interest.

Sponsor Returns & Exit Multiple Sensitivity Stress-Testing: Best applied when a deal team needs to instantly quantify and visualize how variations in transactional entry pricing versus target exit multiples impact investor Net IRR and MOIC thresholds.

Early-Stage or Venture Capital Valuations: This model is not designed for seed-stage startups, pre-revenue companies, or high-growth tech ventures that lack the steady, predictable cash flows required to secure and service structural acquisition debt.

Asset-Heavy Industries with Distressed Collateral: It is less ideal for heavy industrial, real estate, or asset-backed manufacturing sectors where borrowing capacity depends strictly on liquidation values rather than predictable EBITDA operating margins.

Public Market Comparable Trading Adjustments: This framework does not dynamically scrape or adjust for live, public trading comparables (CoComps) or historical transaction precedents (Precedents), focusing instead strictly on bottom-up DCF and targeted LBO pricing models.

Minority-Stake or Venture Debt Analytics: Not suited for growth equity or venture debt investors seeking to analyze partial minority interest positions, anti-dilution clauses, or convertible preferred equity tranches.

Sovereign Tax Jurisdictions Outside Standard Frameworks: While highly functional, the integrated model assumes a baseline corporate tax environment (e.g., UK corporate tax). It does not dynamically adjust for complex cross-border transfer pricing, double-taxation treaties, or regional tax incentives.