Publication number: ELQ-77001-1

View all versions & Certificate

Further information

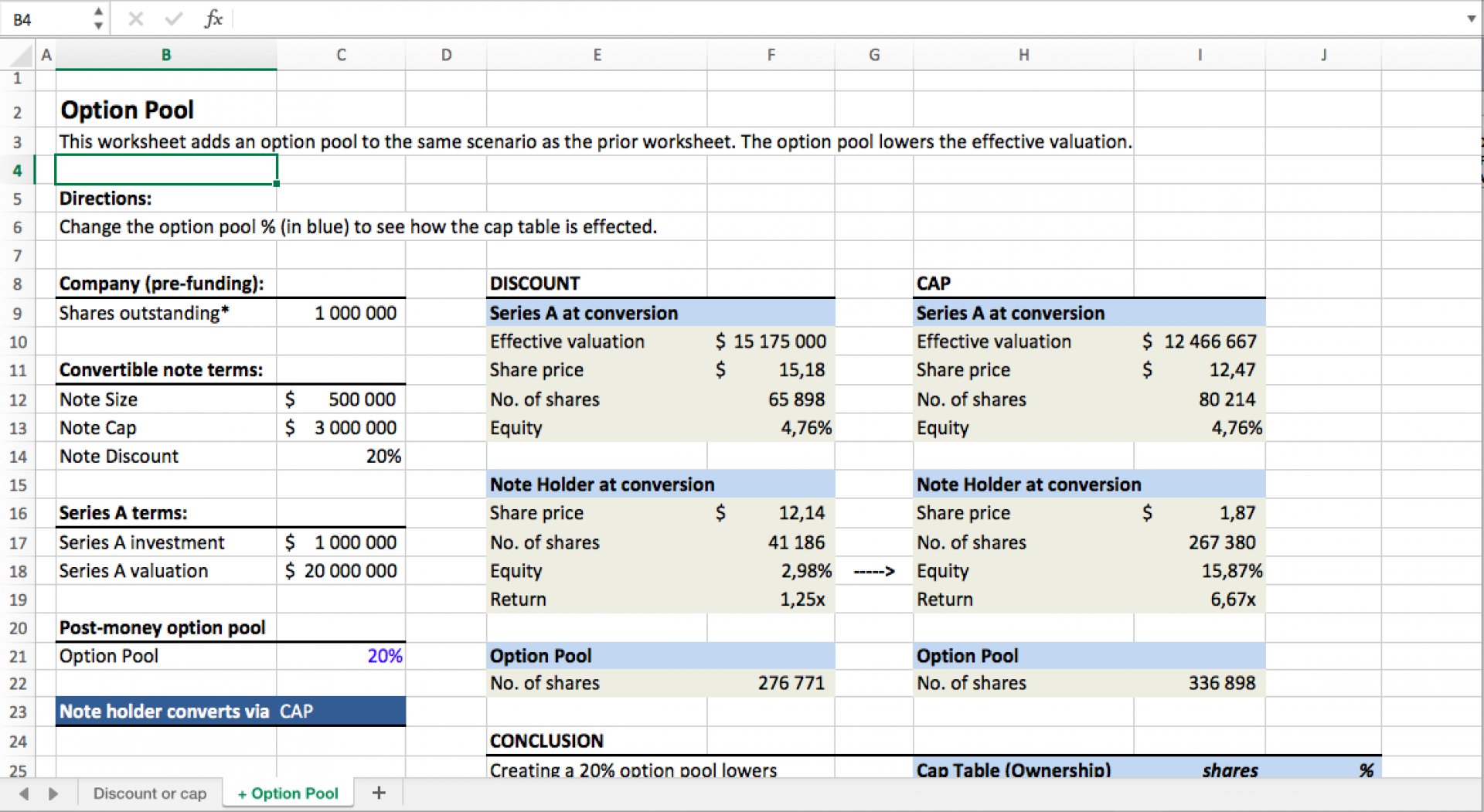

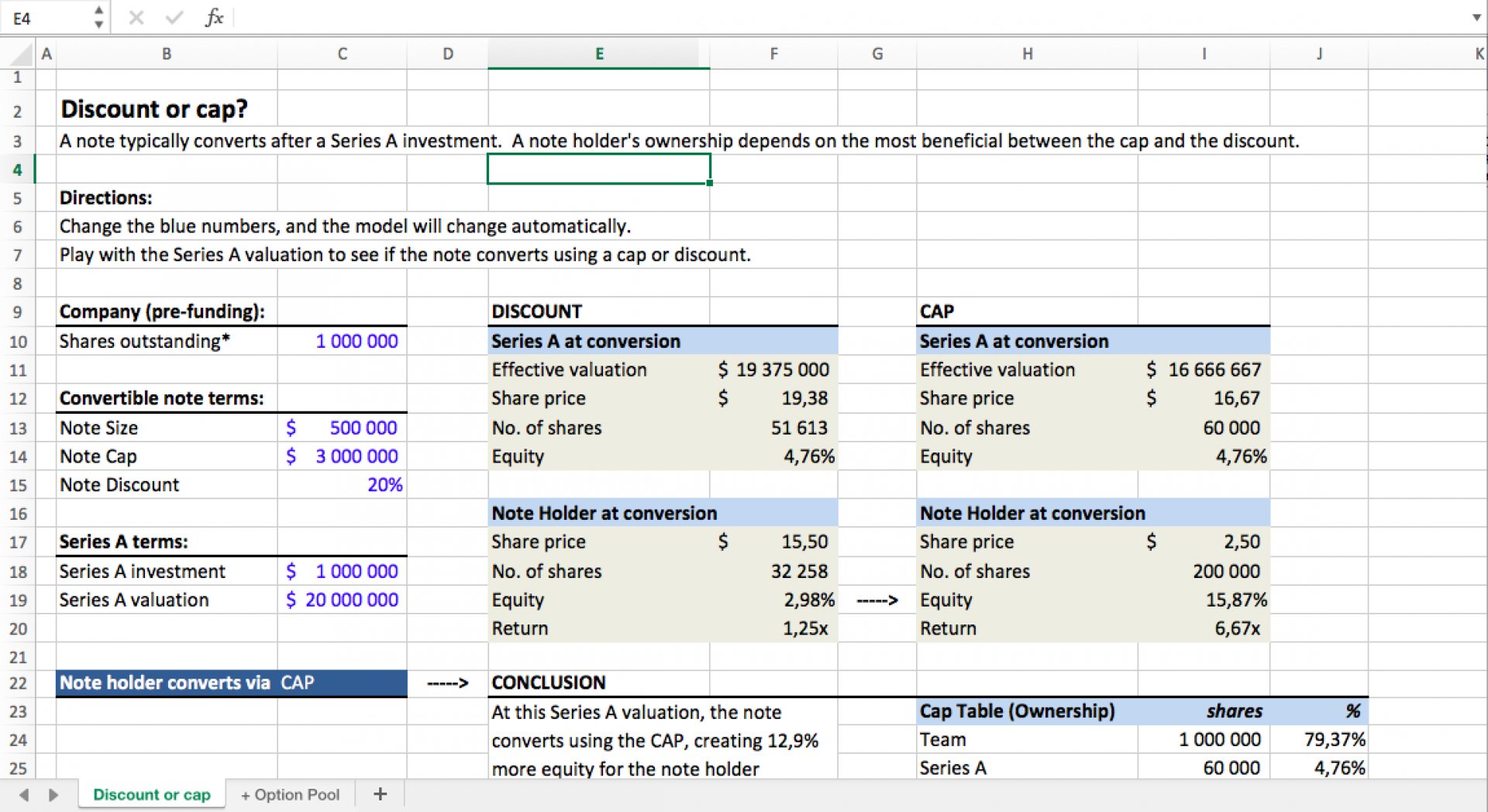

"In this spreadsheet, a note holder converts using whichever of the cap or discount results in a lower share price. But calculating a share price is tricky. This spreadsheet will help take you to the promised land.

For me, the key to calculating share price was learning what “effective valuation” means. "Effective valuation" is sort of like the “enterprise value”, commonly used when talking about publicly traded companies.

Enterprise Value = Market Cap + Debt - Cash

The enterprise value is the amount an acquirer would pay for a company. In this exercise the enterprise value is the “valuation”. But the market cap is what’s used to calculate share price, so we have to solve for it. Assuming there is no cash on the balance sheet, we solve for market cap by subtracting the debt from the enterprise value. The market value of debt depends on if the discount or cap is being used, therefore it’s the “effective valuation”.

Once you have the effective valuation, you can calculate the share price for the Series A investor, and then adjust the share price for the note holder. Click into each cell to study the formula used - it makes more sense visually."

- Raji Bedi, 2012