Originally published: 15/03/2021 08:47

Publication number: ELQ-22156-1

View all versions & Certificate

Publication number: ELQ-22156-1

View all versions & Certificate

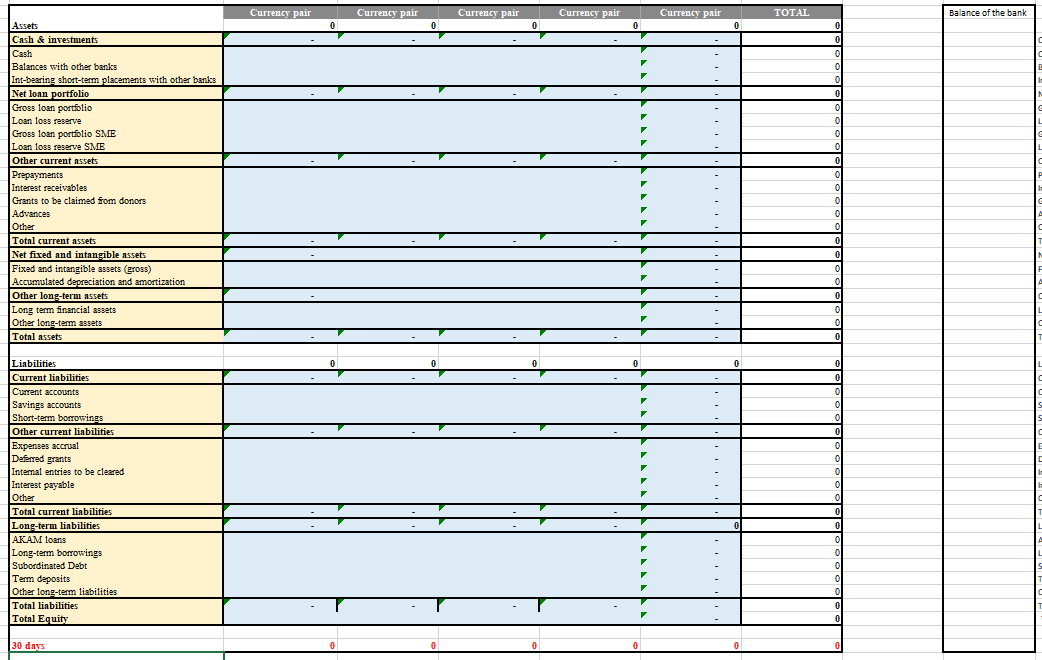

Currency Risk Model for Financial Organizations and Banks

Currency Risk Model for the Commercial Banks and Financial Institutions.

Further information

Mainly for the commercial banks and financial initiations