Originally published: 22/06/2018 08:51

Publication number: ELQ-26701-1

View all versions & Certificate

Publication number: ELQ-26701-1

View all versions & Certificate

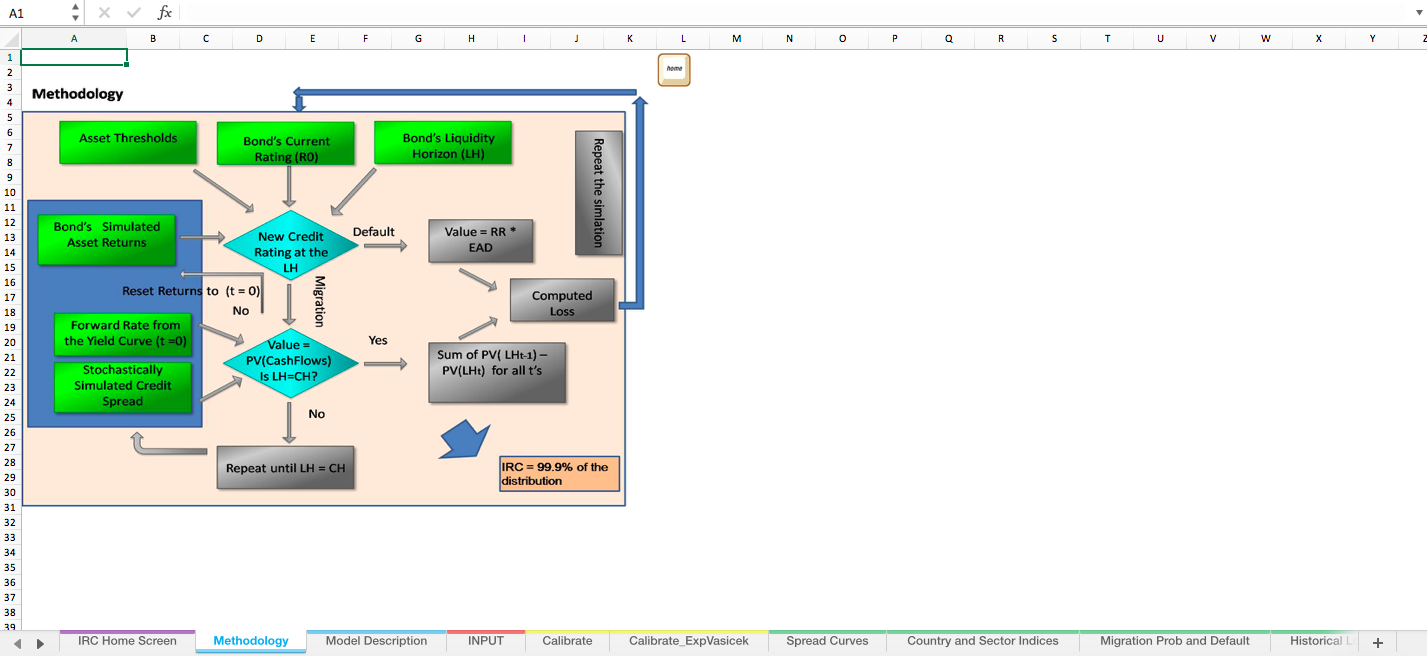

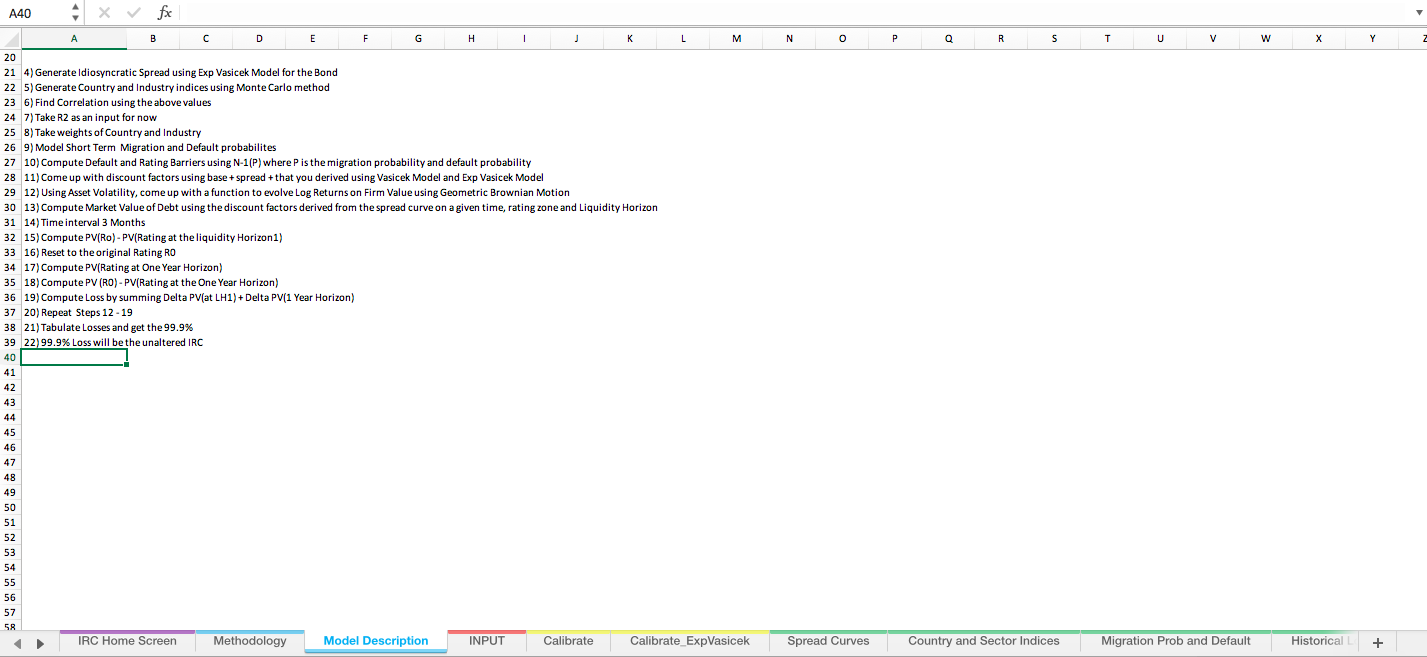

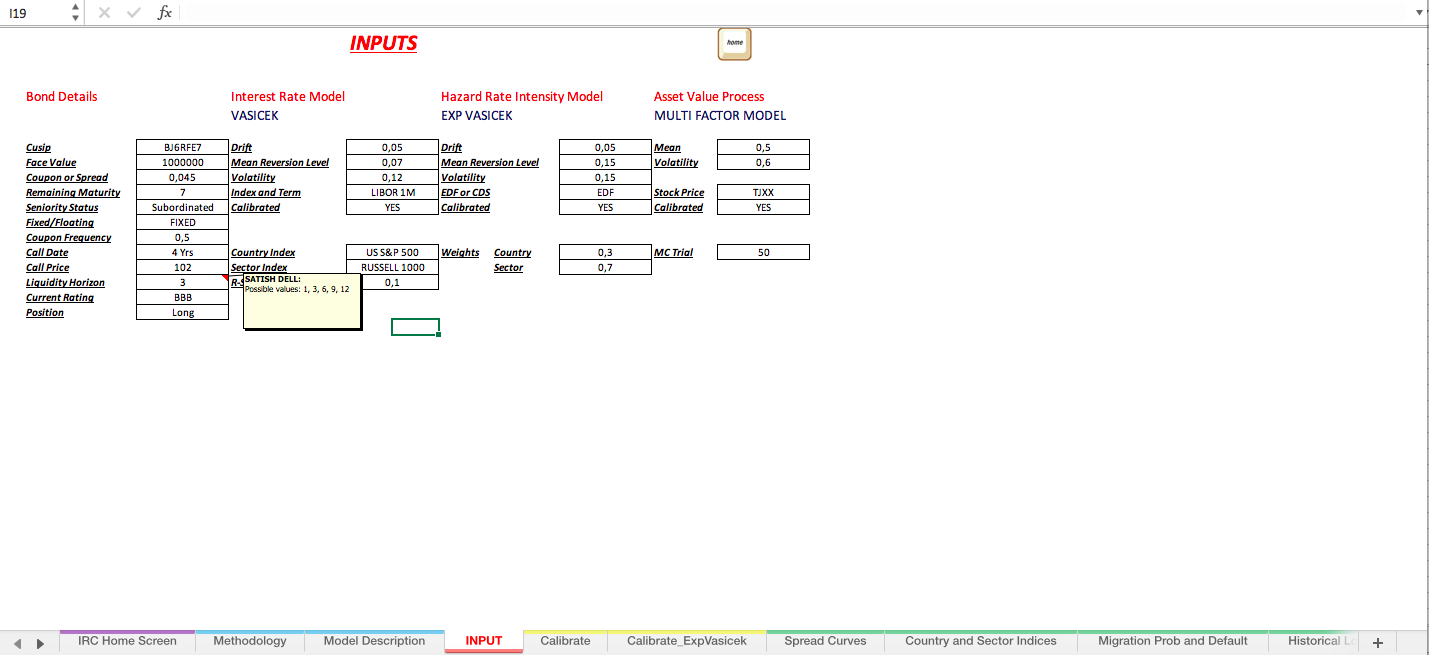

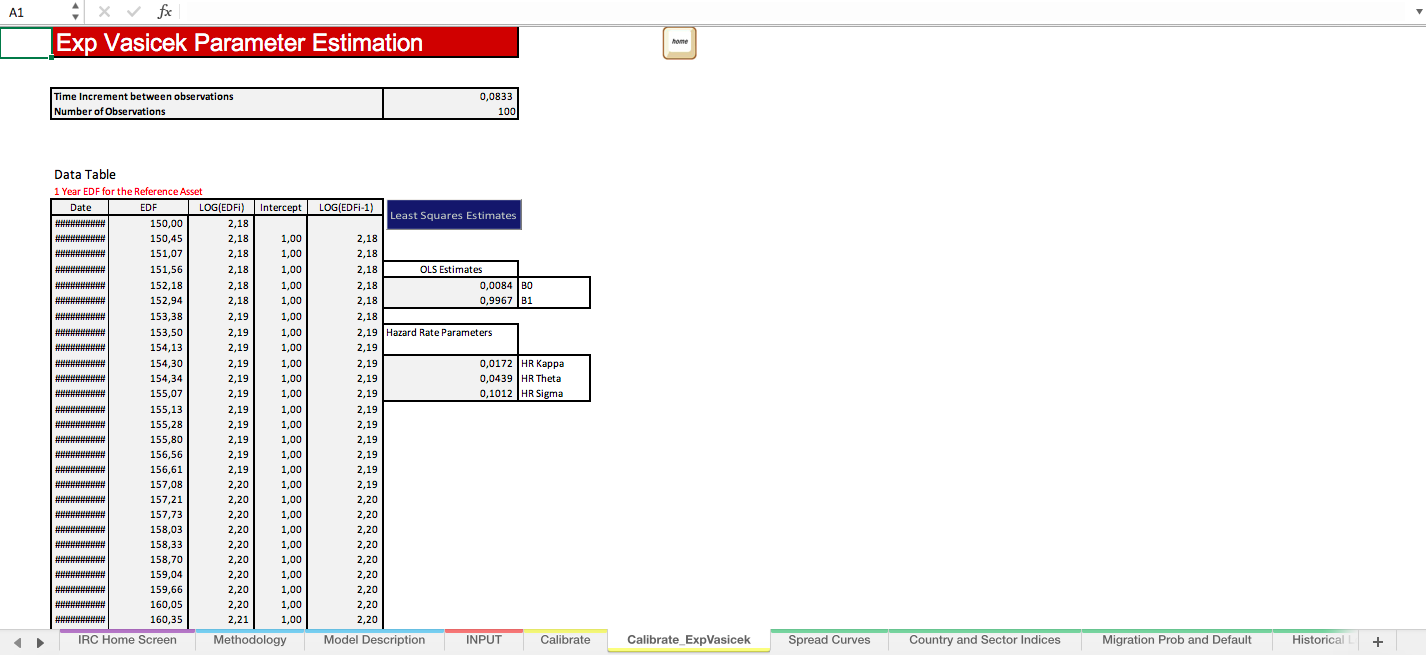

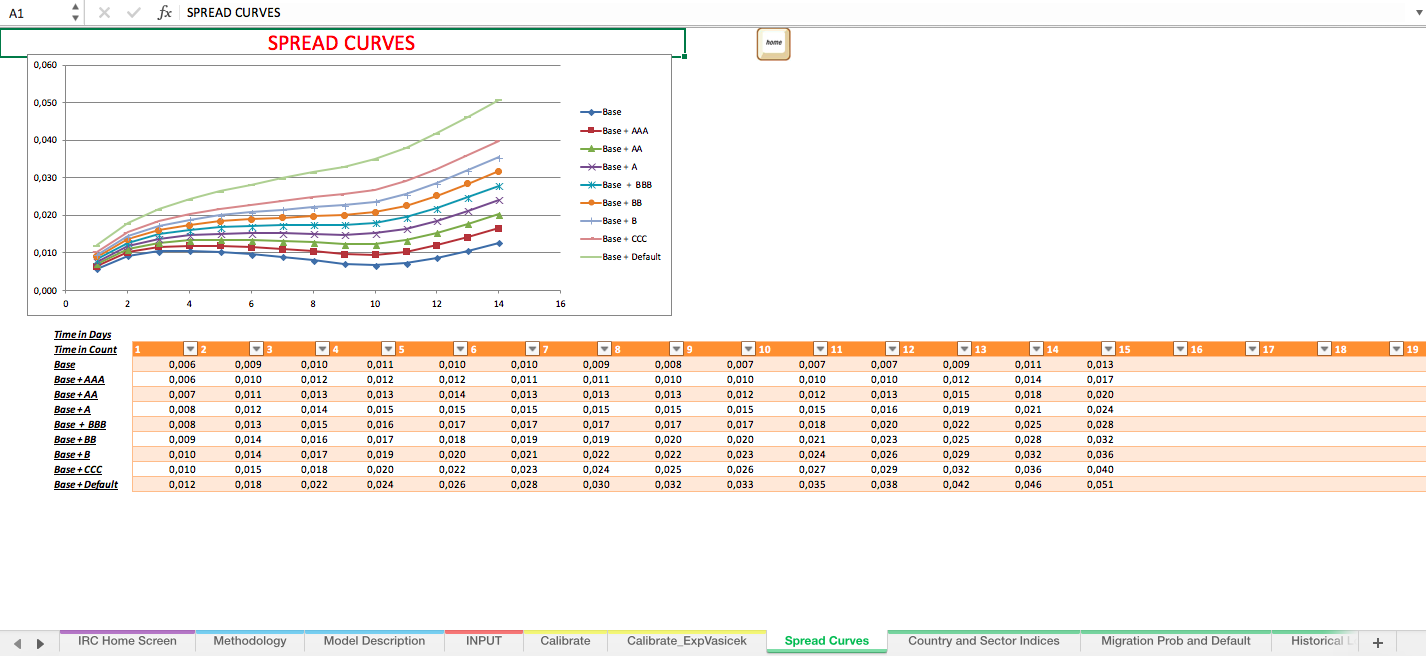

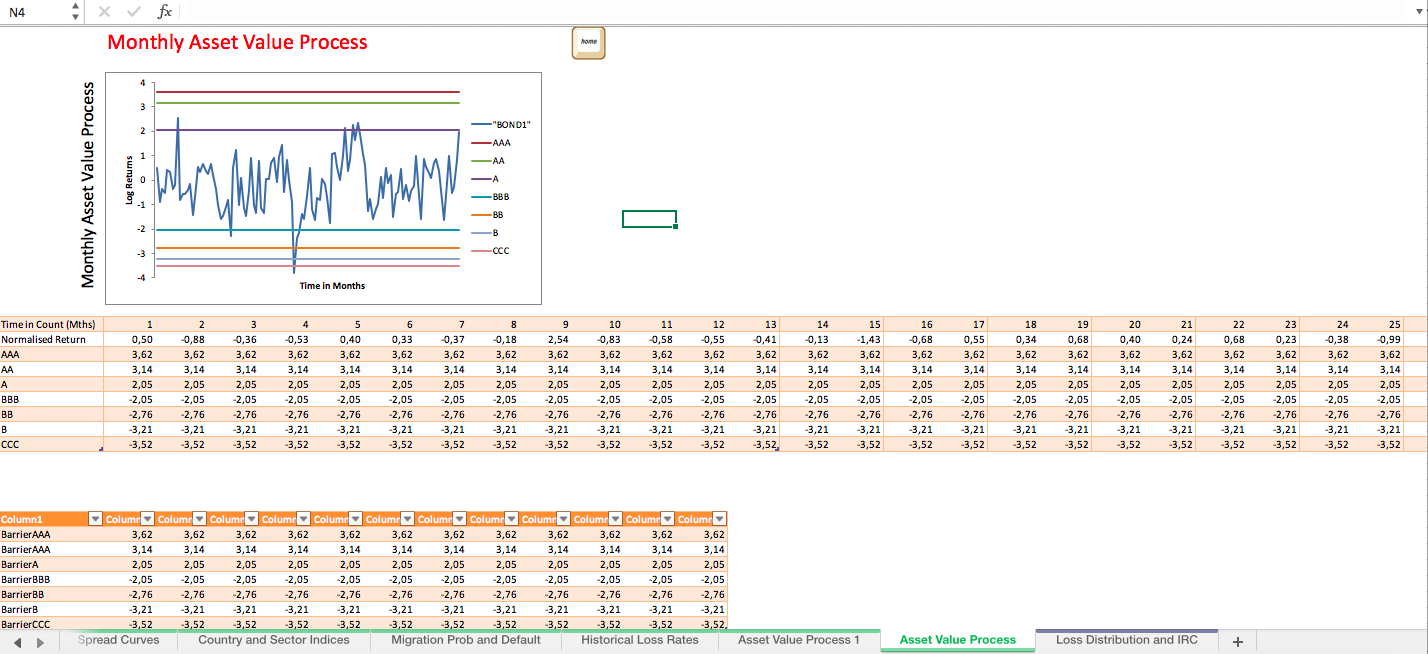

Compute Incremental Risk Charge for a Bond Using Monte Carlo Simulation

A prototype to compute the incremental risk charge (IRC) for a bond position using a novel monte carlo simulation.

Further information

It gives the methodology and a prototype code to compute the incremental risk charge for a single bond position.

It should be programmed to include a portfolio of bonds preferably in a more sophisticated software environment