Originally published: 27/09/2018 07:03

Publication number: ELQ-22592-1

View all versions & Certificate

Publication number: ELQ-22592-1

View all versions & Certificate

"La Doria" Excel Valuation Model

Valuation Model of La Doria (public company)

Description

La Doria group is a leading producer of tomato-based products, fruits, pulses-vegetables, and ready-made sauce product.

The Group is export-focused and principally produces private labels brands for supermarket chains

The company was founded in 1954 by the Ferraioli family, who currently owns c. 63% of the company

The company is:

1. 1st largest producer in Italy of peeled and chopped tomato

2. 1st producer in Italy of preserved pulses

3. 2nd largest producer in Italy of fruit juices and beverages and 1st producer in the private label market segment

4. 1st largest producer in Italy of pasta sauce in the private label segment

5. 1st on the UK market of private label canned tomatoes and preserved pulses

6. 1st on the tomato market in Japan and Australia

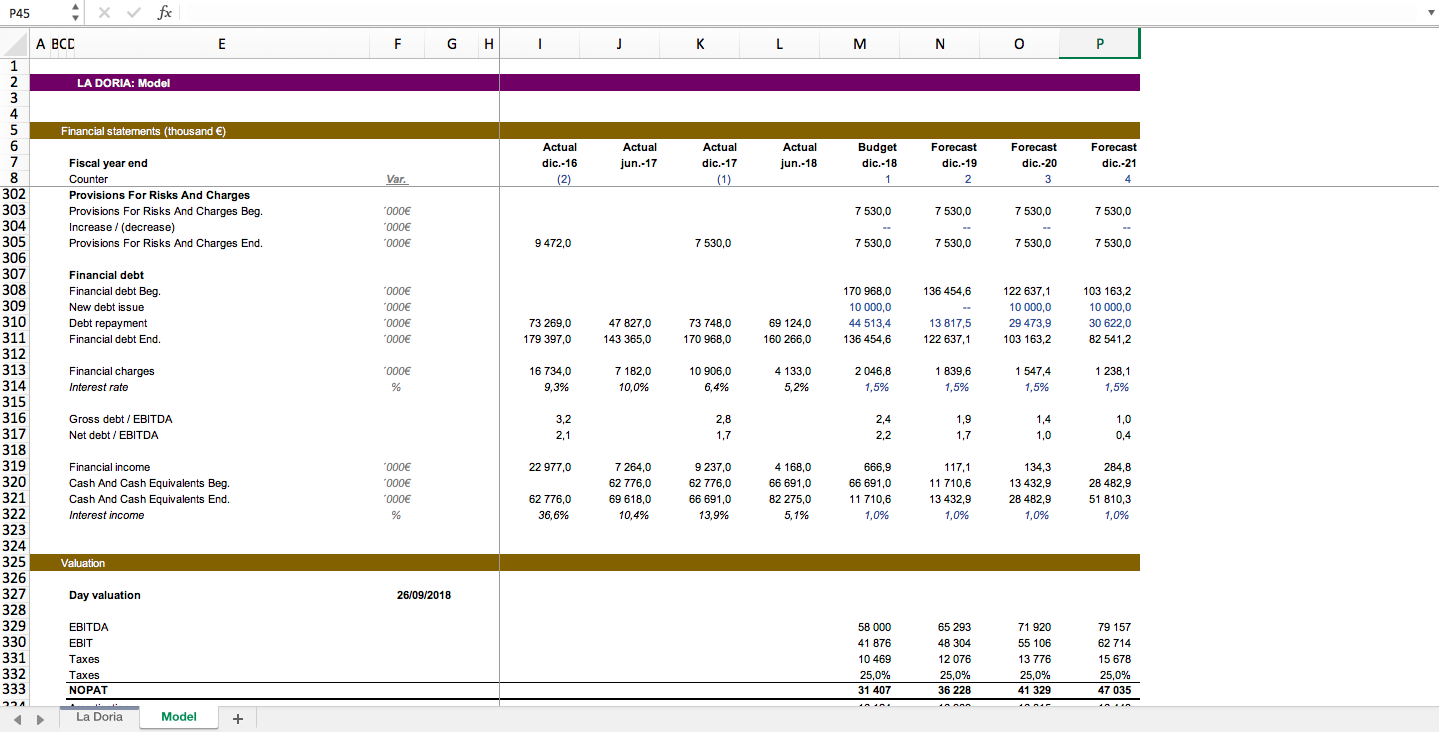

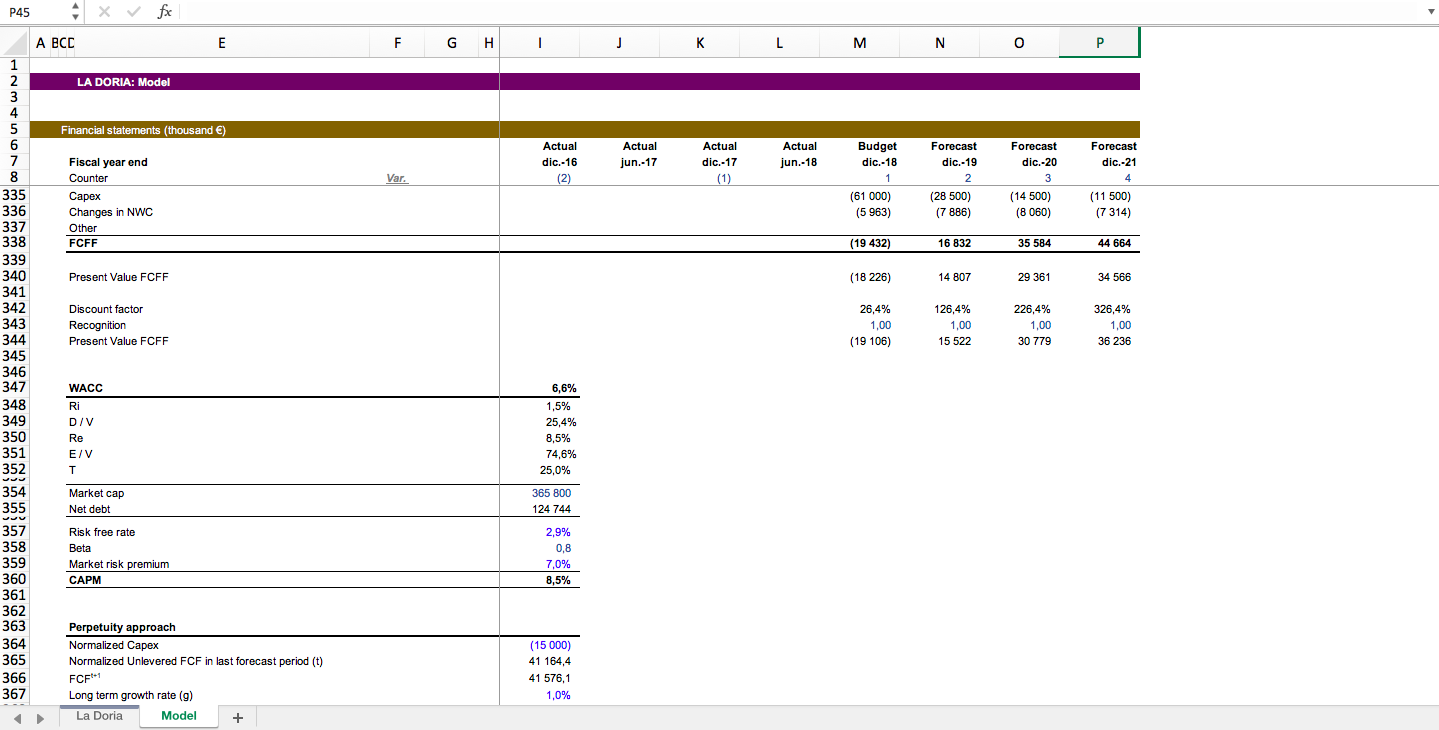

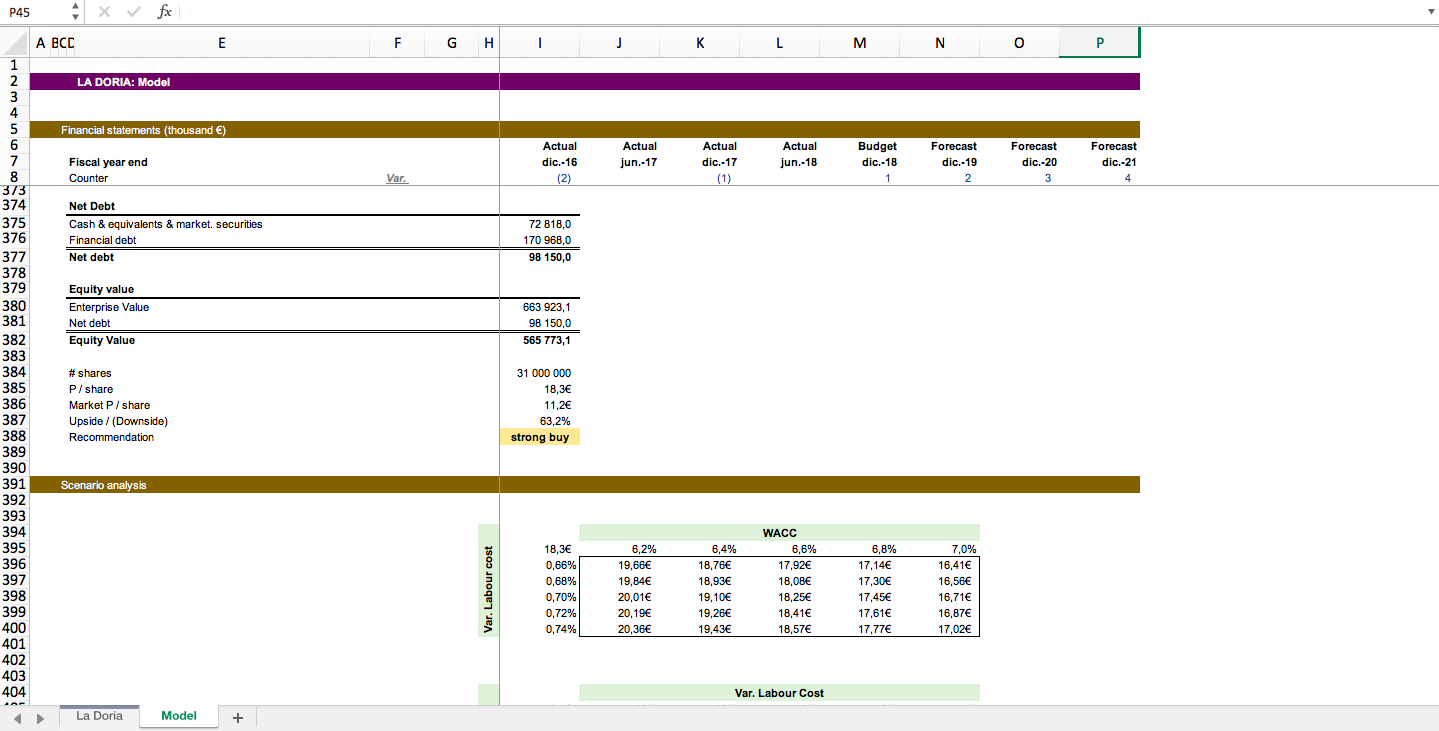

I have tried to assess the fair value of the company according to the DCF model since Banca IMI recently updated their price recommendation

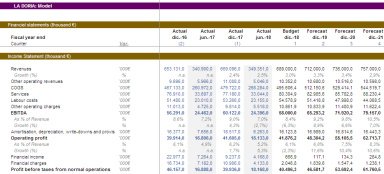

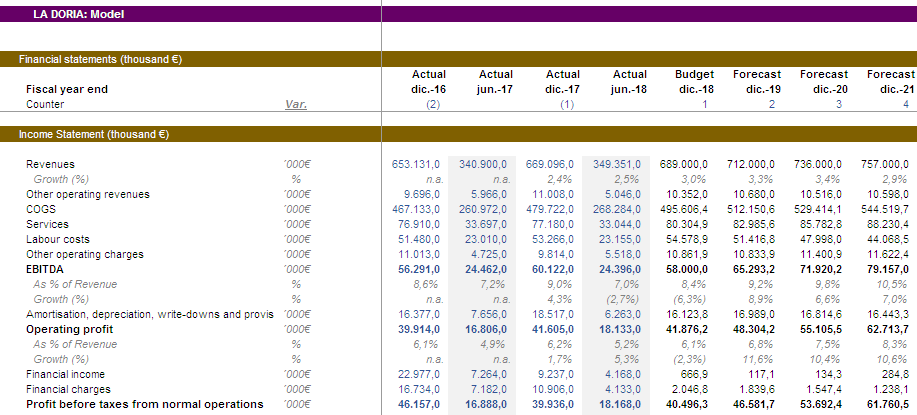

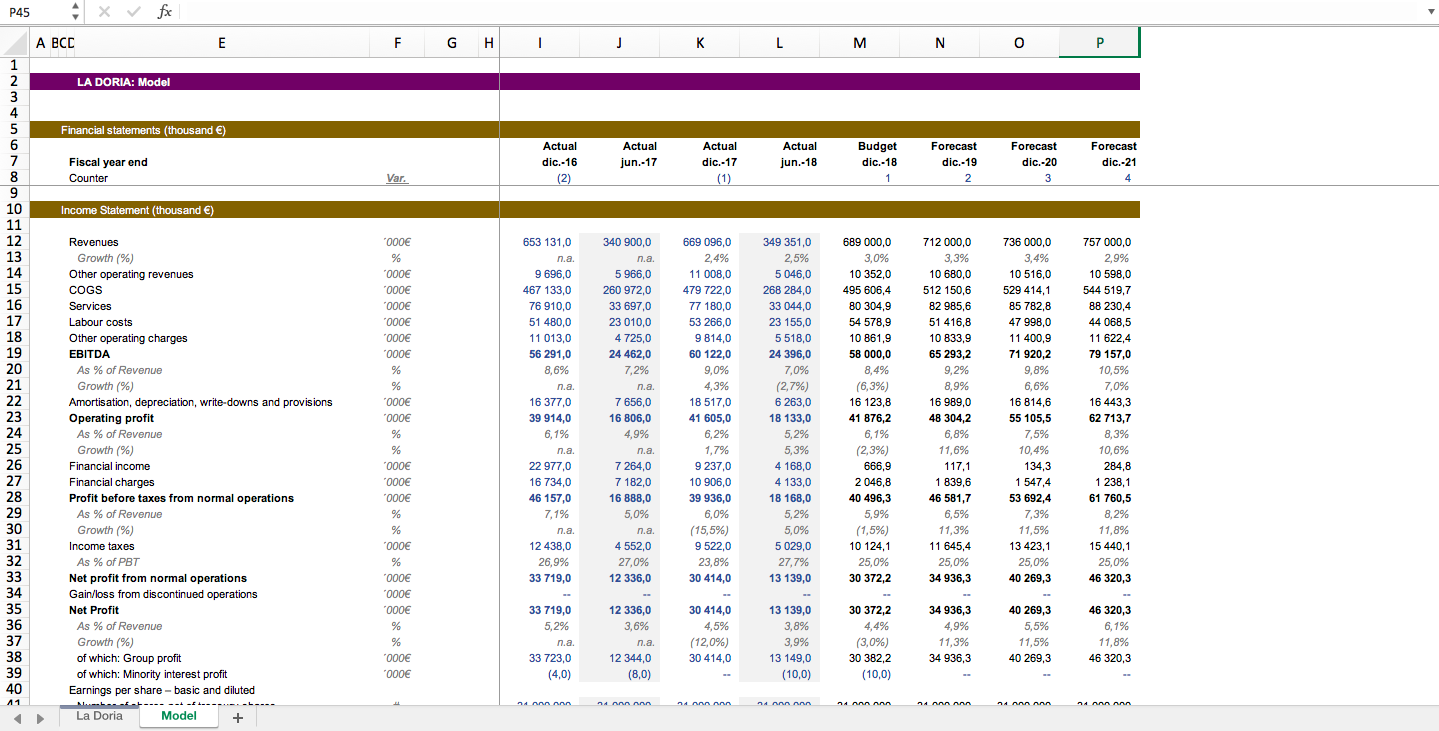

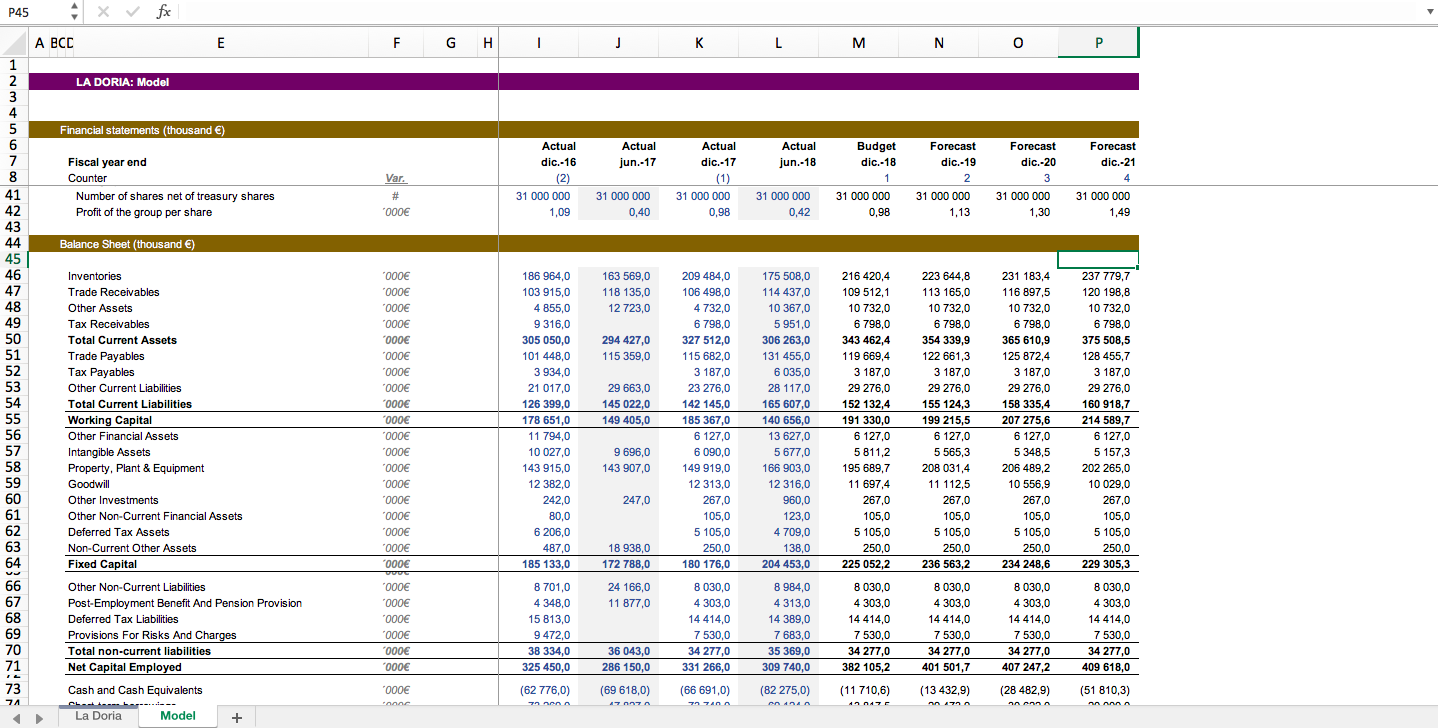

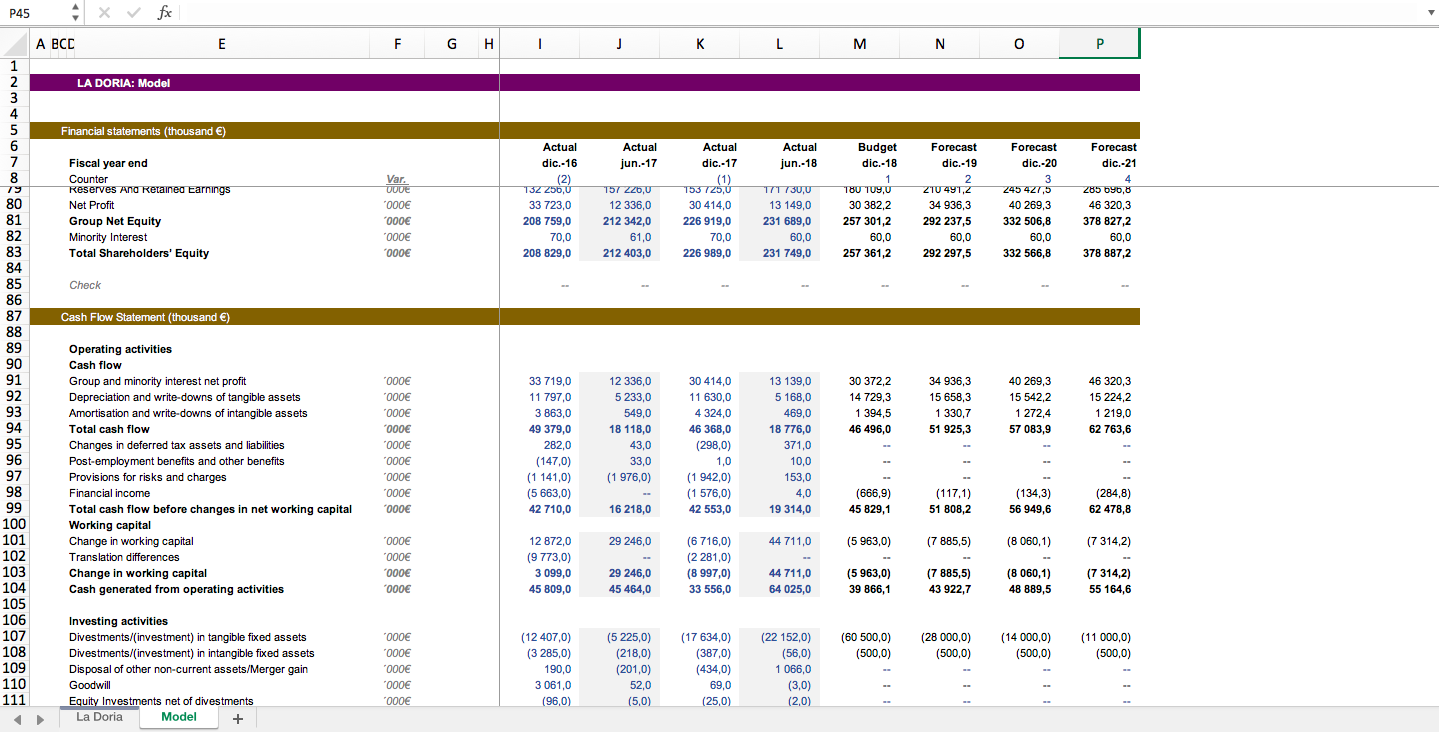

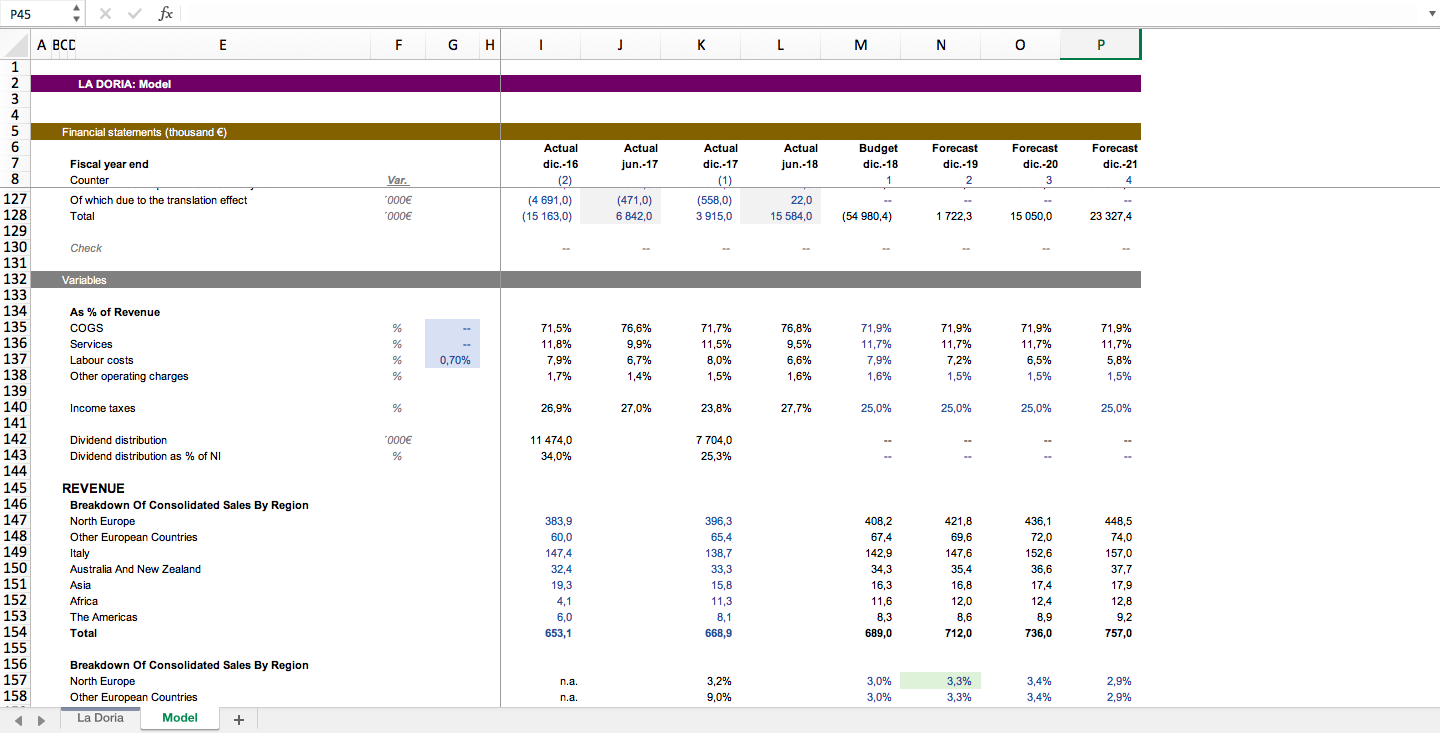

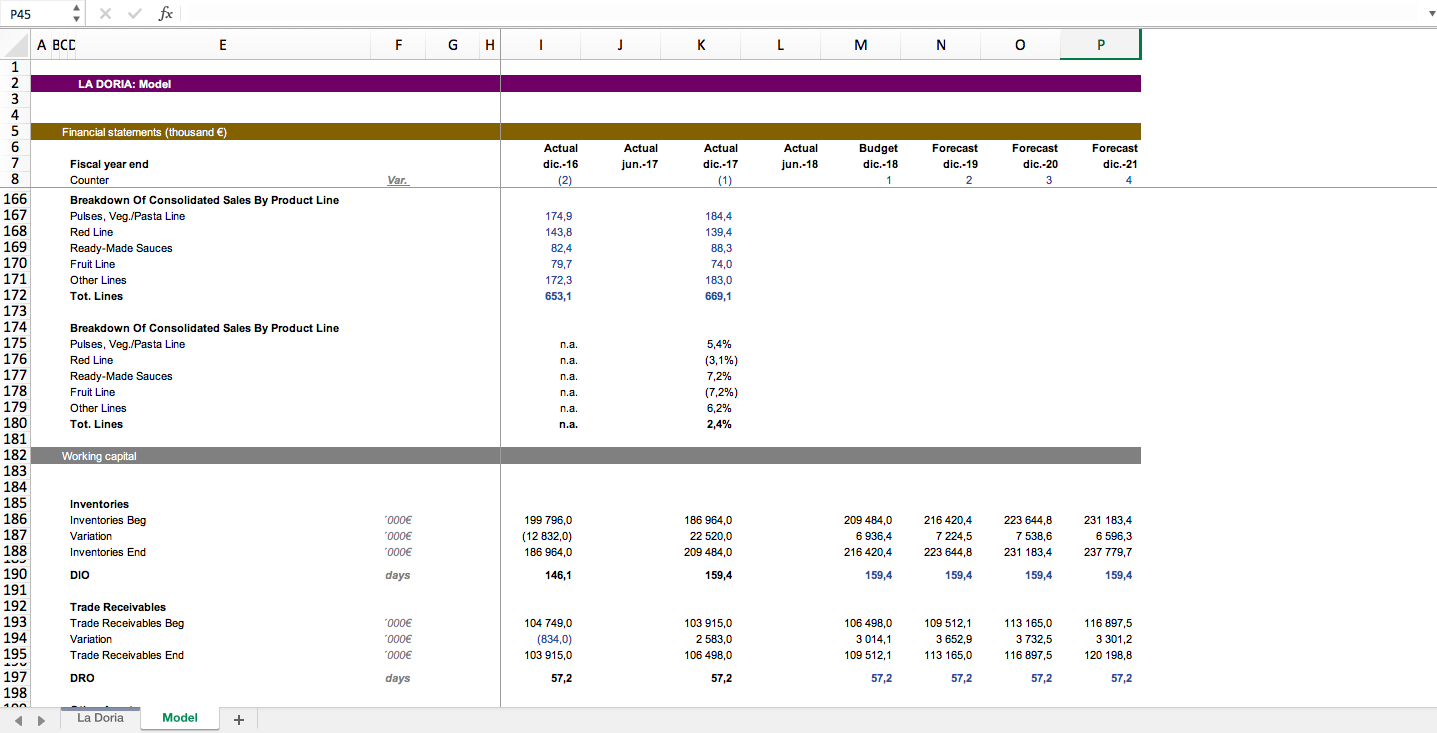

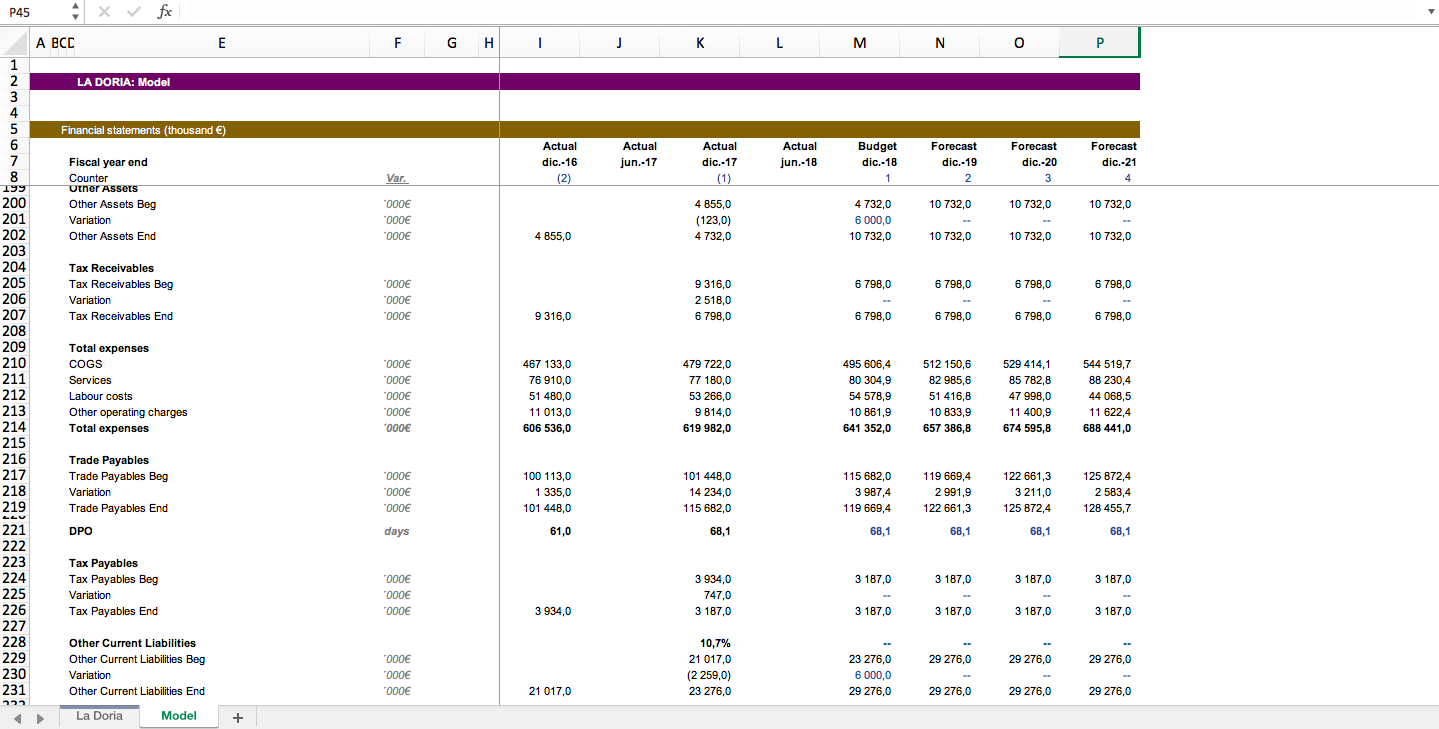

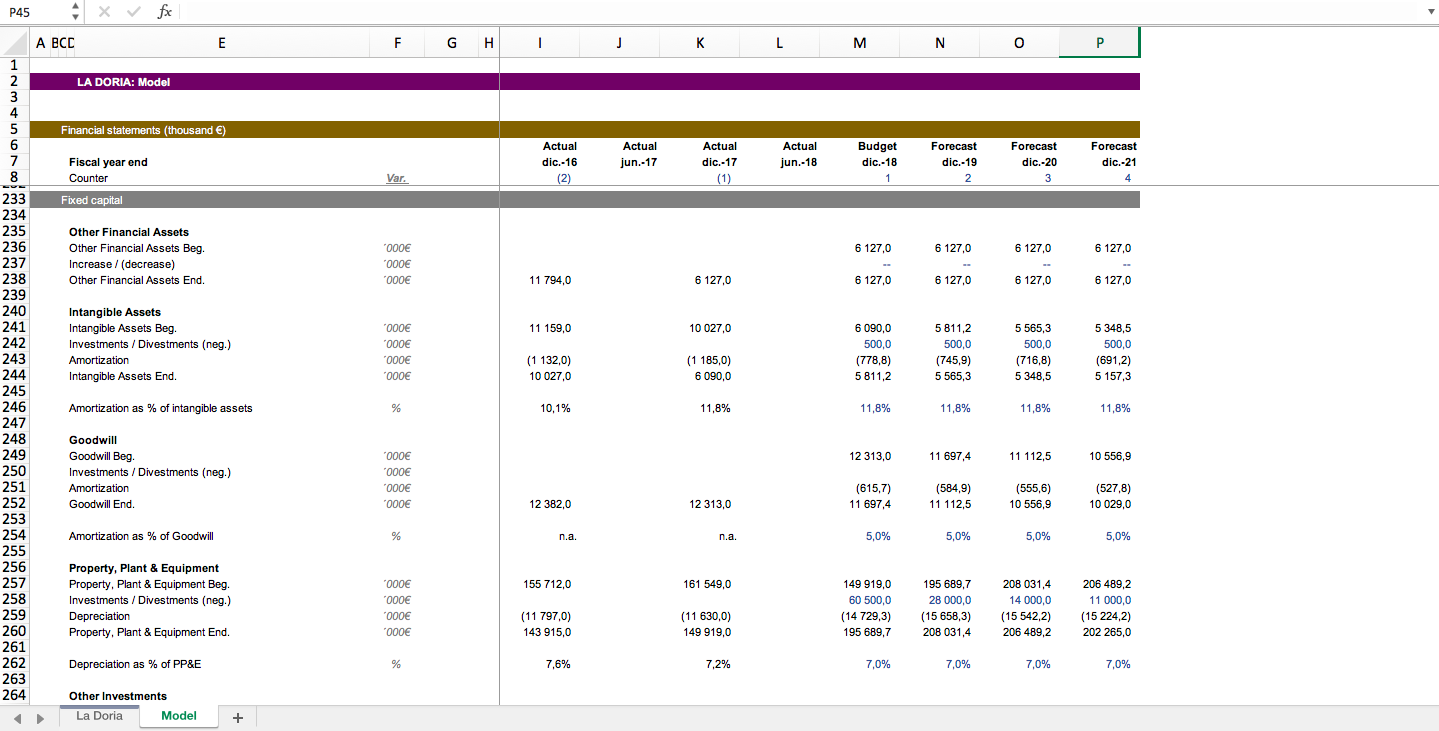

To assess its fair value, I have assumed the company accomplishes its business plan, which implies a growth in revenues of 3.1% (CAGR 2017-2021) and growth in EBITDA of 7.1% (CAGR 2017-2021)

This growth in EBITDA is expected to be achieved thanks to the ambitious investment plan 2018-2021, in which the company aims to invest €115M in optimizing its processes and the closure of one of its facilities in Italy

I have been following the company for 2 years since it seems very interesting to me. The company has above-average operating margins and exports roughly 80% of its production

The company is focused on private labels brands (supermarkets) and its largest market is the UK

The company faces a few challenges in the future:

1. Supermarkets try to squeeze the supplier's margin. La Doria might have an advantage over its competitors since it is more efficient. Besides, the private label's margin is already very tight and supermarkets have little room for reducing it

2. Brexit, as the UK is its largest market. Depending on the Brexit agreement and the fx fluctuation, it might affect the business plan´s company

3. The company aims to change its production mix towards products with higher margins (prepared sauces and juices)

4. Sales to its second largest market (Italy) haven´t recovered yet

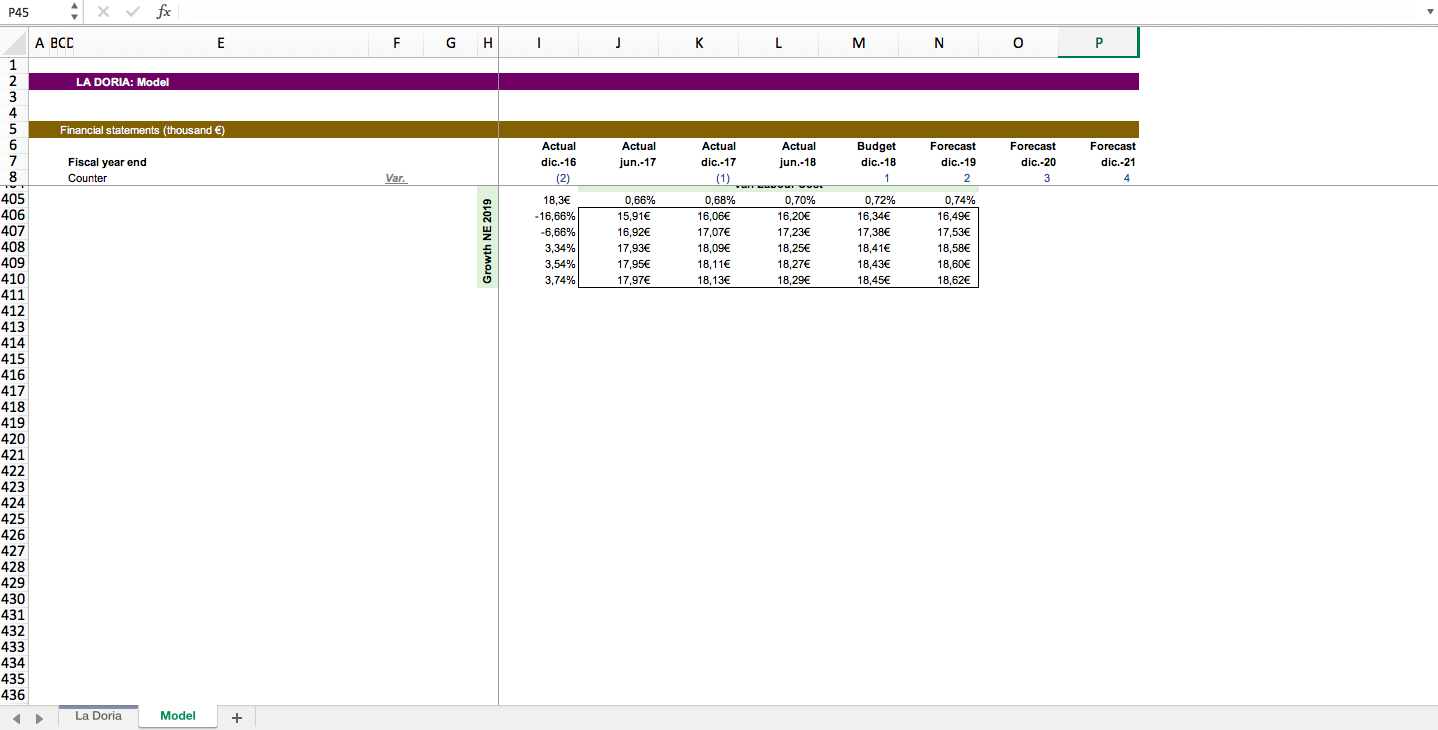

The model would allow to assess different scenarios in revenue growth and there are 2 scenario analysis, in which we assess the price fluctuation according to WACC, Variation labout cost and revenue growth in North European countries in 2019

La Doria group is a leading producer of tomato-based products, fruits, pulses-vegetables, and ready-made sauce product.

The Group is export-focused and principally produces private labels brands for supermarket chains

The company was founded in 1954 by the Ferraioli family, who currently owns c. 63% of the company

The company is:

1. 1st largest producer in Italy of peeled and chopped tomato

2. 1st producer in Italy of preserved pulses

3. 2nd largest producer in Italy of fruit juices and beverages and 1st producer in the private label market segment

4. 1st largest producer in Italy of pasta sauce in the private label segment

5. 1st on the UK market of private label canned tomatoes and preserved pulses

6. 1st on the tomato market in Japan and Australia

I have tried to assess the fair value of the company according to the DCF model since Banca IMI recently updated their price recommendation

To assess its fair value, I have assumed the company accomplishes its business plan, which implies a growth in revenues of 3.1% (CAGR 2017-2021) and growth in EBITDA of 7.1% (CAGR 2017-2021)

This growth in EBITDA is expected to be achieved thanks to the ambitious investment plan 2018-2021, in which the company aims to invest €115M in optimizing its processes and the closure of one of its facilities in Italy

I have been following the company for 2 years since it seems very interesting to me. The company has above-average operating margins and exports roughly 80% of its production

The company is focused on private labels brands (supermarkets) and its largest market is the UK

The company faces a few challenges in the future:

1. Supermarkets try to squeeze the supplier's margin. La Doria might have an advantage over its competitors since it is more efficient. Besides, the private label's margin is already very tight and supermarkets have little room for reducing it

2. Brexit, as the UK is its largest market. Depending on the Brexit agreement and the fx fluctuation, it might affect the business plan´s company

3. The company aims to change its production mix towards products with higher margins (prepared sauces and juices)

4. Sales to its second largest market (Italy) haven´t recovered yet

The model would allow to assess different scenarios in revenue growth and there are 2 scenario analysis, in which we assess the price fluctuation according to WACC, Variation labout cost and revenue growth in North European countries in 2019

This Best Practice includes

1 Excel

Further information

Analysis of the business plan and valuation of the company