Publication number: ELQ-30210-1

View all versions & Certificate

Biotech M&A Model (Excel) — Merck/Pandion $1.85bn Deal Teardown | rNPV · Football Field · ASC 805

A fully-worked teardown of Merck's $1.85bn Pandion acquisition: 17 tabs, 751 live formulas, rNPV, football field & ASC 805. A real deal, not a template.

MBA · I build institutional-grade M&A & valuation models — biotech/healthcare deal teardowns (rNPV, accretion/dilution, football field)Follow

Further information

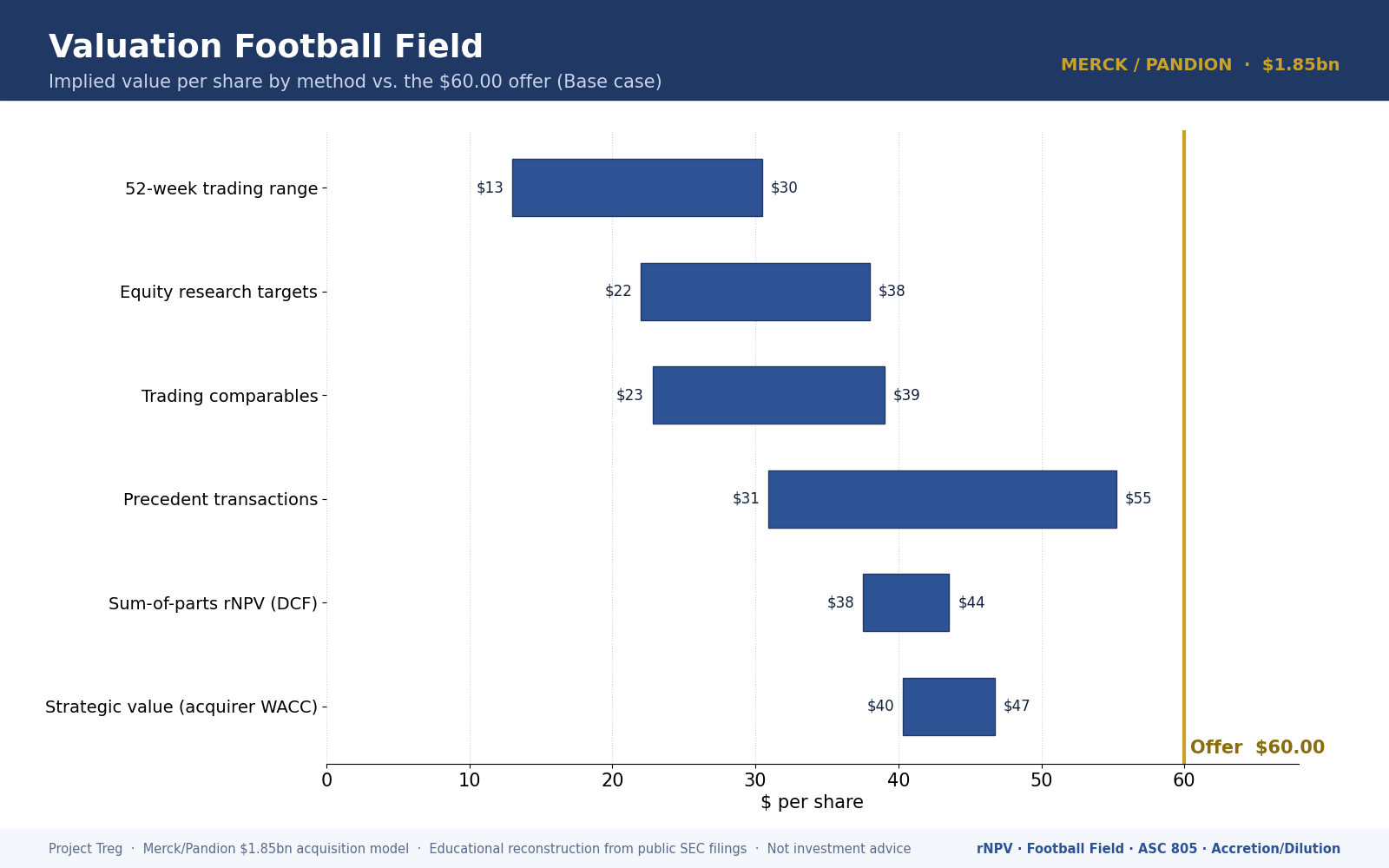

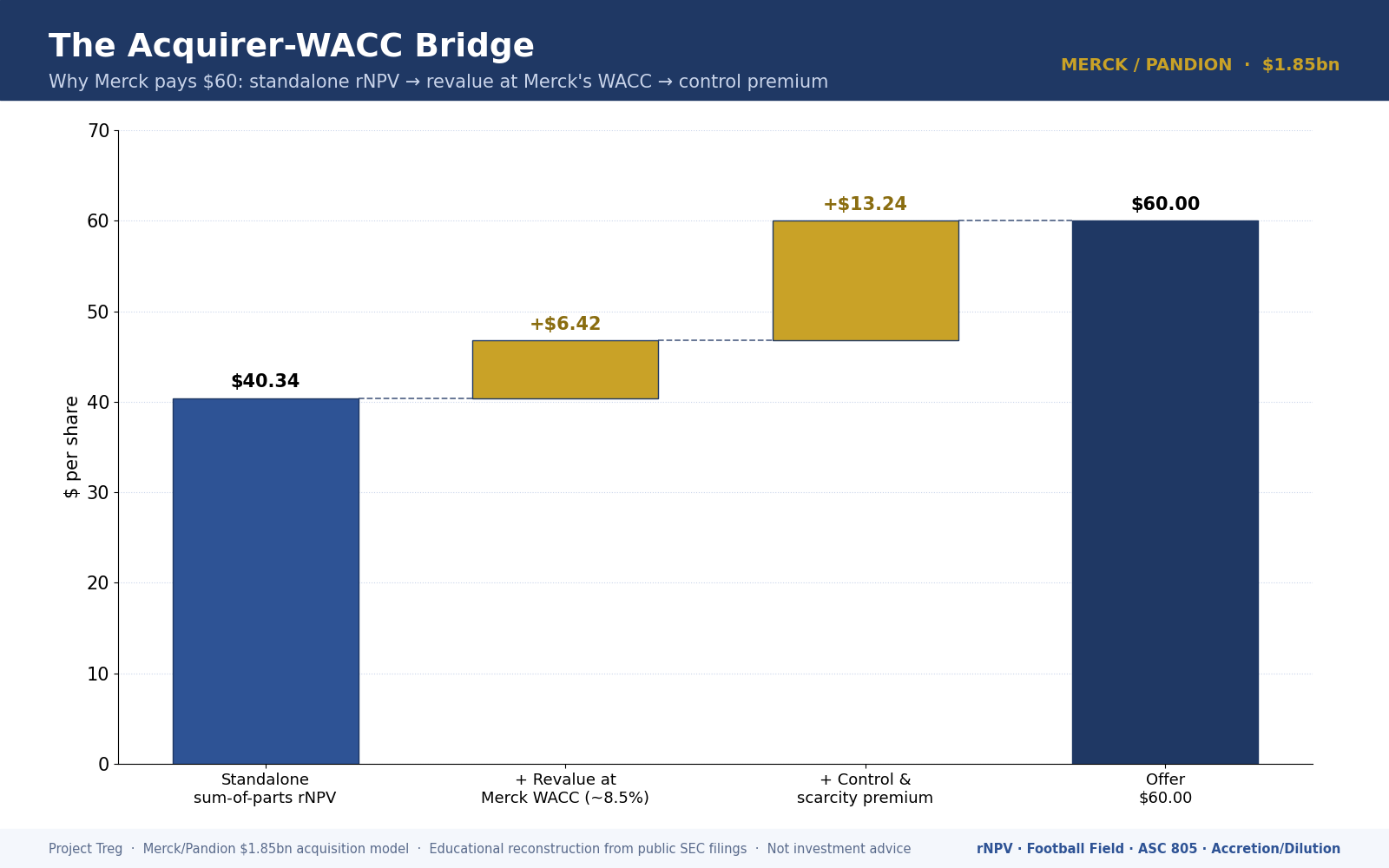

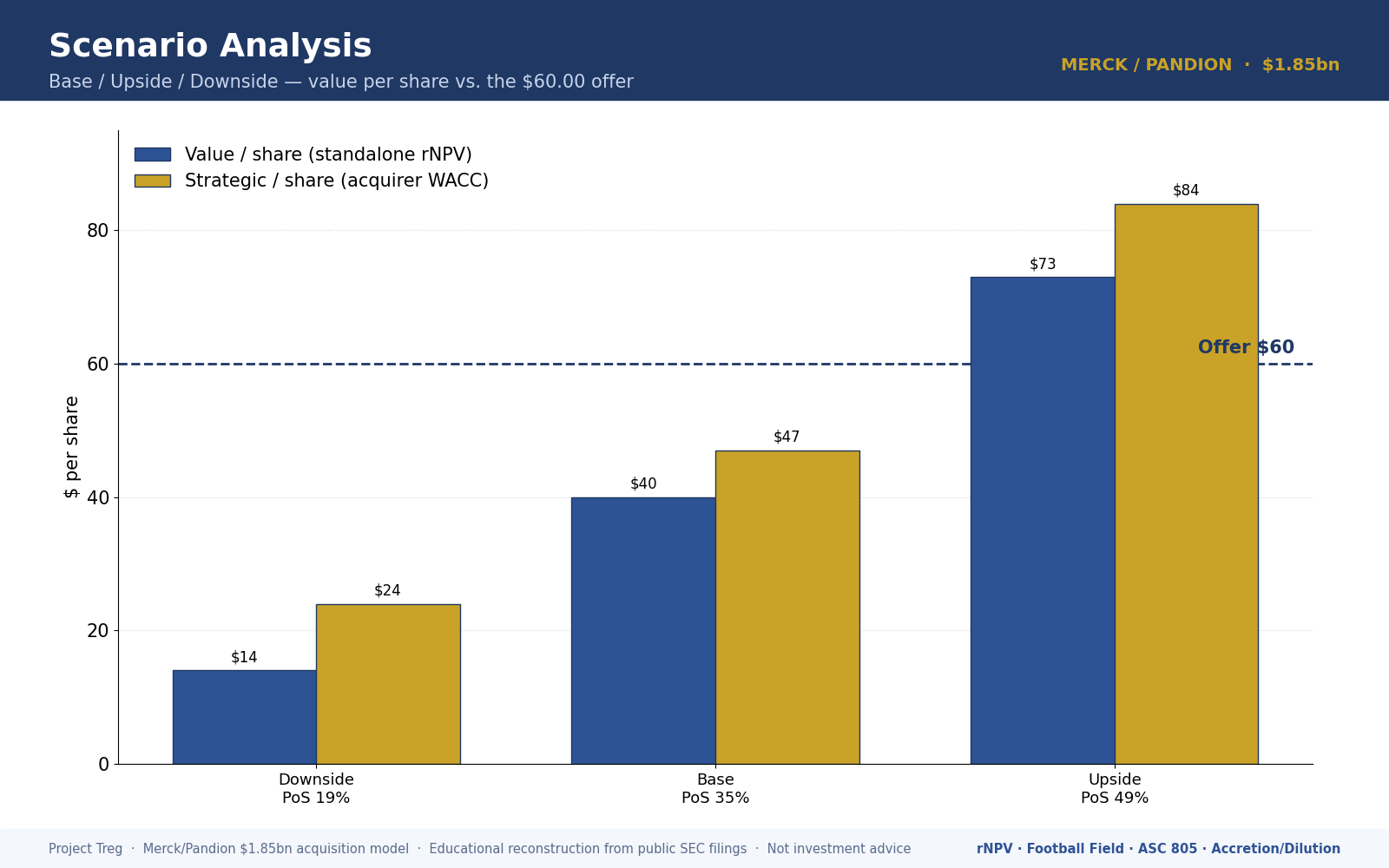

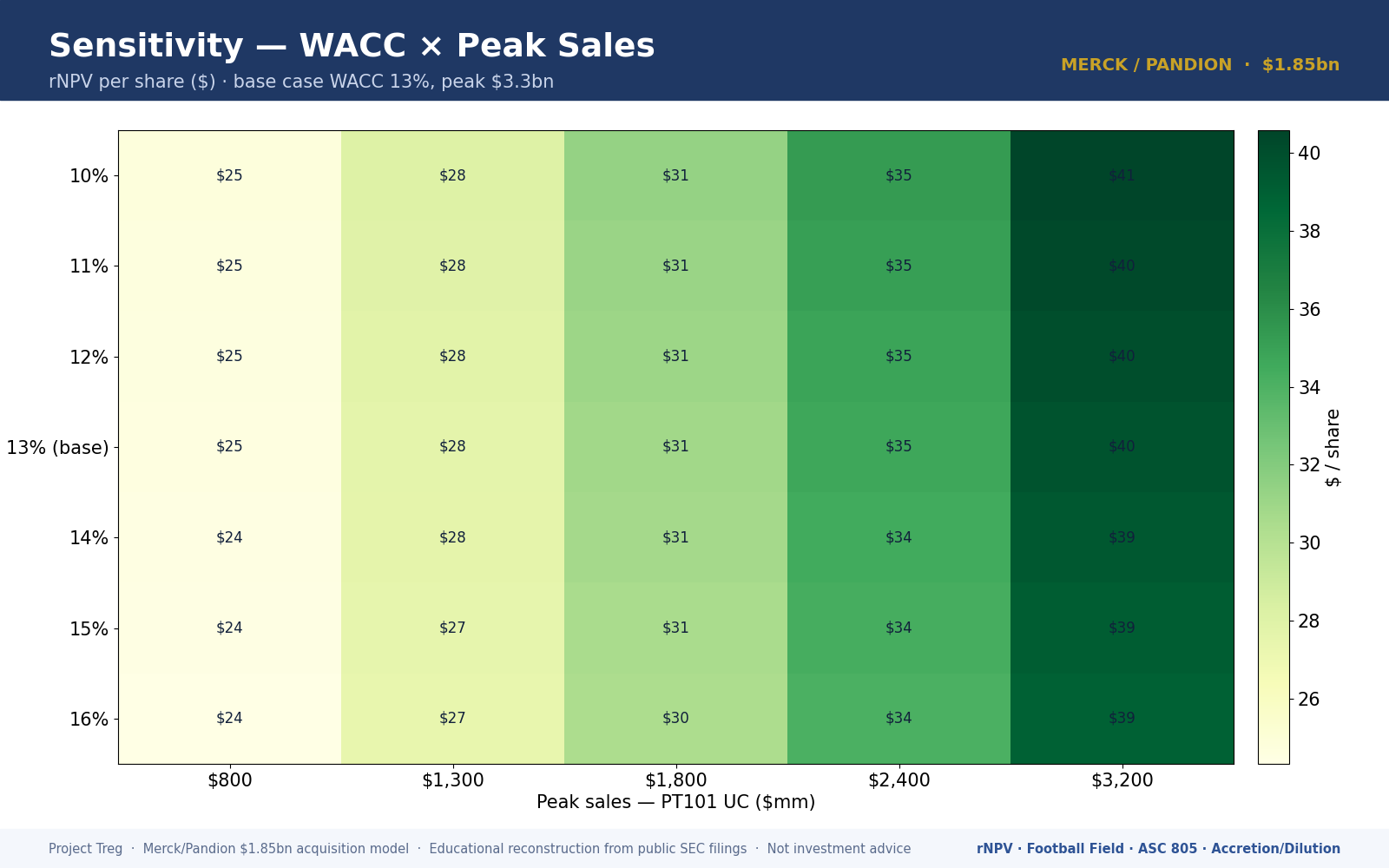

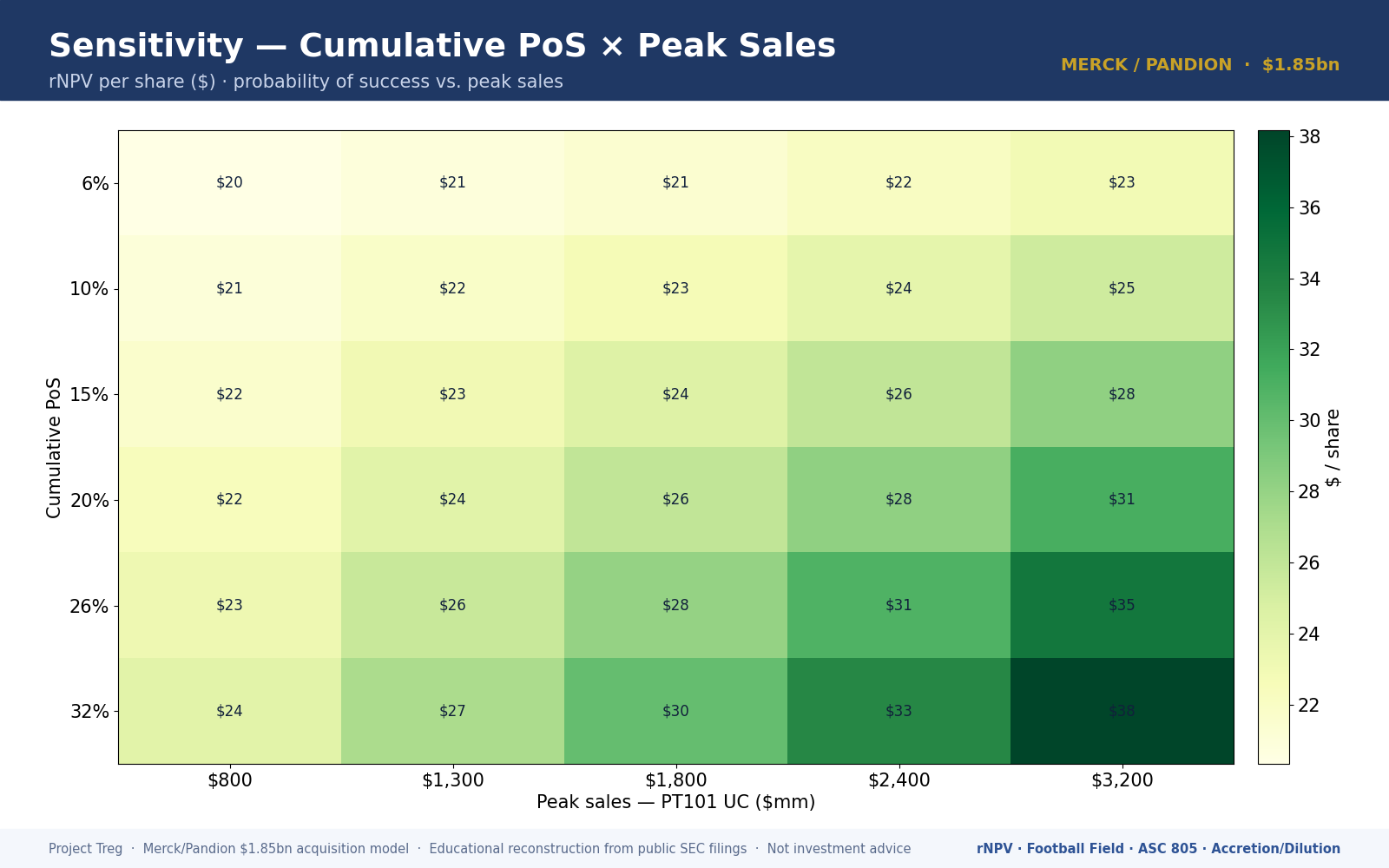

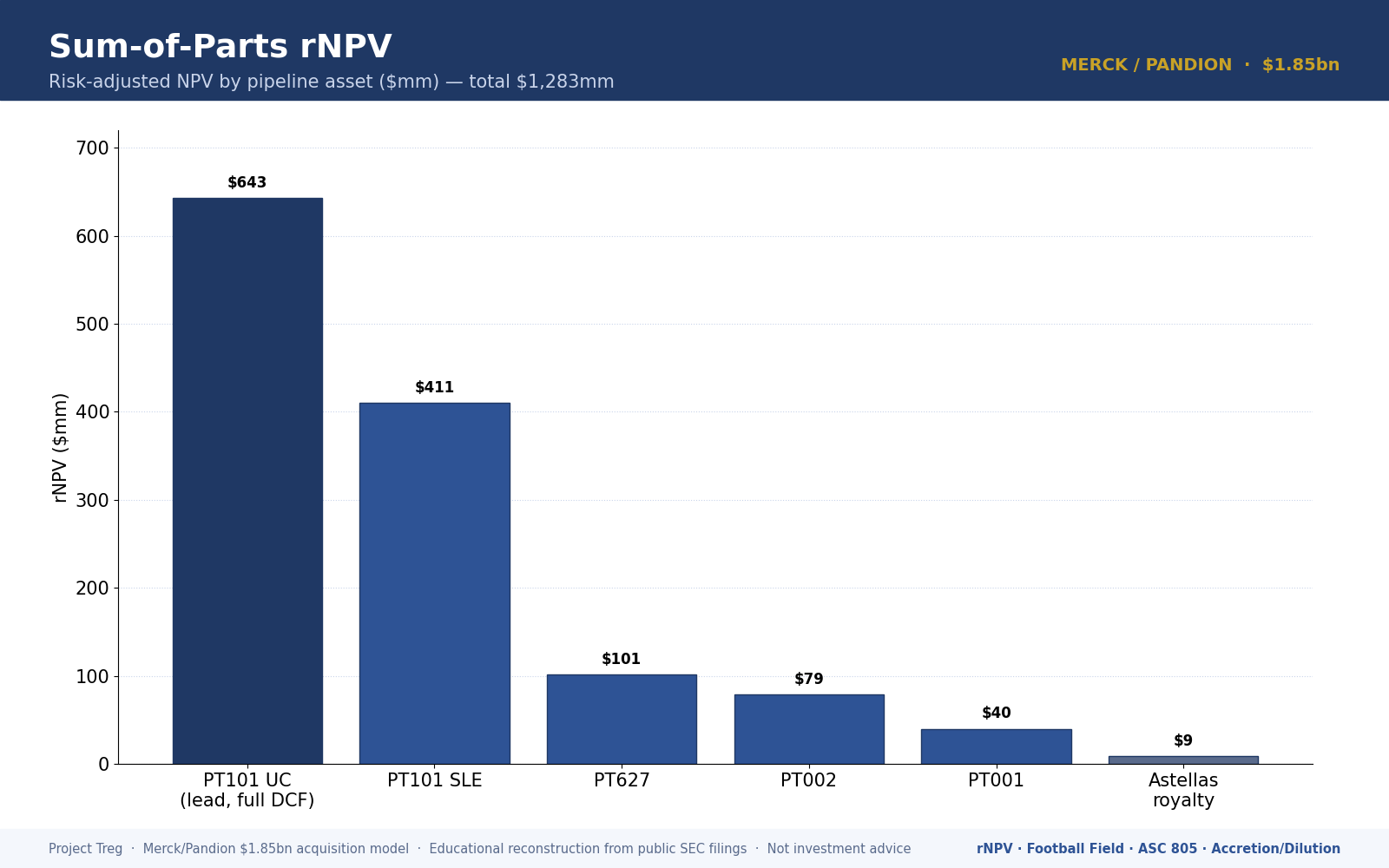

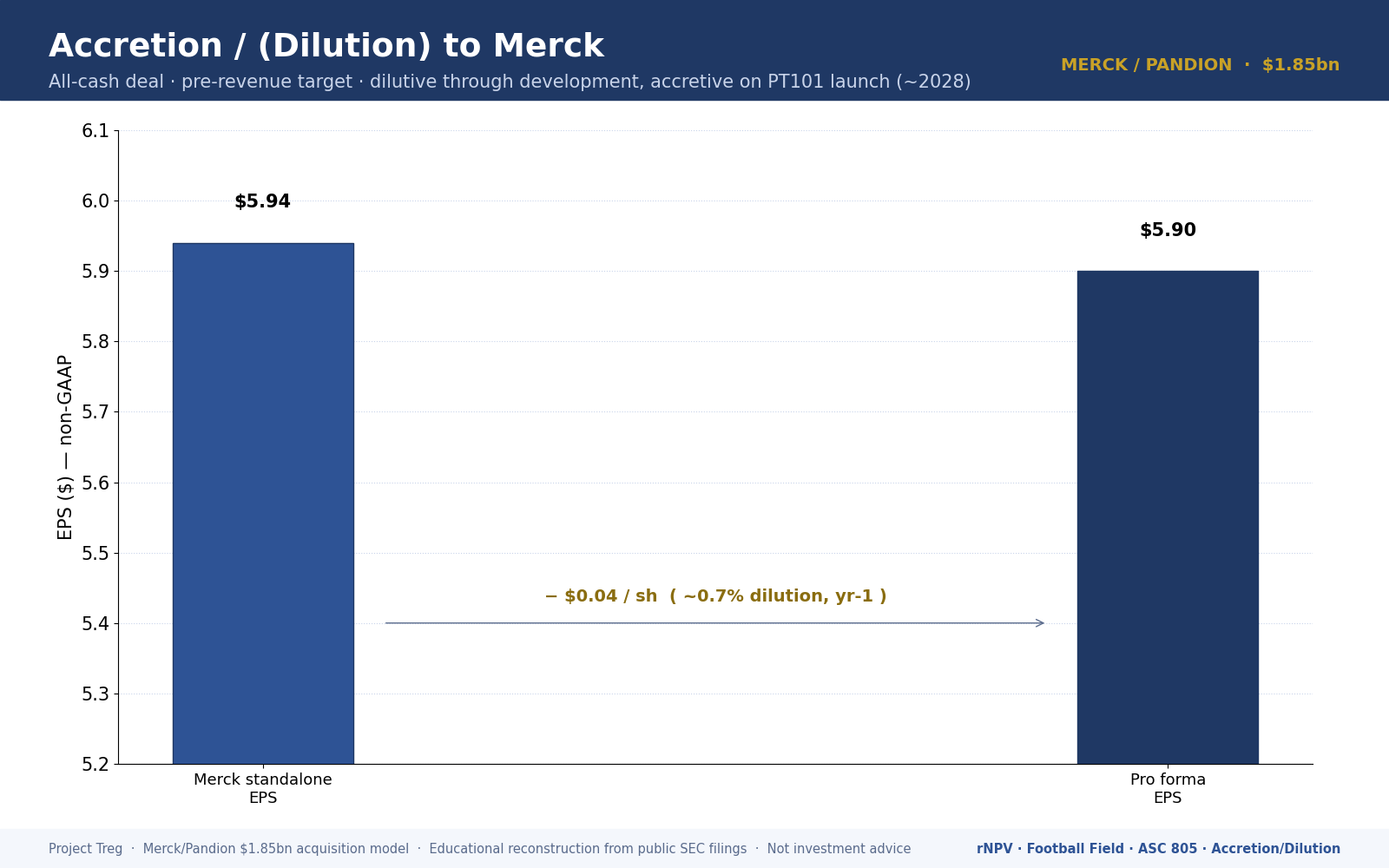

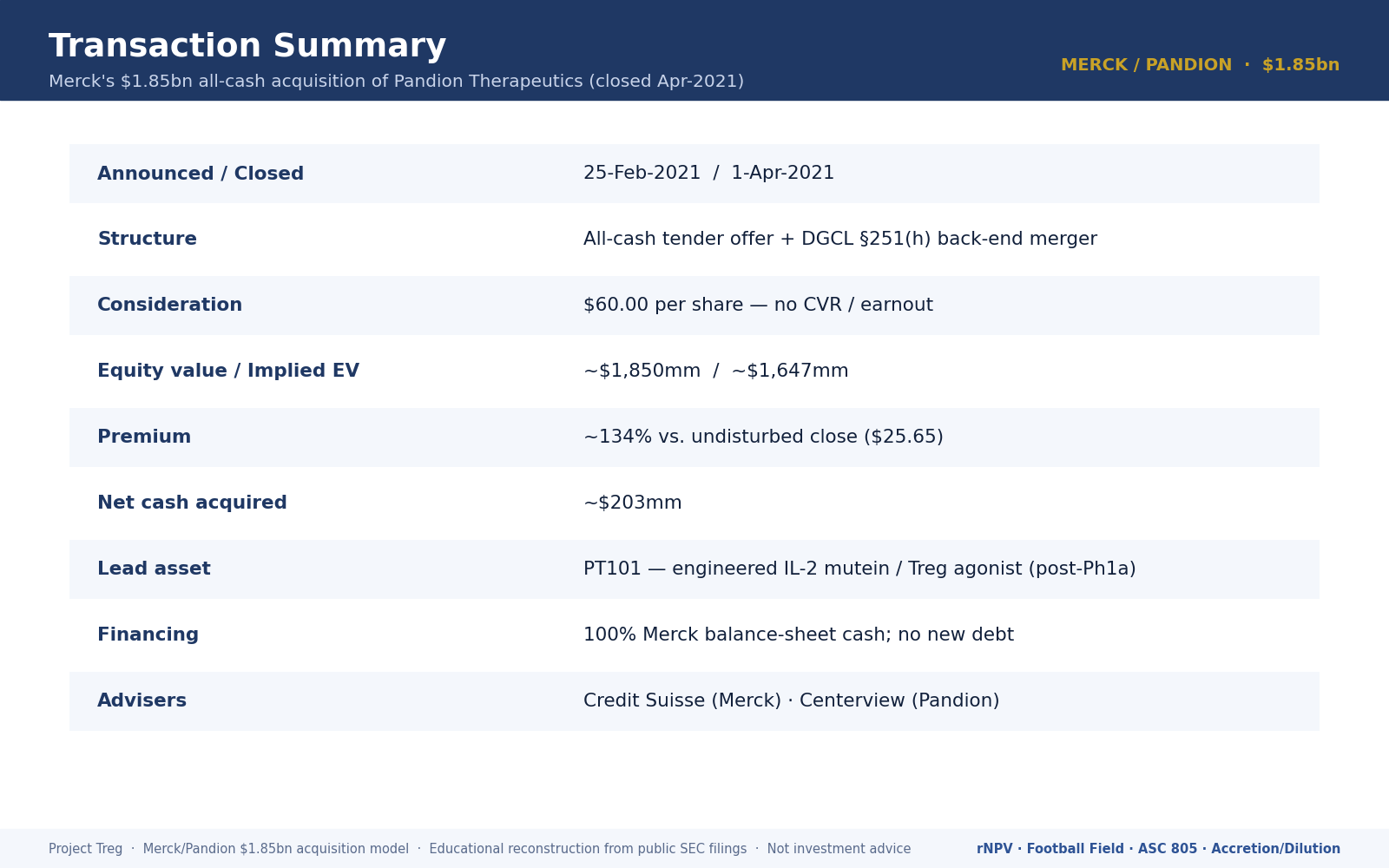

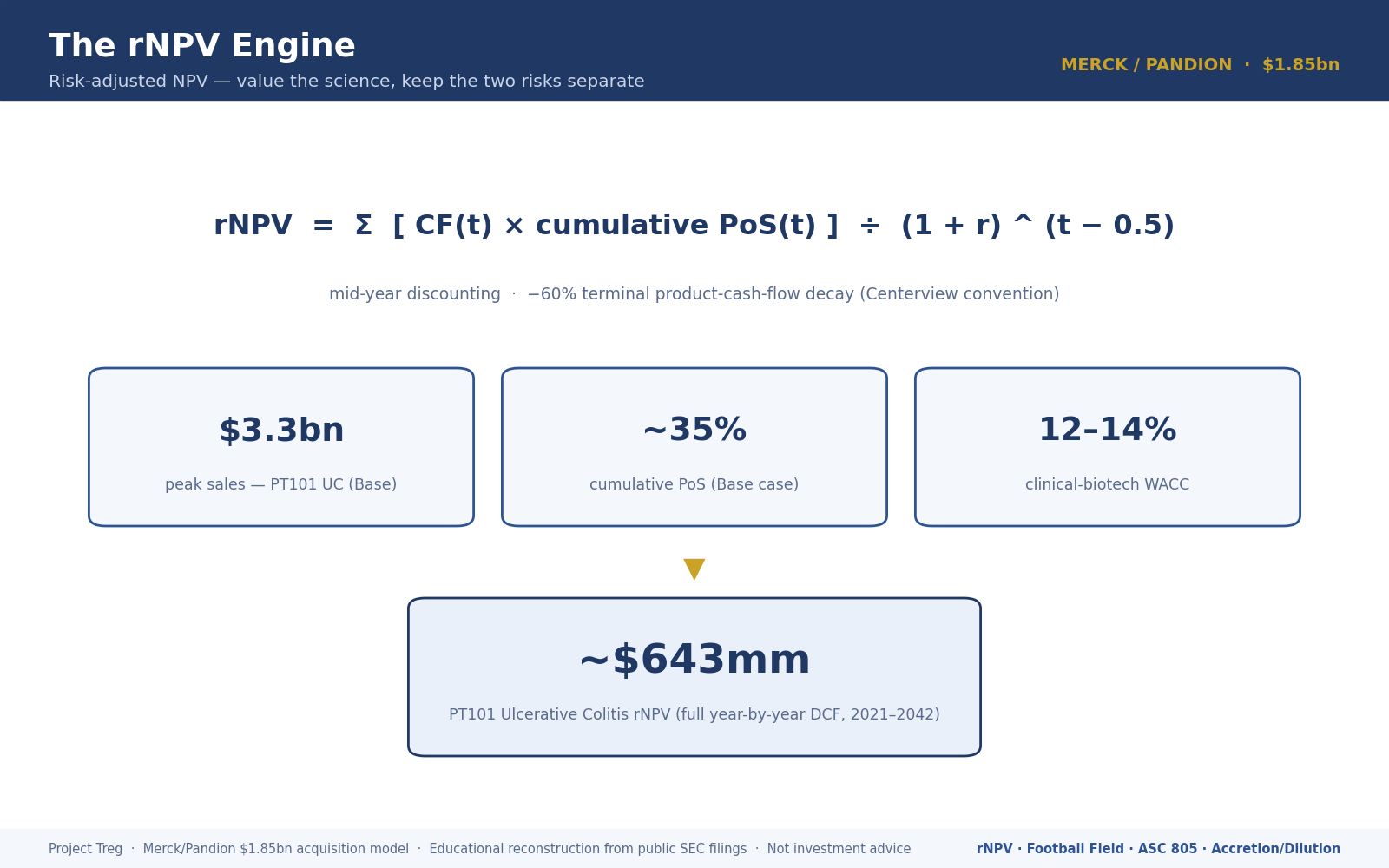

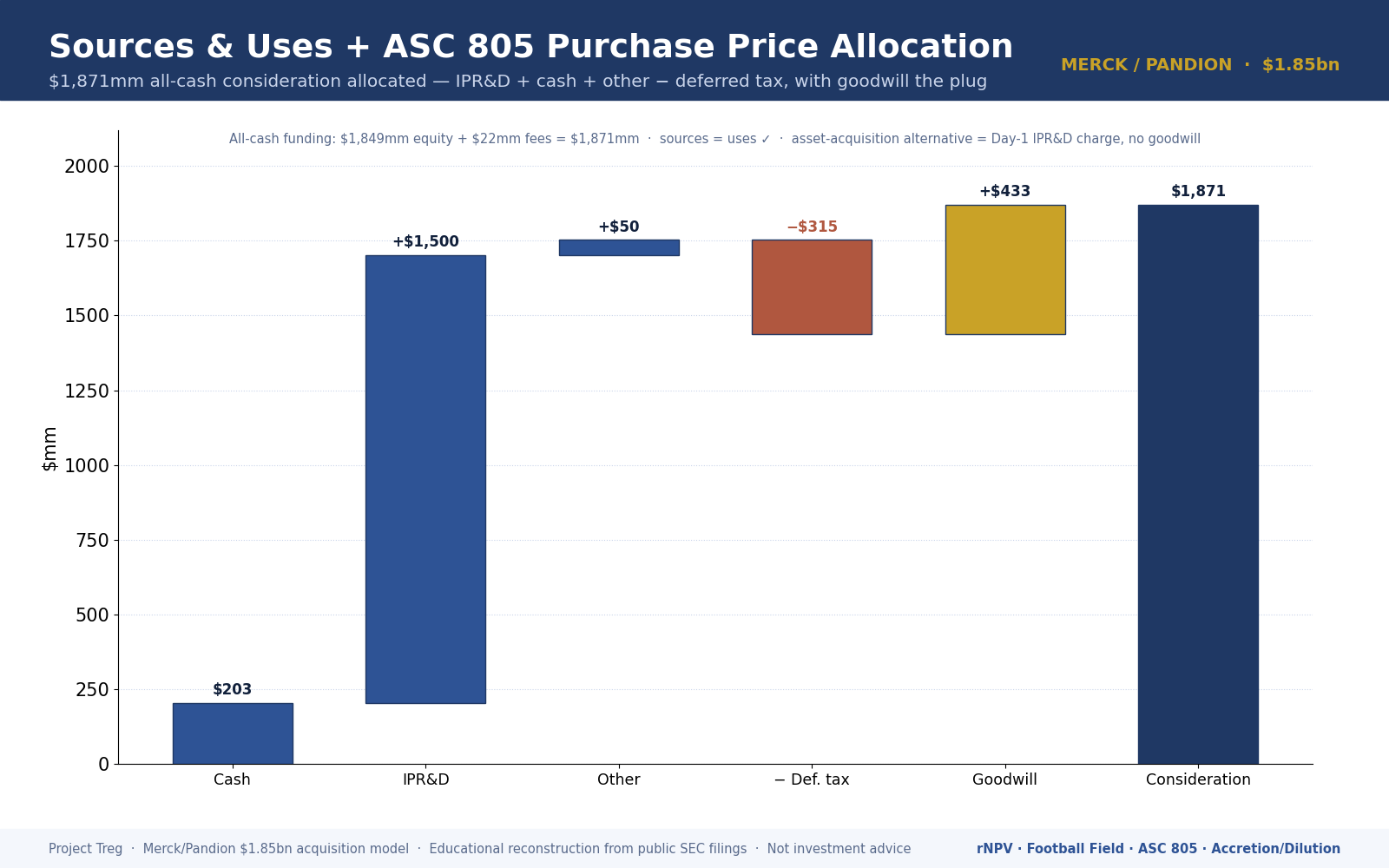

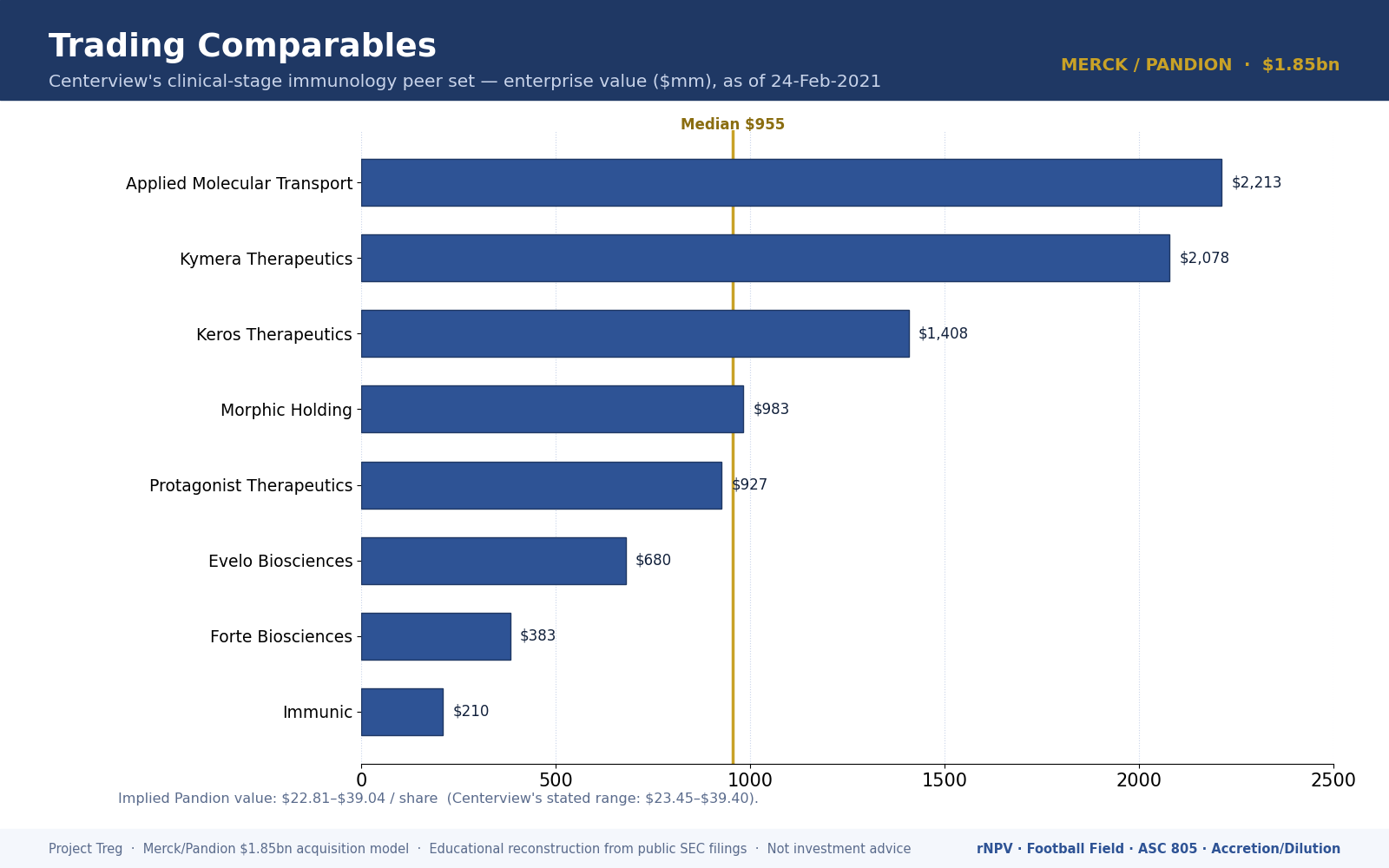

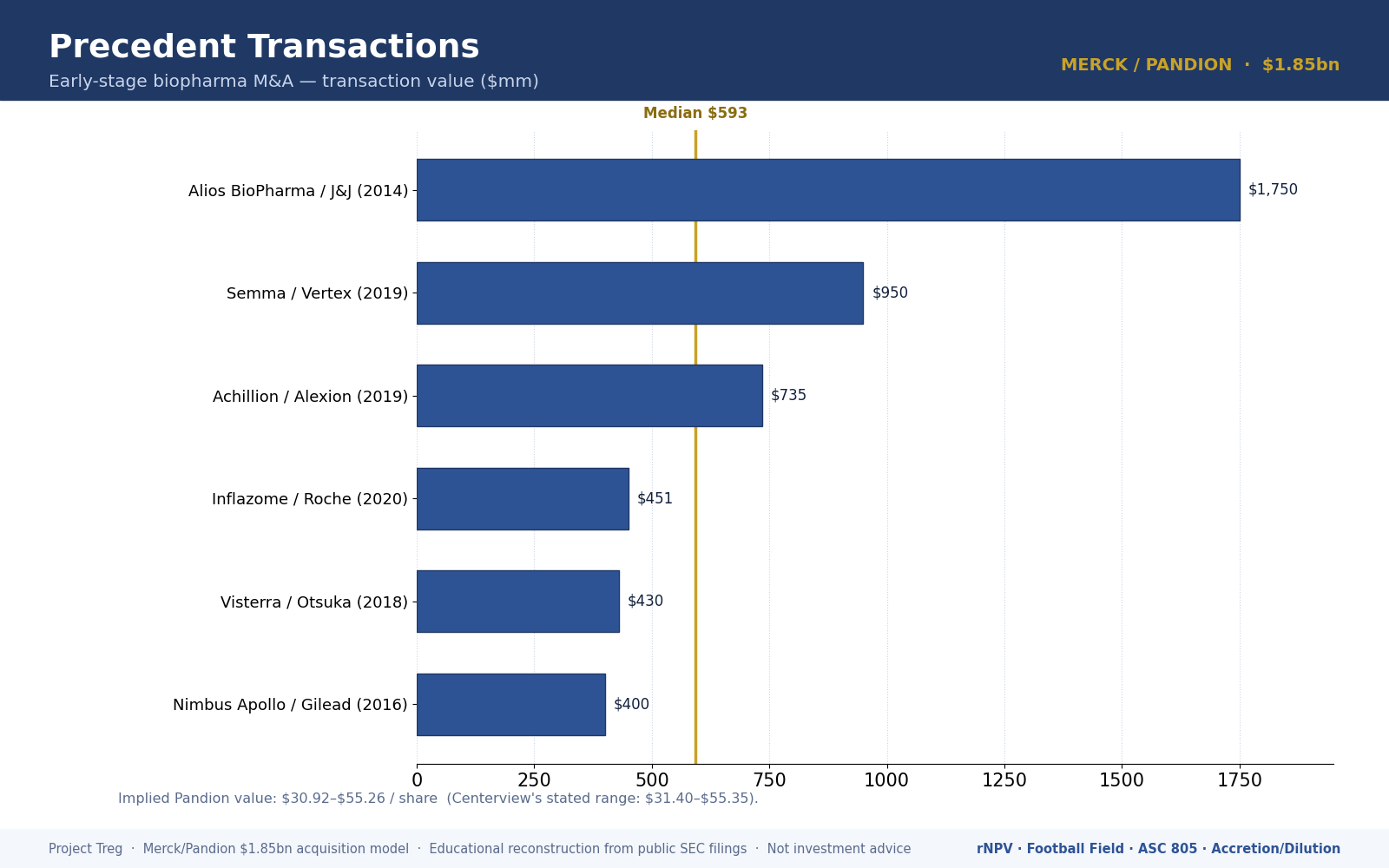

Reconstructs and values Merck's $1.85bn acquisition of Pandion Therapeutics end-to-end - risk-adjusted NPV (PT101 + pipeline), the acquirer-WACC bridge, ASC 805 purchase accounting and EPS accretion/dilution - as a worked, fully sourced teaching and reference case.

You're valuing, or learning to value, a clinical-stage biotech/pharma acquisition - investment-banking, equity-research, private-equity or corporate-development analysts; MBA and interview-prep candidates; anyone who wants a worked rNPV plus full M&A-consequences case sourced to public filings.

You need a blank, build-your-own template for your own company's multi-year operating forecast; a non-biotech or all-stock deal; or audited numbers for live transaction execution (inputs are illustrative and must be re-sourced).