Originally published: 01/07/2020 06:11

Last version published: 01/07/2020 10:54

Publication number: ELQ-23423-2

View all versions & Certificate

Last version published: 01/07/2020 10:54

Publication number: ELQ-23423-2

View all versions & Certificate

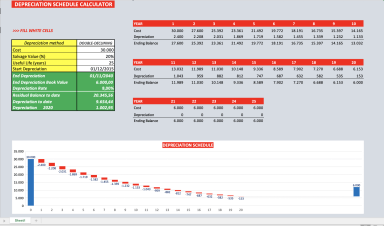

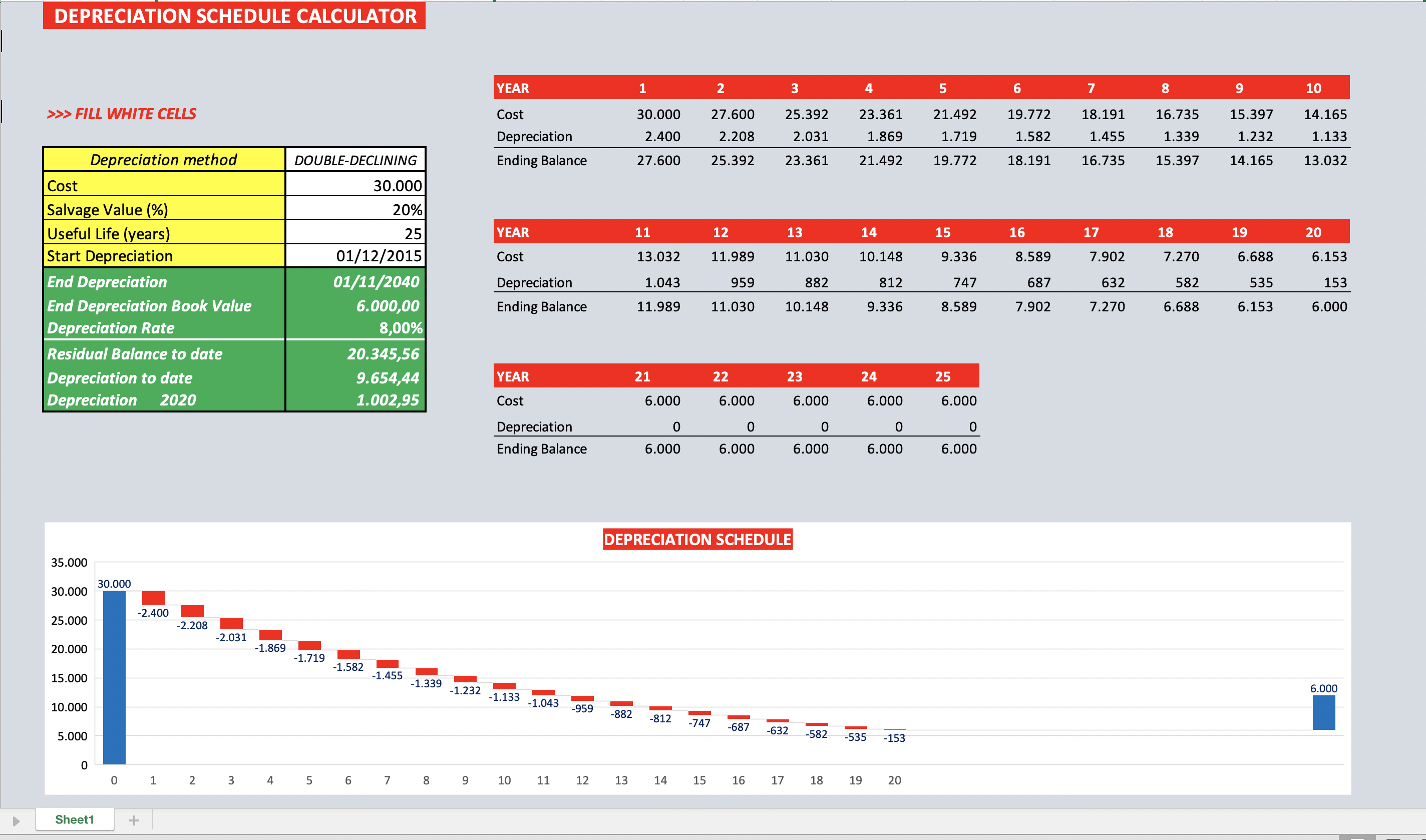

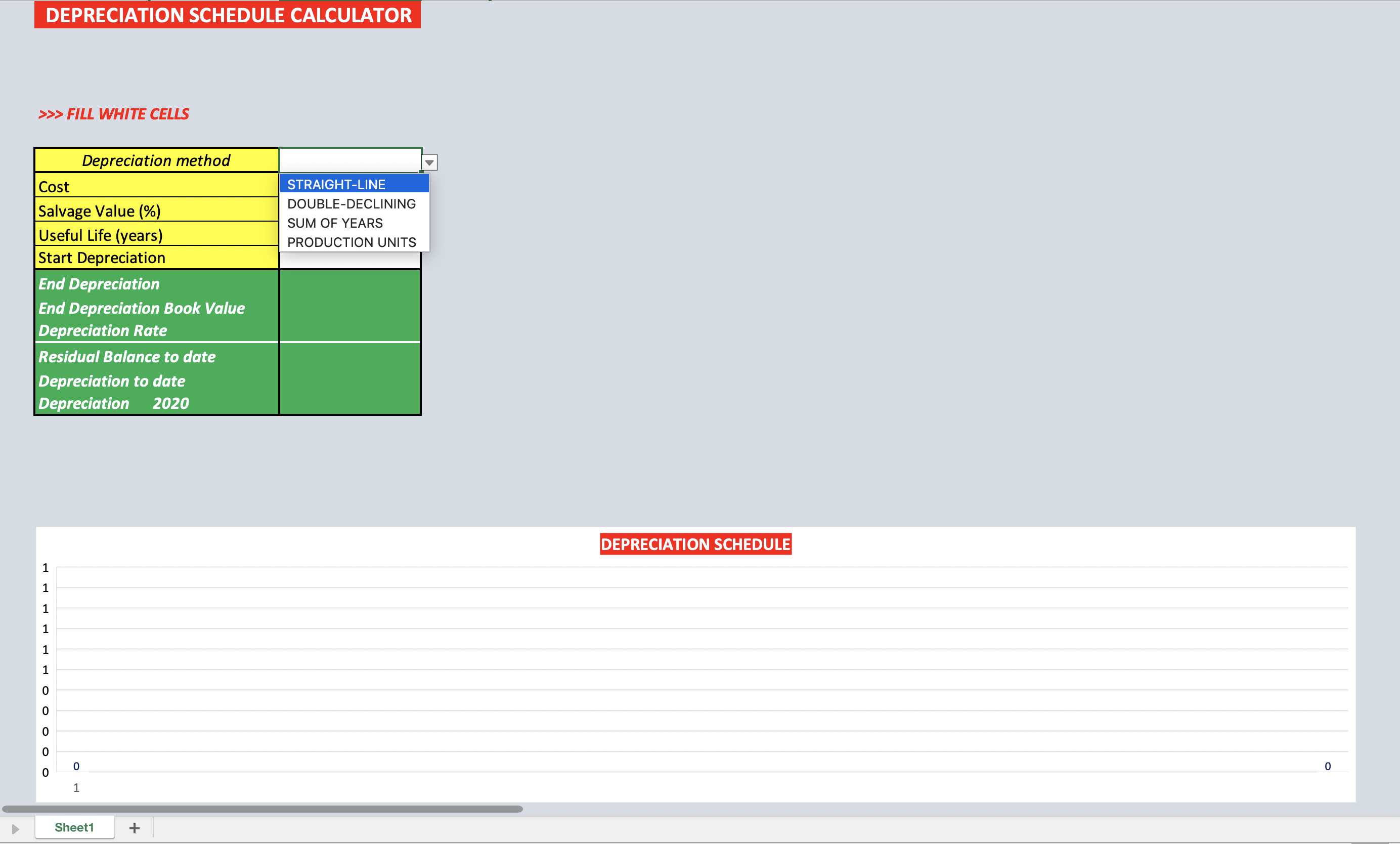

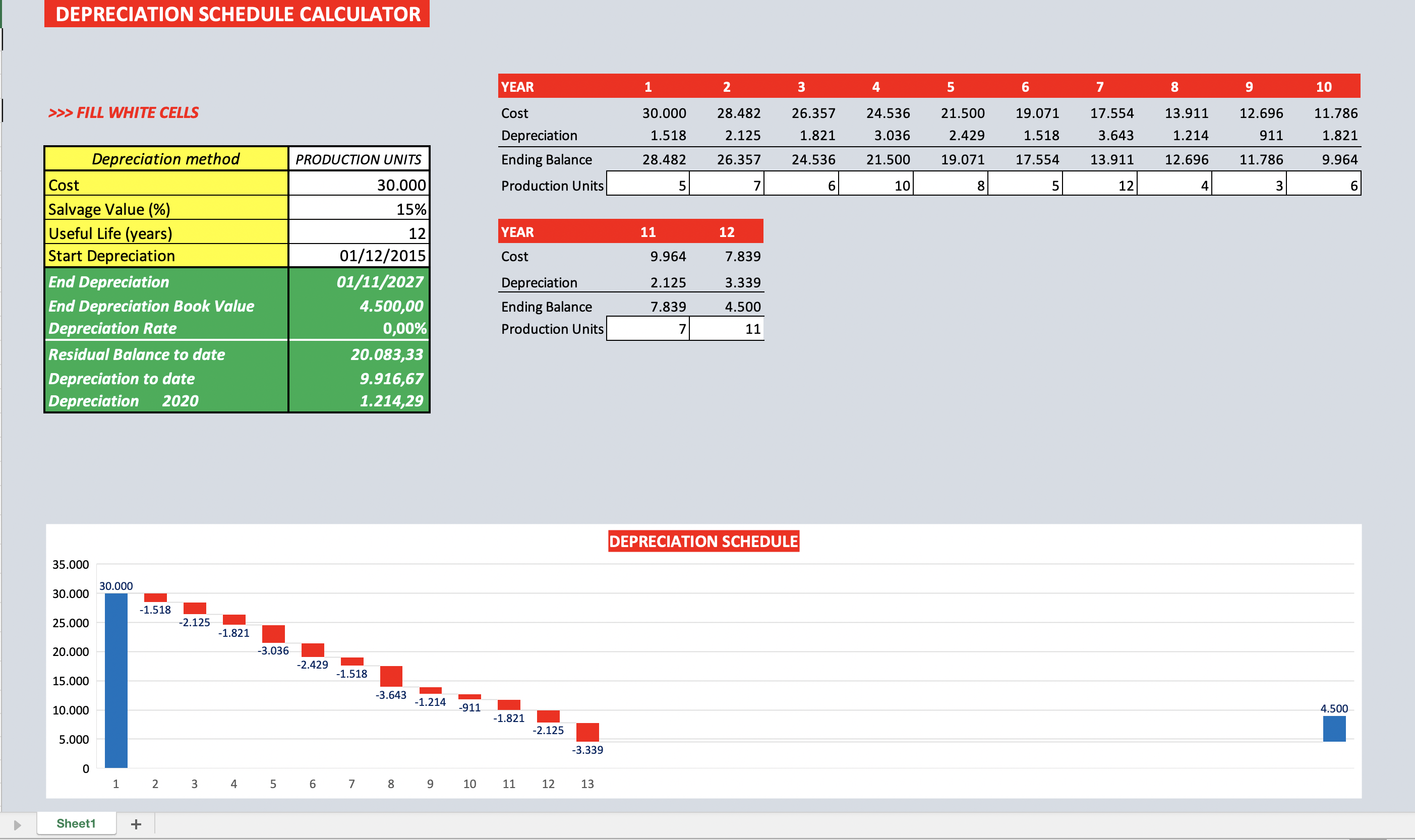

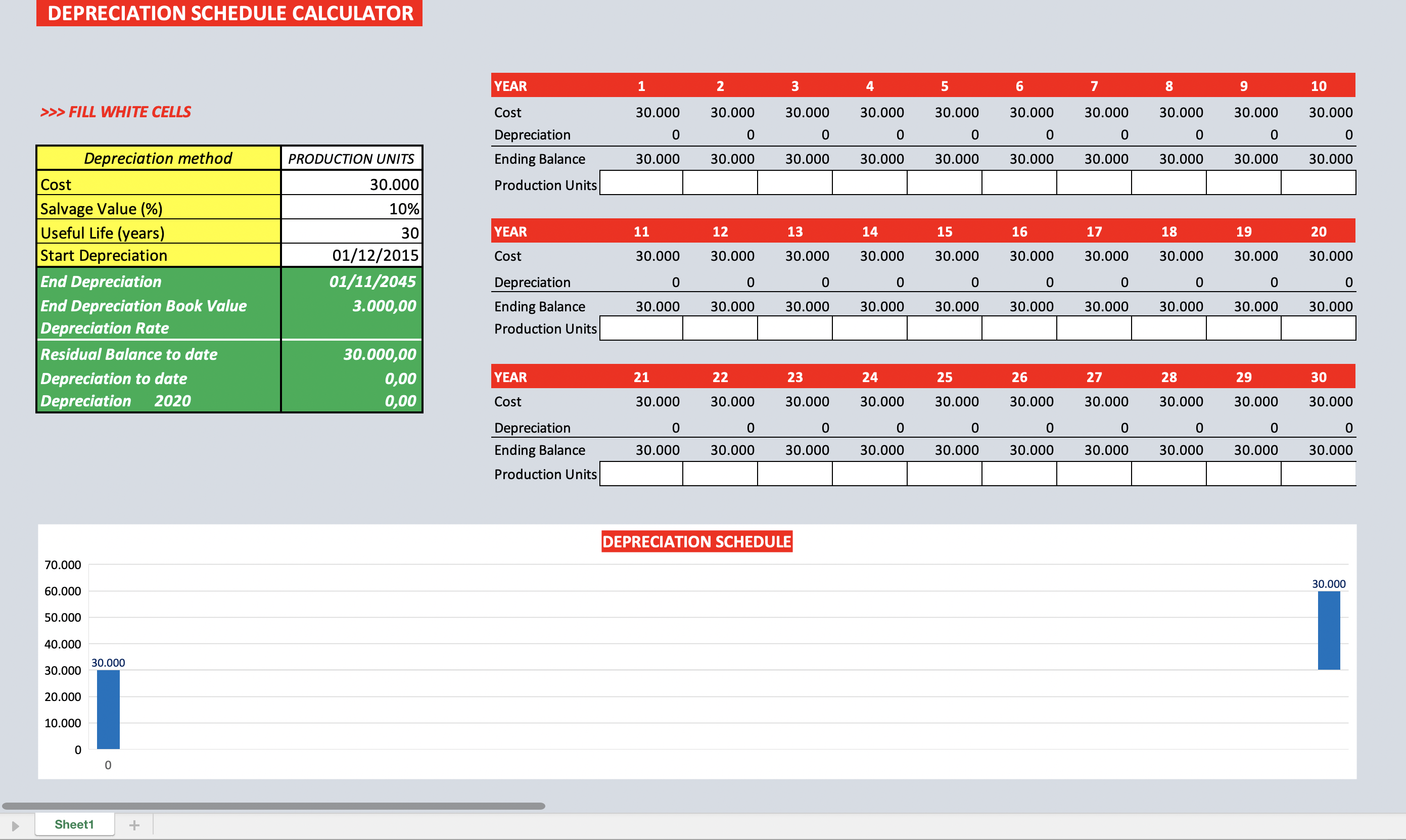

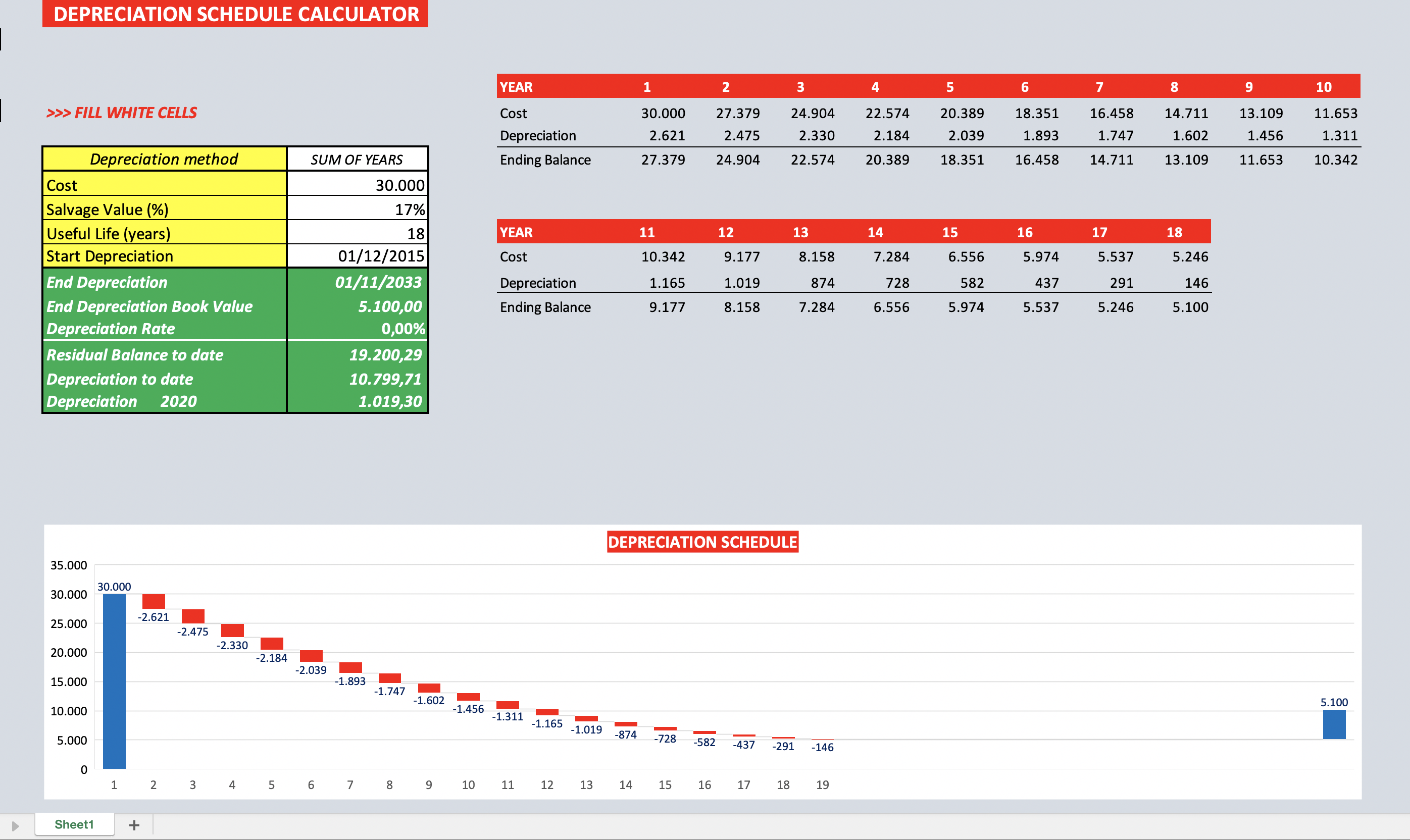

Depreciation Schedule Calculator

Calculate Depreciation of An Asset Using 4 of the most Popular Depreciation Methods.

depreciationamortizationstraight linedeclining balanceunits of productionsum of the yearsmethoduseful lifesalvage valuedepreciation rate

Description

This excel tool will calculate the depreciation expense of a tangible asset, based on the selected depreciation method, generating a depreciation schedule for the full term, also in chart form.

Depreciation is an accounting process by which a company allocates an asset's cost throughout its useful life. In other words, it is the reduction in the value of an asset over time, due to usage, wear and tear, or obsolescence.

According to generally accepted accounting principles, several methods of depreciation can be used. Among the most common:

• Straight-Line Depreciation

• Declining (or Double Declining) Balance Depreciation

• Sum-of-the-Years’ Digits Depreciation

• Units of Production Depreciation

STRAIGHT-LINE DEPRECIATION

The straight-line method is the simplest, calculating depreciation by subtracting from the original cost the estimated salvage value and dividing the difference by the number of years of estimated useful life of the asset. Therefore the same amount of depreciation expense is booked every year and the book value of the asset at the end of useful life will be its salvage value.

DECLINING BALANCE DEPRECIATION

The declining balance method is a type of accelerated depreciation used to write off depreciation costs more quickly and minimize tax exposure. This method can be popular if an asset is expected to have greater utility in its earlier years. It also helps to create a larger realized gain if the asset is actually sold. Some companies may also use the double-declining balance method which is an even more aggressive depreciation methodology for early expense management.

SUM-OF-THE-YEARS’ DIGITS DEPRECIATION

The sum-of-the-years' digits method offers a depreciation rate that accelerates more than the straight-line method, but less than the declining balance method. Annual depreciation is separated into fractions, using the number of years of the business asset's useful life. Such assets may include buildings, machinery, furniture, equipment, vehicles, and electronics.

To cite an example, consider an asset with a useful life of five years, which will have a sum-of-the-years value of 15 (5 + 4 + 3 + 2 + 1). The first year is assigned a value of 5, the second year value of 4, and so on. The depreciation rate for the first year is the straight-line value multiplied by the first year's fraction (5 ÷ 15, or one-third).

Sometimes called the “SYD” method, this approach is also more appropriate than the straight-line depreciation model if an asset depreciates more quickly or has greater production capacity during its earlier years.

UNITS OF PRODUCTION DEPRECIATION

Units of production assign an equal expense rate to each unit produced, which makes it most useful for assembly or production lines. The formula involves using historical costs (the price of an asset based on its nominal or original cost when acquired by the company) and estimated salvage values, and then determines the expense for the accounting period multiplied by the number of units produced or number of hours used.

(including quotes from investopedia.com and corporatefinanceinstitute.com)

This excel tool will calculate the depreciation expense of a tangible asset, based on the selected depreciation method, generating a depreciation schedule for the full term, also in chart form.

Depreciation is an accounting process by which a company allocates an asset's cost throughout its useful life. In other words, it is the reduction in the value of an asset over time, due to usage, wear and tear, or obsolescence.

According to generally accepted accounting principles, several methods of depreciation can be used. Among the most common:

• Straight-Line Depreciation

• Declining (or Double Declining) Balance Depreciation

• Sum-of-the-Years’ Digits Depreciation

• Units of Production Depreciation

STRAIGHT-LINE DEPRECIATION

The straight-line method is the simplest, calculating depreciation by subtracting from the original cost the estimated salvage value and dividing the difference by the number of years of estimated useful life of the asset. Therefore the same amount of depreciation expense is booked every year and the book value of the asset at the end of useful life will be its salvage value.

DECLINING BALANCE DEPRECIATION

The declining balance method is a type of accelerated depreciation used to write off depreciation costs more quickly and minimize tax exposure. This method can be popular if an asset is expected to have greater utility in its earlier years. It also helps to create a larger realized gain if the asset is actually sold. Some companies may also use the double-declining balance method which is an even more aggressive depreciation methodology for early expense management.

SUM-OF-THE-YEARS’ DIGITS DEPRECIATION

The sum-of-the-years' digits method offers a depreciation rate that accelerates more than the straight-line method, but less than the declining balance method. Annual depreciation is separated into fractions, using the number of years of the business asset's useful life. Such assets may include buildings, machinery, furniture, equipment, vehicles, and electronics.

To cite an example, consider an asset with a useful life of five years, which will have a sum-of-the-years value of 15 (5 + 4 + 3 + 2 + 1). The first year is assigned a value of 5, the second year value of 4, and so on. The depreciation rate for the first year is the straight-line value multiplied by the first year's fraction (5 ÷ 15, or one-third).

Sometimes called the “SYD” method, this approach is also more appropriate than the straight-line depreciation model if an asset depreciates more quickly or has greater production capacity during its earlier years.

UNITS OF PRODUCTION DEPRECIATION

Units of production assign an equal expense rate to each unit produced, which makes it most useful for assembly or production lines. The formula involves using historical costs (the price of an asset based on its nominal or original cost when acquired by the company) and estimated salvage values, and then determines the expense for the accounting period multiplied by the number of units produced or number of hours used.

(including quotes from investopedia.com and corporatefinanceinstitute.com)

This Best Practice includes

1 Excel workbook

Domenico Cristarella offers you this Best Practice for free!

download for free

Add to bookmarks