Originally published: 27/03/2023 14:02

Last version published: 22/10/2024 14:30

Publication number: ELQ-13614-2

View all versions & Certificate

Last version published: 22/10/2024 14:30

Publication number: ELQ-13614-2

View all versions & Certificate

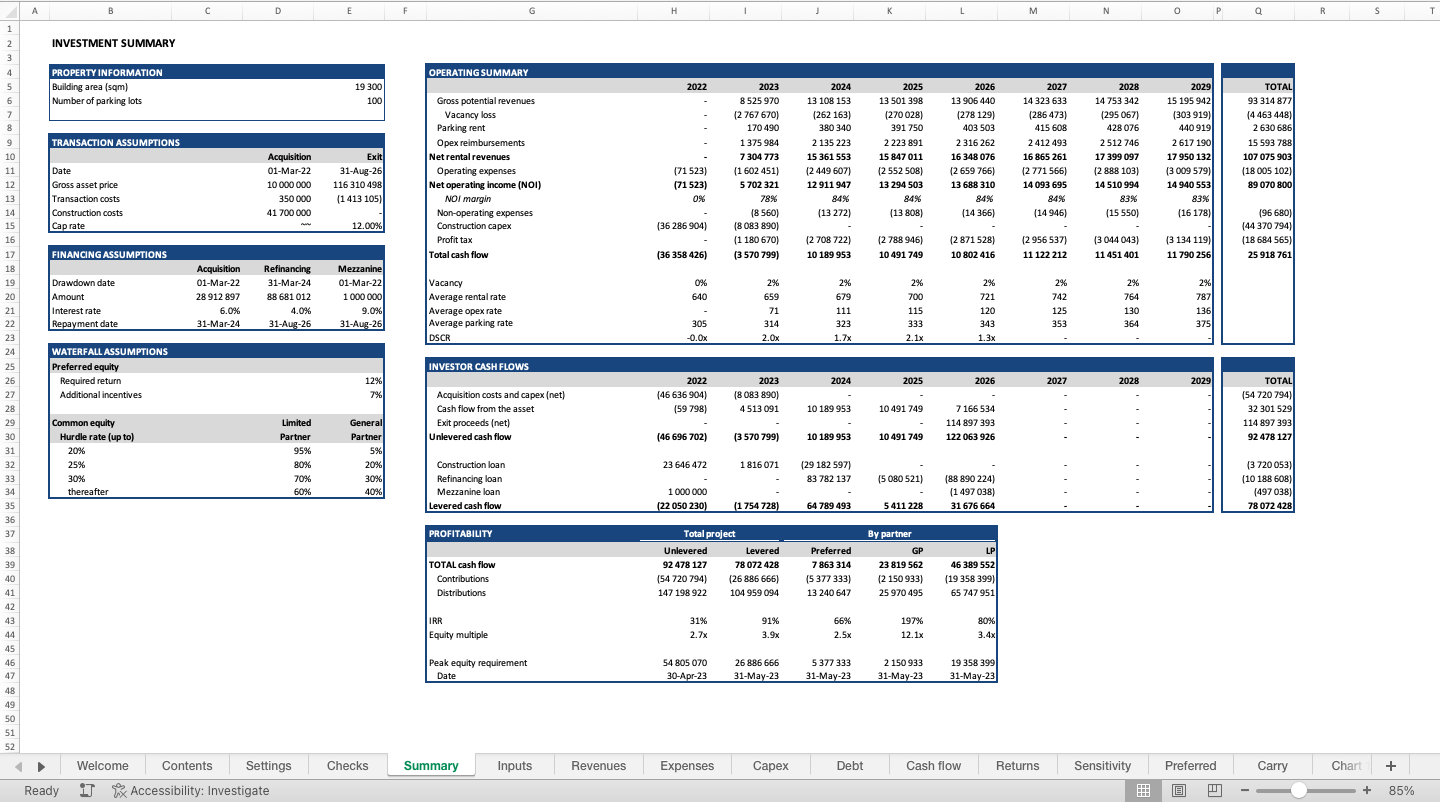

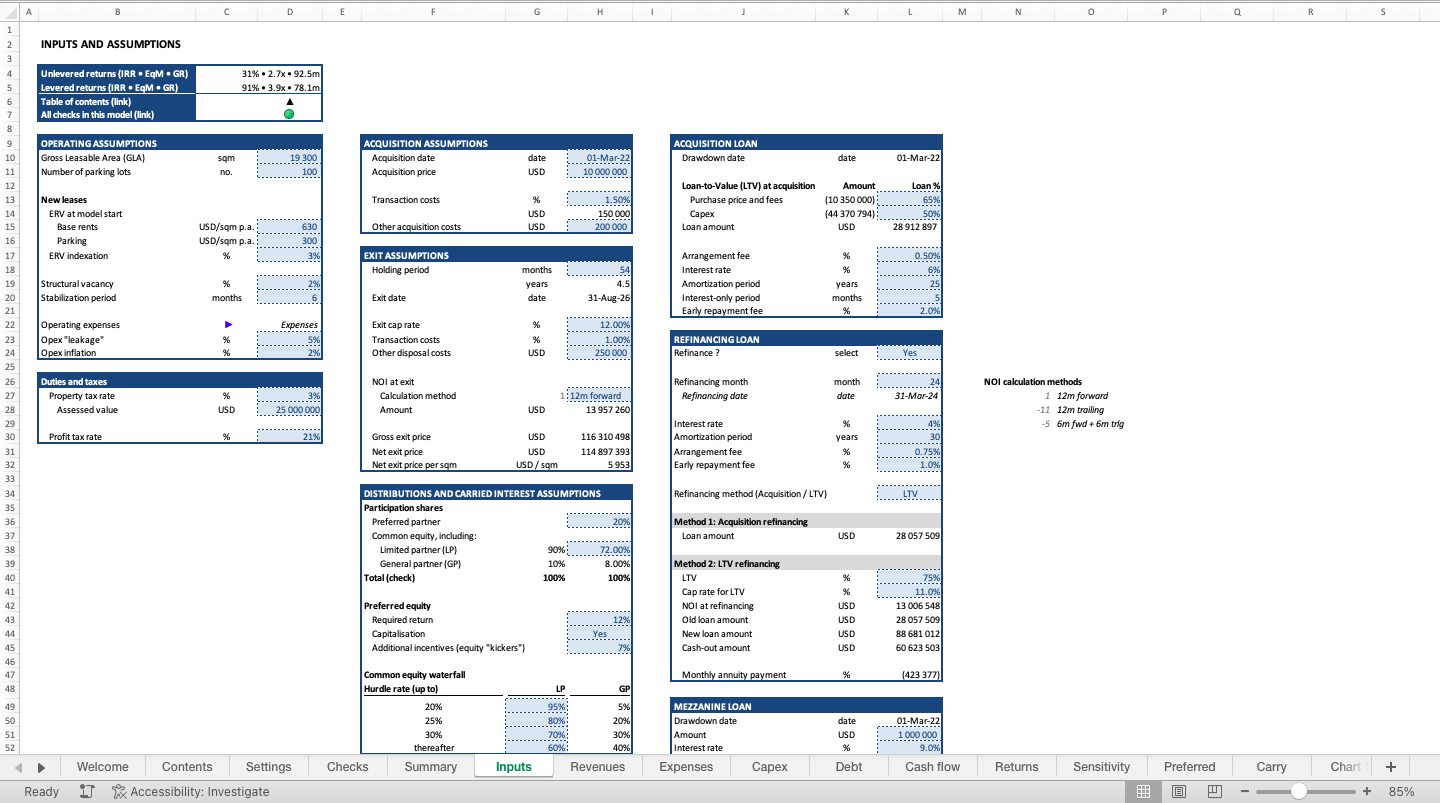

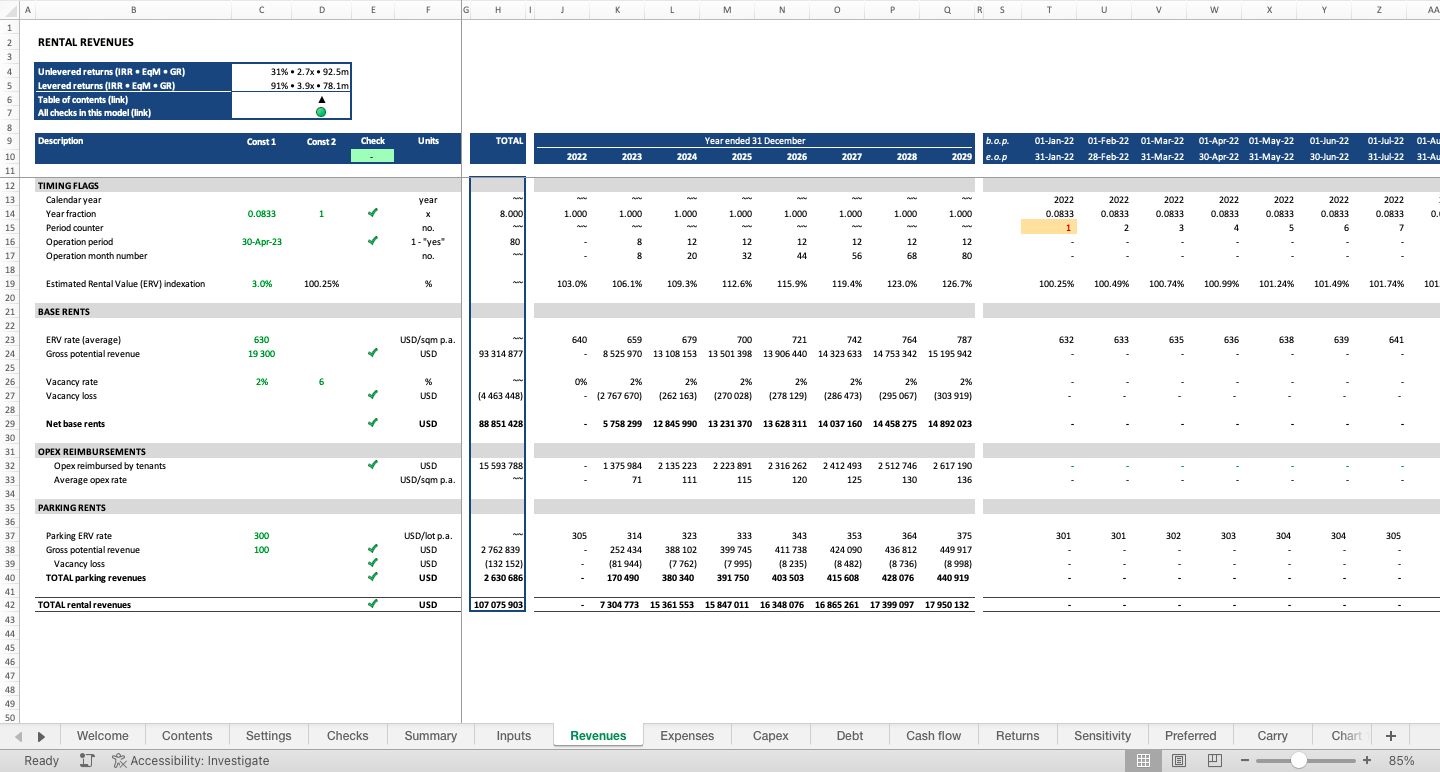

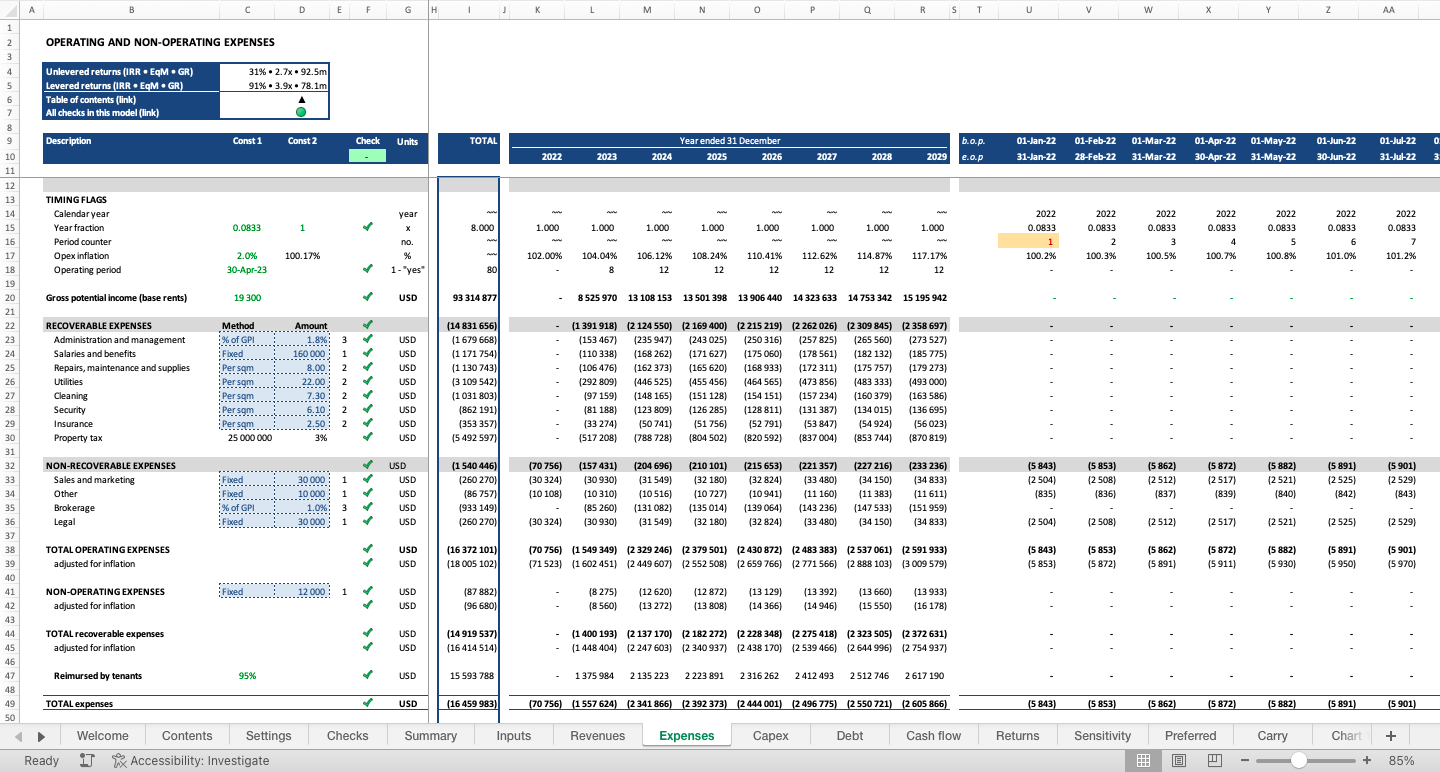

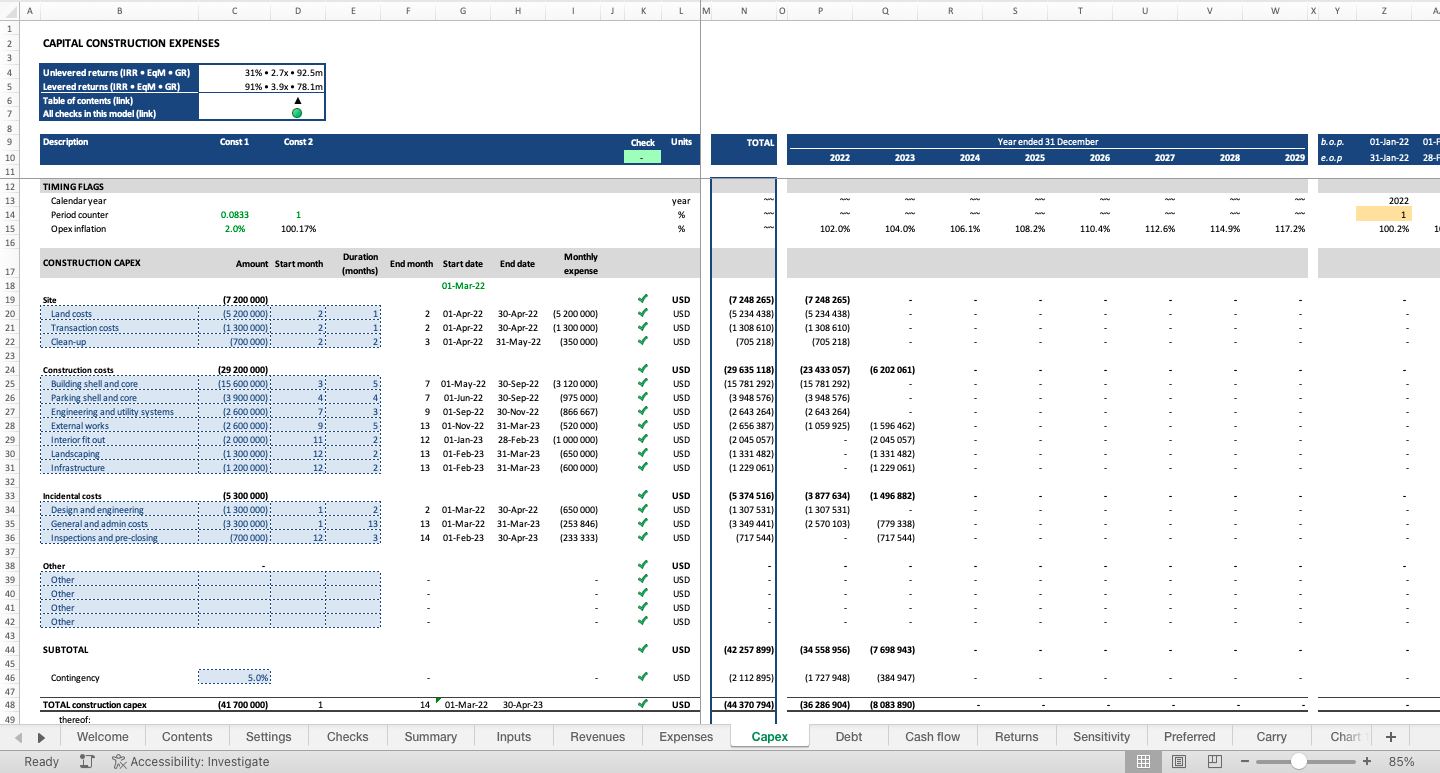

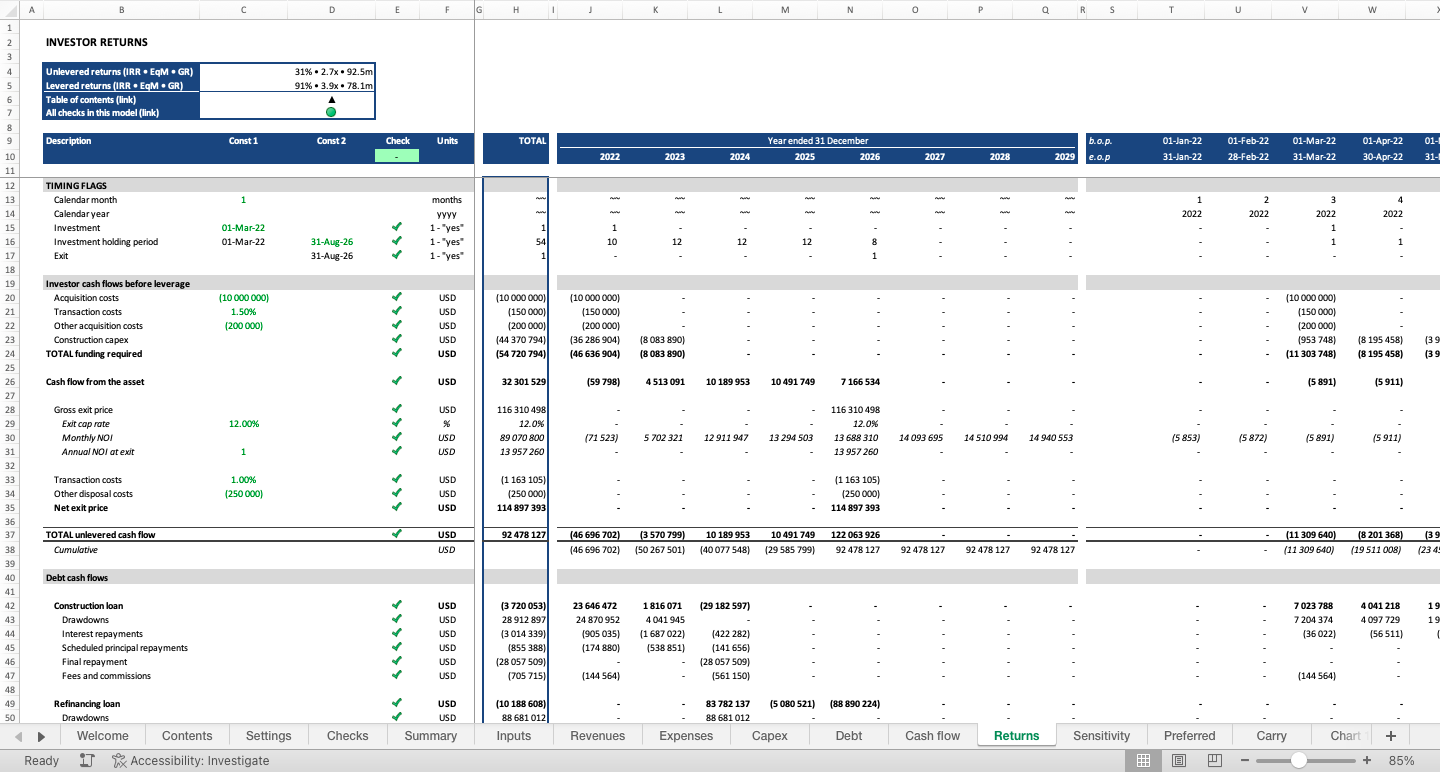

Real Estate Development Financial Model

A professional model for real estate construction (build – hold – sell)

Further information

Calculate future cash flows, returns and sensitivities for the construction and subsequent lease of commercial real estate properties

Use this model if you are considering a construction project of commercial real estate properties

Every investment is unique and so the model might need to be adjusted to your situation. Contact me if you need help tailoring this model or developing a new one