Originally published: 18/05/2020 06:09

Last version published: 13/09/2025 20:37

Publication number: ELQ-46089-5

View all versions & Certificate

Last version published: 13/09/2025 20:37

Publication number: ELQ-46089-5

View all versions & Certificate

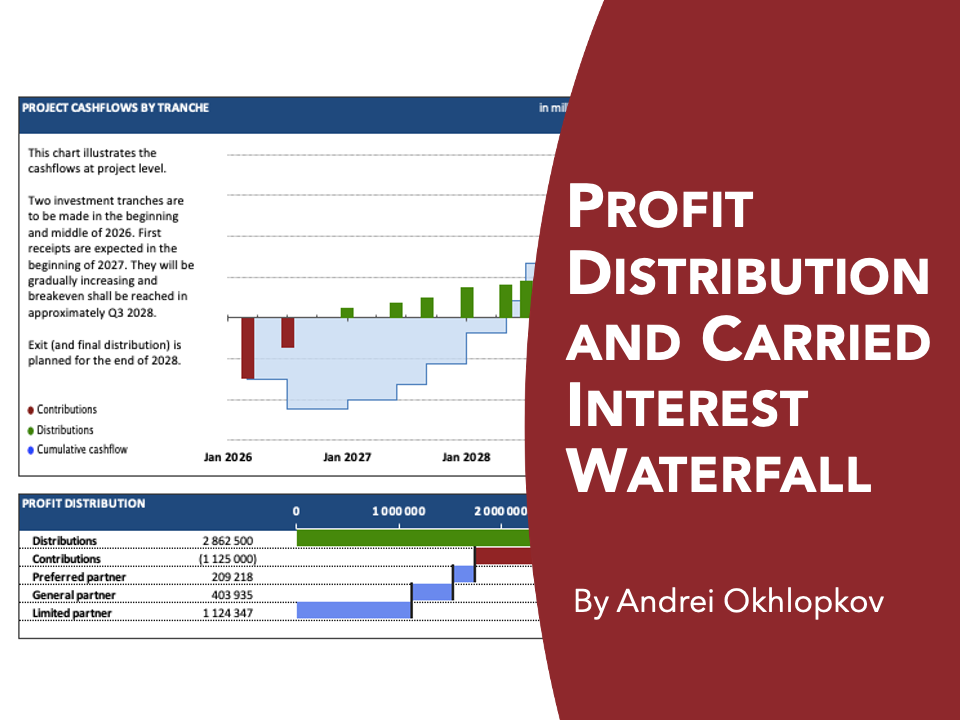

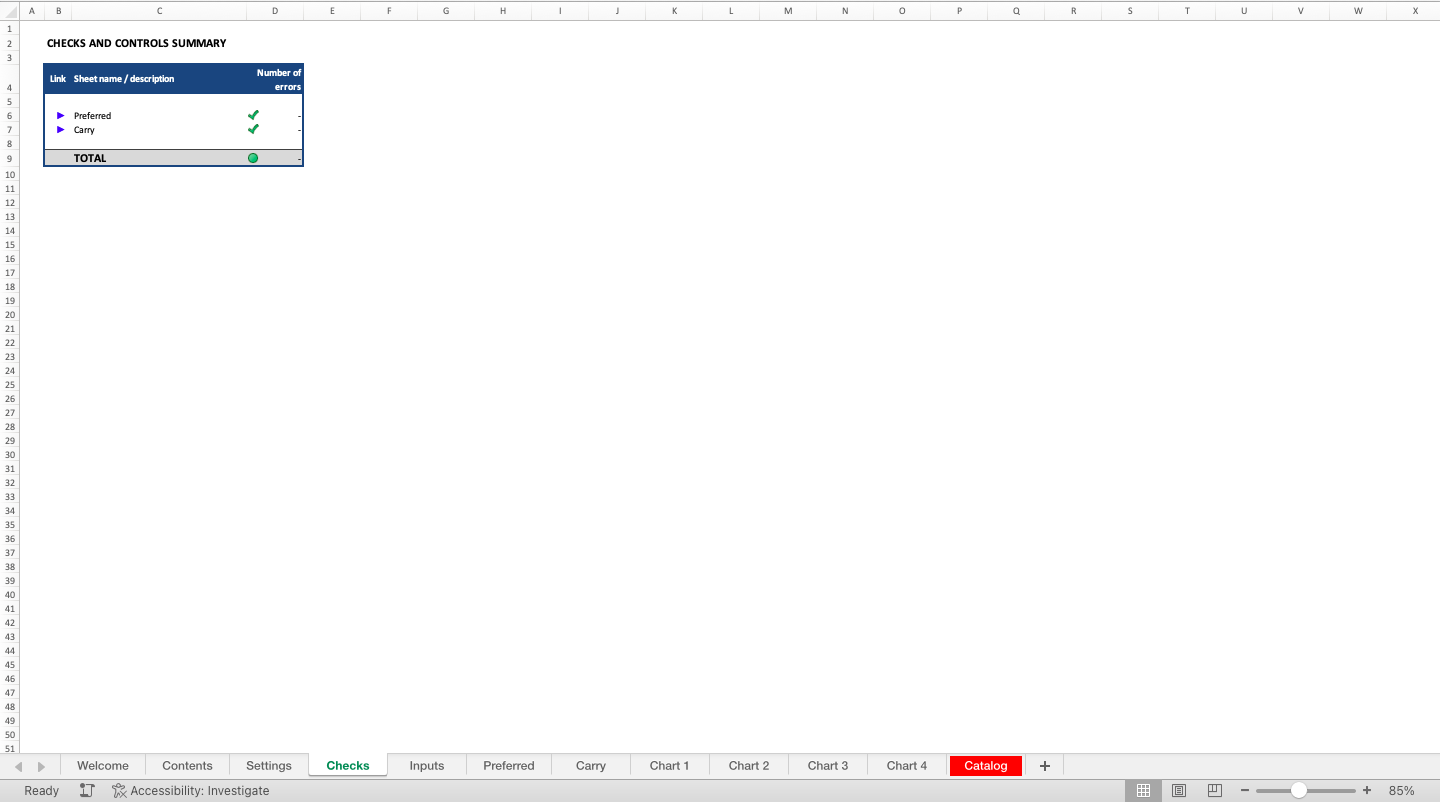

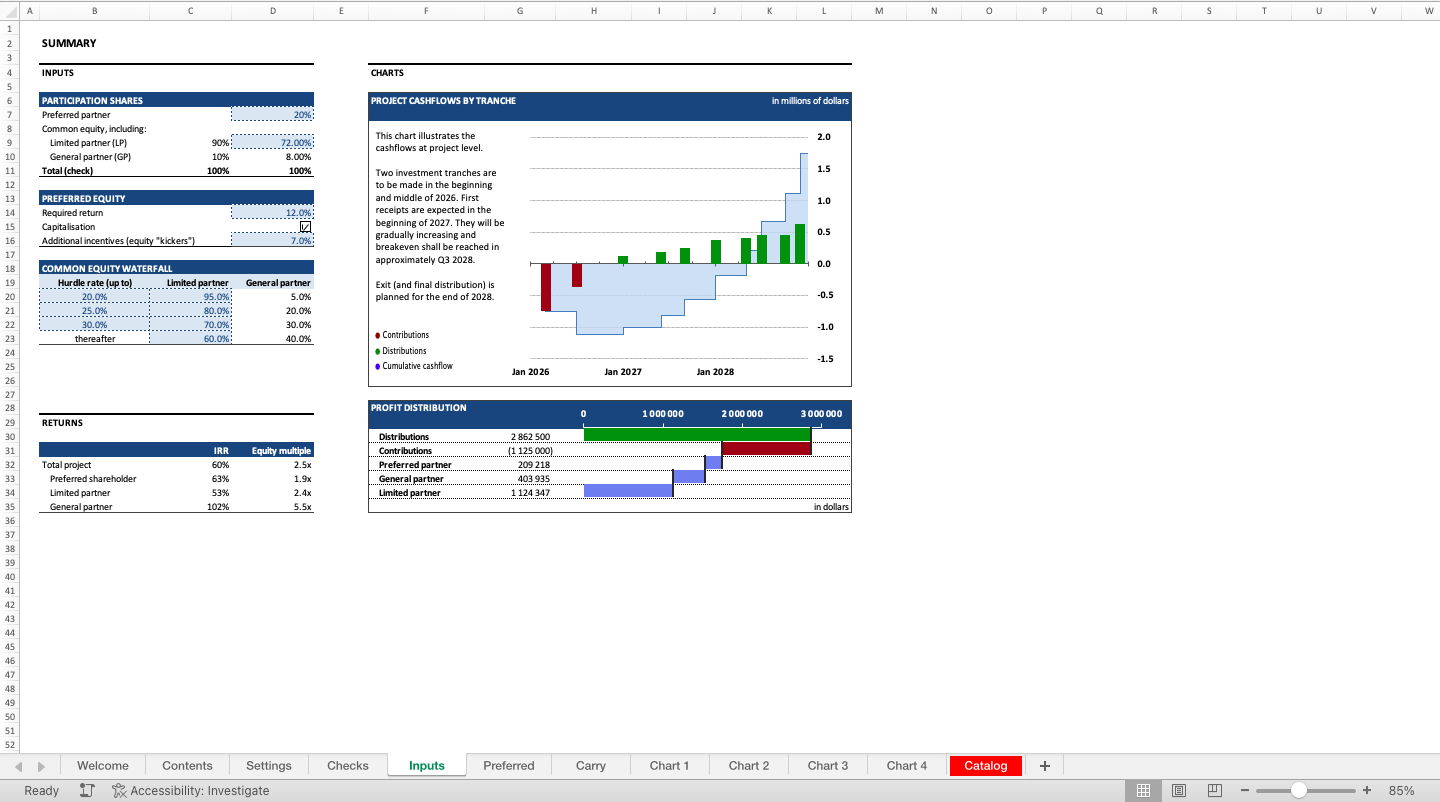

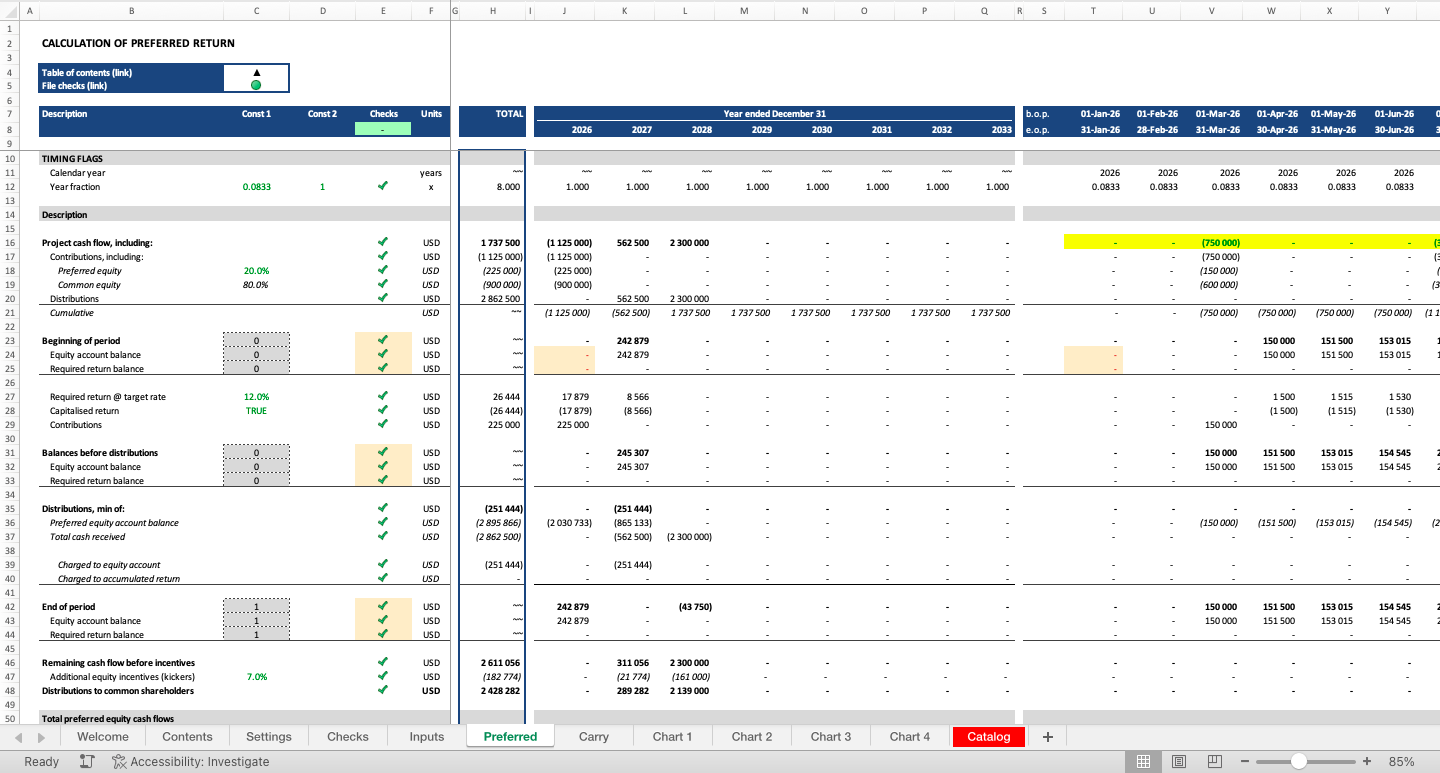

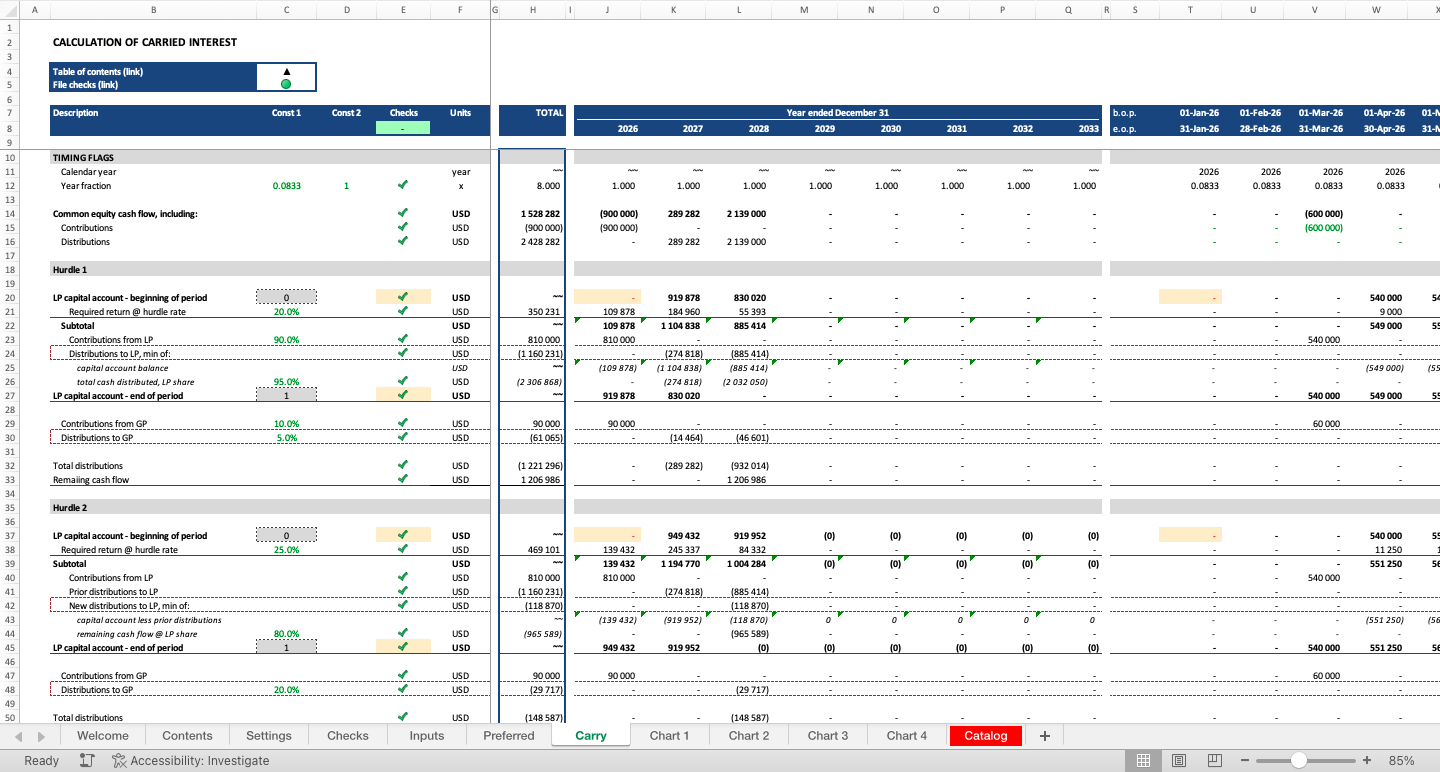

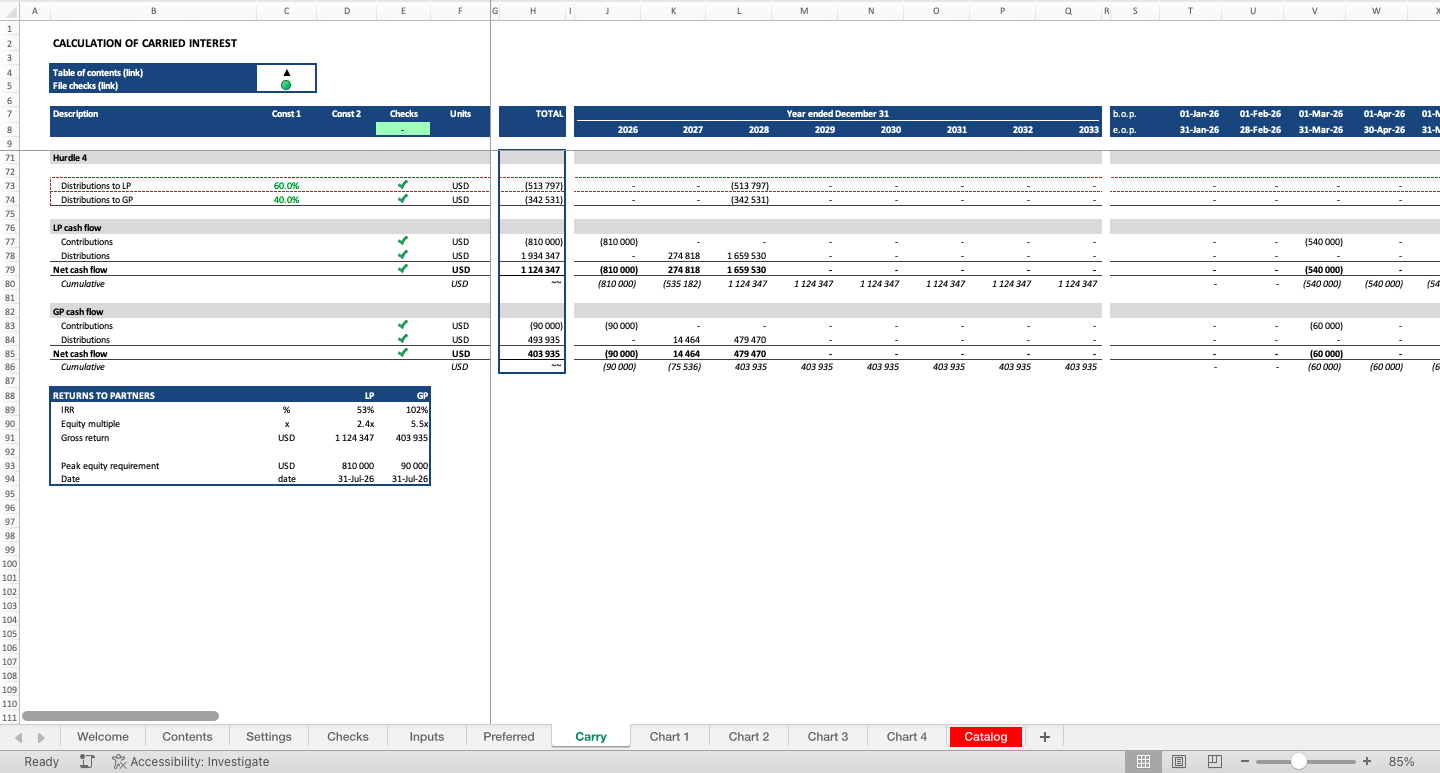

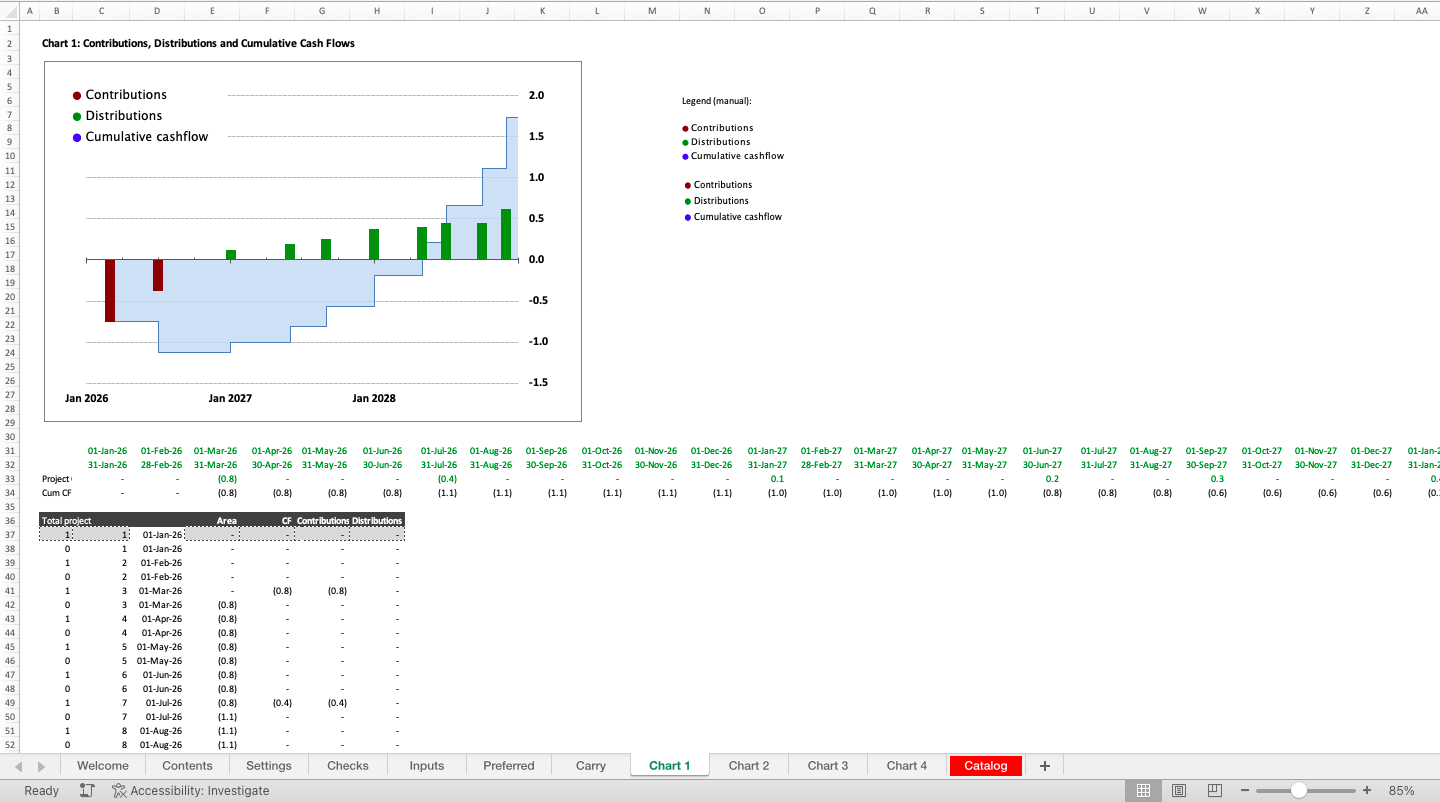

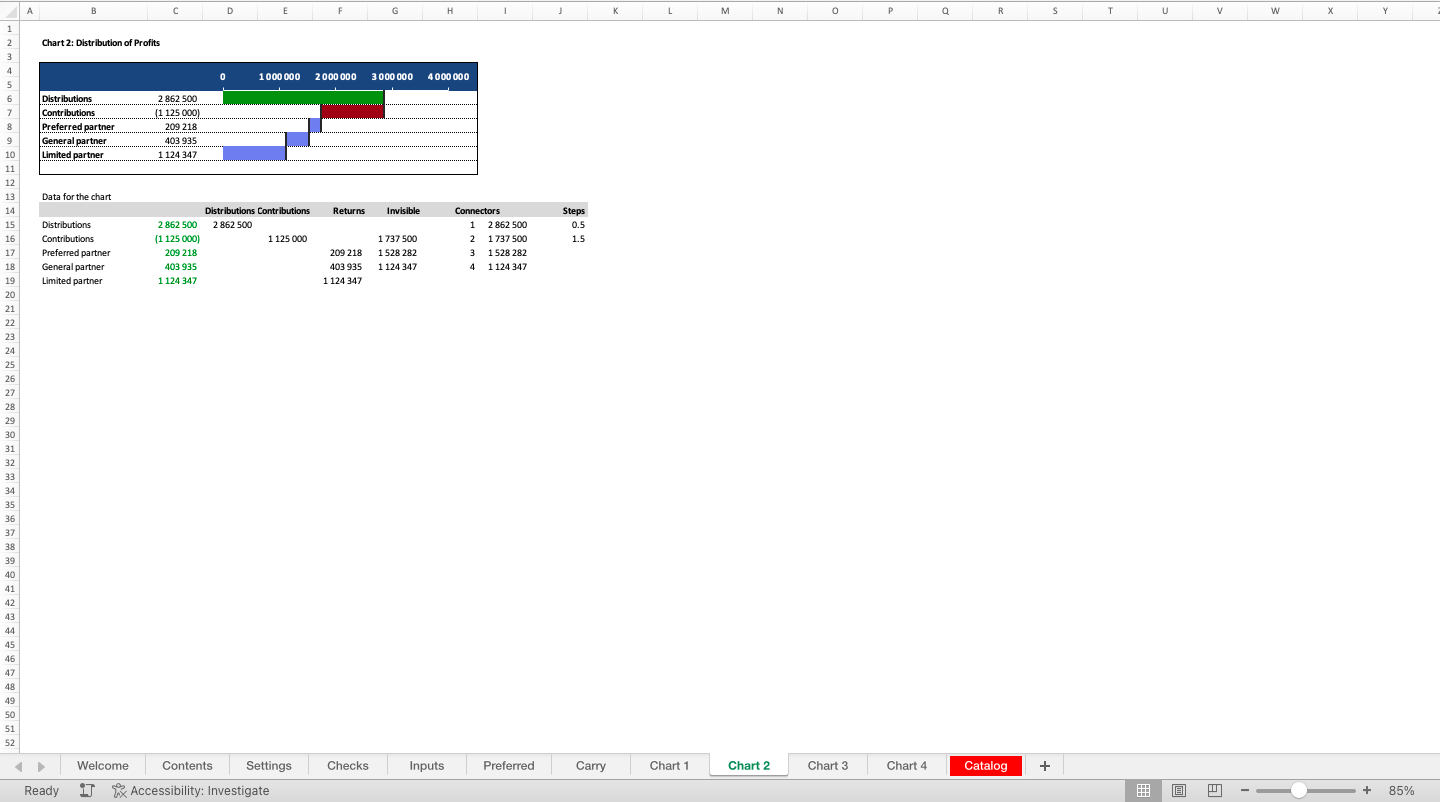

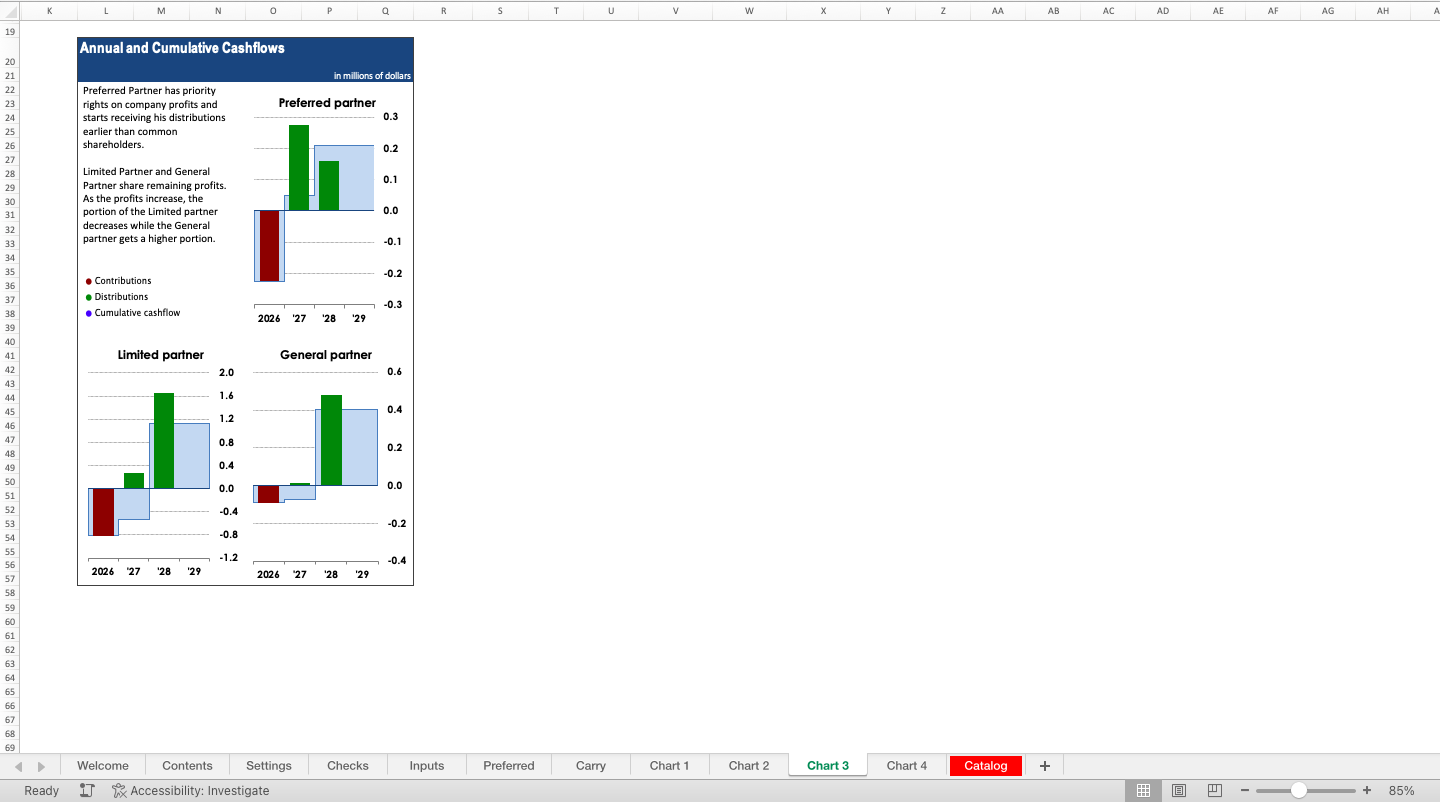

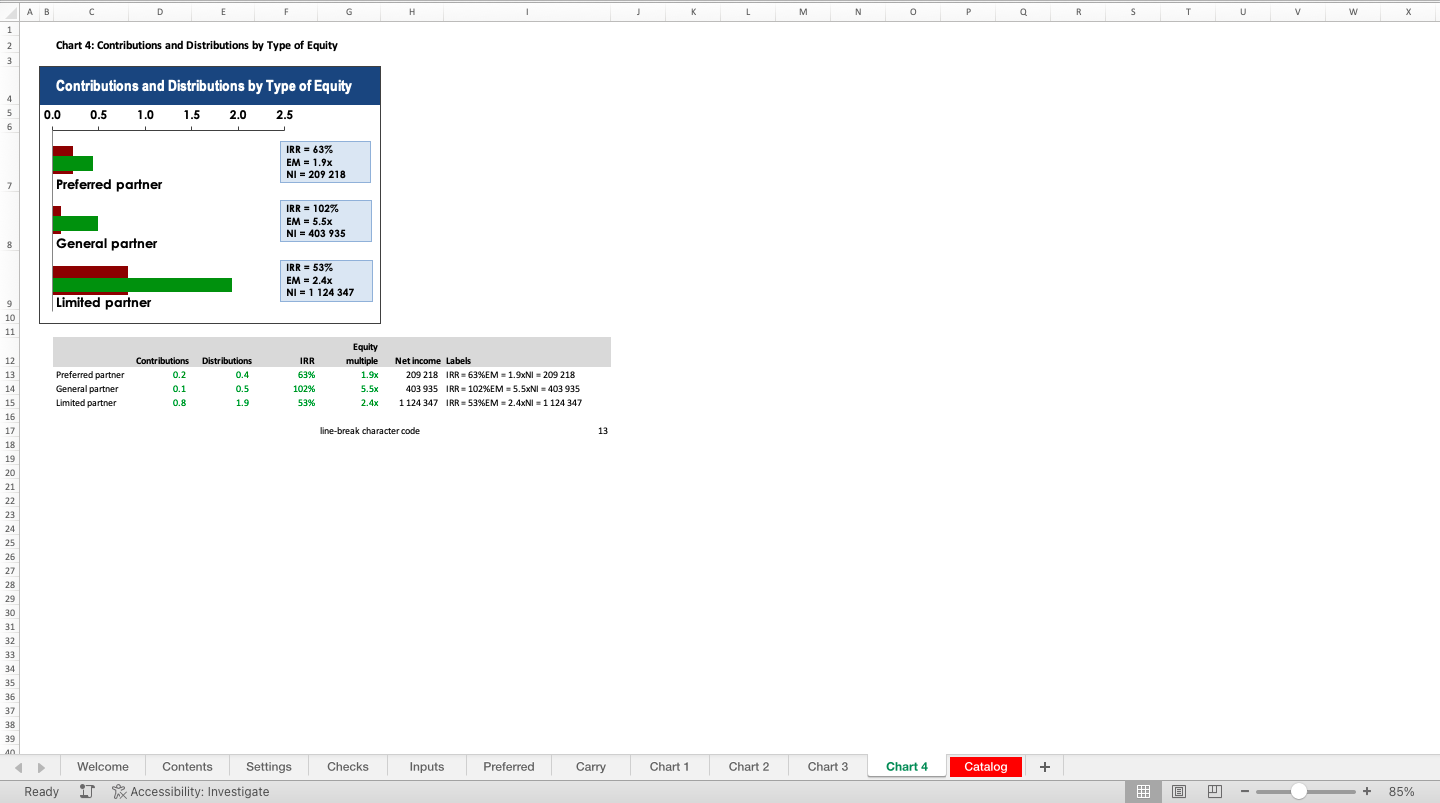

Profit Distribution and Carried Interest Waterfall

A template illustrating various setups of profit distribution between the JV partners with a carried interest waterfall

Further information

Calculate carried interest based on distribution waterfall

Joint ventures or partnerships with carried interest arrangements

Every project is unique and every model requires amendments and adjustments. Contact me if you need help with this or require an entire model done from scratch.