Originally published: 11/07/2022 08:56

Last version published: 09/12/2024 08:32

Publication number: ELQ-48120-3

View all versions & Certificate

Last version published: 09/12/2024 08:32

Publication number: ELQ-48120-3

View all versions & Certificate

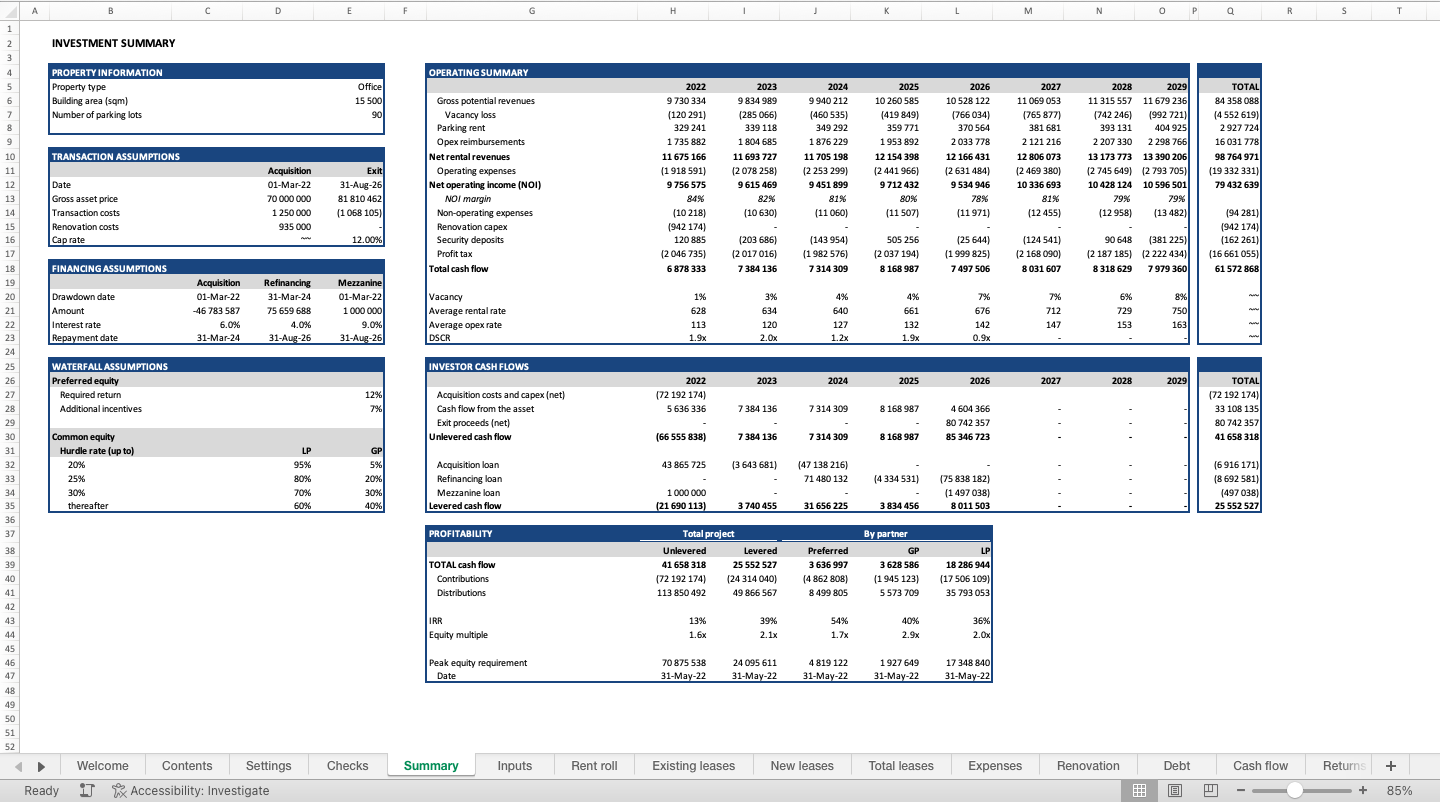

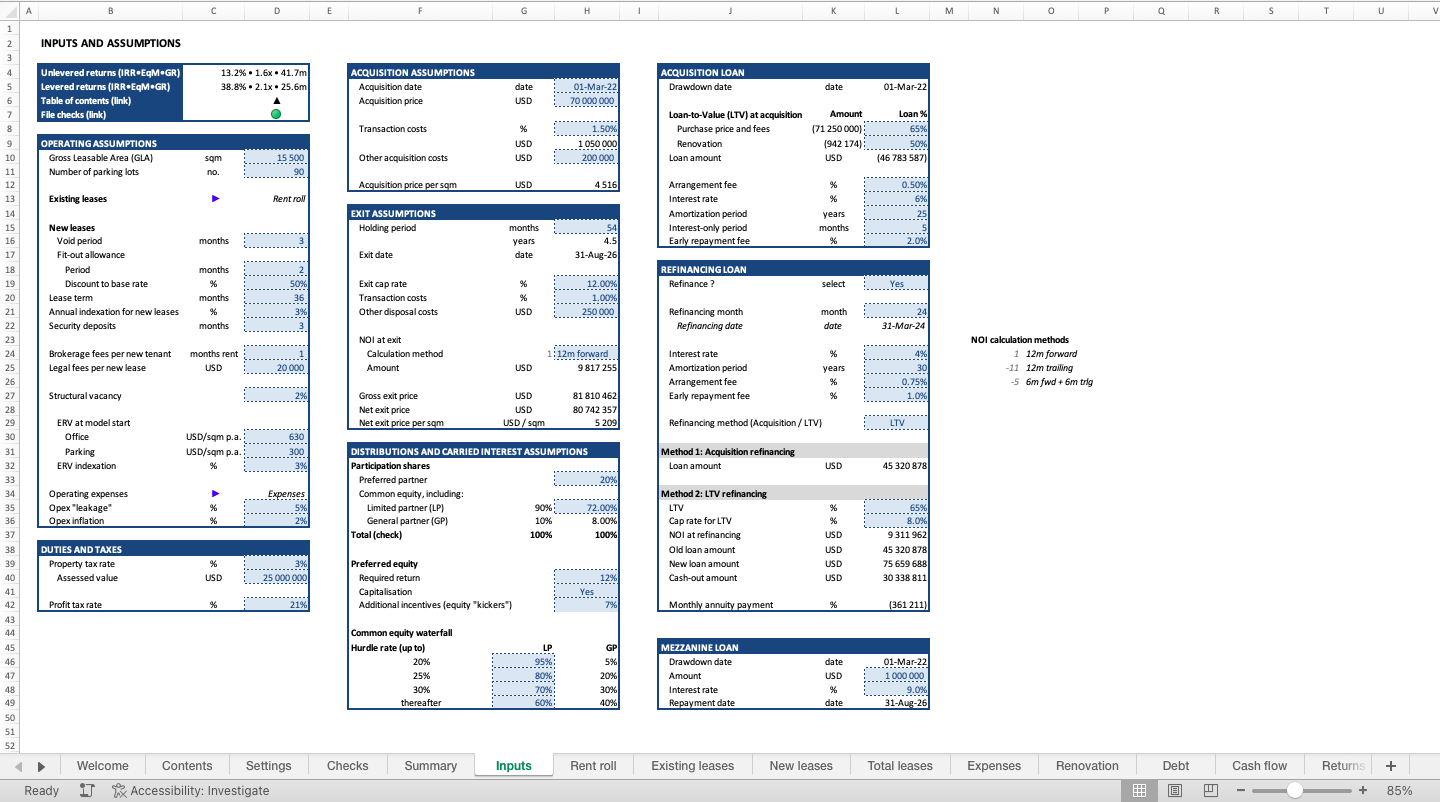

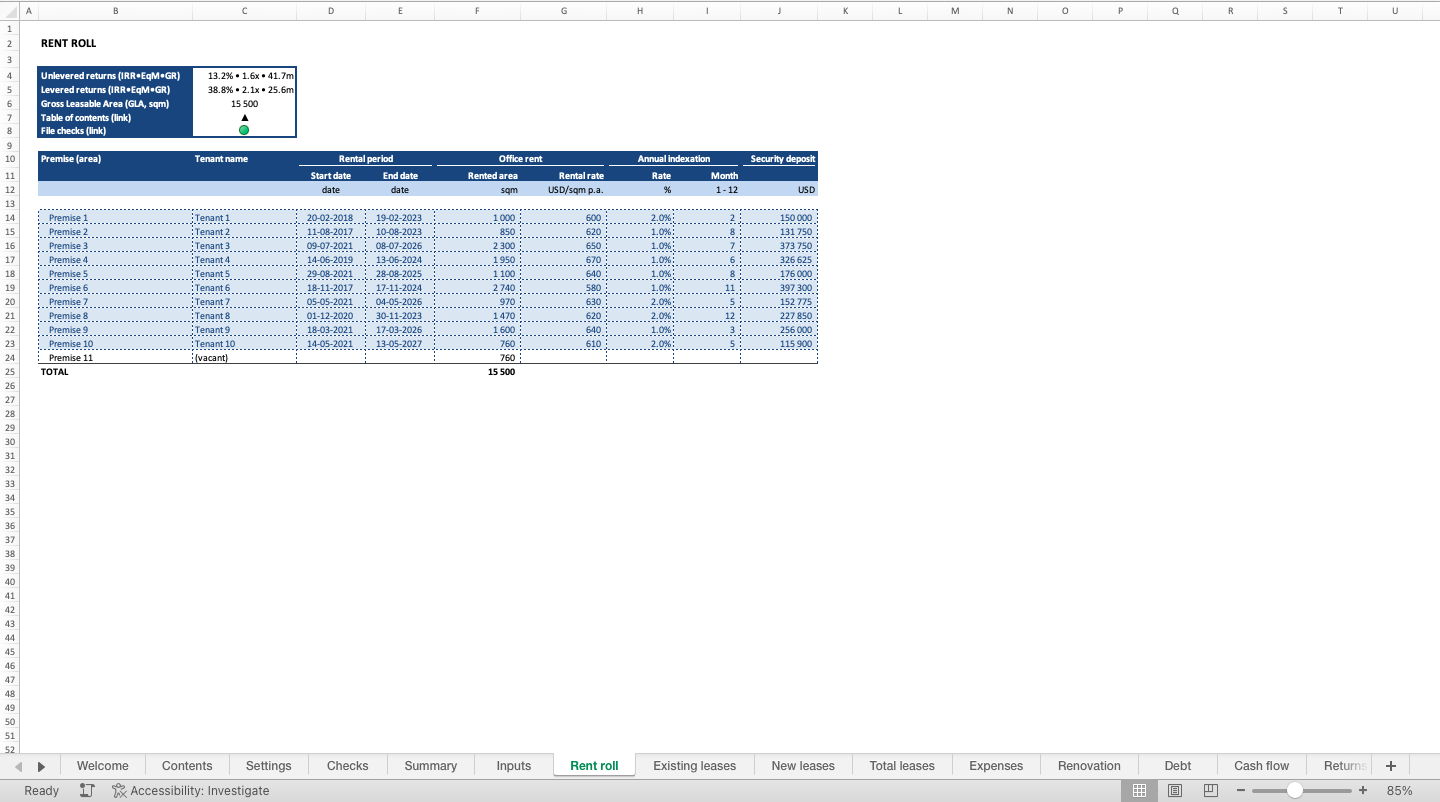

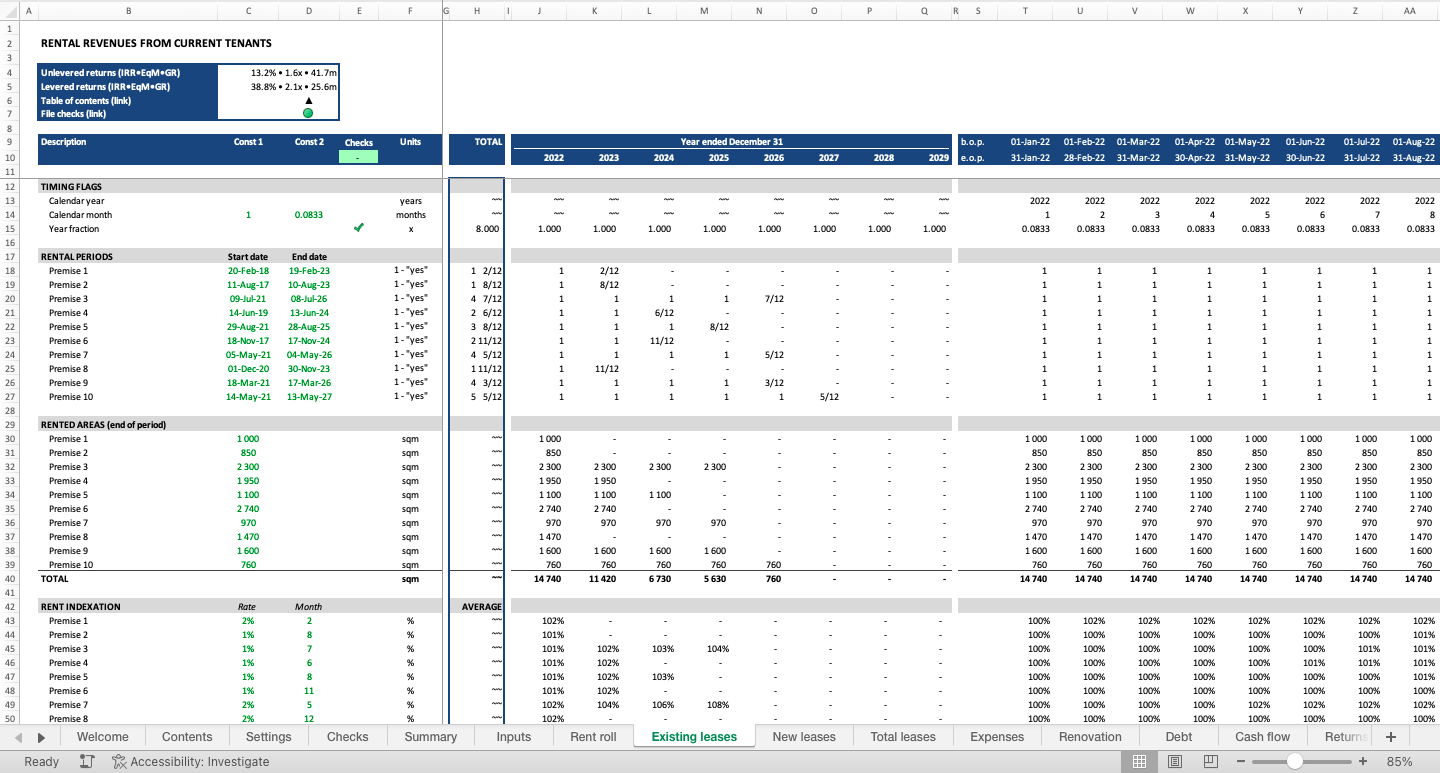

Office Acquisition Financial Model

A professional model for office acquisition

Further information

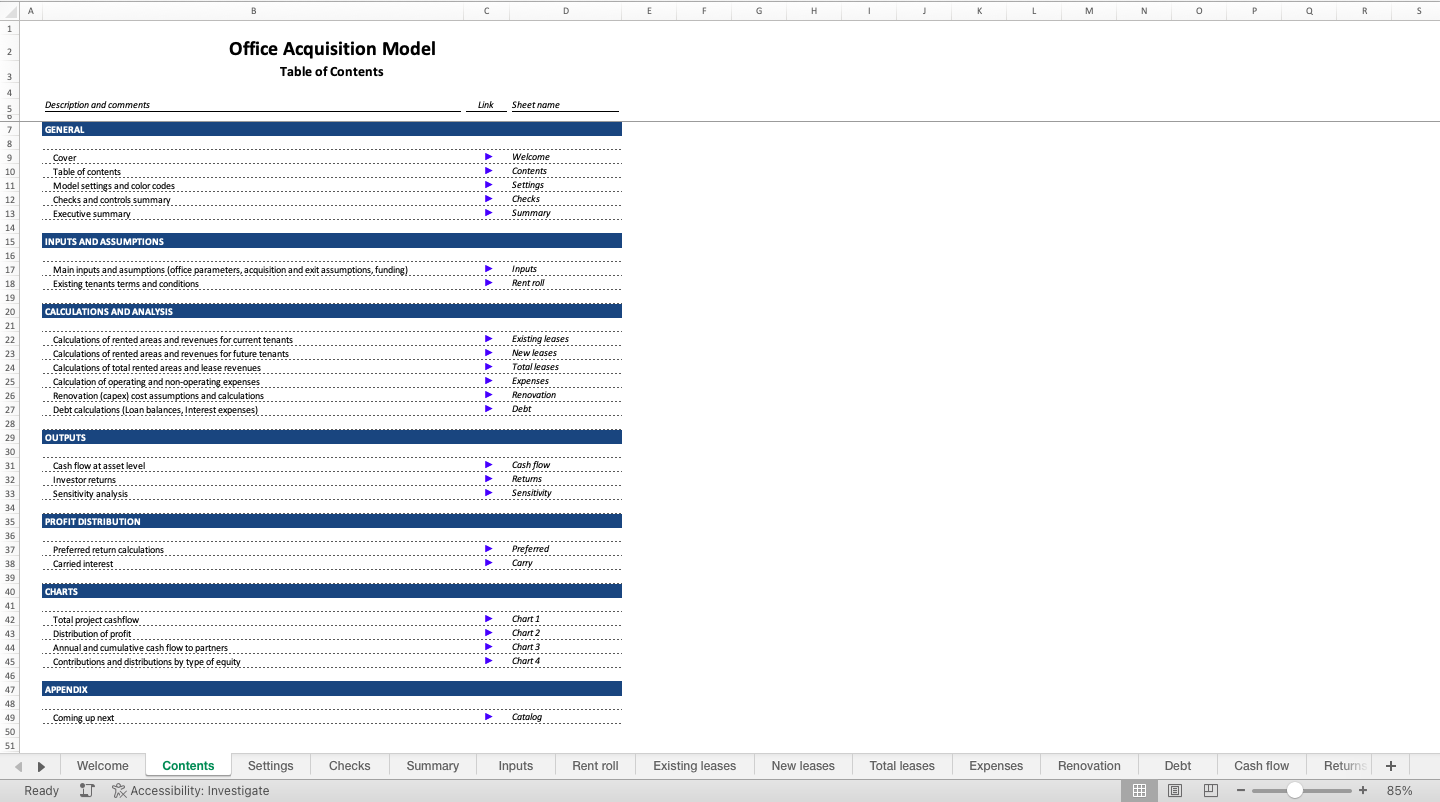

Develop a financial model for an acquisition of a stabilised office building

Investing into office real estate

Every investment is unique and so the model might need to be adjusted to your situation. Contact me if you need help tailoring this model or developing a new one.