Originally published: 30/04/2018 14:47

Last version published: 16/10/2018 09:19

Publication number: ELQ-38904-2

View all versions & Certificate

Last version published: 16/10/2018 09:19

Publication number: ELQ-38904-2

View all versions & Certificate

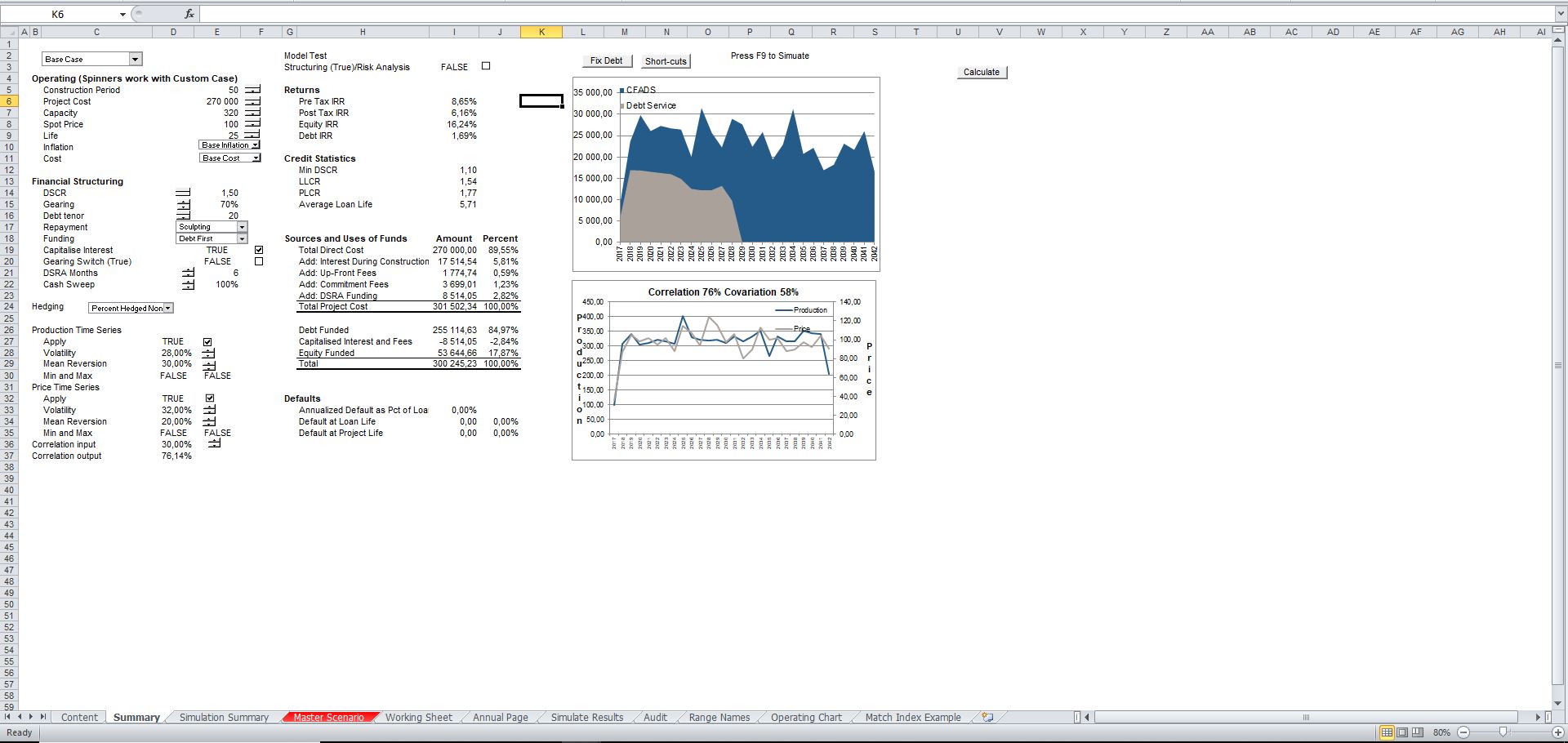

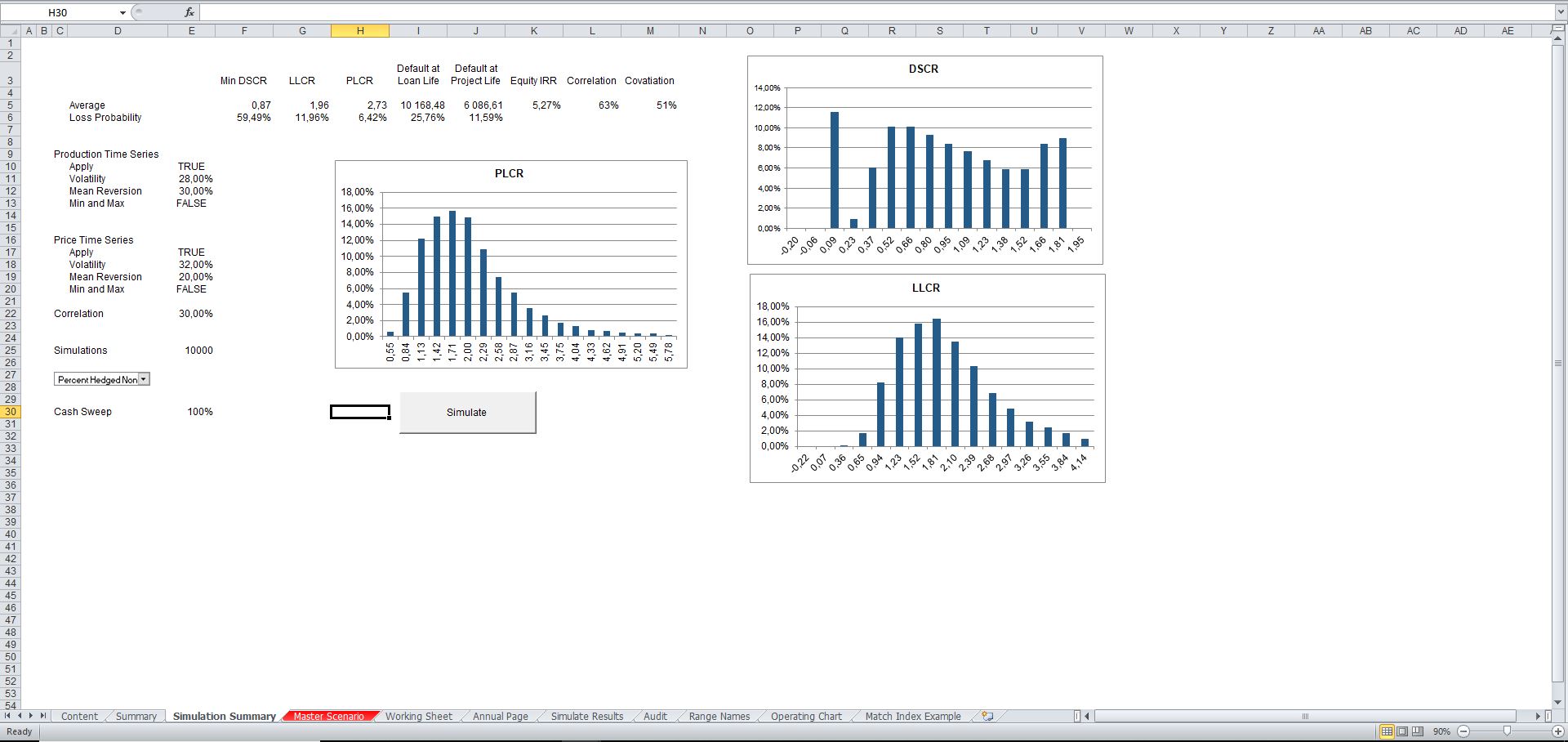

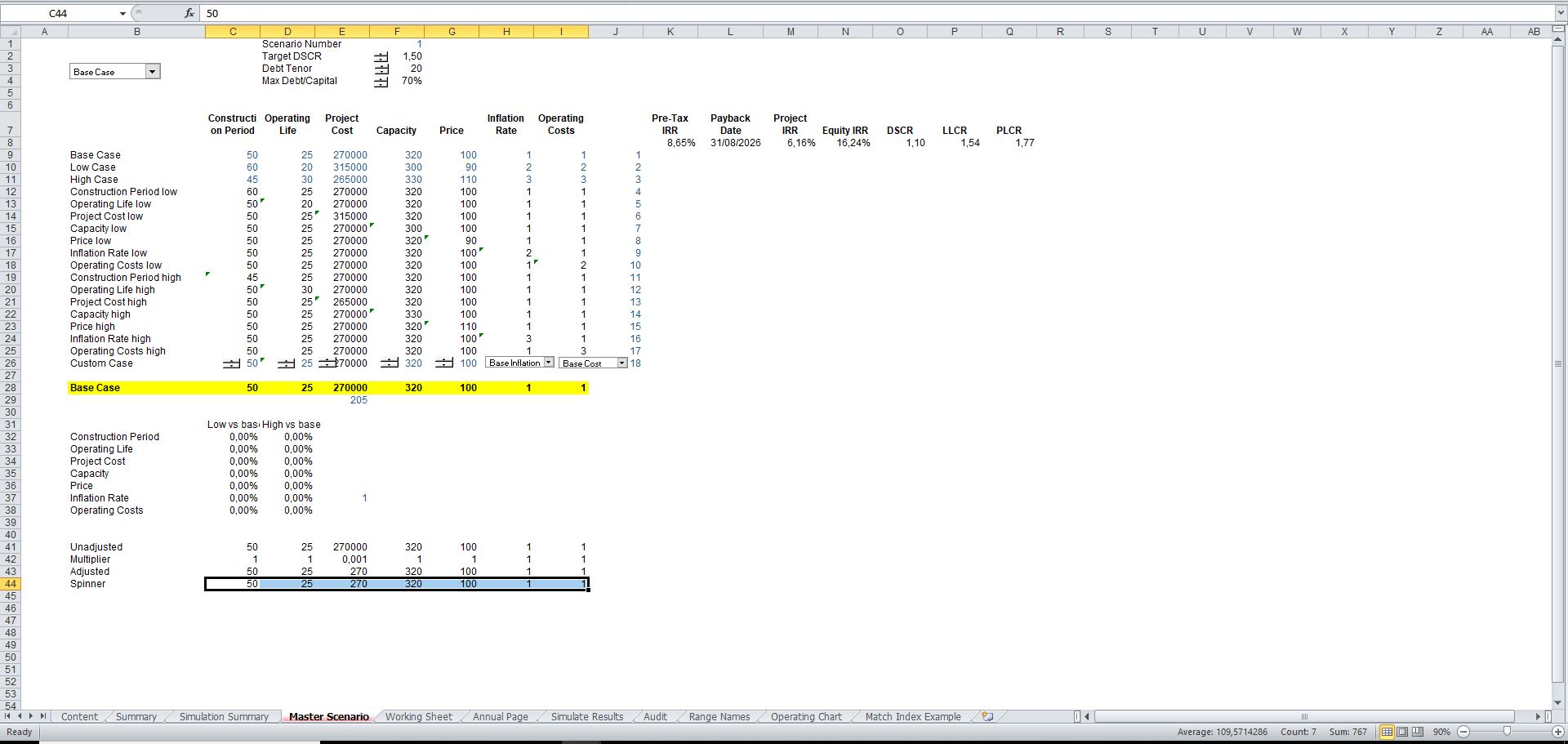

Commodity Price Risk and Monte Carlo Simulation - Project Finance Excel Model

A commodity price risk model with Monte Carlo simulation within a project finance excel model.