Originally published: 03/02/2025 08:53

Publication number: ELQ-20723-1

View all versions & Certificate

Publication number: ELQ-20723-1

View all versions & Certificate

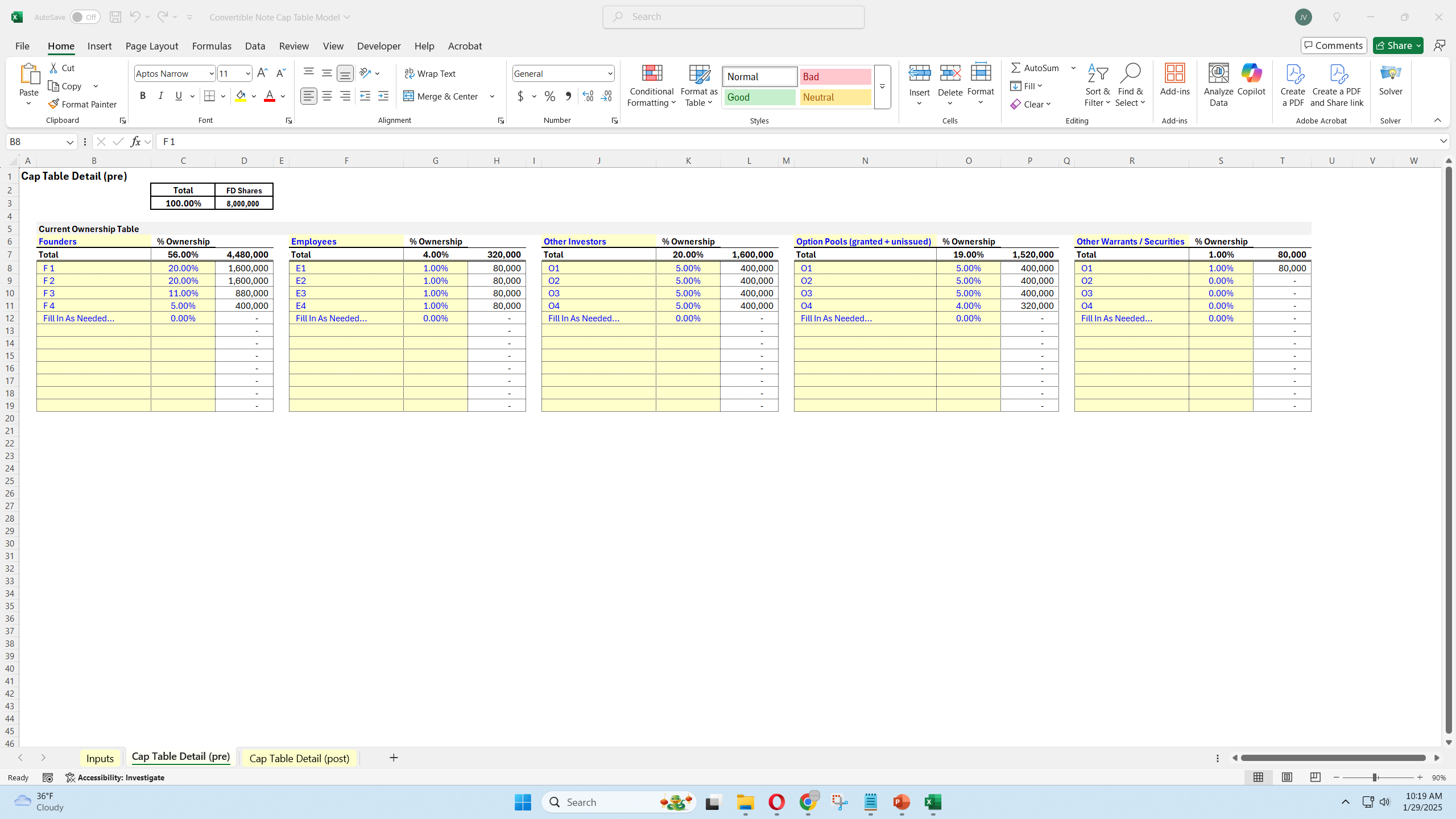

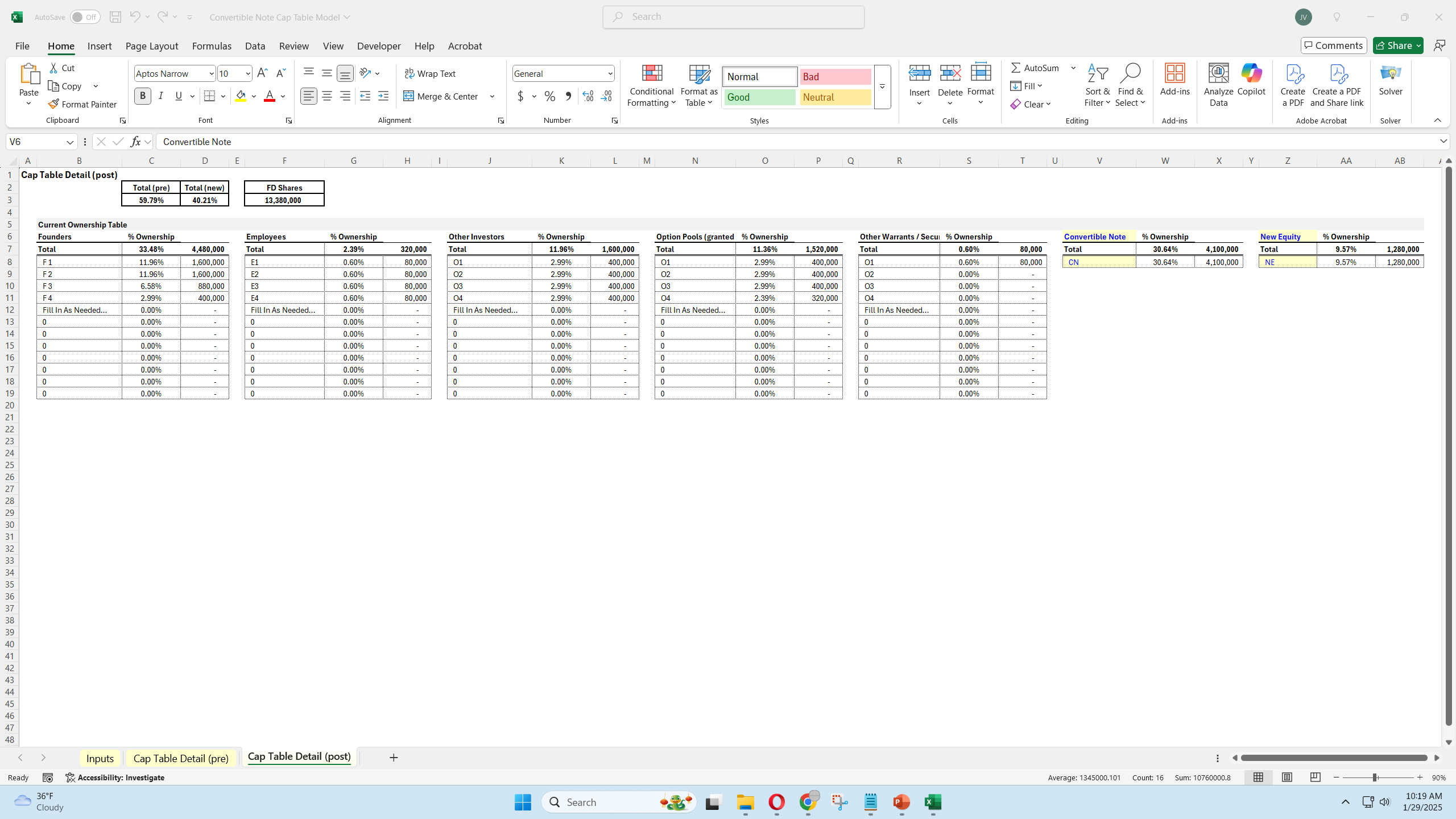

Cap Table with Sensitivity Table, Convertible Note, and Pre/Post-Money Analysis

A general cap table template designed to show dilution effect of a convertible note and/or a new equity raise on existing shareholders.

Description

1. What Is a Cap Table?

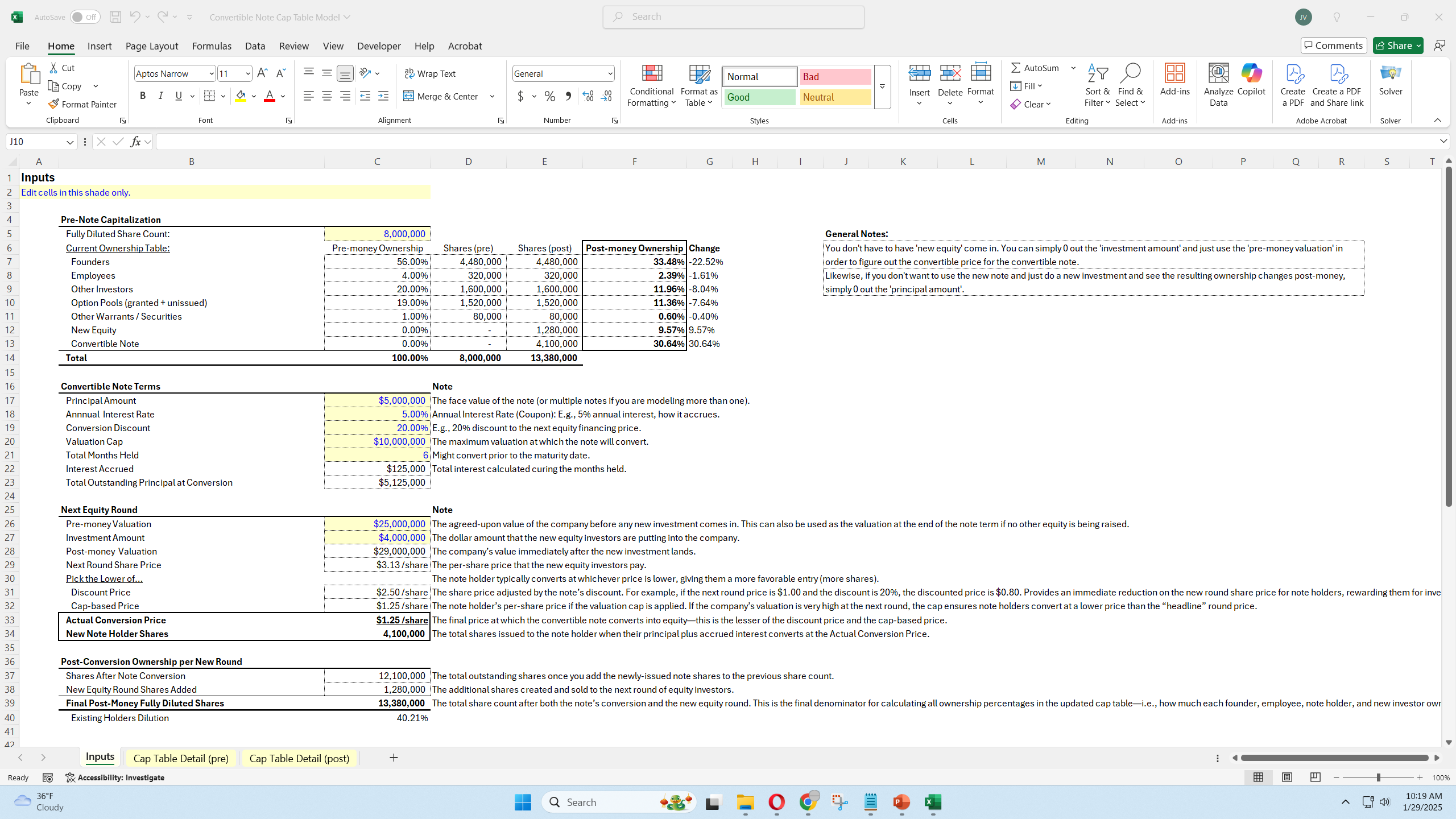

A capitalization table (cap table) is a spreadsheet or document that outlines the equity ownership in a company. It typically shows:

2. Understanding Convertible Notes

3. New Equity Raise

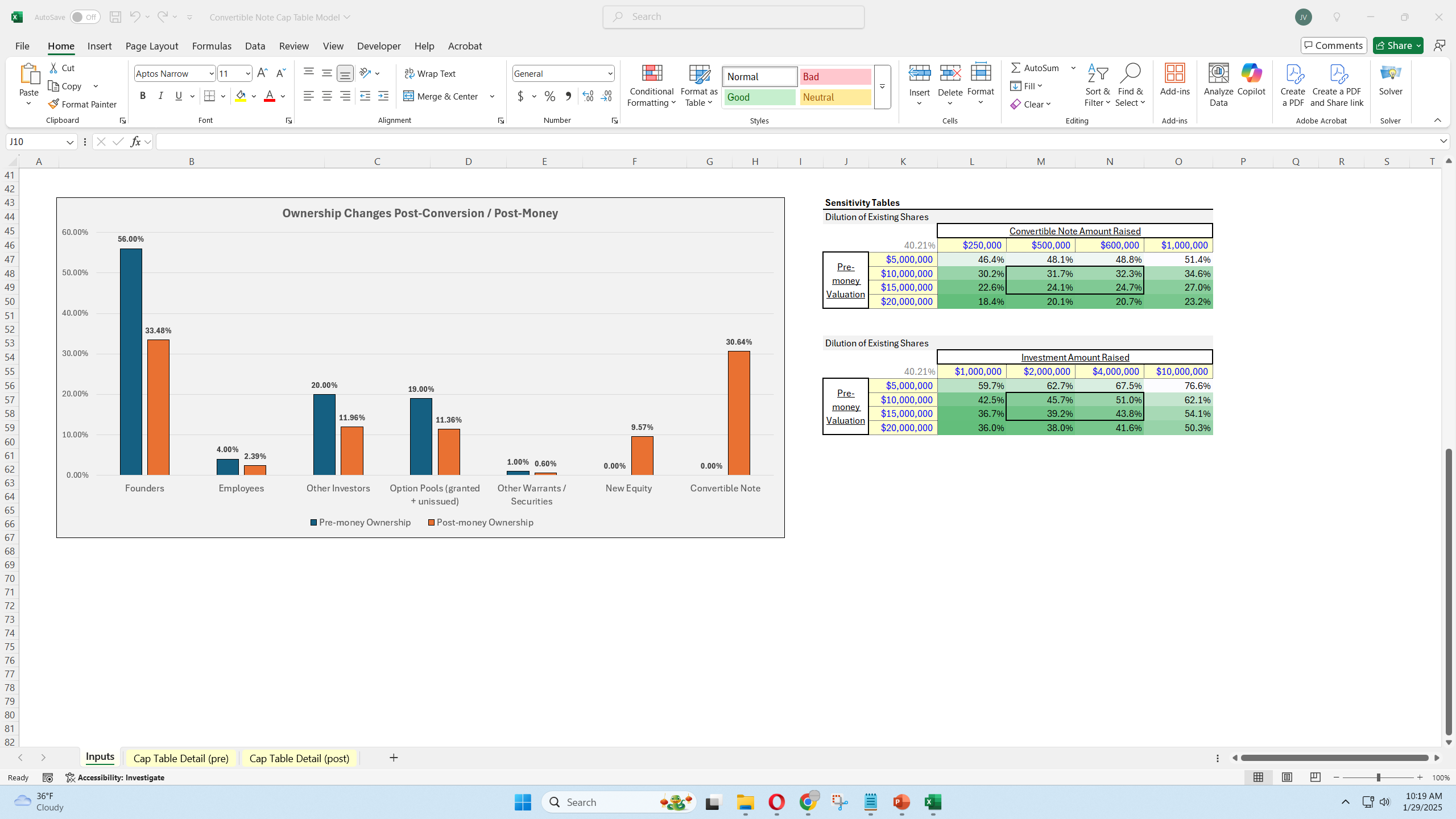

4. Dilution AnalysisDilution in a cap table context refers to the reduction in existing shareholders’ ownership percentages as a result of new shares being issued. In a scenario where you have convertible notes and an equity financing event:

5. Sensitivity AnalysisA sensitivity table can help model how different financing amounts (or convertible note principal balances) affect final ownership and valuations. For instance:

6. Bringing It All Together in the Template

7. Why This Analysis Is Important

1. What Is a Cap Table?

A capitalization table (cap table) is a spreadsheet or document that outlines the equity ownership in a company. It typically shows:

- Each class of security (common shares, preferred shares, options, warrants, etc.)

- The number of shares (or units) each owner holds

- The percentage ownership each stakeholder represents

- Any convertible instruments (e.g., notes, SAFEs) and their potential conversion mechanics

2. Understanding Convertible Notes

- Definition: A convertible note is a short-term debt instrument that typically converts into equity upon certain triggering events (often the next equity financing round).

- Conversion Mechanics:

- Discount Rate: The note holders receive a discount on the share price compared to new equity investors in the next round.

- Valuation Cap: The note might have a “cap” that sets the maximum valuation at which it can convert.

- Interest Accrual: The principal can grow over time as interest accrues, and at conversion, both principal and accrued interest often convert into equity.

- Effect on Ownership: Before conversion, the note is not counted as shares (it’s a debt). After conversion, the note holders become equity holders, causing dilution to existing shareholders.

3. New Equity Raise

- Definition: A new equity raise (sometimes referred to as a “priced round” or “Series A/B, etc.”) is when a company sells shares of its stock at a defined price per share.

- Pre-Money vs. Post-Money Valuation:

- Pre-Money: The valuation of the company before the new capital is added.

- Post-Money: The valuation of the company after the new capital is added.

- Dilution: When new shares are issued, all existing shareholders’ ownership percentages typically go down unless they invest proportionately in the new round.

4. Dilution AnalysisDilution in a cap table context refers to the reduction in existing shareholders’ ownership percentages as a result of new shares being issued. In a scenario where you have convertible notes and an equity financing event:

- Convertible Note Conversion:

- The note holders convert into equity at a certain share price (which might be discounted or capped).

- This creates new shares, diluting existing owners.

- New Equity Round:

- Additional shares are created and sold to new (or sometimes existing) investors.

- This further dilutes existing owners (including, by now, the converted note holders).

5. Sensitivity AnalysisA sensitivity table can help model how different financing amounts (or convertible note principal balances) affect final ownership and valuations. For instance:

- Varying Convertible Note Principal:

- If the principal is higher, when the note converts, the number of shares created is greater (all else equal).

- This leads to a larger ownership percentage for note holders and more dilution to existing shareholders.

- Varying Equity Raised:

- Raising more money at a fixed valuation means issuing more shares, increasing dilution.

- Conversely, if the company raises less, existing shareholders hold a greater proportion.

6. Bringing It All Together in the Template

- Pre-Transaction Ownership: Start with a snapshot of ownership before the note converts or new equity is raised. This typically includes:

- Founders’ shares

- Equity allocated for employees (option pool)

- Any existing angel or seed investor shares

- Convertible Note Section:

- Principal, accrued interest, conversion discount, valuation cap (if applicable)

- Calculations showing how many new shares will be issued upon conversion under different assumptions

- Equity Raise Section:

- Pre-money valuation or share price

- Amount of capital to be raised

- Resulting share issuance and ownership

- Dilution Analysis:

- Show the revised ownership for each stakeholder after the note conversion and new equity raise

- Highlight the resulting percentages for each founder, existing investors, employee option pool, and new investors

- Sensitivity Table:

- Columns/rows that vary key assumptions (e.g., amount of note principal, interest rate, new equity amount, or share price)

- Updated ownership percentages based on each scenario

7. Why This Analysis Is Important

- Strategic Decision-Making: Founders and management can see how different financing scenarios impact their long-term ownership and control of the company.

- Investor Transparency: Potential investors appreciate clarity on how previous convertible notes will convert, ensuring there are no surprises about final ownership percentages.

- Negotiation Tool: With clear visuals and data-driven insights, stakeholders can negotiate valuation, discount rates, or share prices with a better understanding of the downstream effects on everyone’s ownership.

This Best Practice includes

1 Excel model and 1 Tutorial Video

Further information

Provide information about each equity ownership group after a convertible note converts and/or a new equity raise round happens.

Any startup that is raising money.