Originally published: 25/02/2021 08:33

Publication number: ELQ-65571-1

View all versions & Certificate

Publication number: ELQ-65571-1

View all versions & Certificate

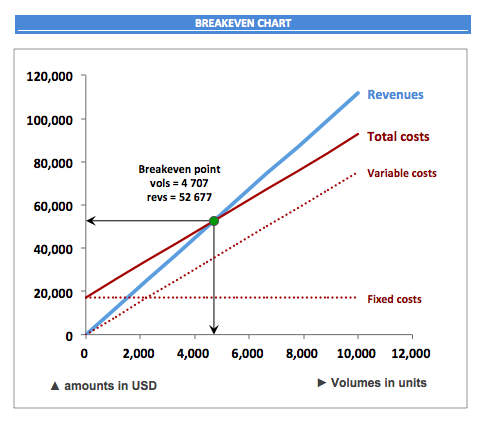

Cost-Volume-Profit (Breakeven) Analysis

A template to perform cost-volume-profit (CVP, or breakeven) analysis

Further information

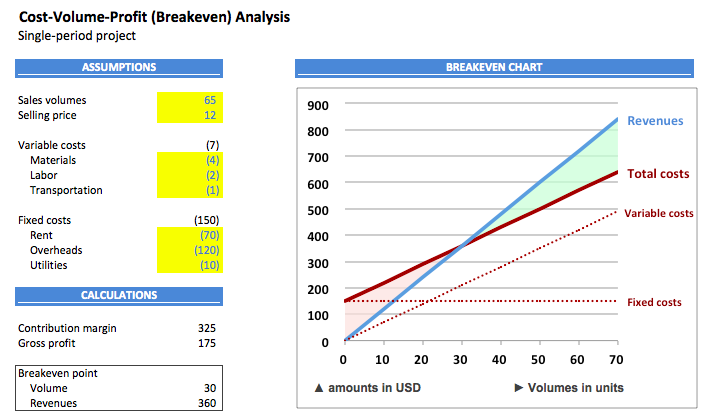

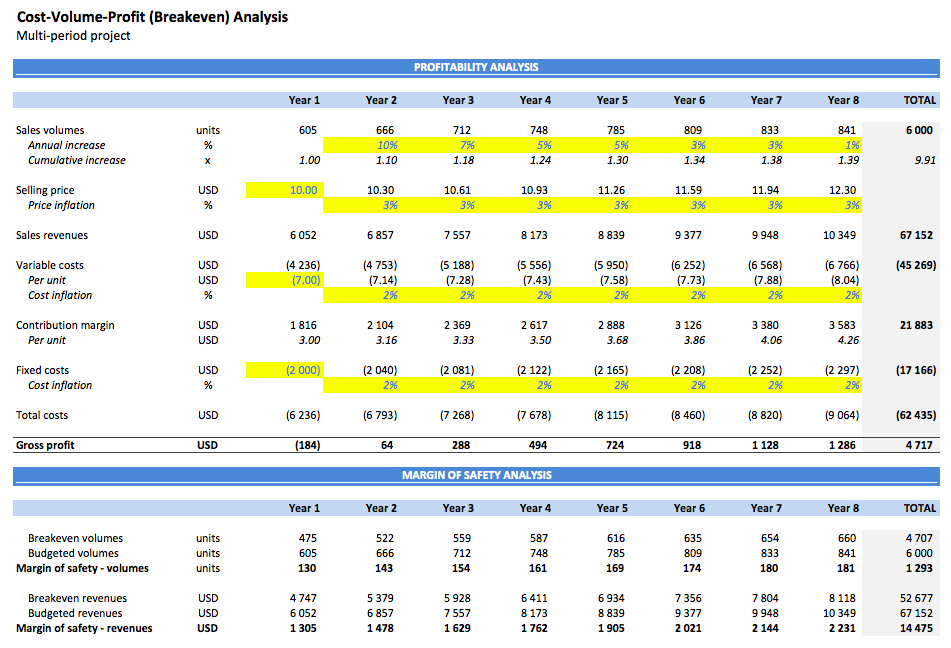

Carry out cost-volume-profit (breakeven) analysis

A manufacturer producing commodities with fixed and variable costs

See the limitations of CVP analysis in the description