Originally published: 17/10/2022 08:23

Last version published: 05/02/2025 08:08

Publication number: ELQ-26521-3

View all versions & Certificate

Last version published: 05/02/2025 08:08

Publication number: ELQ-26521-3

View all versions & Certificate

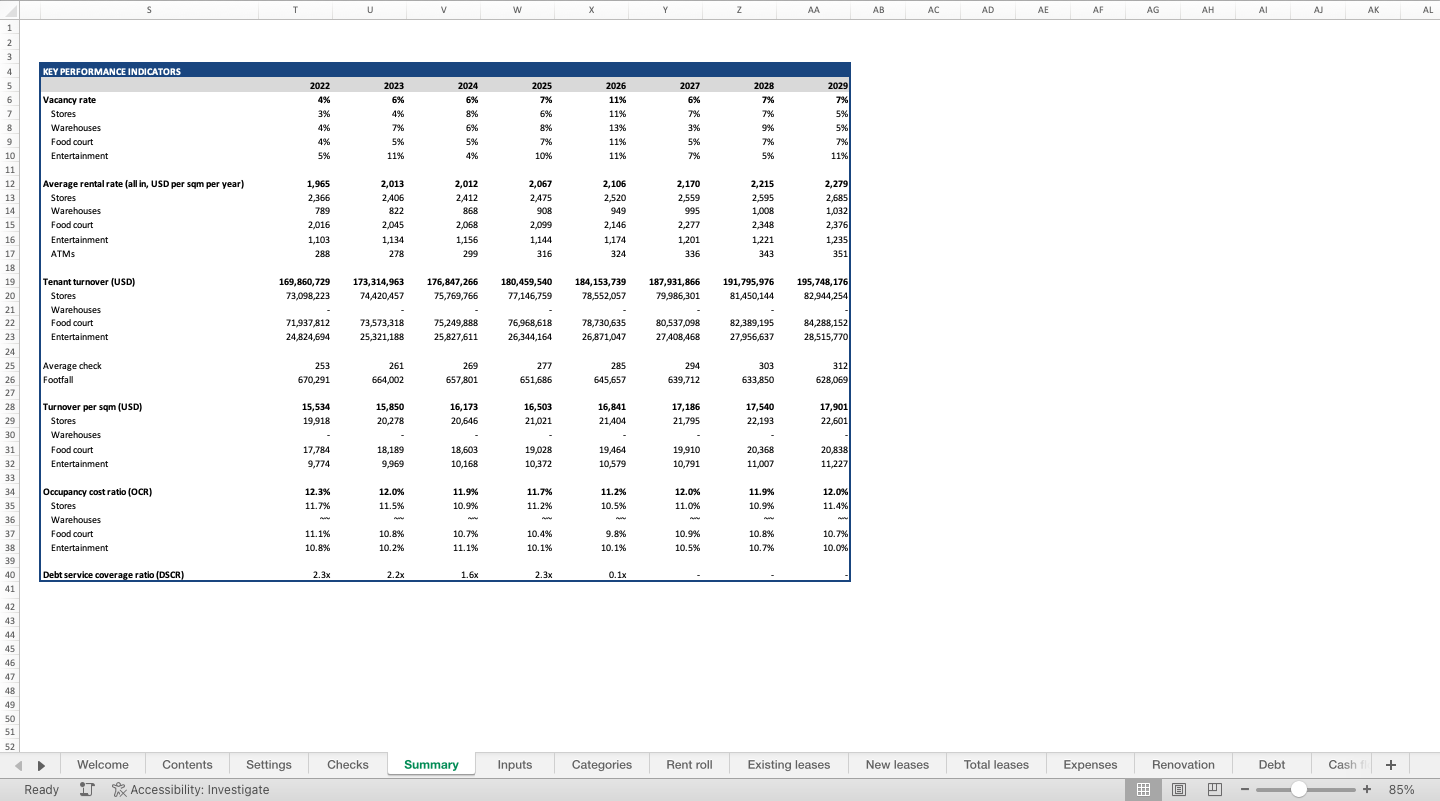

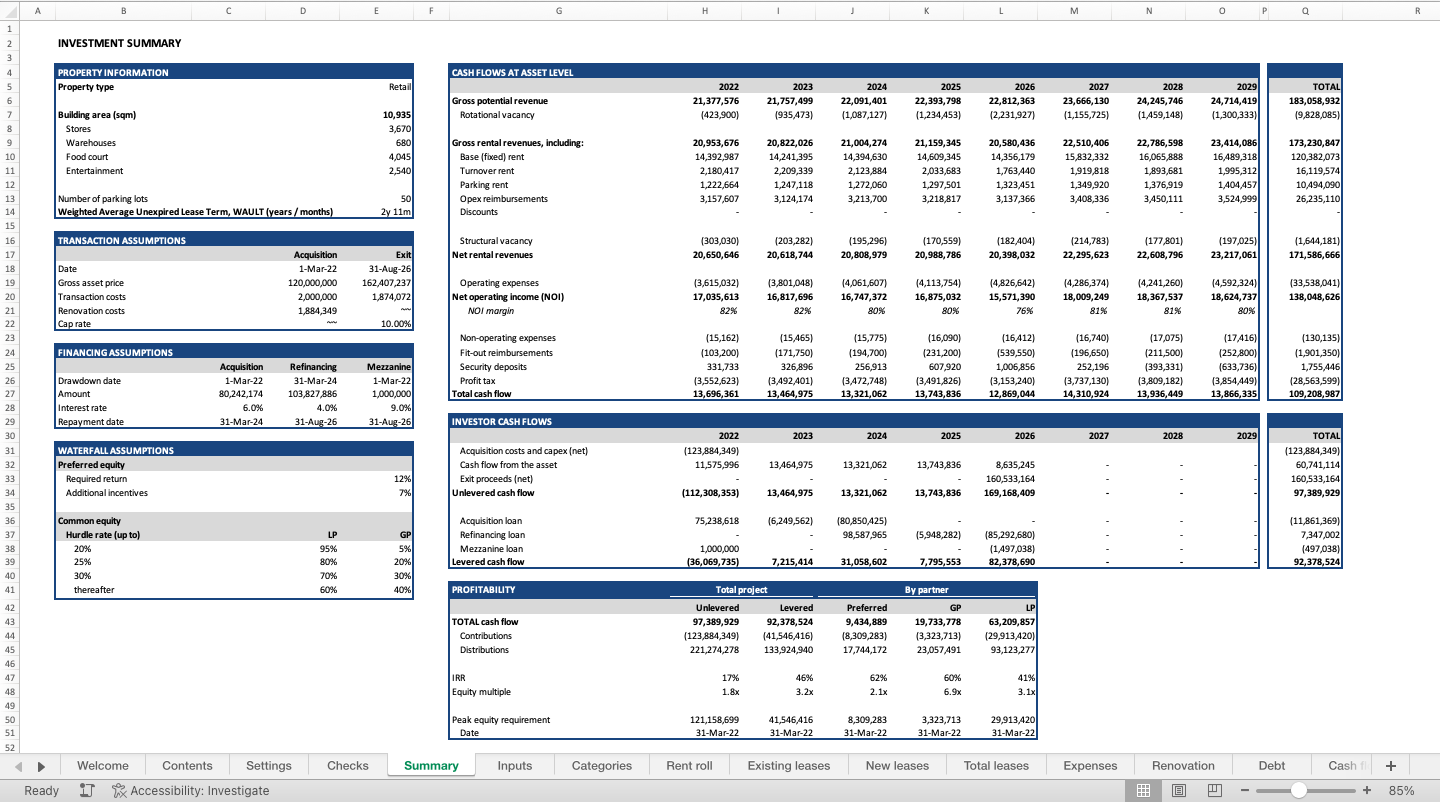

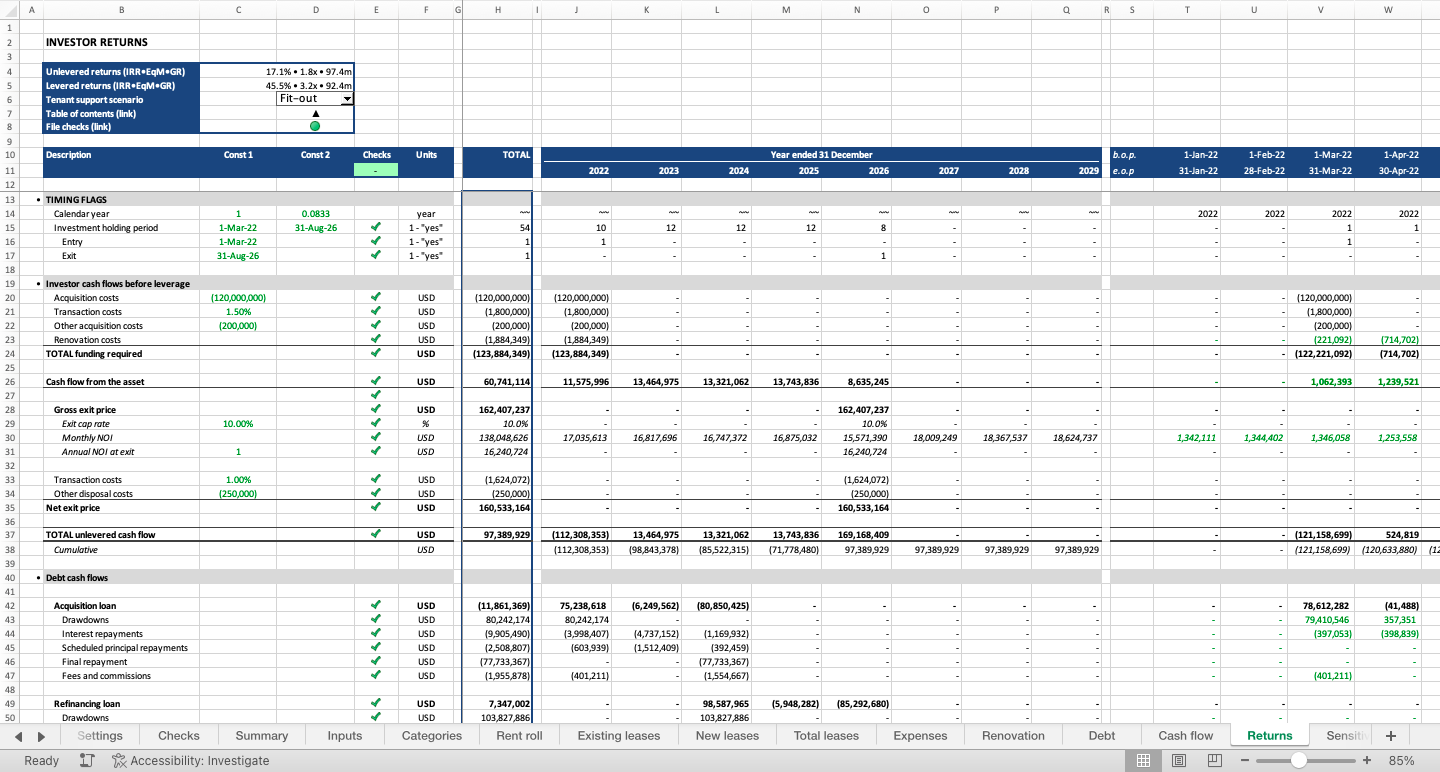

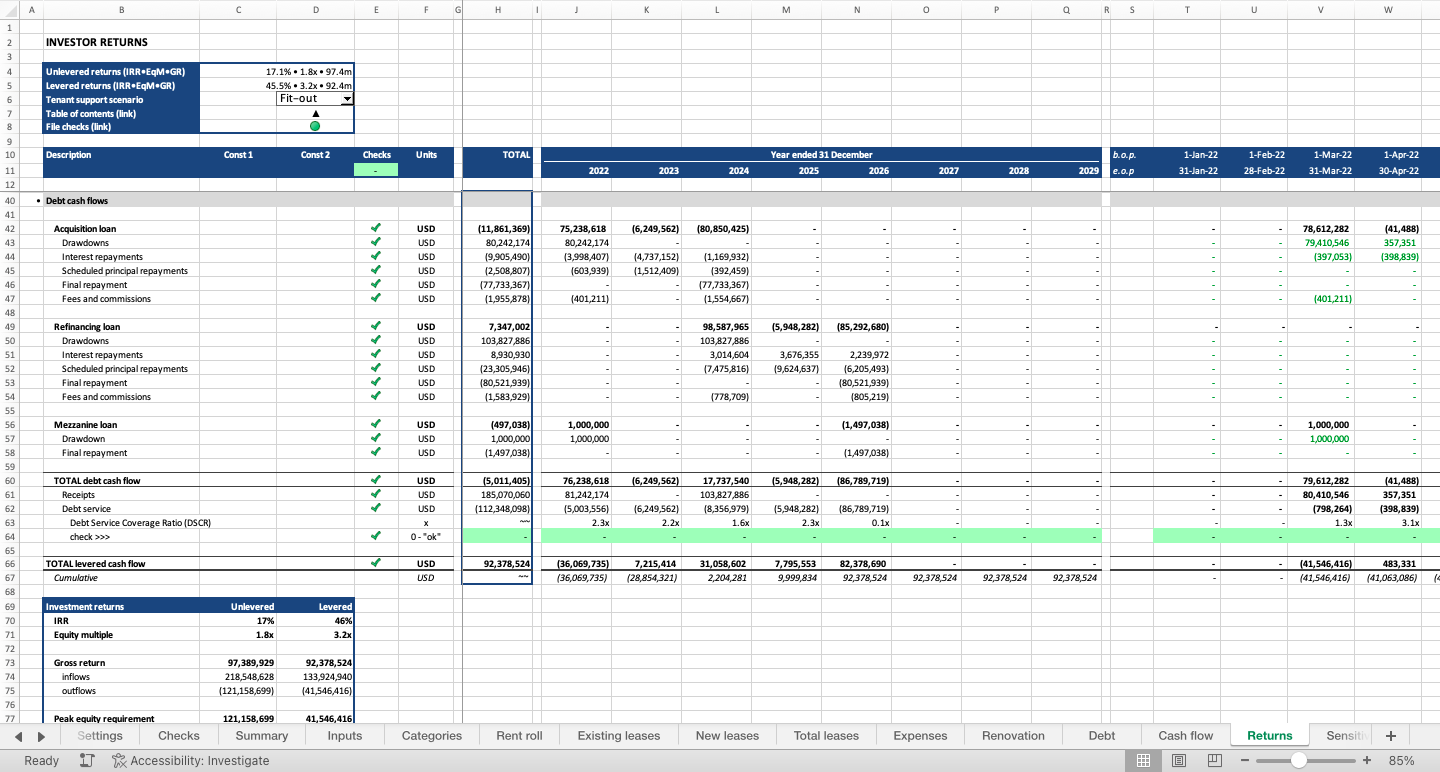

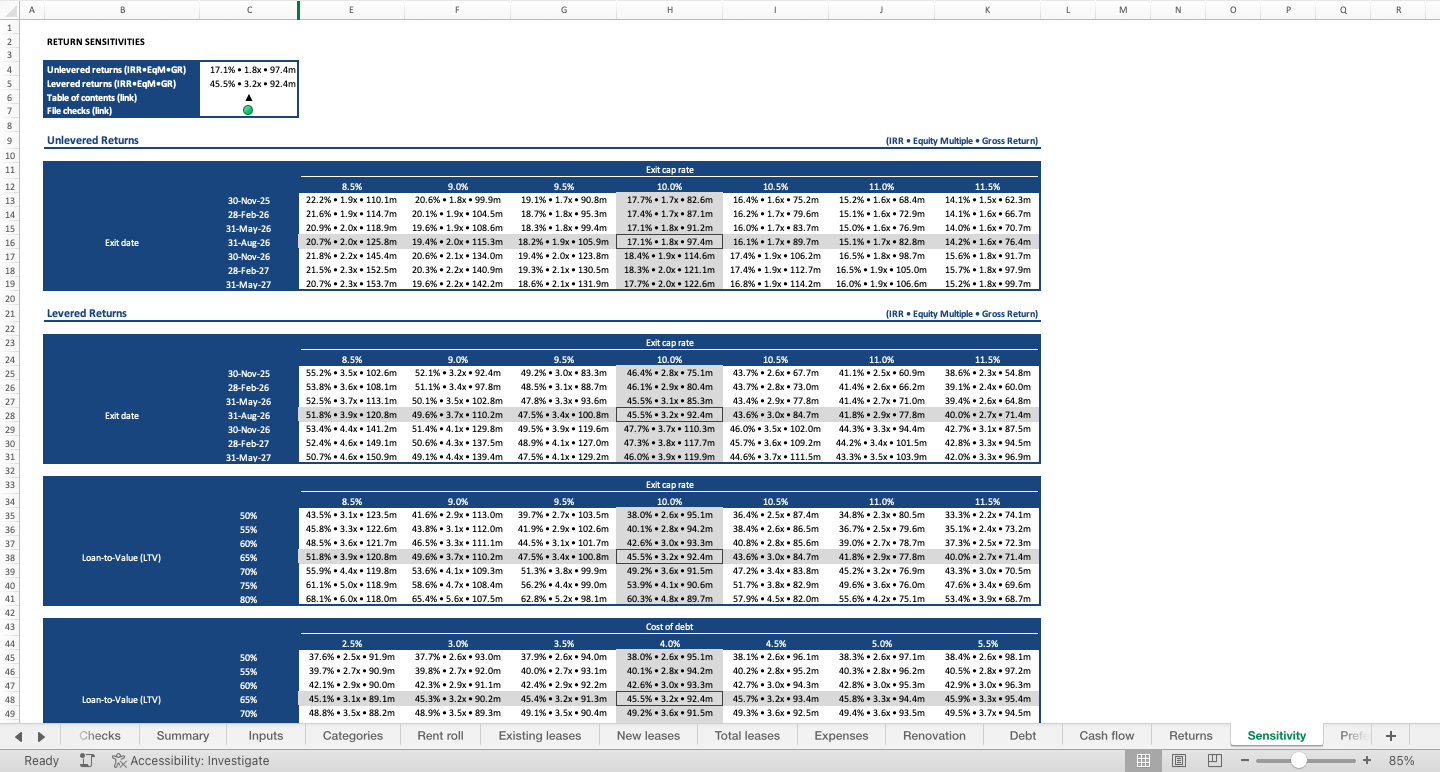

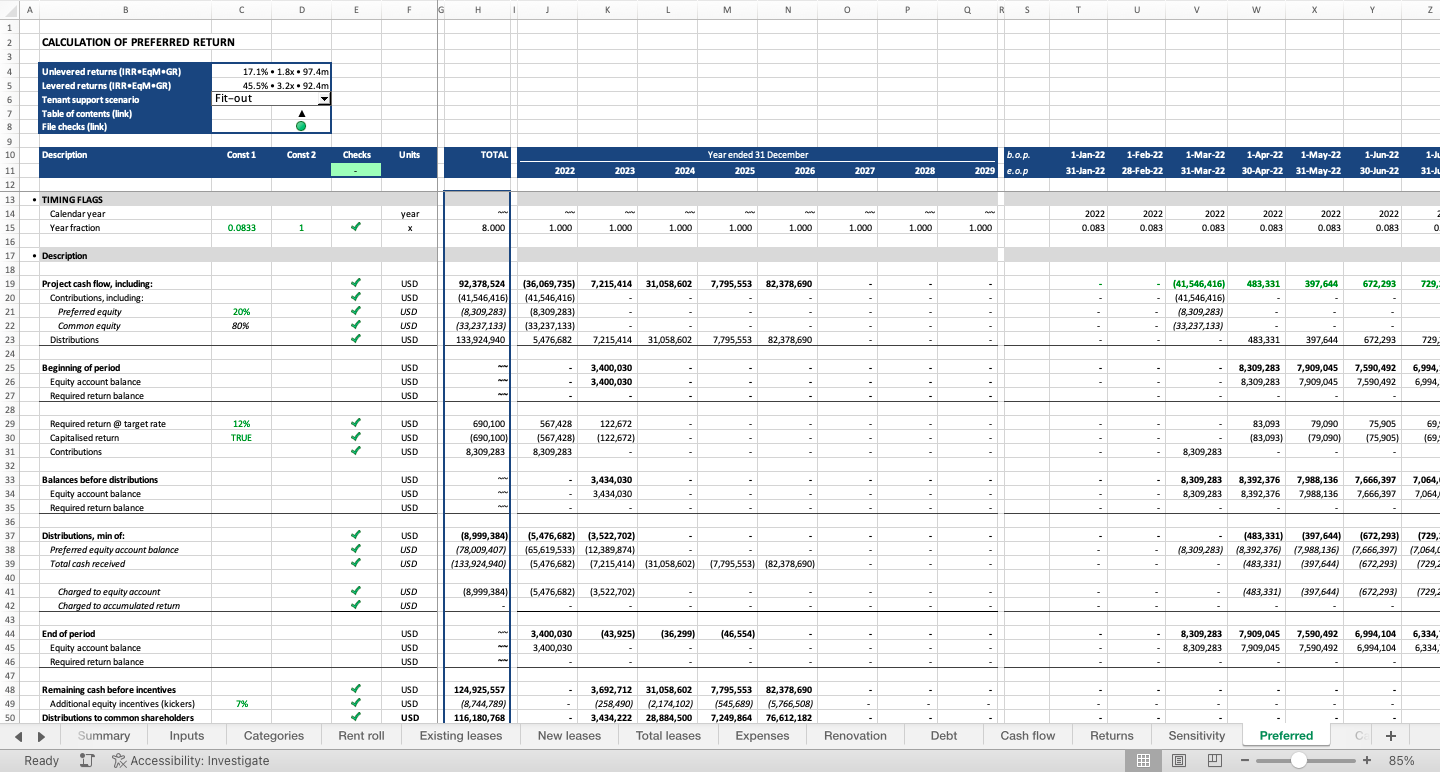

Retail Property Acquisition Financial Model

A professional model for retail property acquisition (buy – hold – sell)

Further information

Calculate future cash flows, returns and sensitivity for the acquisition of a retail property (shopping center, mall, etc.)

Use this model if you are considering investing into a development of a retail property

Every investment is unique and so the model might need to be adjusted to your situation. Contact me if you need help tailoring this model or developing a new one.