Originally published: 23/03/2017 13:24

Last version published: 28/03/2025 13:29

Publication number: ELQ-92315-16

View all versions & Certificate

Last version published: 28/03/2025 13:29

Publication number: ELQ-92315-16

View all versions & Certificate

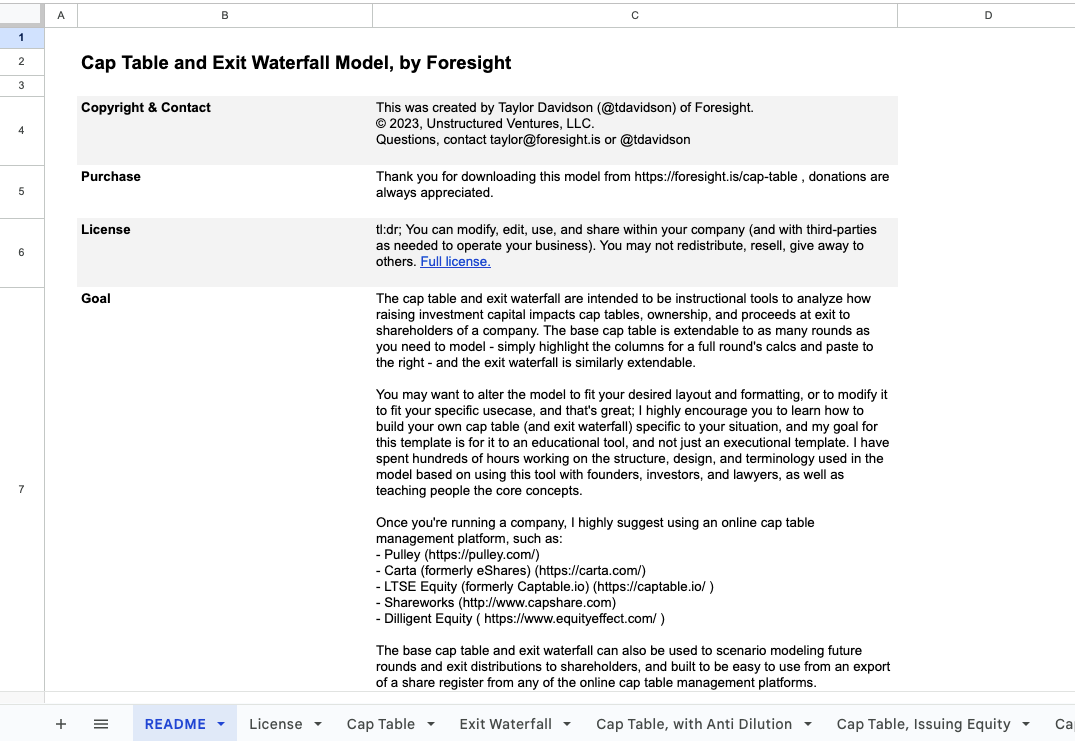

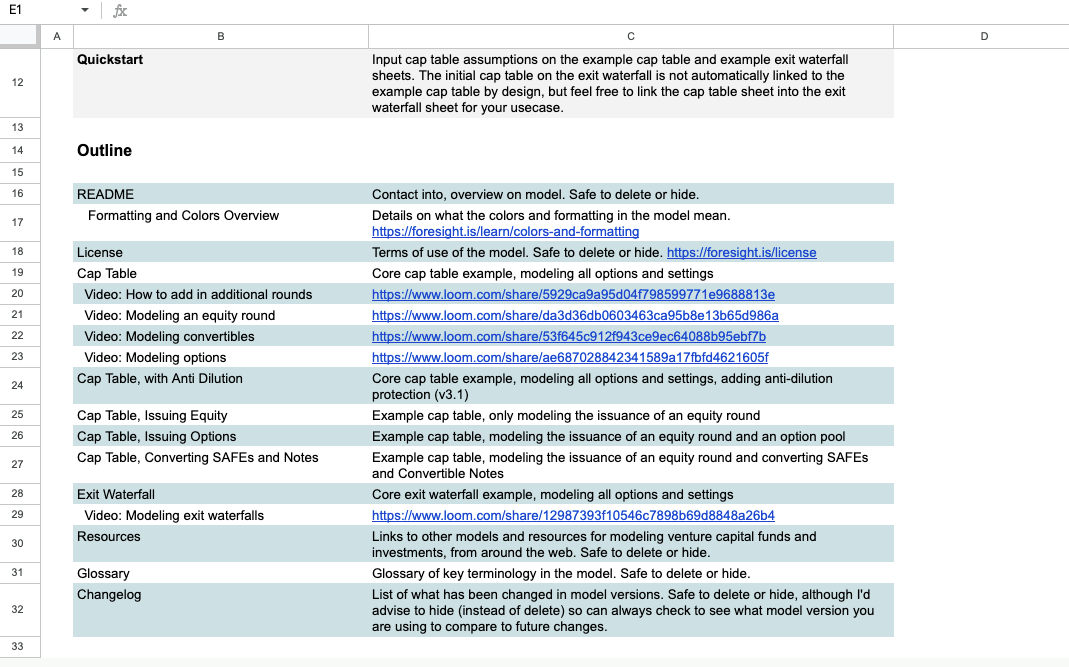

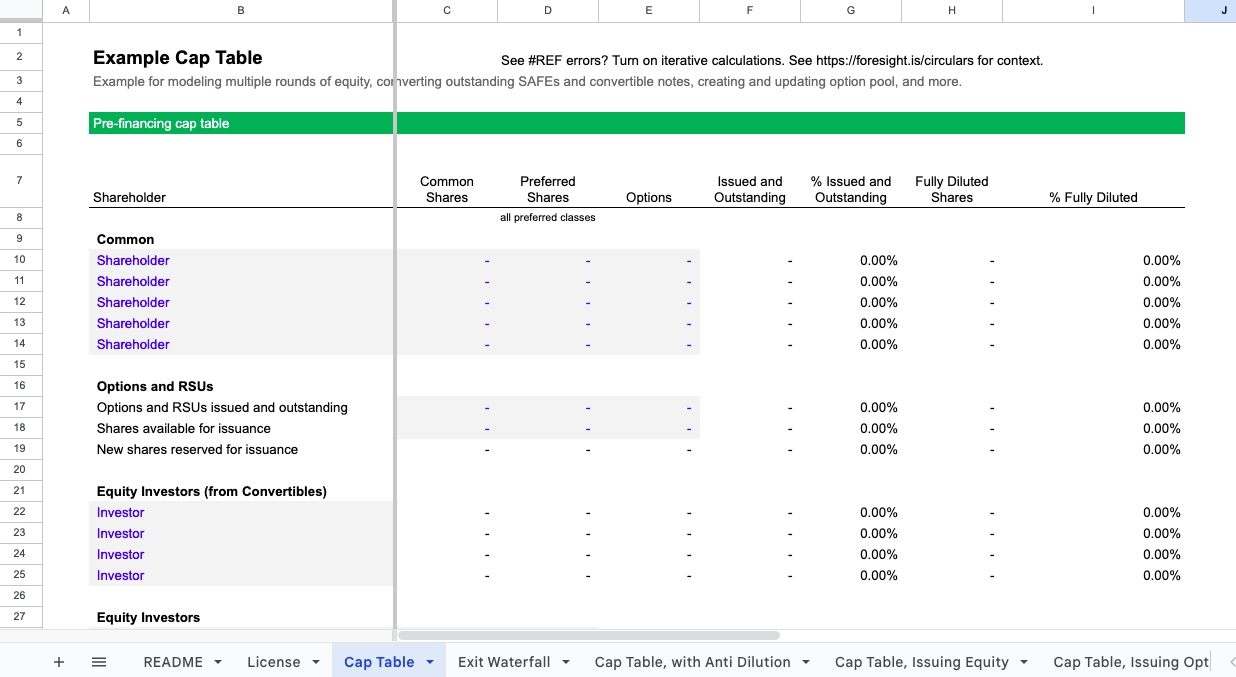

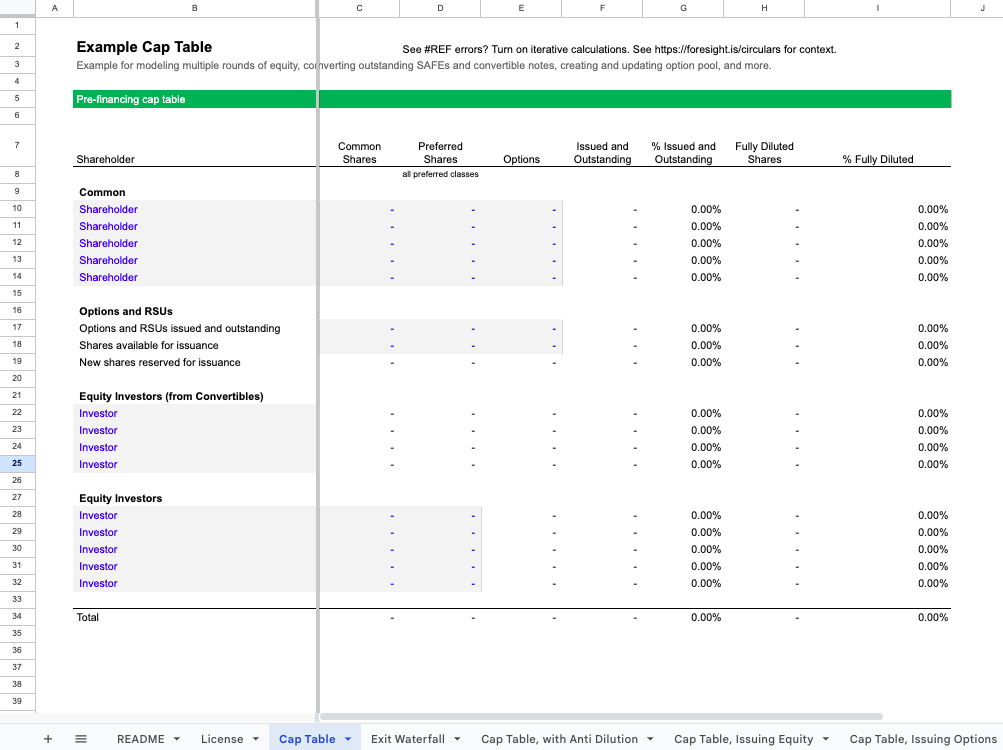

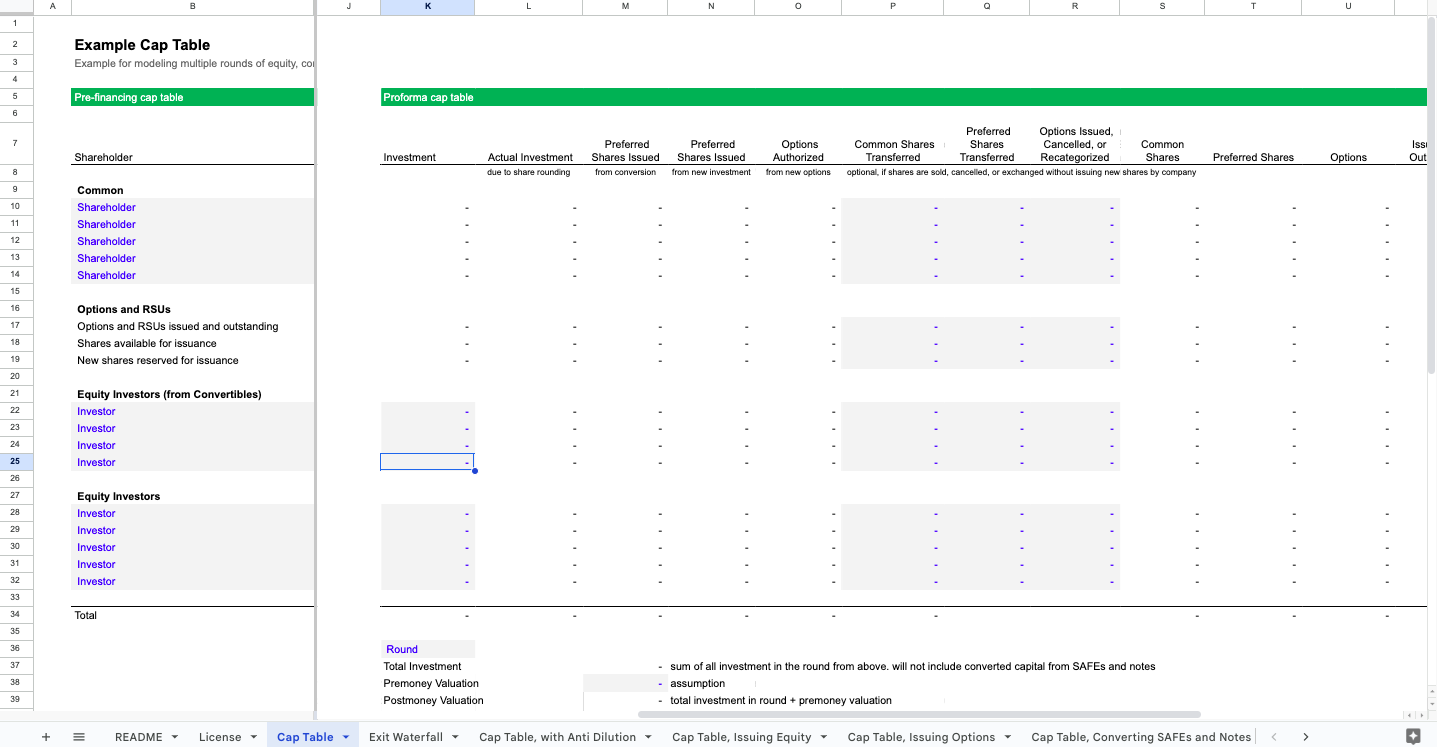

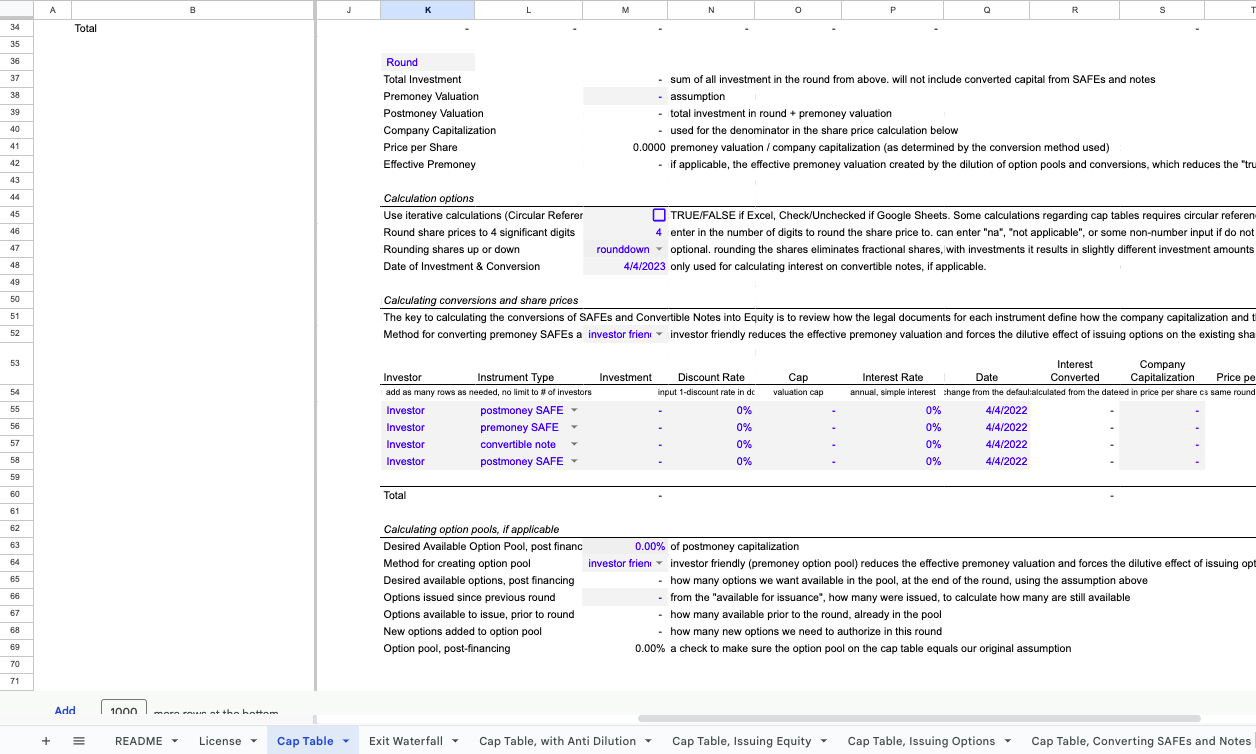

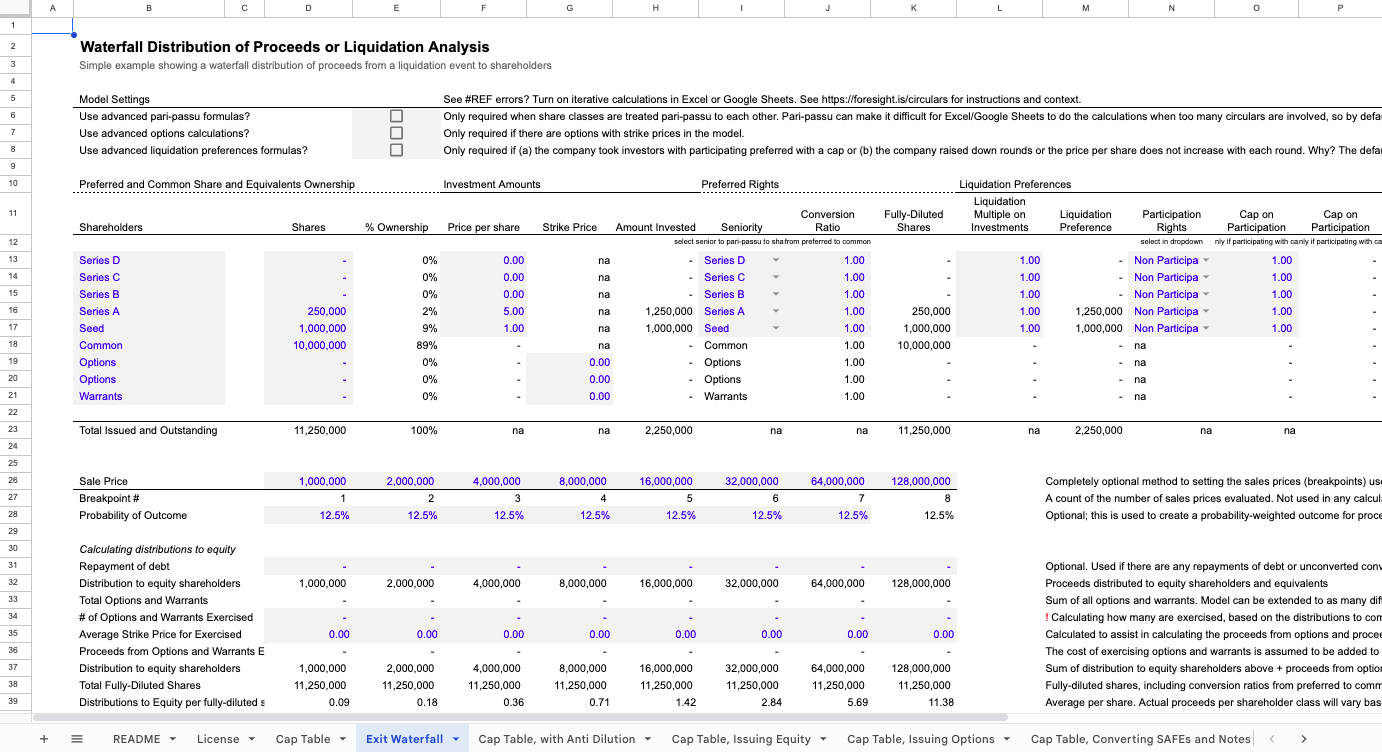

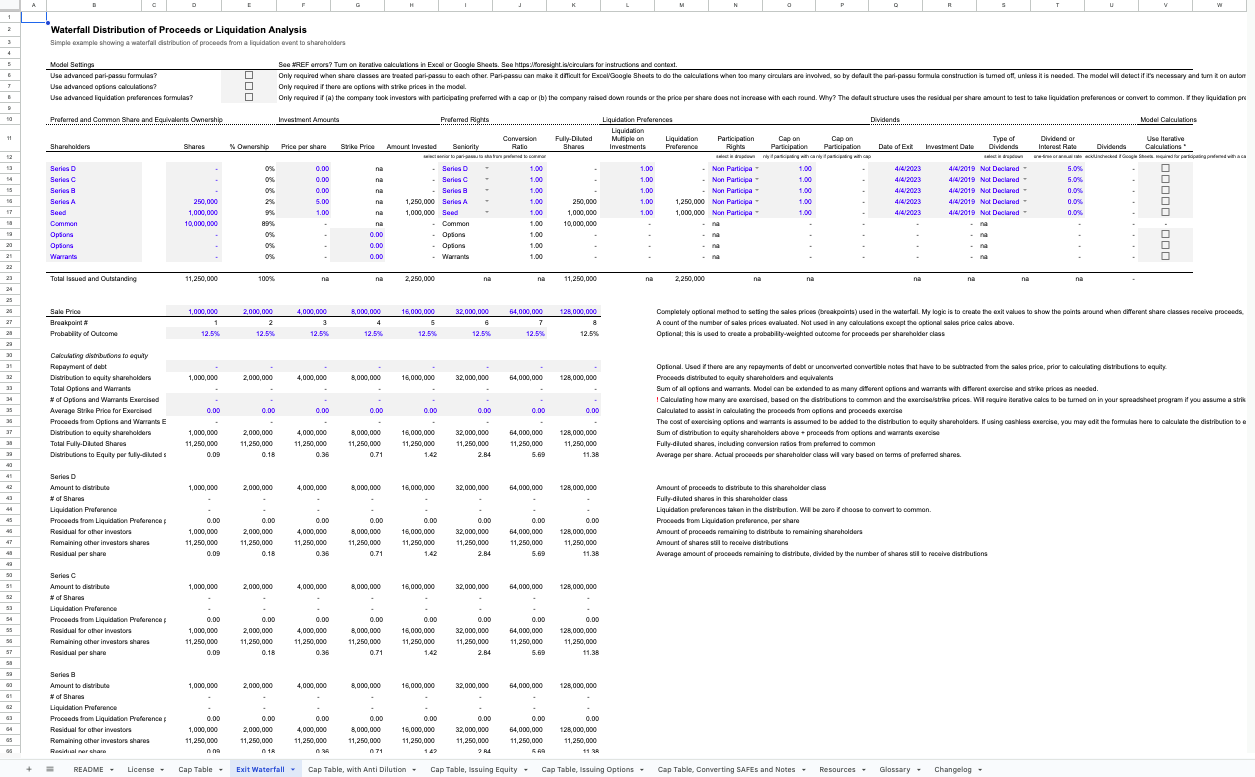

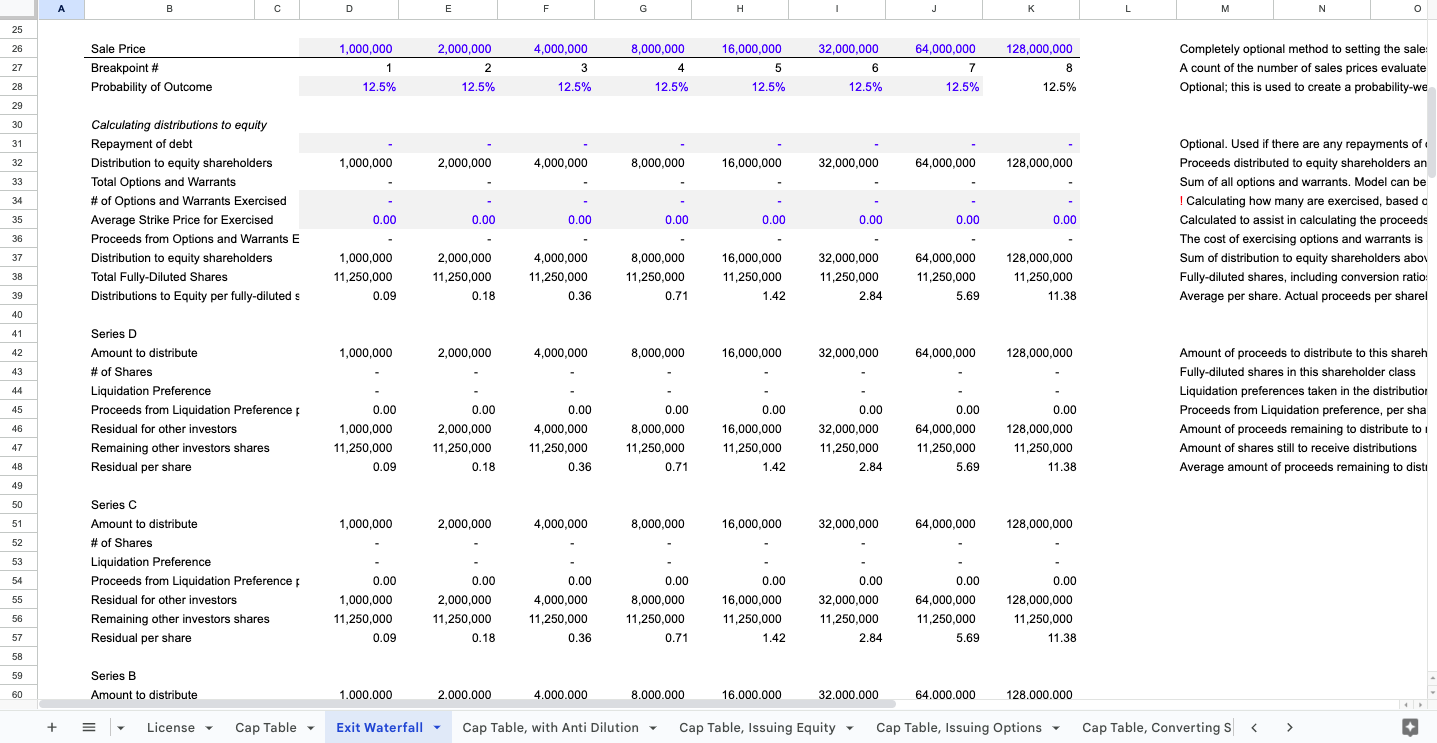

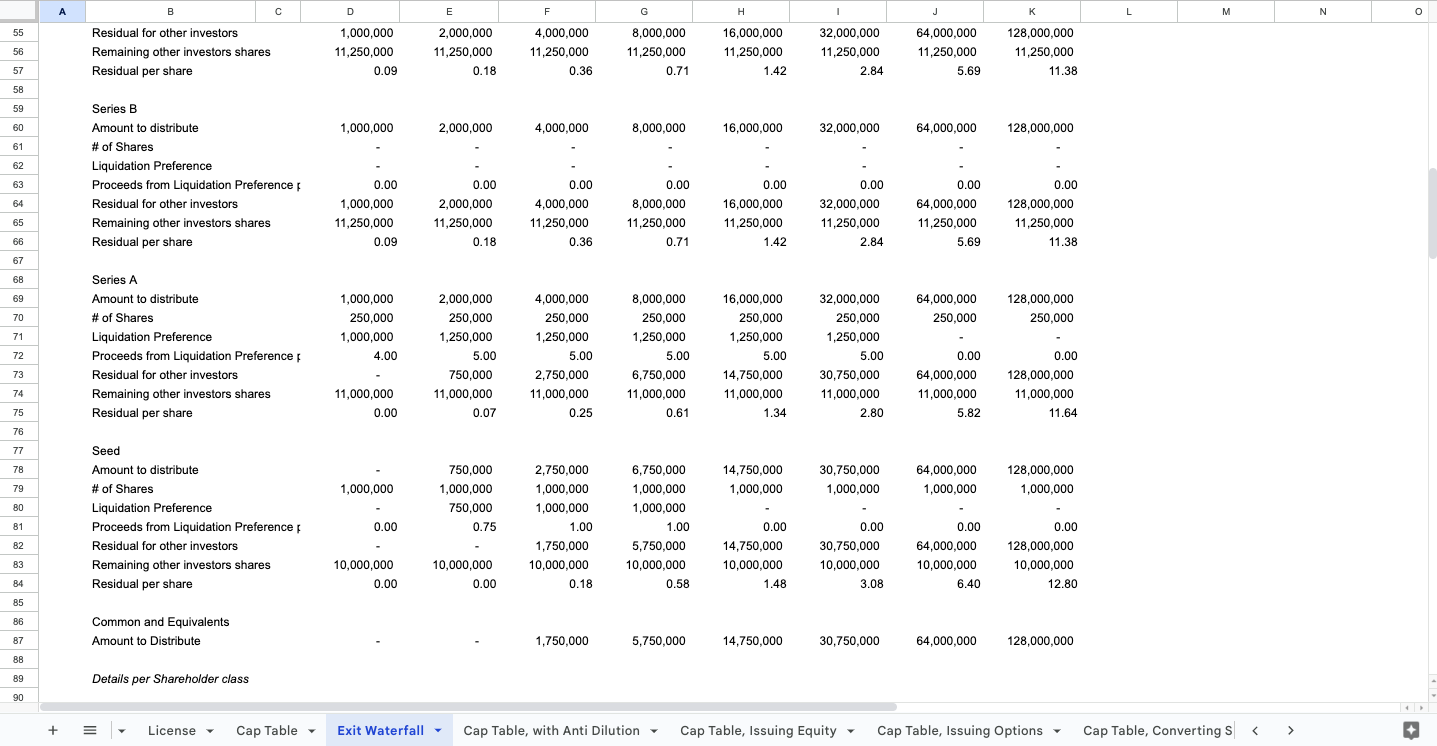

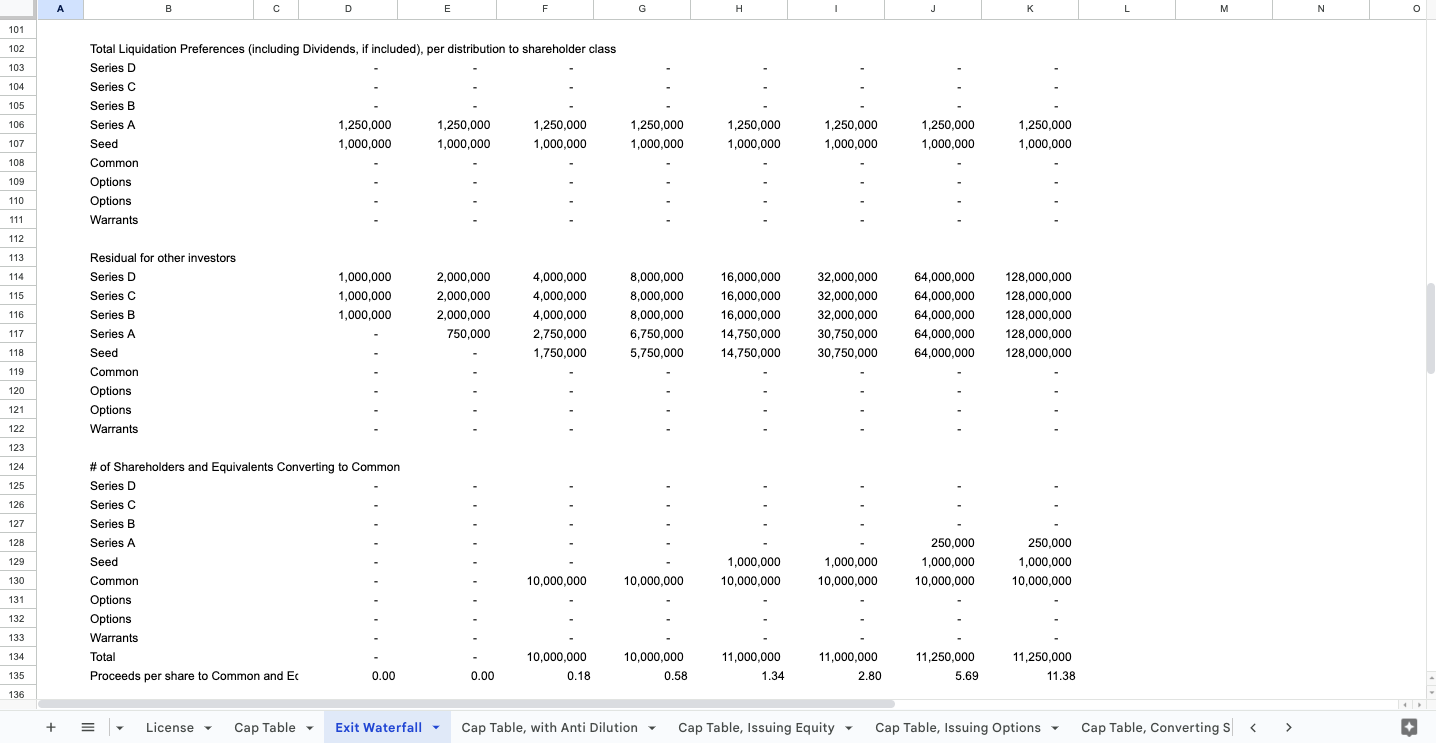

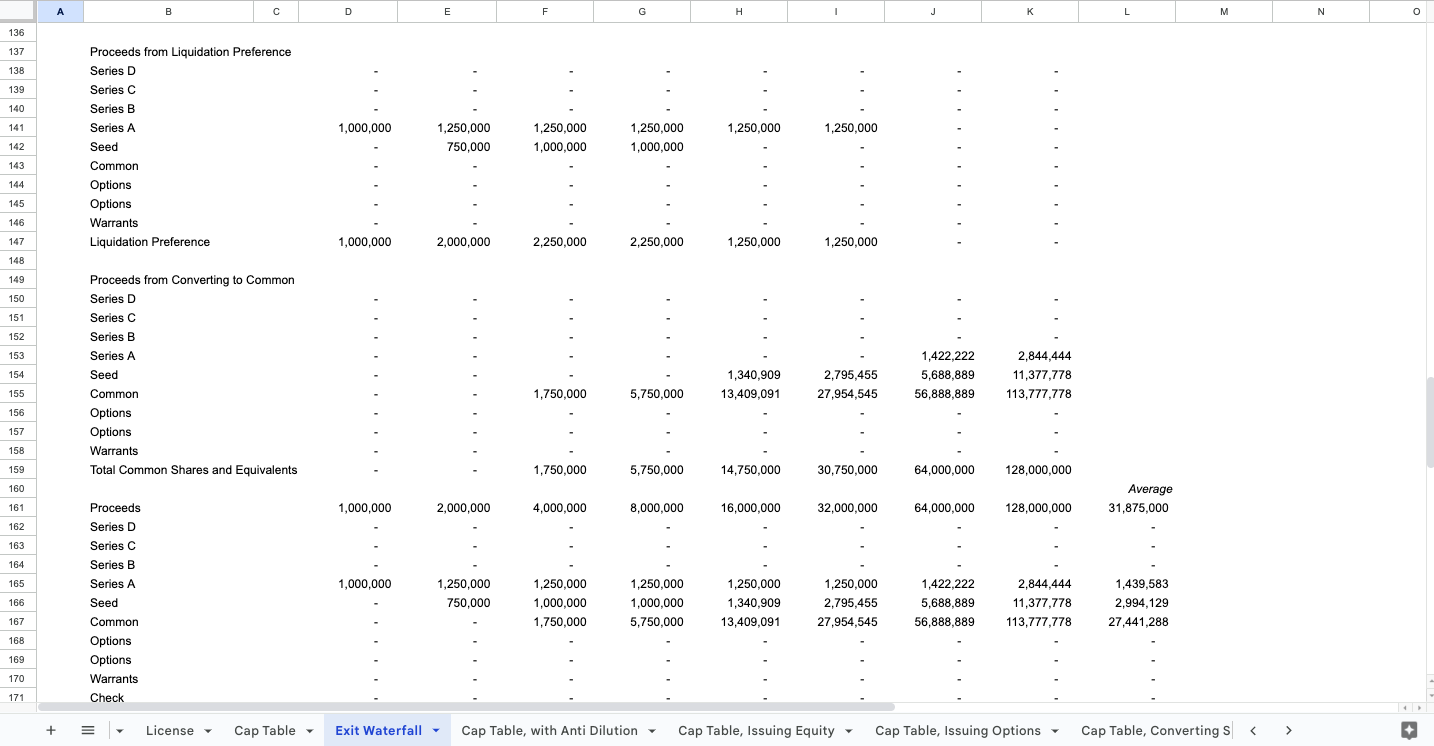

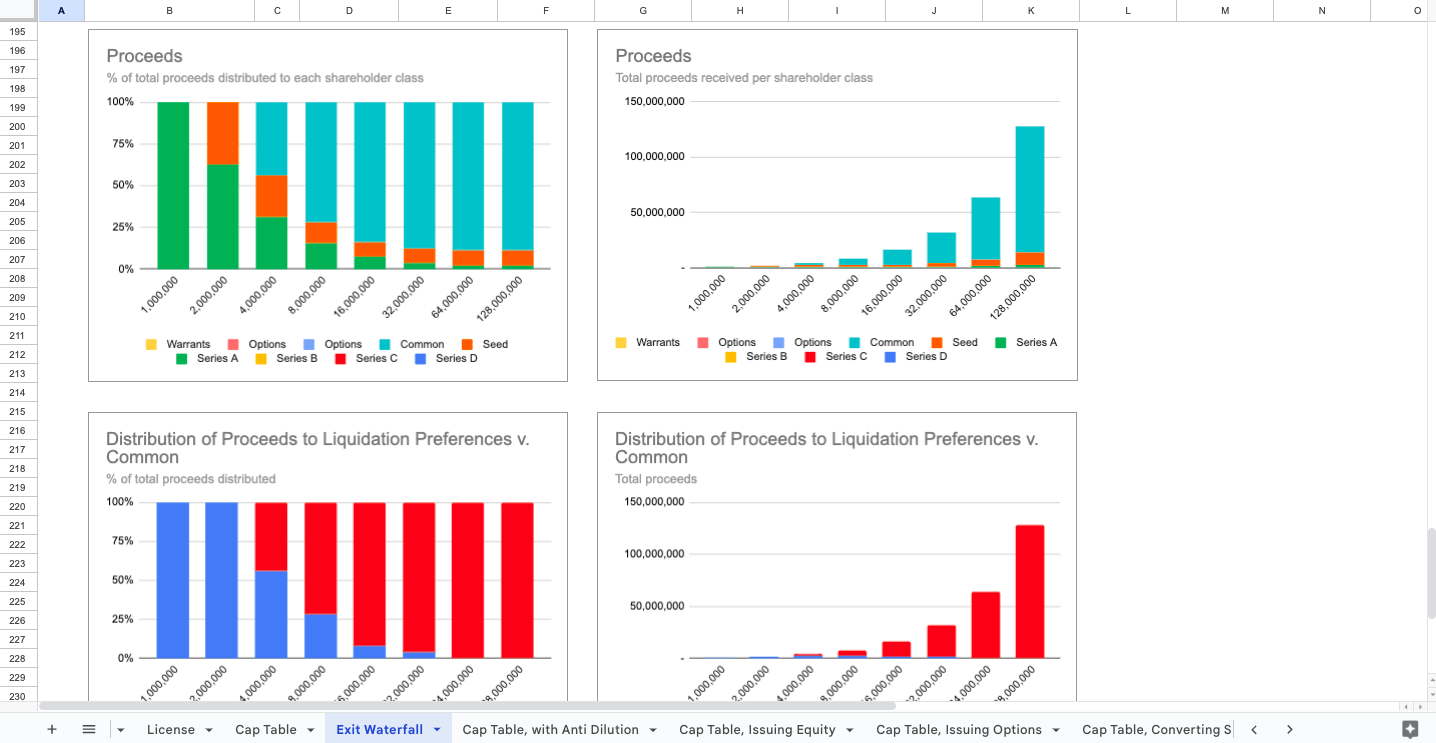

Cap Table and Exit Waterfall Template for Excel and Google Sheets

Cap Table and Exit Waterfall Template for Founders and Investors

Further information

Forecast how rounds of financing impact ownership, valuation, dilution, and exit proceeds. Provide a working cap table and exit waterfall that companies can use across a wide variety of capitalization situations. Provide a set of simpler instructional tools that focus on teaching users how to issue equity rounds and convertible instruments, how to convert convertibles, and how to issue option pools.

Startups raising investment funds through equity, convertible notes, premoney and postmoney SAFEs. Investors looking to value prospective investments.